France Analog Semiconductor Market Report: Trends, Growth and Forecast (2026-2032)

By Type (General-Purpose Analog ICs, Application-Specific Analog ICs), By Product Function (Power Management ICs, Amplifiers & Comparators, Signal Conversion ICs / Data Converters, Interface ICs, RF & Microwave Analog ICs, Others), By End-use Industry (Consumer Electronics, Computing & Data Infrastructure, Telecommunications, Automotive & Transportation, Industrial & Manufacturing, Healthcare & Life Sciences, Aerospace & Defense, Others) ... Read more

|

Major Players

|

France Analog Semiconductor Market Statistics and Insights, 2026

- Market Size Statistics

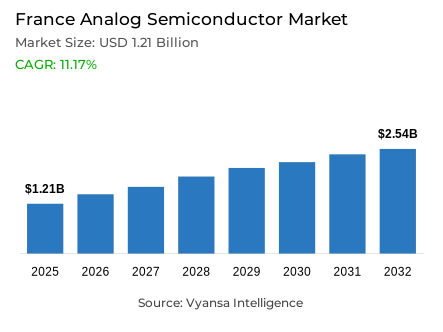

- Analog semiconductor market size in France was valued at USD 1.21 billion in 2025 and is estimated at USD 1.36 billion in 2026.

- The market size is expected to grow to USD 2.54 billion by 2032.

- Market to register a CAGR of around 11.17% during 2026-32.

- Product Function Shares

- Power management ics grabbed market share of 35%.

- Competition

- Analog semiconductor in France is currently being catered to by more than 10 companies.

- Top 5 companies acquired around 30% of the market share in 2026.

- Semiconductor Components Industries L.L.C. (onsemi), Renesas Electronics Corporation, Microchip Technology Inc., STMicroelectronics International N.V., Texas Instruments Incorporated etc., are few of the top companies.

- End-use Industry

- Automotive & transportation grabbed 30% of the market.

France Analog Semiconductor Market Outlook

France analog semiconductor market covers analog integrated circuits, power management ICs, signal conversion ICs, amplifiers, comparators, interface ICs, RF analog ICs, and mixed-signal semiconductors used across automotive electronics, computing infrastructure, telecommunications, industrial automation, healthcare devices, aerospace systems, and consumer electronics. It is valued at USD 1.21 billion in 2025, USD 1.36 billion in 2026, and USD 2.54 billion by 2032, with an 11.17% CAGR during 2026-2032. These devices convert real-world signals into controllable electronic outputs across mission-critical French systems.

Policy direction and connectivity modernization are strengthening the France analog semiconductor market. The European Chips Act targets stronger EU semiconductor supply resilience and reduced external dependency, while France 2030 links connectivity policy to 100% 5G coverage by 2030 and industrial 5G uptake. These priorities expand demand for analog front-end ICs, voltage regulators, ADC and DAC chips, RF front ends, and interface components that support connected factories, smart meters, transport electronics, medical equipment, and telecommunications infrastructure.

Industrial impact is concentrated in localized wafer fabrication, design specialization, and procurement security. France analog semiconductor industry benefits from the Crolles semiconductor hub, Grenoble semiconductor cluster, automotive OEM demand, aerospace electronics, and energy infrastructure projects, creating a supply base where mature-node chips remain commercially essential. For buyers, sourcing visibility improves when suppliers combine high-reliability analog components, design support, qualification capability, distribution reach, and compliance-ready product documentation for French and European electronics manufacturers.

Supplier strategy is moving toward higher-value power efficiency, mixed-signal integration, and automotive-grade reliability. France analog semiconductor market momentum in 2026 is shaped by vehicle electrification, factory automation, renewable-energy integration, and 5G network densification, while France analog semiconductor industry participants are prioritizing application-specific analog ICs, compact power architectures, sensor interface ICs, and local technical support. This trajectory supports more resilient procurement pipelines and raises competitive intensity among integrated device manufacturers, fabless vendors, and specialist distributors.

France Analog Semiconductor Market Growth Driver

Electrification and Embedded Mobility Demand Lift Analog IC Uptake

Vehicle electrification and electronics-heavy platform design are increasing analog IC intensity across French mobility supply chains. Battery management, traction inverter monitoring, zonal power distribution, ADAS sensors, infotainment, and charging interfaces require power management ICs, comparators, amplifiers, data converters, and signal conditioning ICs. This raises design-in opportunities for the France analog semiconductor market because automakers and Tier-1 suppliers need compact, qualified, energy-efficient chips that protect system uptime and meet safety requirements.

ACEA reported that EU battery-electric car registrations reached 1,880,370 units in 2025, capturing 17.4% share, while France posted 12.5% growth among the four largest BEV markets. This supports France analog semiconductor industry demand by expanding semiconductor content per vehicle, improving procurement visibility for automotive-grade power ICs, and strengthening supplier positioning across vehicle power, sensing, charging, and control electronics used in next-generation platforms and fleet electrification programs across domestic OEM qualification cycles, electronics sourcing plans, and platform redesign programs.

France Analog Semiconductor Market Challenge

Capacity Timing and Supply Localization Remain Procurement Constraints

Capacity timing, mature-node availability, and fragmented European investment planning constrain supply assurance for analog chip buyers in France. The France analog semiconductor market depends on wafer fabrication, packaging, testing, and imported upstream materials that cannot be expanded quickly when automotive, telecom, and industrial customers tighten qualification windows. This creates pricing risk, longer design cycles, and constrained vendor flexibility across safety-critical mobility systems, energy infrastructure, and precision industrial automation while narrowing approved replacement options during shortages.

The European Court of Auditors reported in 2025 that achieving the EU target of 20% global microchip production by 2030 is very unlikely. That assessment pressures France analog semiconductor industry participants because localization goals may not translate into timely capacity, forcing procurement teams to maintain multi-source strategies, buffer inventories, qualification alternatives, and distributor-backed supply programs for power ICs, data converters, RF components, interface devices, and sensor interface ICs across longer automotive and industrial redesign cycles.

Unlock Market Intelligence

Explore the market potential with our data-driven report

France Analog Semiconductor Market Trend

5G Densification Pushes RF and Mixed-Signal Integration

5G network densification and industrial connectivity are shifting analog chip demand toward RF front ends, low-noise amplifiers, filters, interface ICs, and high-efficiency power regulation. The France analog semiconductor market gains from this transition because telecom equipment, connected factories, transport corridors, and IoT devices require stable signal conversion and power control at the edge. This strengthens demand for mixed-signal semiconductors across distributed infrastructure. It also improves demand visibility for analog chip vendors serving French telecom integrators.

ANFR reported that, as of 1 June 2026, 55,365 5G sites were authorized in France and 49,004 were technically operational. This deployment trend supports France analog semiconductor industry adoption by expanding RF analog IC requirements, increasing procurement for telecom-grade power components, and encouraging suppliers to localize technical support around network equipment, connected sensors, and low-power edge devices across equipment refresh cycles, private 5G projects, spectrum-efficient radios, and industrial IoT gateways and maintenance planning.

France Analog Semiconductor Market Opportunity

Renewable Power Systems Create High-Value Power IC Openings

Renewable energy integration creates a high-value opening for suppliers of power ICs, voltage regulators, isolation components, battery management ICs, and precision monitoring devices. The France analog semiconductor market can capture higher demand from solar inverters, grid equipment, smart meters, EV charging, and building-energy systems because these applications require efficient conversion, thermal control, and sensor accuracy. Distribution partners gain leverage when they offer design assistance for energy projects and verified sourcing for rugged power architectures.

RTE data shows mainland France reached 30.4 GW of cumulative solar capacity at end-2025 after adding 5.9 GW during the year. This strengthens France analog semiconductor industry opportunities by expanding demand for power conversion ICs, analog front-end ICs, and protection components used in distributed energy assets, while improving supplier access to utilities, inverter makers, charging-equipment manufacturers, and industrial energy-management integrators. This improves demand capture for analog chip vendors with qualified portfolios, application engineering, and channel coverage.

Unlock Market Intelligence

Explore the market potential with our data-driven report

France Analog Semiconductor Market Segmentation Analysis

By Product Function

- Power Management ICs

- Amplifiers & Comparators

- Signal Conversion ICs / Data Converters

- Interface ICs

- RF & Microwave Analog ICs

- Others

Power management ICs lead product function with 35% share because French electronics manufacturers are prioritizing voltage regulation, battery management, thermal protection, and energy efficiency across vehicles, factories, telecom equipment, medical devices, and renewable-energy systems. Within the France analog semiconductor market, this segment benefits from broad design reuse, high component density per system, and recurring qualification demand across both general-purpose analog ICs and application-specific analog ICs especially where power efficiency affects uptime and component qualification.

Infineon introduced the OPTIREG TLF35585 power management IC in February 2025 for demanding automotive applications, integrating efficient voltage regulation with monitoring and control functions for safety-related ECUs. This product direction supports procurement momentum for automotive-grade power management ICs, raises specification expectations, and strengthens pricing resilience for suppliers serving high-compliance French mobility and industrial electronics programs as OEMs shift from board-level discrete power designs toward integrated, monitored, and thermally optimized analog power architectures under longer validation cycles.

By End-use Industry

- Consumer Electronics

- Computing & Data Infrastructure

- Telecommunications

- Automotive & Transportation

- Industrial & Manufacturing

- Healthcare & Life Sciences

- Aerospace & Defense

- Others

Automotive and transportation hold 30% share under end-use industry because French vehicle platforms are absorbing more analog content through electrification, sensing, lighting, charging, connectivity, and power distribution. The segment influences the France analog semiconductor market through long qualification cycles, higher reliability thresholds, and multi-year component sourcing programs. Demand is reinforced by OEM and Tier-1 needs for battery management ICs, sensor interface ICs, comparators, and automotive-grade power ICs and fleet electrification roadmaps across domestic automakers and suppliers.

STMicroelectronics highlights a smart battery-management front-end IC with synchronized monitoring and ASIL-D-ready safety features for smart mobility applications. This supports end-use adoption by showing how analog semiconductor suppliers are aligning product specifications with vehicle safety, battery accuracy, and energy-efficiency requirements, improving competitive positioning for vendors that can provide automotive documentation, design support, and production continuity to French mobility supply chains across vehicle platforms where safety diagnostics conversion efficiency and supply continuity influence supplier selection.

List of Companies Covered in France Analog Semiconductor Market

The companies listed below are highly influential in the France analog semiconductor market, with a significant market share and a strong impact on industry developments.

- Semiconductor Components Industries L.L.C. (onsemi)

- Renesas Electronics Corporation

- Microchip Technology Inc.

- STMicroelectronics International N.V.

- Texas Instruments Incorporated

- Analog Devices Inc.

- Infineon Technologies AG

- NXP B.V.

- Skyworks Solutions Inc.

- Qorvo Inc.

Market News & Updates

- STMicroelectronics International N.V., 2025:

STMicroelectronics introduced silicon photonics and next-generation BiCMOS technologies for high-performance cloud optical interconnects. The company stated that both technologies are being industrialized and manufactured at its 300mm Crolles fab in France. The update supports France-based production of advanced mixed-signal semiconductor technologies used in AI clusters and optical connectivity systems.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- France Analog Semiconductor Market Policies, Regulations, and Standards

- France Analog Semiconductor Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- France Analog Semiconductor Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Type

- General-Purpose Analog ICs- Market Insights and Forecast 2022-2032, USD Million

- Application-Specific Analog ICs- Market Insights and Forecast 2022-2032, USD Million

- By Product Function

- Power Management ICs- Market Insights and Forecast 2022-2032, USD Million

- Amplifiers & Comparators- Market Insights and Forecast 2022-2032, USD Million

- Signal Conversion ICs / Data Converters- Market Insights and Forecast 2022-2032, USD Million

- Interface ICs- Market Insights and Forecast 2022-2032, USD Million

- RF & Microwave Analog ICs- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By End-use Industry

- Consumer Electronics- Market Insights and Forecast 2022-2032, USD Million

- Computing & Data Infrastructure- Market Insights and Forecast 2022-2032, USD Million

- Telecommunications- Market Insights and Forecast 2022-2032, USD Million

- Automotive & Transportation- Market Insights and Forecast 2022-2032, USD Million

- Industrial & Manufacturing- Market Insights and Forecast 2022-2032, USD Million

- Healthcare & Life Sciences- Market Insights and Forecast 2022-2032, USD Million

- Aerospace & Defense- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Type

- Market Size & Growth Outlook

- France General-Purpose Analog ICs Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Product Function- Market Insights and Forecast 2022-2032, USD Million

- By End-use Industry- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- France Application-Specific Analog ICs Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Product Function- Market Insights and Forecast 2022-2032, USD Million

- By End-use Industry- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- STMicroelectronics International N.V.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Texas Instruments Incorporated

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Analog Devices Inc.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Infineon Technologies AG

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- NXP B.V.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Semiconductor Components Industries L.L.C. (onsemi)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Renesas Electronics Corporation

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Microchip Technology Inc.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Skyworks Solutions, Inc.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Qorvo Inc.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- STMicroelectronics International N.V.

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Type |

|

| By Product Function |

|

| By End-use Industry |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.