France Alcoholic Drinks Market Report: Trends, Growth and Forecast (2026-2032)

By Type (Beer, Cider/Perry, RTDs, Spirits, Wine), By Alcohol Content (High, Medium, Low), By Flavor (Unflavored, Flavored), By Packaging Type (Glass Bottles, Tins, Plastic Bottles, Others), By Sales Channel (On-Trade, Off-Trade (Retail Offline, Retail Online)) ... Read more

|

Major Players

|

France Alcoholic Drinks Market Statistics and Insights, 2026

- Market Size Statistics

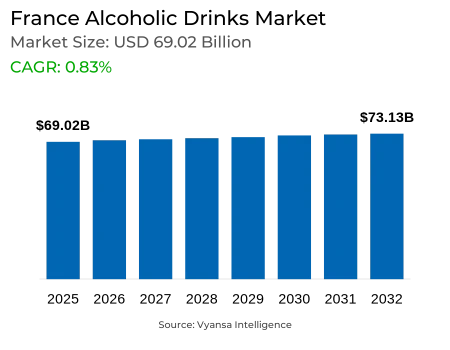

- Alcoholic Drinks in France is estimated at $ 69.02 Billion.

- The market size is expected to grow to $ 73.13 Billion by 2032.

- Market to register a CAGR of around 0.83% during 2026-32.

- Type Shares

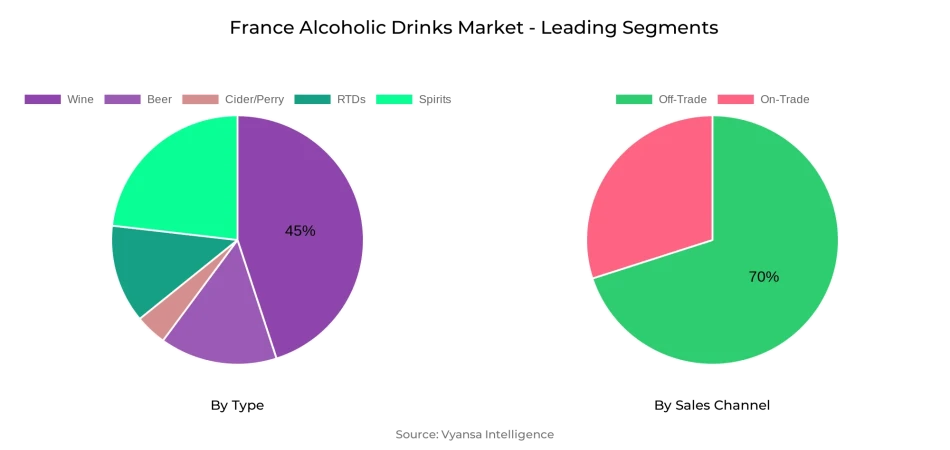

- Wine grabbed market share of 45%.

- Competition

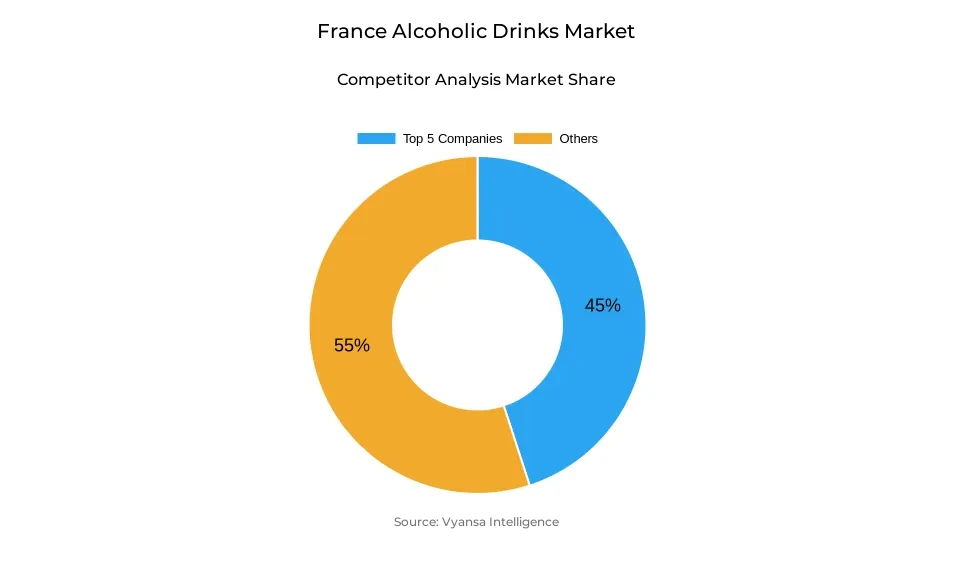

- More than 10 companies are actively engaged in producing Alcoholic Drinks in France.

- Top 5 companies acquired 45% of the market share.

- Pernod Ricard Groupe, Grands Chais de France SA, Les, Union In Vivo Sca, Heineken NV, Carlsberg A/S etc., are few of the top companies.

- Sales Channel

- Off-Trade grabbed 70% of the market.

France Alcoholic Drinks Market Outlook

French Alcoholic Drinks Market was valued at USD 69.02 billion and is expected to grow to USD 73.13 billion by 2032. Though volume sales declined in 2025, value sales increased, mostly influenced by inflation and price hikes across many categories. Regardless of continuous economic and political difficulties, the industry has remained resilient as consumers increasingly focus on quality over quantity. This change is especially seen among millennials, who are embracing more responsible drinking practices. Further, events like the Paris Olympic Games facilitated on-trade channel growth by increasing tourism and social events.

Off-trade channels are in control of the French alcoholic beverages market, with a share of almost 70% of total sales. Customers favor supermarkets, hypermarkets, and specialist shops, driven by their convenience and value for money. Meanwhile, on-trade sales are also picking up pace with the revival of tourism, restaurants, and nightlife. Nevertheless, a clear change in end users trend indicates the increasing demand for smaller pack sizes and de-premiumization, with most households still living within budgeted expenses.

In the future, the market is set to experience a volume decrease in consumption thanks to increasing health consciousness and changing demographics. Meanwhile, value sales are projected to hold steady with the boost from innovation and premiumization. The growing popularity of no- and low-alcohol (nolo) drinks is changing the competitive scenario, particularly among young end users. Hybrid innovation and environmentally friendly production are also on the rise, attracting consumers who are interested in authenticity, transparency, and quality.

The French alcoholic beverages market overall has excellent prospects for long-term stability. Expansion will be driven by premium craft spirits, re-emerging cocktail culture, and the growth of the no/low alcohol category, while the off-trade channels will remain instrumental in driving future trends.

France Alcoholic Drinks Market Growth Driver

Increasing end users' Health Awareness

Growing health consciousness among end users is shaping the expansion of the French Alcoholic Drinks Market. Increasing, end users are opting consciously to regulate alcohol consumption as a result of health concerns as well as the desire for sustained wellness. This leads to a shift towards naturally made lower-alcohol and no-alcohol drinks, since end users look for alternatives that are in harmony with healthier lifestyles without eliminating social drinking altogether.

They are reacting by increasing non-and low-alcohol ranges, launching new products with improved nutritional benefits and lower alcohol levels. Mindful drinking campaigns, as well as schemes such as Dry January, further underpin end users interest in moderation. This increased health awareness drives market growth by providing new product opportunities and increasing the attractiveness of alcoholic beverages to a more health-aware end users base.

France Alcoholic Drinks Market Trend

Mindful Drinking and Quality Focus

End users in French are increasingly prioritising quality over quantity, leading to a greater focus on mindful drinking in the alcoholic beverages segment. Millennials and younger end users cut back on alcohol but crave premium experiences, hence a desire for well-developed, higher-quality drinks. This shift drives consumption habits within beer, wine, and spirits, with moderation as the key focus.

The market reacts by developing products that appeal to selective and health-conscious end users, focusing on taste, craftsmanship, and premium positioning. End users become more selective, preferring drinks that provide distinctive flavors or value, while cutting back on overall consumption. This trend is reshaping conventional market forms and prompting manufacturers to match offerings with changing tastes.

Unlock Market Intelligence

Explore the market potential with our data-driven report

France Alcoholic Drinks Market Opportunity

Innovation in Hybrid and Sustainable Products

French Alcoholic Drinks Market for alcohol will gain from opportunities in hybrid and sustainable product innovation. Manufacturers are likely to introduce the products that blend categories, e.g., beer-cider hybrids and Ready-to-Drink products based on wine, developing new consumption experiences. These innovations will appeal to end users looking for novelty and variety.

Sustainability and transparency of production will increasingly drive opportunities, resonating with millennials and Gen Z who are most interested in storytelling of environmental and human dimensions of wine production. With emphasis on green processes and innovative product ideas, the industry can differentiate and capture premium segments. These strategies are expected to drive growth and bring end users participation in the years to come.

Unlock Market Intelligence

Explore the market potential with our data-driven report

France Alcoholic Drinks Market Segmentation Analysis

By Type

- Beer

- Cider/Perry

- RTDs

- Spirits

- Wine

The segment with highest market share under Type segment is Wine, with 45% market share. Wine remains France strongest-selling product because of its cultural importance and prevalence of consumption, even in the face of threats from inflation and reduced end users confidence. While premium products like Champagne and cognac declined in 2024, cheaper wines, including small- and medium-sized bag-in-box sizes, gained traction.

End users are increasingly opting for value-for-money products while continuing to express interest in flavoured and innovative wines. Ready-to-drink wines (RTDs) based on wine also continue to have a strong presence, with volume share being contributed by brands such as Maison Le Star. This indicates that wine, in both heritage and hybrid forms, continues to be the most resistant and highly consumed alcohol drink category in France.

By Sales Channel

- On-Trade

- Off-Trade

The segment with highest market share under Sales channel is Off-Trade, and it holds a 70% market share. Off-Trade continues to be the choice for French end users because of the convenience, variety, and accessibility provided by supermarkets, hypermarkets, and specialist stores. end users still prefer buying wines, beers, and spirits from these stores, especially when price promotion, reduced packaging, and bundles are offered.

While on-trade sales bounced back in 2024 after COVID-19 restrictions were lifted and the Paris Olympics, off-trade remains dominant because it is both affordable and accessible in urban as well as rural regions. Retailers also updated their offerings according to shifting end users tastes with added curated choices, wine festivals, and hybrid products, further reinforcing off-trade's grip on the French Alcoholic Drinks Market .

Top Companies in France Alcoholic Drinks Market

The top companies operating in the market include Pernod Ricard Groupe, Grands Chais de France SA, Les, Union In Vivo Sca, Heineken NV, Carlsberg A/S, Castel Groupe, Anheuser-Busch InBev NV, La Martiniquaise SVS, Brasserie De Saint-Omer, Advini SA, etc., are the top players operating in the France Alcoholic Drinks Market.

Frequently Asked Questions

Related Report

1. Market Segmentation

1.1. Research Scope

1.2. Research Methodology

1.3. Definitions and Assumptions

2. Executive Summary

3. France Alcoholic Drinks Market Policies, Regulations, and Standards

4. France Alcoholic Drinks Market Dynamics

4.1. Growth Factors

4.2. Challenges

4.3. Trends

4.4. Opportunities

5. France Alcoholic Drinks Market Statistics, 2022-2032F

5.1. Market Size & Growth Outlook

5.1.1. By Revenues in US$ Million

5.1.2. By Quantity Sold in Million Litres

5.2. Market Segmentation & Growth Outlook

5.2.1. By Type

5.2.1.1. Beer- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2. Cider/Perry- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3. RTDs- Market Insights and Forecast 2022-2032, USD Million

5.2.1.4. Spirits- Market Insights and Forecast 2022-2032, USD Million

5.2.1.5. Wine- Market Insights and Forecast 2022-2032, USD Million

5.2.2. By Alcohol Content

5.2.2.1. High- Market Insights and Forecast 2022-2032, USD Million

5.2.2.2. Medium- Market Insights and Forecast 2022-2032, USD Million

5.2.2.3. Low- Market Insights and Forecast 2022-2032, USD Million

5.2.3. By Flavor

5.2.3.1. Unflavored- Market Insights and Forecast 2022-2032, USD Million

5.2.3.2. Flavored- Market Insights and Forecast 2022-2032, USD Million

5.2.4. By Packaging Type

5.2.4.1. Glass Bottles- Market Insights and Forecast 2022-2032, USD Million

5.2.4.2. Tins- Market Insights and Forecast 2022-2032, USD Million

5.2.4.3. Plastic Bottles- Market Insights and Forecast 2022-2032, USD Million

5.2.4.4. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.5. By Sales Channel

5.2.5.1. On-Trade- Market Insights and Forecast 2022-2032, USD Million

5.2.5.2. Off-Trade- Market Insights and Forecast 2022-2032, USD Million

5.2.5.2.1. Retail Offline- Market Insights and Forecast 2022-2032, USD Million

5.2.5.2.2. Retail Online- Market Insights and Forecast 2022-2032, USD Million

5.2.6. By Competitors

5.2.6.1. Competition Characteristics

5.2.6.2. Market Share & Analysis

6. France Beer Market Statistics, 2022-2032F

6.1. Market Size & Growth Outlook

6.1.1. By Revenues in US$ Million

6.1.2. By Quantity Sold in Million Litres

6.2. Market Segmentation & Growth Outlook

6.2.1. By Alcohol Content- Market Insights and Forecast 2022-2032, USD Million

6.2.2. By Flavor- Market Insights and Forecast 2022-2032, USD Million

6.2.3. By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

6.2.4. By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

7. France Cider/Perry Market Statistics, 2022-2032F

7.1. Market Size & Growth Outlook

7.1.1. By Revenues in US$ Million

7.1.2. By Quantity Sold in Million Litres

7.2. Market Segmentation & Growth Outlook

7.2.1. By Alcohol Content- Market Insights and Forecast 2022-2032, USD Million

7.2.2. By Flavor- Market Insights and Forecast 2022-2032, USD Million

7.2.3. By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

7.2.4. By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

8. France Ready-to-Drink Market Statistics, 2022-2032F

8.1. Market Size & Growth Outlook

8.1.1. By Revenues in US$ Million

8.1.2. By Quantity Sold in Million Litres

8.2. Market Segmentation & Growth Outlook

8.2.1. By Alcohol Content- Market Insights and Forecast 2022-2032, USD Million

8.2.2. By Flavor- Market Insights and Forecast 2022-2032, USD Million

8.2.3. By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

8.2.4. By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

9. France Spirits Market Statistics, 2022-2032F

9.1. Market Size & Growth Outlook

9.1.1. By Revenues in US$ Million

9.1.2. By Quantity Sold in Million Litres

9.2. Market Segmentation & Growth Outlook

9.2.1. By Alcohol Content- Market Insights and Forecast 2022-2032, USD Million

9.2.2. By Flavor- Market Insights and Forecast 2022-2032, USD Million

9.2.3. By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

9.2.4. By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

10. France Wine Market Statistics, 2022-2032F

10.1.Market Size & Growth Outlook

10.1.1. By Revenues in US$ Million

10.1.2. By Quantity Sold in Million Litres

10.2.Market Segmentation & Growth Outlook

10.2.1. By Alcohol Content- Market Insights and Forecast 2022-2032, USD Million

10.2.2. By Flavor- Market Insights and Forecast 2022-2032, USD Million

10.2.3. By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

10.2.4. By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

11. Competitive Outlook

11.1.Company Profiles

11.1.1. Heineken NV

11.1.1.1. Business Description

11.1.1.2. Product Portfolio

11.1.1.3. Collaborations & Alliances

11.1.1.4. Recent Developments

11.1.1.5. Financial Details

11.1.1.6. Others

11.1.2. Carlsberg A/S

11.1.2.1. Business Description

11.1.2.2. Product Portfolio

11.1.2.3. Collaborations & Alliances

11.1.2.4. Recent Developments

11.1.2.5. Financial Details

11.1.2.6. Others

11.1.3. Castel Groupe

11.1.3.1. Business Description

11.1.3.2. Product Portfolio

11.1.3.3. Collaborations & Alliances

11.1.3.4. Recent Developments

11.1.3.5. Financial Details

11.1.3.6. Others

11.1.4. Anheuser-Busch InBev NV

11.1.4.1. Business Description

11.1.4.2. Product Portfolio

11.1.4.3. Collaborations & Alliances

11.1.4.4. Recent Developments

11.1.4.5. Financial Details

11.1.4.6. Others

11.1.5. La Martiniquaise SVS

11.1.5.1. Business Description

11.1.5.2. Product Portfolio

11.1.5.3. Collaborations & Alliances

11.1.5.4. Recent Developments

11.1.5.5. Financial Details

11.1.5.6. Others

11.1.6. Pernod Ricard Groupe

11.1.6.1. Business Description

11.1.6.2. Product Portfolio

11.1.6.3. Collaborations & Alliances

11.1.6.4. Recent Developments

11.1.6.5. Financial Details

11.1.6.6. Others

11.1.7. Grands Chais de France SA, Les

11.1.7.1. Business Description

11.1.7.2. Product Portfolio

11.1.7.3. Collaborations & Alliances

11.1.7.4. Recent Developments

11.1.7.5. Financial Details

11.1.7.6. Others

11.1.8. Union In Vivo Sca

11.1.8.1. Business Description

11.1.8.2. Product Portfolio

11.1.8.3. Collaborations & Alliances

11.1.8.4. Recent Developments

11.1.8.5. Financial Details

11.1.8.6. Others

11.1.9. Brasserie De Saint-Omer

11.1.9.1. Business Description

11.1.9.2. Product Portfolio

11.1.9.3. Collaborations & Alliances

11.1.9.4. Recent Developments

11.1.9.5. Financial Details

11.1.9.6. Others

11.1.10. Advini SA

11.1.10.1. Business Description

11.1.10.2. Product Portfolio

11.1.10.3. Collaborations & Alliances

11.1.10.4. Recent Developments

11.1.10.5. Financial Details

11.1.10.6. Others

12. Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Type |

|

| By Alcohol Content |

|

| By Flavor |

|

| By Packaging Type |

|

| By Sales Channel |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.