Finland Plant-Based Dairy Market Report: Trends, Growth and Forecast (2026-2032)

Product Type (Plant-Based Milk (Soy Drinks, Almond, Blends, Coconut, Oat, Rice, Other Plant-Based Milk), Plant-Based Yoghurt, Plant-Based Cheese), Sales Channel (Retail Offline (Grocery Retailers, Convenience Retailers, Supermarkets, Hypermarkets), Retail Online) ... Read more

|

Major Players

|

Finland Plant-Based Dairy Market Statistics and Insights, 2026

- Market Size Statistics

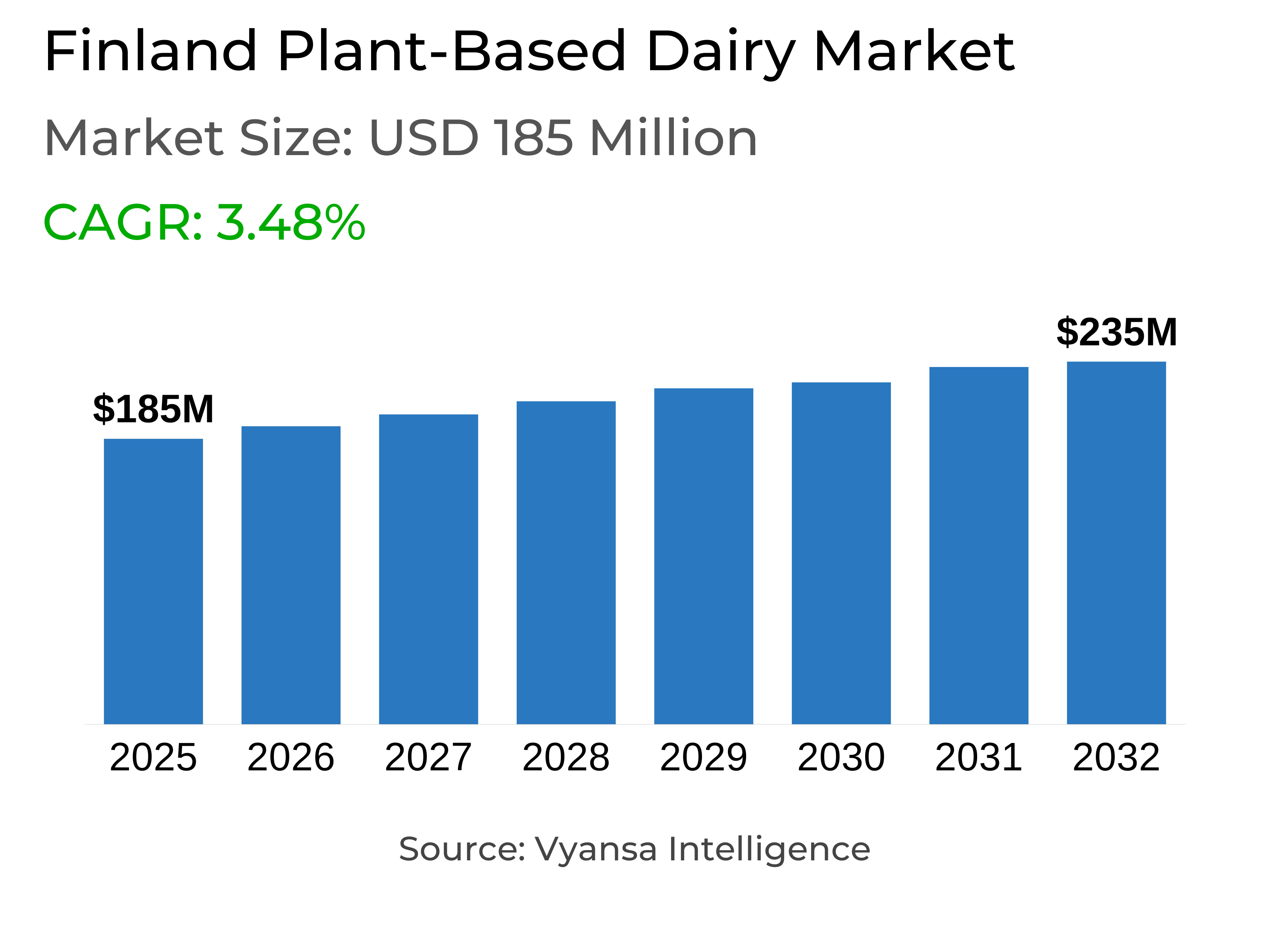

- Plant-based dairy in finland is estimated at USD 185 million.

- The market size is expected to grow to USD 235 million by 2032.

- Market to register a cagr of around 3.48% during 2026-32.

- Product Type Shares

- Plant-based milk grabbed market share of 65%.

- Competition

- More than 10 companies are actively engaged in producing plant-based dairy in finland.

- Top 5 companies acquired around 70% of the market share.

- Kesko Oyj, Raisio Oyj, Juustoportti Oy, Valio Oy, Oatly AB etc., are few of the top companies.

- Sales Channel

- Retail offline grabbed 95% of the market.

Finland Plant-Based Dairy Market Outlook

The Finland plant-based dairy market will continue to follow its growth pattern during the forecast period. Estimated to be $185 million in 2025, the market will expand to $235 million by 2032 due to increasing end-users' demand for sustainable, nutritious, and vegan-friendly products. Plant-based milks, led by oat-based ones, will remain the most dynamic segment due to its local heritage, nutritional profile, and use as part of everyday life, such as with coffee and in cooking.

top 5 players command a market share of around 70% with key players like Valio Oy are expanding portfolios with product innovation, strategic acquisitions, and increased production capacities. Brands are introducing fortified, protein-fortified, and premium plant-based substitutes, while private label ranges are dynamic, offering value-for-money, high-quality products appealing to price-sensitive and quality-driven end users.

Retail Offline is the predominant distribution of sales, around 95% of the activity happening there. Hypermarkets dominate due to their large assortments, convenience, and regular promotion campaigns. Retail online is on the rising path, as bolstered by better distribution systems, click-and-collect deals, and enticing online assortments, though remaining the less contributing part of the total stores.

Health and sustainability trends will lead growth in the future. End users increasingly seek products that utilize local, ethically sourced ingredients and sustainable production practices. Brands are responding by delivering recyclable packaging, reduced carbon footprints, and green manufacturing practices. Future innovation through taste, texture, and nutritional content will further fuel the appeal of plant-based dairy to progressively broader audiences of health- and climate-conscious Finland end users.

Finland Plant-Based Dairy Market Growth DriverHealth and Wellness Trends Propelling Plant-Based Dairy Growth

The growth of end users interest in health, nutrition, and wellness is driving Finland plant-based dairy market. Finland end users are embracing plant-based foods as a component of healthier diets, aiming to reduce saturated fat intake while incorporating functional nutrients such as vitamins D, B12, riboflavin, and calcium. Fortified oat drinks and barista-style beverages have grown particularly well-liked with their nutritional content alongside convenience and functional value for coffee, cooking, and smoothies. New flavors, combined with convenience and functional value, help to engage a wide category of end users seeking indulgence and wellness in everyday use.

The broader health-conscious trend is driving trial of various plant-based formats, including low-sugar yogurts, dessert-like protein products, and fortified beverages. End users increasingly want functional nutrition, well-balanced diets, and ingredient transparency when selecting plant-based dairy products. Health and wellness consciousness keeps driving category growth, positioning plant-based dairy at the forefront of Finland's shifting food culture and converting new end users seeking healthier, more nutrient-enriched alternatives.

Finland Plant-Based Dairy Market TrendChanging end users Preferences and Dynamic Dietary Trends

End users preferences in Finland are shifting towards plant-based milk alternatives that address health, indulgence, and convenience. Oat-based drinks continue to be at the forefront, driven by their Nordic superfood positioning and popularity among vegans as well as health-conscious non-vegans. New introductions such as Oatly iKaffe Vanilla and Caramel, fortified with vitamins D, B12, riboflavin, and calcium, demonstrate end users higher desire for functional products to aid health in addition to rich taste. The launches demonstrate that Finland end userss are looking more and more for products that are able to satisfy more than one lifestyle requirement simultaneously, incorporating plant-based living, nutritional benefit, and taste satisfaction.

Beyond beverages, end users are exploring new forms such as plant-based desserts and snack drinks, which signal interest and receptiveness to experimenting with various product forms. Foods as Valio Oddlygood Dessert Dreamy Vanilla and Elovena Proteiinivanukas Mokkapala answer this trend with decadent, protein-rich, and convenient options. The growing uptake of these innovations indicates a clear trajectory: Finland end users are increasing plant-based food option choices and increasingly integrating these alternatives into everyday routines, driving category diversification and market growth.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Finland Plant-Based Dairy Market OpportunitySustainability Initiatives Driving Future Market Growth

The growing emphasis on sustainability in Finland’s plant-based dairy market enables companies to strengthen brand differentiation and attract environmentally conscious end users. Local origin, carbon footprint, and eco-friendly packaging are increasingly emerging as purchasing drivers. Fazer Aito, for example, bases its position on Nordic oats and recyclable pack, while Elovena roots itself in carbon-neutral energy and Finland sourcing, delivering strong end users resonance and establishing trust in plant-based alternatives.

Future expansion is expected through more intense embedding of sustainability strategies across product development, ingredients, and packaging. Brands which convey environmentally meaningful benefits with functional and health-based product features will tend to appeal to a larger group, including non-vegetarians who want climate-friendly options. By embedding sustainability into the value proposition at its core, companies can foster loyalty, differentiation from the competition, and set themselves up for long-term growth as Finland end users increasingly prioritize environmentally sustainable consumption.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Finland Plant-Based Dairy Market Segmentation Analysis

By Product Type

- Plant-Based Milk

- Plant-Based Yoghurt

- Plant-Based Cheese

The segment with highest market share under Product Type is plant milk with a share of around 65% in Finland plant dairy market. Oat variants remain the most dynamic, appreciated for being indigenous, mild-tasting, and versatile for coffee, cooking, and everyday use. Nutrient-enriched with vitamin D, riboflavin, B12, and calcium, such drinks are attractive to healthy end userx as well as vegan and environmentally friendly lifestyles.

Other plant-based milk brands have reinforced total growth by pushing innovation in flavour and formats, including barista-style and single-serve snack formats. Increased availability in supermarkets and hypermarkets, combined with competitive pricing and promotions, continues to be fundamental to driving the dominance of plant-based milk, the leading segment dictating the Finland plant-based dairy market.

By Sales Channel

- Retail Offline

- Retail Online

The segment with highest market share under Sales Channel is retail offline with about a 95% market share of the Finland plant-based dairy market. Hypermarkets are the most accessed channel, offering convenience for weekly grocery buying and extensive product range, such as private label, premium, and organic plant-based options. Special offers and in-store promotions also support purchasing, particularly among price-sensitive end users.

Supermarkets also contribute to retail offline domination by ensuring excellent shelf presence and varied selections suitable for various end users tastes. Though retail online is growing due to convenience, expanded distribution networks, and web-based access to promotions, retail offline remains the primary channel for Finland end users with a convergence of convenience, assortment, and value.

Top Companies in Finland Plant-Based Dairy Market

The top companies operating in the market include Kesko Oyj, Raisio Oyj, Juustoportti Oy, Valio Oy, Oatly AB, Seege Oy Ab, S Group, Fazer Finland Oy, Lidl Suomi Ky, Kavli Oy, etc., are the top players operating in the finland plant-based dairy market.

Frequently Asked Questions

Related Report

1. Market Segmentation

1.1. Research Scope

1.2. Research Methodology

1.3. Definitions and Assumptions

2. Executive Summary

3. Finland Plant Based Dairy Market Policies, Regulations, and Standards

4. Finland Plant Based Dairy Market Dynamics

4.1. Growth Factors

4.2. Challenges

4.3. Trends

4.4. Opportunities

5. Finland Plant Based Dairy Market Statistics, 2022-2032F

5.1. Market Size & Growth Outlook

5.1.1.By Revenues in US$ Million

5.2. Market Segmentation & Growth Outlook

5.2.1.By Product Type

5.2.1.1. Plant-Based Milk- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.1. Soy Drinks- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.2. Almond- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.3. Blends- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.4. Coconut- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.5. Oat- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.6. Rice- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.7. Other Plant-Based Milk- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2. Plant-Based Yoghurt- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3. Plant-Based Cheese- Market Insights and Forecast 2022-2032, USD Million

5.2.2.By Sales Channel

5.2.2.1. Retail Offline- Market Insights and Forecast 2022-2032, USD Million

5.2.2.1.1. Grocery Retailers- Market Insights and Forecast 2022-2032, USD Million

5.2.2.1.2. Convenience Retailers- Market Insights and Forecast 2022-2032, USD Million

5.2.2.1.3. Supermarkets- Market Insights and Forecast 2022-2032, USD Million

5.2.2.1.4. Hypermarkets- Market Insights and Forecast 2022-2032, USD Million

5.2.2.2. Retail Online- Market Insights and Forecast 2022-2032, USD Million

5.2.3.By Competitors

5.2.3.1. Competition Characteristics

5.2.3.2. Market Share & Analysis

6. Finland Plant-Based Milk Market Outlook, 2022-2032F

6.1. Market Size & Growth Outlook

6.1.1.By Revenues in US$ Million

6.2. Market Segmentation & Growth Outlook

6.2.1.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

7. Finland Plant-Based Yoghurt Market Outlook, 2022-2032F

7.1. Market Size & Growth Outlook

7.1.1.By Revenues in US$ Million

7.2. Market Segmentation & Growth Outlook

7.2.1.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

8. Finland Plant-Based Cheese Market Outlook, 2022-2032F

8.1. Market Size & Growth Outlook

8.1.1.By Revenues in US$ Million

8.2. Market Segmentation & Growth Outlook

8.2.1.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

9. Competitive Outlook

9.1. Company Profiles

9.1.1.Valio Oy

9.1.1.1. Business Description

9.1.1.2. Product Portfolio

9.1.1.3. Collaborations & Alliances

9.1.1.4. Recent Developments

9.1.1.5. Financial Details

9.1.1.6. Others

9.1.2.Oatly AB

9.1.2.1. Business Description

9.1.2.2. Product Portfolio

9.1.2.3. Collaborations & Alliances

9.1.2.4. Recent Developments

9.1.2.5. Financial Details

9.1.2.6. Others

9.1.3.Seege Oy Ab

9.1.3.1. Business Description

9.1.3.2. Product Portfolio

9.1.3.3. Collaborations & Alliances

9.1.3.4. Recent Developments

9.1.3.5. Financial Details

9.1.3.6. Others

9.1.4.S Group

9.1.4.1. Business Description

9.1.4.2. Product Portfolio

9.1.4.3. Collaborations & Alliances

9.1.4.4. Recent Developments

9.1.4.5. Financial Details

9.1.4.6. Others

9.1.5.Fazer Finland Oy

9.1.5.1. Business Description

9.1.5.2. Product Portfolio

9.1.5.3. Collaborations & Alliances

9.1.5.4. Recent Developments

9.1.5.5. Financial Details

9.1.5.6. Others

9.1.6.Kesko Oyj

9.1.6.1. Business Description

9.1.6.2. Product Portfolio

9.1.6.3. Collaborations & Alliances

9.1.6.4. Recent Developments

9.1.6.5. Financial Details

9.1.6.6. Others

9.1.7.Raisio Oyj

9.1.7.1. Business Description

9.1.7.2. Product Portfolio

9.1.7.3. Collaborations & Alliances

9.1.7.4. Recent Developments

9.1.7.5. Financial Details

9.1.7.6. Others

9.1.8.Juustoportti Oy

9.1.8.1. Business Description

9.1.8.2. Product Portfolio

9.1.8.3. Collaborations & Alliances

9.1.8.4. Recent Developments

9.1.8.5. Financial Details

9.1.8.6. Others

9.1.9.Lidl Suomi Ky

9.1.9.1. Business Description

9.1.9.2. Product Portfolio

9.1.9.3. Collaborations & Alliances

9.1.9.4. Recent Developments

9.1.9.5. Financial Details

9.1.9.6. Others

9.1.10. Kavli Oy

9.1.10.1. Business Description

9.1.10.2. Product Portfolio

9.1.10.3. Collaborations & Alliances

9.1.10.4. Recent Developments

9.1.10.5. Financial Details

9.1.10.6. Others

10. Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Product Type |

|

| By Sales Channel |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.