Europe Water Pump Market Report: Trends, Growth and Forecast (2026-2032)

By Pump Type (Centrifugal Pump (Overhung Pumps (Vertical Line, Horizontal End Suction), Split Case Pumps (Single/Two Stage, Multi Stage), Vertical Pumps (Turbine, Axial, Mixed Flow), Submersible Pumps (Solid Handling, Non-Solid Handling)), Positive Displacement Pump (Diaphragm Pumps, Piston Pumps, Gear Pumps, Lobe Pumps, Progressive Cavity Pumps, Screw Pumps, Vane Pumps, Peristaltic Pumps, Others)), By End User (Oil & Gas, Power, Residential, Agriculture & Irrigation, Commercial Building, HVAC, Chemical, Water & Wastewater, Food & Beverage, Others), By Country (Germany, France, Italy, Spain, The UK, Poland, Benelux, Rest of Europe) ... Read more

|

Major Players

|

Europe Water Pump Market Statistics and Insights, 2026

- Market Size Statistics

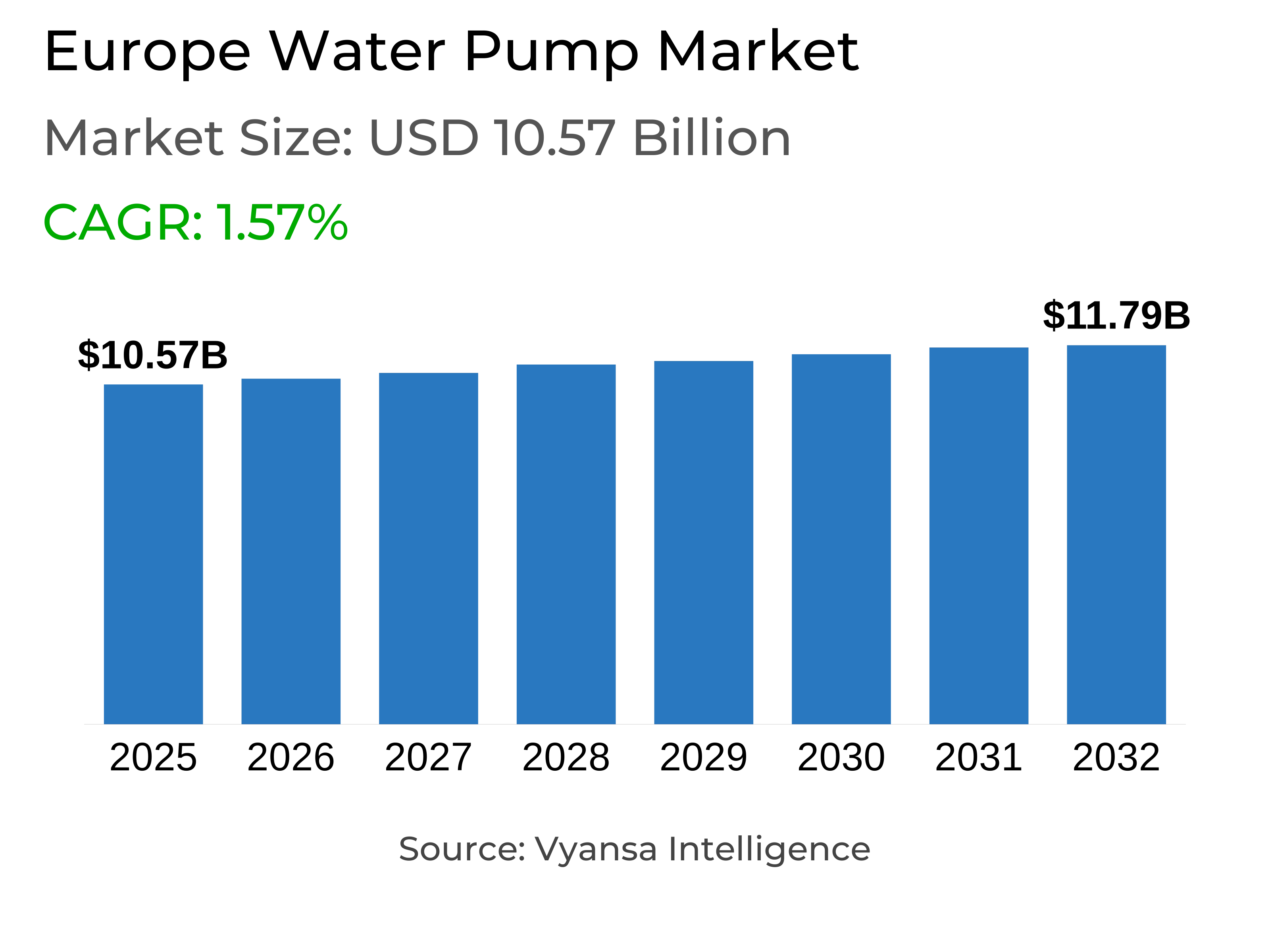

- Europe Water Pump Market is estimated at $ 10.57 Billion.

- The market size is expected to grow to $ 11.79 Billion by 2032.

- Market to register a CAGR of around 1.57% during 2026-32.

- Pump Type Shares

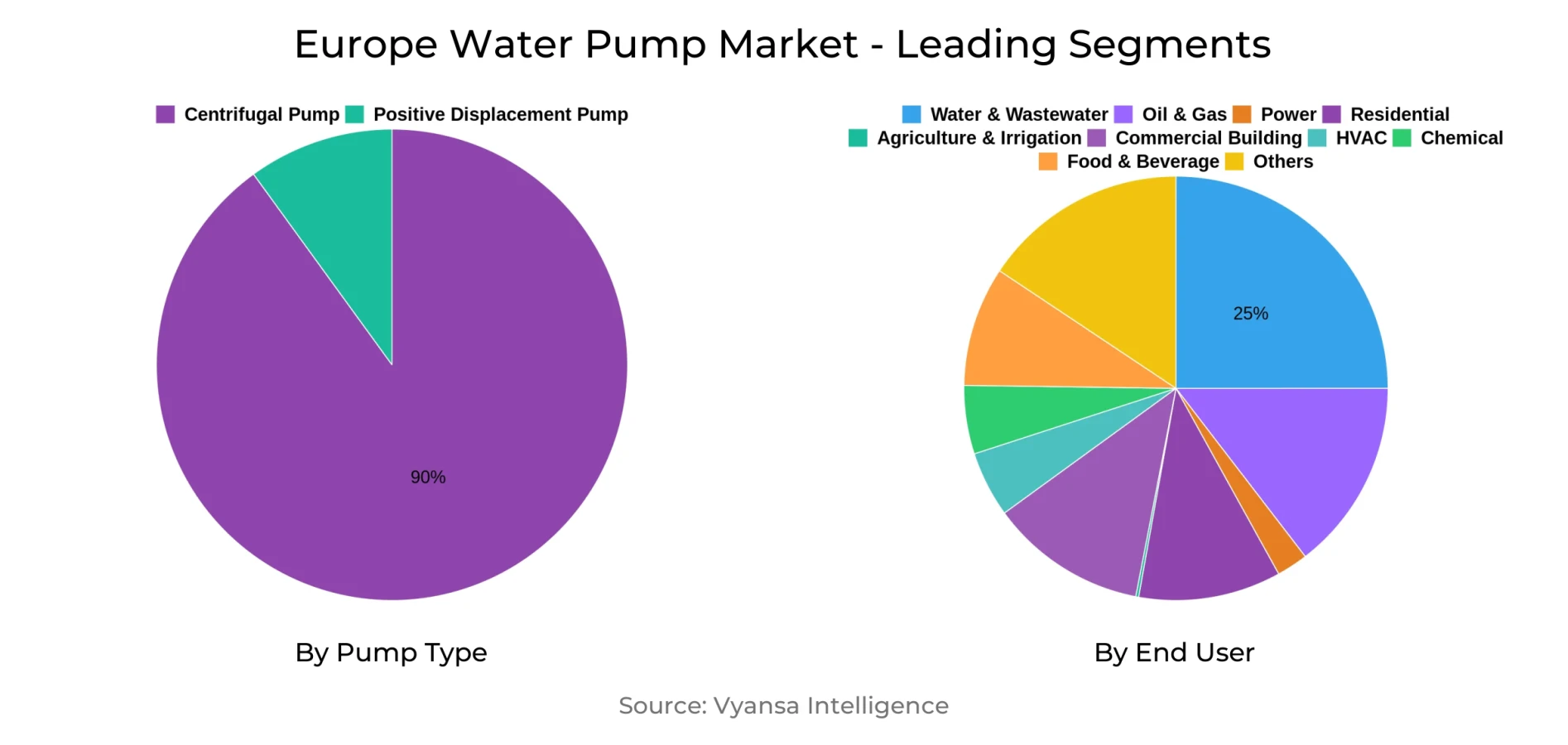

- Centrifugal Pump grabbed market share of 90%.

- Competition

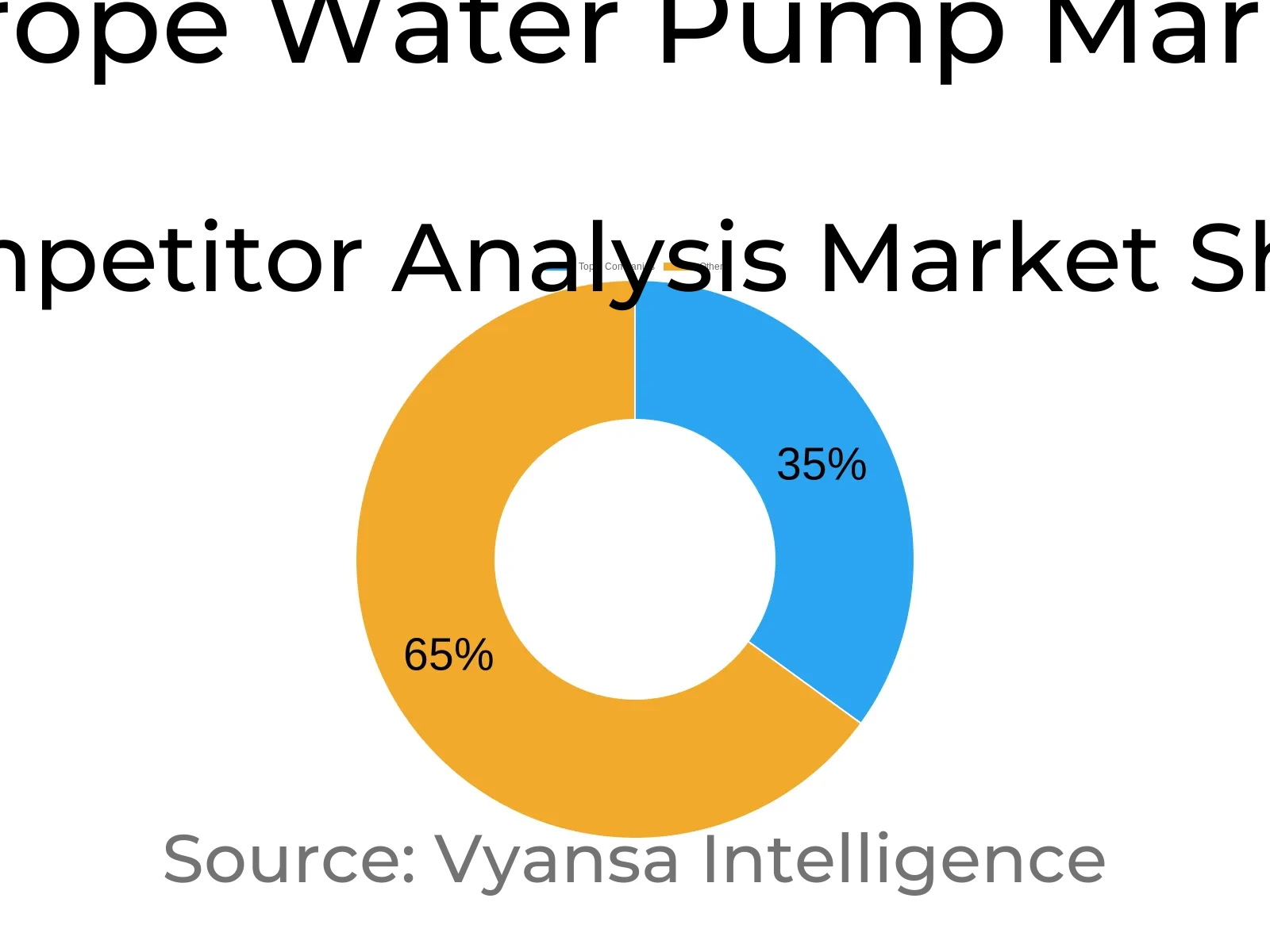

- More than 10 companies are actively engaged in producing Water Pump in Europe.

- Top 5 companies acquired 35% of the market share.

- ITT, IDEX, Dover, Flowserve, Sulzer AG etc., are few of the top companies.

- End User

- Water & Wastewater grabbed 25% of the market.

- Country

- Germany leads with a 30% share of the Europe Market.

Europe Water Pump Market Outlook

Europe Water Pump Market is valued at $10.57 billion in 2025 and is anticipated to grow to $11.79 billion by 2032, fueled by modernization programs and more stringent energy efficiency standards. Governments throughout the EU are spending more than €3.3 billion to refurbish production lines and replace antiquated municipal infrastructure with encouragement of IE4 and IE5 motor technologies. These activities, with corro-sion-resistant and low-noise pump designs, are decreasing the costs of operation and facilitating the EU Green Deal targets and making European pump production more competitive and sustainable.

Smart and modulated pump technology is increasingly dominant in the market. IoT-connected sensors, AI-based predictive maintenance, and cloud monitoring make it possible for end users to save as much as 20% of energy and lower downtime by as much as 25%. Modular designs go further in improving maintenance effectiveness, saving service time by almost 30%, and facilitating decentralized water management in cities and remote locations. Such innovations further solidify operational reliability and address increasing demand for efficient distribution of water across industries and municipalities.

Centrifugal pumps lead the market, having 90% of installations because they are versatile, low maintenance, and cost-effective. Positive displacement pumps are picking up pace in niche applications such as chemical dosing and oil & gas, being the most rapidly growing sector. Water & Wastewater is the leading end user with a market share of 25%, with municipal utilities giving high priority to high-efficiency pumps in order to keep the water clean and supply running. Agriculture & Irrigation is the growth leader sector, fueled by precise irrigation and water-efficient water management practices.

Germany remains the largest contributor, holding a 30% share of Europe’s water pump production, supported by advanced engineering infrastructure and specialized manufacturing hubs. More than 10 companies operate in Europe, with the top 5 controlling 35% of the market, highlighting both competition and collaboration in driving technological innovation. Strong government support, skilled workforce availability, and significant R&D investment continue to position Europe as a leader in efficient, low-carbon water infrastructure solutions.

Europe Water Pump Market Growth Driver

Infrastructure Modernization Fuels Market Expansion

The Europe Water Pump Market is experiencing rapid growth fueled by the imperative energy efficiency regulations necessitating the adoption of IE4 and IE5 motor technologies. The governments of the EU are investing more than €3.3 billion to upgrade pump production lines and replace aging municipal infrastructure. These developments encourage the creation of corrosion-resistant, low-noise designs that reduce operating costs while advancing the EU's Green Deal goals. Such innovations are redefining industry competitiveness by instilling sustainability at the very fabric of pump technology.

At the same time, the shift in the region towards digitalized operations bolsters system optimization. The widespread adoption of variable frequency drives and cloud-monitoring platforms facilitates predictive maintenance and real-time diagnosis, cutting downtime by up to 25%. The integration of smart control systems with eco-efficient materials makes Europe's pump manufacturing ecosystem a leader in low-carbon water infrastructure solutions.

Europe Water Pump Market Challenge

Aging Infrastructure Impedes Technological Integration

The process of modernizing the water pump infrastructure in Europe is constantly hampered by aging distribution systems. About 60% of the water networks in the EU are more than 30 years old, which causes frequent leakages, inefficiencies, and energy losses. The addition of latest pump technologies to these vintage networks is also hindered by incompatible specifications and reduced spatial compatibility, allowing slow progress toward complete system upgrade.

Besides, the lack of trained installers and technicians accelerates project timelines. The mismatch between skilled workforce availability and rising replacement demand pushes back retrofit schedules beyond initial projections. Closing this talent gap and aligning technical requirements across EU member states are key to ensuring smooth take-up of new-generation pump systems and keeping the pace in infrastructure rejuvenation activities.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Europe Water Pump Market Trend

Adoption of Smart Pump Technologies Gains Momentum

Smart pumping systems integrated with IoT-based sensors are changing operational efficiency at a lightning-fast pace in Europe. With the use of AI-powered predictive analytics, end customers are able to save up to 20% energy as compared to traditional units. Real-time monitoring dashboards provide valuable insights into such prime parameters as flow rate, pressure fluctuations, and motor conditions, allowing proactive maintenance and avoiding the threat of system failure.

In addition, the increasing use of modular pump designs facilitates quicker and less expensive maintenance. The adaptable structures enable fast component exchange with service time being minimized by almost 30%. With the evolution of decentralized water management among municipalities and industrial operators, such intelligent, modular systems improve reliability and resilience in urban and rural European environments alike.

Europe Water Pump Market Opportunity

Circular Economy Principles Reinforce Market Competitiveness

The Europe Water Pump Market is becoming more in line with the continent's circular economy goals. Original equipment manufacturers (OEMs) are redirecting as much as 80% of recovered stainless steel and copper from end-of-life pumps, effectively diverting reliance on raw material imports. This transition to remanufacturing sharply lowers production costs while stabilizing supply chains in the face of unstable commodity prices.

A number of OEMs also introduced refurbishment programs that promote the return of old pumps for reconditioning. These programs lengthen equipment lives, facilitate the reduction of waste, and enhance long-term brand loyalty. By integrating recycling and resource recovery into business models, manufacturers not only meet EU sustainability directives but also achieve a competitive advantage through improved operating and environmental efficiency.

Europe Water Pump Market Country Analysis

Germany is the dominant market, holding a 30% share in Europe's water pump manufacture in 2025. The large industrial base and high-level engineering capacity of the country form the basis for its leadership, with a high concentration of specialist factory capacity in Baden-Württemberg and North Rhine-Westphalia guaranteeing uniform quality and mass production. The strong production environment underpins both local application and export markets, cementing Germany's position as Europe's water pump innovation and manufacturing powerhouse.

Government support further reinforces market development, with the German Federal Ministry for Economic Affairs and Climate Action offering efficiency grants and low-interest loans to drive modernization in both public utilities and private industries. With a highly qualified workforce and massive R&D spending by top pump OEMs, Germany remains the standard-bearer in terms of reliability, operating efficiency, and technology innovation in water management systems.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Europe Water Pump Market Segmentation Analysis

By Pump Type

- Centrifugal Pump

- Positive Displacement Pump

Centrifugal pumps have a majority share in the Europe Water Pump Market with a market share of 90% under the pump type segment. Their flexibility in use, minimal maintenance needs, and cost-effectiveness render them an absolute necessity in municipal water supply, heating, ventilation, and air conditioning, and industrial processing. End-suction, split-case, and multistage types offer adaptable performance abilities that serve various flow and pressure requirements, contributing to their high penetration across the region.

However, positive displacement pumps are quickly gaining ground in niche applications. Their precise flow control and ability to manage high-viscosity fluids make them perfectly suited for industries like chemical dosing and oil & gas. Although their market share is still smaller, they are the fastest-growing segment, bolstered by technological advancements and growing demand for precision-crafted fluid transfer systems.

By End User

- Oil & Gas

- Power

- Residential

- Agriculture & Irrigation

- Commercial Building

- HVAC

- Chemical

- Water & Wastewater

- Food & Beverage

- Others

Water & Wastewater is the largest end-user sector, capturing a 25% market share in 2025. Municipal utilities are the earliest adopters of high-efficiency pumps to ensure water quality requirements and maintain supply consistency across urban and rural areas. Ongoing pressure to enhance treatment facilities and distribution networks continues to drive demand for high-end pumping solutions designed for extended operating cycles.

On the other hand, Agriculture & Irrigation is the most rapidly growing segment, which has registered a CAGR of 4.1% in 2026–2032. Energy-efficient pumping units integrated within precision irrigation networks improve water conservation and crop yield. With climate variability increasing throughout Europe, the agricultural industry's emphasis on sustainable irrigation habits is likely to reinforce pump demand even more in the next few years.

Top Companies in Europe Water Pump Market

The top companies operating in the market include ITT, IDEX, Dover, Flowserve, Sulzer AG, KSB, Xylem, Grundfos, Ebara, SPX Flow, Others (Kirloskar, Wilo, etc.), etc., are the top players operating in the Europe Water Pump Market.

Frequently Asked Questions

Related Report

1. Market Segmentation

1.1. Research Scope

1.2. Research Methodology

1.3. Definitions and Assumptions

2. Executive Summary

3. Europe Water Pump Market Policies, Regulations, and Standards

4. Europe Water Pump Market Dynamics

4.1. Growth Factors

4.2. Challenges

4.3. Trends

4.4. Opportunities

5. Europe Water Pump Market Statistics, 2022-2032F

5.1. Market Size & Growth Outlook

5.1.1.By Revenues in US$ Million

5.1.2.By Units Sold in Million Units

5.2. Market Segmentation & Growth Outlook

5.2.1.By Pump Type

5.2.1.1. Centrifugal Pump- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.1. Overhung Pumps- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.1.1. Vertical Line- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.1.2. Horizontal End Suction- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.2. Split Case Pumps- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.2.1. Single/Two Stage- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.2.2. Multi Stage- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.3. Vertical Pumps- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.3.1. Turbine- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.3.2. Axial- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.3.3. Mixed Flow- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.4. Submersible Pumps- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.4.1. Solid Handling- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.4.2. Non-Solid Handling- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2. Positive Displacement Pump- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.1. Diaphragm Pumps- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.2. Piston Pumps- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.3. Gear Pumps- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.4. Lobe Pumps- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.5. Progressive Cavity Pumps- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.6. Screw Pumps- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.7. Vane Pumps- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.8. Peristaltic Pumps- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.9. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.2.By End User

5.2.2.1. Oil & Gas- Market Insights and Forecast 2022-2032, USD Million

5.2.2.2. Power- Market Insights and Forecast 2022-2032, USD Million

5.2.2.3. Residential- Market Insights and Forecast 2022-2032, USD Million

5.2.2.4. Agriculture & Irrigation- Market Insights and Forecast 2022-2032, USD Million

5.2.2.5. Commercial Building- Market Insights and Forecast 2022-2032, USD Million

5.2.2.6. HVAC- Market Insights and Forecast 2022-2032, USD Million

5.2.2.7. Chemical- Market Insights and Forecast 2022-2032, USD Million

5.2.2.8. Water & Wastewater- Market Insights and Forecast 2022-2032, USD Million

5.2.2.9. Food & Beverage- Market Insights and Forecast 2022-2032, USD Million

5.2.2.10. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.3.By Country

5.2.3.1. Germany

5.2.3.2. France

5.2.3.3. Italy

5.2.3.4. Spain

5.2.3.5. The UK

5.2.3.6. Poland

5.2.3.7. Benelux

5.2.3.8. Rest of Europe

5.2.4.By Competitors

5.2.4.1. Competition Characteristics

5.2.4.2. Market Share & Analysis

6. Germany Water Pump Market Statistics, 2022-2032F

6.1. Market Size & Growth Outlook

6.1.1.By Revenues in US$ Million

6.1.2.By Units Sold in Million Units

6.2. Market Segmentation & Growth Outlook

6.2.1.By Pump Type- Market Insights and Forecast 2022-2032, USD Million

6.2.2.By End User- Market Insights and Forecast 2022-2032, USD Million

7. France Water Pump Market Statistics, 2022-2032F

7.1. Market Size & Growth Outlook

7.1.1.By Revenues in US$ Million

7.1.2.By Units Sold in Million Units

7.2. Market Segmentation & Growth Outlook

7.2.1.By Pump Type- Market Insights and Forecast 2022-2032, USD Million

7.2.2.By End User- Market Insights and Forecast 2022-2032, USD Million

8. Italy Water Pump Market Statistics, 2022-2032F

8.1. Market Size & Growth Outlook

8.1.1.By Revenues in US$ Million

8.1.2.By Units Sold in Million Units

8.2. Market Segmentation & Growth Outlook

8.2.1.By Pump Type- Market Insights and Forecast 2022-2032, USD Million

8.2.2.By End User- Market Insights and Forecast 2022-2032, USD Million

9. Spain Water Pump Market Statistics, 2022-2032F

9.1. Market Size & Growth Outlook

9.1.1.By Revenues in US$ Million

9.1.2.By Units Sold in Million Units

9.2. Market Segmentation & Growth Outlook

9.2.1.By Pump Type- Market Insights and Forecast 2022-2032, USD Million

9.2.2.By End User- Market Insights and Forecast 2022-2032, USD Million

10. The UK Water Pump Market Statistics, 2022-2032F

10.1. Market Size & Growth Outlook

10.1.1. By Revenues in US$ Million

10.1.2. By Units Sold in Million Units

10.2. Market Segmentation & Growth Outlook

10.2.1. By Pump Type- Market Insights and Forecast 2022-2032, USD Million

10.2.2. By End User- Market Insights and Forecast 2022-2032, USD Million

11. Poland Water Pump Market Statistics, 2022-2032F

11.1. Market Size & Growth Outlook

11.1.1. By Revenues in US$ Million

11.1.2. By Units Sold in Million Units

11.2. Market Segmentation & Growth Outlook

11.2.1. By Pump Type- Market Insights and Forecast 2022-2032, USD Million

11.2.2. By End User- Market Insights and Forecast 2022-2032, USD Million

12. Benelux Water Pump Market Statistics, 2022-2032F

12.1. Market Size & Growth Outlook

12.1.1. By Revenues in US$ Million

12.1.2. By Units Sold in Million Units

12.2. Market Segmentation & Growth Outlook

12.2.1. By Pump Type- Market Insights and Forecast 2022-2032, USD Million

12.2.2. By End User- Market Insights and Forecast 2022-2032, USD Million

13. Competitive Outlook

13.1. Company Profiles

13.1.1. Flowserve

13.1.1.1. Business Description

13.1.1.2. Product Portfolio

13.1.1.3. Collaborations & Alliances

13.1.1.4. Recent Developments

13.1.1.5. Financial Details

13.1.1.6. Others

13.1.2. Sulzer AG

13.1.2.1. Business Description

13.1.2.2. Product Portfolio

13.1.2.3. Collaborations & Alliances

13.1.2.4. Recent Developments

13.1.2.5. Financial Details

13.1.2.6. Others

13.1.3. KSB

13.1.3.1. Business Description

13.1.3.2. Product Portfolio

13.1.3.3. Collaborations & Alliances

13.1.3.4. Recent Developments

13.1.3.5. Financial Details

13.1.3.6. Others

13.1.4. Xylem

13.1.4.1. Business Description

13.1.4.2. Product Portfolio

13.1.4.3. Collaborations & Alliances

13.1.4.4. Recent Developments

13.1.4.5. Financial Details

13.1.4.6. Others

13.1.5. Grundfos

13.1.5.1. Business Description

13.1.5.2. Product Portfolio

13.1.5.3. Collaborations & Alliances

13.1.5.4. Recent Developments

13.1.5.5. Financial Details

13.1.5.6. Others

13.1.6. ITT

13.1.6.1. Business Description

13.1.6.2. Product Portfolio

13.1.6.3. Collaborations & Alliances

13.1.6.4. Recent Developments

13.1.6.5. Financial Details

13.1.6.6. Others

13.1.7. IDEX

13.1.7.1. Business Description

13.1.7.2. Product Portfolio

13.1.7.3. Collaborations & Alliances

13.1.7.4. Recent Developments

13.1.7.5. Financial Details

13.1.7.6. Others

13.1.8. Dover

13.1.8.1. Business Description

13.1.8.2. Product Portfolio

13.1.8.3. Collaborations & Alliances

13.1.8.4. Recent Developments

13.1.8.5. Financial Details

13.1.8.6. Others

13.1.9. Ebara

13.1.9.1. Business Description

13.1.9.2. Product Portfolio

13.1.9.3. Collaborations & Alliances

13.1.9.4. Recent Developments

13.1.9.5. Financial Details

13.1.9.6. Others

13.1.10. SPX Flow

13.1.10.1.Business Description

13.1.10.2.Product Portfolio

13.1.10.3.Collaborations & Alliances

13.1.10.4.Recent Developments

13.1.10.5.Financial Details

13.1.10.6.Others

13.1.11. Others (Kirloskar, Wilo, etc.)

13.1.11.1.Business Description

13.1.11.2.Product Portfolio

13.1.11.3.Collaborations & Alliances

13.1.11.4.Recent Developments

13.1.11.5.Financial Details

13.1.11.6.Others

14. Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Pump Type |

|

| By End User |

|

| By Country |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.