Europe Artificial Intelligence in Manufacturing Market Report: Trends, Growth and Forecast (2026-2032)

By Offering (Hardware, Software, Services), By Technology (Machine Learning, Computer Vision, Natural Language Processing, Context-Aware Computing, Generative AI, Others), By Application (Predictive Maintenance & Machinery Inspection, Quality Control & Reclamation, Production Planning & Process Optimization, Supply Chain & Inventory Optimization, Energy Management, Material Movement & Industrial Robotics, Field Services, Cybersecurity, Others), By Industry (Automotive, Semiconductor & Electronics, Energy & Power, Metals & Heavy Machinery, Food & Beverages, Pharmaceuticals & Medical Devices, Aerospace & Defense, Others), By Country (The UK, Germany, France, Italy, Spain, Rest of Europe) ... Read more

|

Major Players

|

Europe Artificial Intelligence in Manufacturing Market Statistics and Insights, 2026

- Market Size Statistics

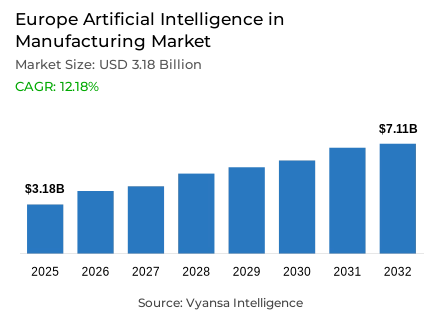

- Artificial intelligence USDUSDUSDUSDUSDUSD manufacturing market size in Europe was valued at USD 3.18 billion in 2025 and is estimated at USD 3.6 billion in 2026.

- The market size is expected to grow to USD 7.11 billion by 2032.

- Market to register a CAGR of around 12.18% during 2026-32.

- Application Shares

- Predictive maintenance & machinery inspection grabbed market share of 35%.

- Competition

- Artificial intelligence in manufacturing in Europe is currently being catered to by more than 10 companies.

- Top 5 companies acquired around 15% of the market share in 2026.

- Amazon Web Services EMEA SARL (AWS), Dassault Systèmes S.E., NVIDIA Corp., Siemens AG, Microsoft Ireland Operations Limited (Microsoft) etc., are few of the top companies.

- Industry

- Automotive grabbed 30% of the market.

- Country

- Germany leads with a 25% share of the Europe market.

Europe Artificial Intelligence in Manufacturing Market Outlook

Industrial AI is moving from isolated pilots into production-critical manufacturing workflows across Europe. The Europe artificial intelligence in manufacturing market covers software, hardware, and services used for predictive maintenance, visual inspection, planning, robotics, energy management, cybersecurity, and factory decision support. Valued at USD 3.18 billion in 2025, USD 3.6 billion in 2026, and USD 7.11 billion by 2032, the market advances at a 12.18% CAGR during 2026-2032 as manufacturers prioritize measurable productivity, uptime, and quality outcomes.

Policy support, AI infrastructure, industrial data readiness, and automation pressure are strengthening adoption across the Europe artificial intelligence in manufacturing industry. The European Commission’s 2026 Apply AI Strategy prioritizes sectoral AI uptake, SME deployment, and technological sovereignty, which supports demand for trusted industrial AI Europe platforms across machinery, automotive, electronics, energy-intensive production, and regulated manufacturing environments. This policy direction improves confidence for manufacturers evaluating AI governance, cybersecurity, and cross-border deployment models.

The Europe artificial intelligence in manufacturing market is becoming an operational efficiency layer rather than a discretionary digital investment. Manufacturers use smart factory AI to reduce unplanned downtime, stabilize quality, optimize energy consumption, and improve production scheduling. These use cases strengthen procurement justification because factory leaders increasingly connect AI-enabled manufacturing to throughput resilience, compliance readiness, worker augmentation, and supplier competitiveness, while aligning platform selection with measurable plant-level performance indicators and lifecycle cost discipline.

Supplier positioning is shifting toward integrated industrial software stacks, edge AI in manufacturing, digital twin manufacturing, and agentic factory copilots. Siemens’ 2026 Hannover Messe agenda emphasized industry-specific AI for quality and efficiency, reinforcing the Europe artificial intelligence in manufacturing industry trajectory toward domain-trained tools, sovereign deployment models, and measurable operational uptake across European production networks. Competitive intensity now favors vendors that combine OT integration, cloud scalability, and factory-specific domain expertise for scalable production modernization programs through validated enterprise deployment models.

Europe Artificial Intelligence in Manufacturing Market Growth Driver

Uptime Economics Accelerating Factory AI Adoption

Uptime protection and quality assurance are raising AI procurement priority across discrete and process manufacturers. The Europe artificial intelligence in manufacturing market benefits as plant operators shift from reactive maintenance to predictive analytics, machine condition monitoring, anomaly detection, and automated quality assurance. These capabilities improve asset utilization, reduce production variability, and support faster decision-making where skilled maintenance capacity remains constrained and production networks require higher resilience, especially across automotive, electronics, pharmaceuticals, and heavy machinery facilities.

Eurostat data shows that 20.0% of EU enterprises with at least 10 employees used AI technologies in 2025, up from 13.5% in 2024. This adoption base supports the Europe artificial intelligence in manufacturing industry because manufacturers can justify AI investment through downtime reduction, visual inspection, production planning, and resource efficiency rather than broad experimentation, improving budget approval and operational deployment visibility across multi-plant organizations and supplier networks within capital-intensive European manufacturing clusters and regulated plants.

Europe Artificial Intelligence in Manufacturing Market Challenge

Data Governance Friction Slowing Scale-Up

Data governance complexity slows deployment when factories connect AI models to production equipment, supplier systems, machine logs, and quality records. The Europe artificial intelligence in manufacturing market faces procurement friction because manufacturers must align industrial data access, cybersecurity, model transparency, and auditability before scaling AI across MES, SCADA, ERP, PLM, and shop-floor control layers. Integration risk is highest where legacy assets generate fragmented, low-context operational data during brownfield modernization programs with limited available engineering bandwidth.

The European Commission states that the Data Act applies from 12 September 2025 and provides legal clarity on access to and use of data. This affects the Europe artificial intelligence in manufacturing industry by raising expectations for compliant data-sharing, cloud switching, and connected-product data governance, which can lengthen vendor qualification cycles and increase implementation effort for AI manufacturing software across regulated facilities and delaying proof-of-concept conversion into repeatable plant rollouts across complex European production networks.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Europe Artificial Intelligence in Manufacturing Market Trend

Sovereign Compute Reshaping Industrial AI Deployment

Sovereign AI infrastructure is changing how manufacturers evaluate cloud, simulation, and factory data workloads. The Europe artificial intelligence in manufacturing market is gaining from AI-ready compute capacity that supports digital twin manufacturing, industrial generative AI, robotics simulation, and physics-based optimization without forcing every workload into generic public-cloud environments. This trend strengthens supplier differentiation around latency, data control, and industrial model performance while improving confidence among compliance-sensitive manufacturers that need secure operational technology integration.

NVIDIA stated in 2025 that an industrial AI factory in Germany would support European manufacturers with 10,000 GPUs, DGX B200 systems, RTX PRO Servers, CUDA-X libraries, RTX, and Omniverse workloads. This development strengthens manufacturing adoption by improving access to high-performance simulation, industrial AI training, and AI robotics workflows for design, engineering, and production optimization, particularly where advanced product development depends on rapid virtual validation cycles and production engineering teams require faster decision support at scale safely.

Europe Artificial Intelligence in Manufacturing Market Opportunity

SME Factory Modernization Opening Vendor White Space

AI deployment among mid-sized manufacturers remains underpenetrated, creating room for scalable industrial analytics platforms, implementation partners, and edge-to-cloud service providers. The Europe artificial intelligence in manufacturing market can capture demand where suppliers package predictive maintenance AI, AI quality inspection, production scheduling, and energy optimization into modular deployments with clear payback logic and limited disruption to existing control systems, especially for plants lacking deep internal data science teams and mature factory data architecture.

The European Commission reports that 19 AI Factories and 13 Antennas are operational or associated with AI-optimized supercomputers across the EU ecosystem. This supports the Europe artificial intelligence in manufacturing industry by expanding compute access, technical support, and data-lab capacity for SMEs, allowing vendors to localize solutions, shorten pilot cycles, and improve market access for smart manufacturing AI applications, industrial automation vendors, and factory modernization partners across manufacturing clusters requiring trusted adoption pathways and regional service scalability needs.

Europe Artificial Intelligence in Manufacturing Market Country Analysis

By Country

- The UK

- Germany

- France

- Italy

- Spain

- Rest of Europe

Germany holds 25% share due to its dense automotive, machinery, electronics, and industrial automation base. The Europe artificial intelligence in manufacturing market is strongly shaped by Germany’s concentration of high-value factories, engineering talent, industrial software suppliers, and automation integrators. This gives the Europe artificial intelligence in manufacturing market a country-level demand anchor where manufacturers invest in uptime, quality, energy efficiency, and production flexibility across export-oriented plants and supplier networks with strong Industry 4.0 maturity and advanced factory automation ecosystems.

Germany Trade & Invest reported that Germany produced 4.15 million passenger vehicles in 2025, making it Europe’s leading production site. This strengthens the Europe artificial intelligence in manufacturing industry by supporting demand for AI-enabled inspection, robotics, predictive maintenance, and production optimization across large plants, supplier parks, and export-oriented manufacturing networks that require resilient, data-driven operating models and higher transparency across production assets, maintenance cycles, and quality systems and scalable industrial AI uptake.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Europe Artificial Intelligence in Manufacturing Market Segmentation Analysis

By Application

- Predictive Maintenance & Machinery Inspection

- Quality Control & Reclamation

- Production Planning & Process Optimization

- Supply Chain & Inventory Optimization

- Energy Management

- Material Movement & Industrial Robotics

- Field Services

- Cybersecurity

- Others

Predictive Maintenance & Machinery Inspection holds 35% share because factories assign immediate budget priority to downtime prevention, asset reliability, and machine health visibility. The Europe artificial intelligence in manufacturing market benefits from this segment’s direct link to measurable productivity outcomes, as AI converts sensor data, maintenance histories, vibration signals, and operator inputs into failure prediction, inspection prioritization, and faster root-cause response, supporting stronger capacity utilization and reduced production interruption risk.

Siemens stated that its generative AI-powered maintenance offering extends Senseye Predictive Maintenance with new capabilities supporting every stage of the maintenance cycle. This strengthens segment demand by moving maintenance workflows from calendar-based intervention toward intelligent, data-driven decision support, enabling manufacturers to improve asset performance, reduce emergency repairs, and plan service resources more efficiently across complex production environments with fewer unplanned stoppages and clearer procurement justification for scaling industrial maintenance analytics across sites within asset-heavy factories and high-compliance manufacturing plants across Europe.

By Industry

- Automotive

- Semiconductor & Electronics

- Energy & Power

- Metals & Heavy Machinery

- Food & Beverages

- Pharmaceuticals & Medical Devices

- Aerospace & Defense

- Others

Automotive holds 30% share because vehicle manufacturing combines high automation intensity, model variation, quality sensitivity, and strict production-cycle discipline. The Europe artificial intelligence in manufacturing market gains from automotive demand for computer vision inspection, AI robotics, predictive maintenance, process optimization, and supply chain analytics across body shops, battery assembly, paint shops, and final assembly lines, where downtime and defects carry high operational cost and influence supplier qualification metrics across tiered automotive ecosystems.

IFR reported that Europe’s automotive industry installed 23,000 industrial robots in 2024, the second-best result in five years. This evidence supports the Europe artificial intelligence in manufacturing industry because robotized automotive plants create demand for AI-enabled motion optimization, visual inspection, predictive service, and production intelligence that improves equipment availability, quality stability, and flexible manufacturing across high-volume vehicle platforms as electrification increases production complexity and data requirements for plant operators across multi-brand European production networks and platform changeovers.

Various Market Players in Europe Artificial Intelligence in Manufacturing Market

The companies mentioned below are highly active in the Europe artificial intelligence in manufacturing market, occupying a considerable portion of the market and shaping industry progress.

- Amazon Web Services EMEA SARL (AWS)

- Dassault Systèmes S.E.

- NVIDIA Corp.

- Siemens AG

- Microsoft Ireland Operations Limited (Microsoft)

- Schneider Electric SE

- ABB Ltd

- SAP SE

- International Business Machines Corporation

- Rockwell Automation Inc.

- Google Cloud EMEA Limited

- Oracle Corporation

Market News & Updates

- Siemens AG, 2026:

Siemens showcased industrial AI solutions at Hannover Messe in Germany, including autonomous workflows, digital twins, and AI-enabled manufacturing tools. The company positioned the technologies around flexible manufacturing, traceability, and more efficient production operations. The update supports European manufacturers adopting AI for factory planning, process control, quality improvement, and operational decision support.

- SAP SE, 2025:

SAP launched the Industrial AI Cloud project with European and global partners to support “Industrial AI Made in Europe.” The project is designed to give European companies secure AI infrastructure and easier integration of AI into industrial operations. The update supports manufacturing users that need sovereign AI deployment, industrial data control, and scalable AI adoption.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- Europe Artificial Intelligence in Manufacturing Market Policies, Regulations, and Standards

- Europe Artificial Intelligence in Manufacturing Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- Europe Artificial Intelligence in Manufacturing Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Offering

- Hardware- Market Insights and Forecast 2022-2032, USD Million

- Software- Market Insights and Forecast 2022-2032, USD Million

- Services- Market Insights and Forecast 2022-2032, USD Million

- By Technology

- Machine Learning- Market Insights and Forecast 2022-2032, USD Million

- Computer Vision- Market Insights and Forecast 2022-2032, USD Million

- Natural Language Processing- Market Insights and Forecast 2022-2032, USD Million

- Context-Aware Computing- Market Insights and Forecast 2022-2032, USD Million

- Generative AI- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Application

- Predictive Maintenance & Machinery Inspection- Market Insights and Forecast 2022-2032, USD Million

- Quality Control & Reclamation- Market Insights and Forecast 2022-2032, USD Million

- Production Planning & Process Optimization- Market Insights and Forecast 2022-2032, USD Million

- Supply Chain & Inventory Optimization- Market Insights and Forecast 2022-2032, USD Million

- Energy Management- Market Insights and Forecast 2022-2032, USD Million

- Material Movement & Industrial Robotics- Market Insights and Forecast 2022-2032, USD Million

- Field Services- Market Insights and Forecast 2022-2032, USD Million

- Cybersecurity- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Industry

- Automotive- Market Insights and Forecast 2022-2032, USD Million

- Semiconductor & Electronics- Market Insights and Forecast 2022-2032, USD Million

- Energy & Power- Market Insights and Forecast 2022-2032, USD Million

- Metals & Heavy Machinery- Market Insights and Forecast 2022-2032, USD Million

- Food & Beverages- Market Insights and Forecast 2022-2032, USD Million

- Pharmaceuticals & Medical Devices- Market Insights and Forecast 2022-2032, USD Million

- Aerospace & Defense- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Country

- The UK

- Germany

- France

- Italy

- Spain

- Rest of Europe

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Offering

- Market Size & Growth Outlook

- The UK Artificial Intelligence in Manufacturing Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Offering- Market Insights and Forecast 2022-2032, USD Million

- By Technology- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Industry- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Germany Artificial Intelligence in Manufacturing Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Offering- Market Insights and Forecast 2022-2032, USD Million

- By Technology- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Industry- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- France Artificial Intelligence in Manufacturing Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Offering- Market Insights and Forecast 2022-2032, USD Million

- By Technology- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Industry- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Italy Artificial Intelligence in Manufacturing Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Offering- Market Insights and Forecast 2022-2032, USD Million

- By Technology- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Industry- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Spain Artificial Intelligence in Manufacturing Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Offering- Market Insights and Forecast 2022-2032, USD Million

- By Technology- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Industry- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Siemens AG

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Microsoft Ireland Operations Limited (Microsoft)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Schneider Electric SE

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- ABB Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- SAP SE

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Amazon Web Services EMEA SARL (AWS)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Dassault Systèmes S.E.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- NVIDIA Corp.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- International Business Machines Corporation

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Rockwell Automation, Inc.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Google Cloud EMEA Limited

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Oracle Corporation

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Siemens AG

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Offering |

|

| By Technology |

|

| By Application |

|

| By Industry |

|

| By Country |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.