Denmark Plant-Based Dairy Market Report: Trends, Growth and Forecast (2026-2032)

Product Type (Plant-Based Milk (Soy Drinks, Almond, Blends, Coconut, Oat, Rice, Other Plant-Based Milk), Plant-Based Yoghurt, Plant-Based Cheese), Sales Channel (Retail Offline (Grocery Retailers, Convenience Retailers, Supermarkets, Hypermarkets), Retail Online) ... Read more

|

Major Players

|

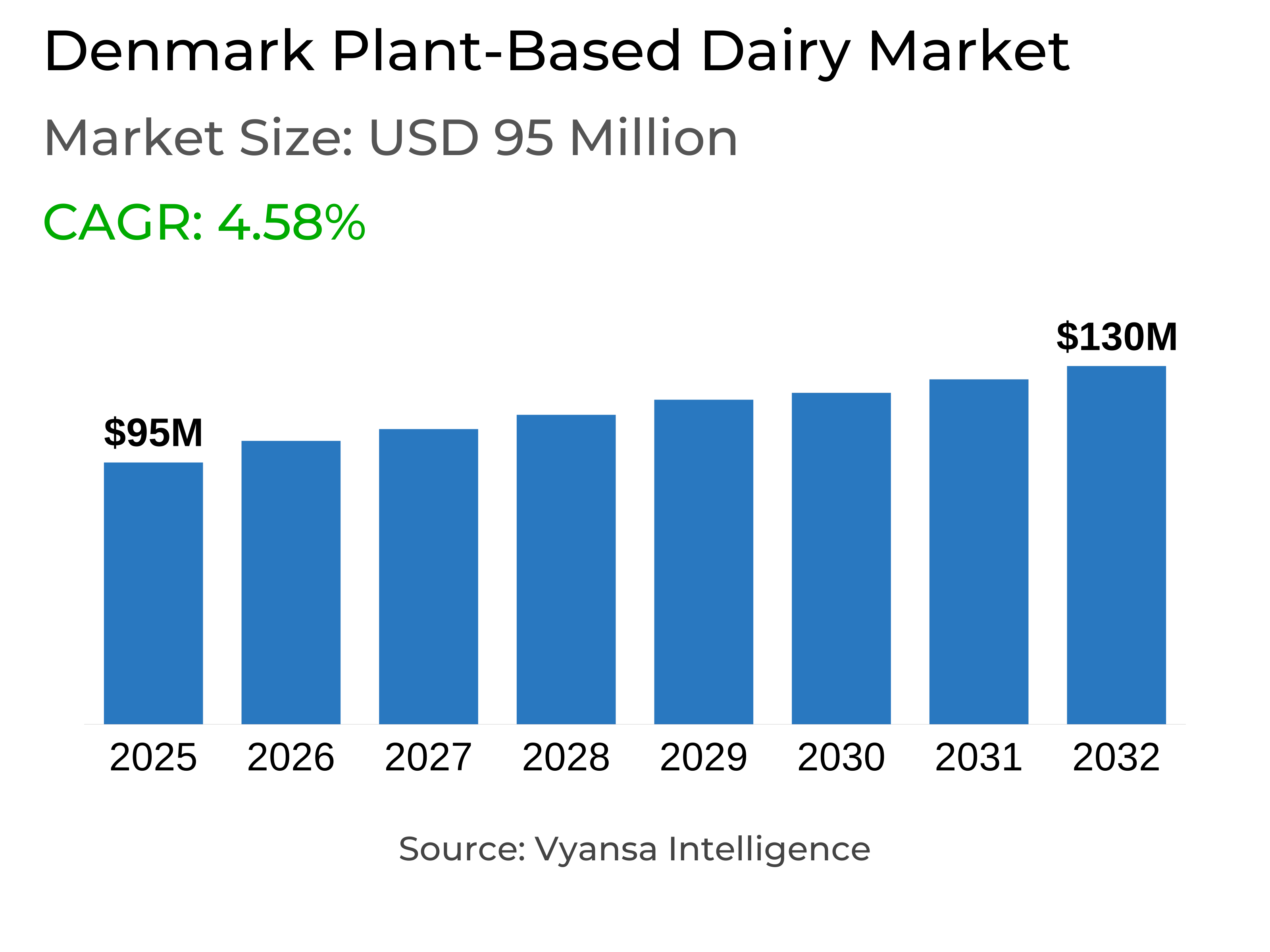

Denmark Plant-Based Dairy Market Statistics and Insights, 2026

- Market Size Statistics

- Plant-based dairy in denmark is estimated at $ 95 million.

- The market size is expected to grow to $ 130 million by 2032.

- Market to register a cagr of around 4.58% during 2026-32.

- Product Type Shares

- Plant-based milk grabbed market share of 75%.

- Competition

- More than 5 companies are actively engaged in producing plant-based dairy in denmark.

- Top 5 companies acquired around 60% of the market share.

- EVA GmbH, Arla Foods Amba, Bel Nordic AB, Naturli' Foods A/S, Danone AB etc., are few of the top companies.

- Sales Channel

- Retail offline grabbed 95% of the market.

Denmark Plant-Based Dairy Market Outlook

Denmark plant-based dairy market will continue to grow steadily during the forecast period. Estimated at $95 million in 2025, the market is expected to rise to $130 million by 2032, showing ongoing demand for plant-based drinks and other dairy alternatives. While overall growth will be smaller than previous years, base categories like plant milk are in line to remain a permanent fixture of everyday shopping due to their adaptability, gentle taste, and suitability for coffee and cooking.

Key players in the market, numbering more than five, are driving growth through innovation, quality, and expanded assortments. The top five companies alone account for 60% of the market, with Naturli Foods maintaining a leading position through popular oat-based drinks and yoghurts. Private label offerings and competitive pricing have also made plant-based dairy more accessible, supporting broader end users adoption.

Retail offline remains the preponderant distribution channel, with 95% of market passing through it. The discounters are also likely to remain a significant distribution channel, leveraging value for money and wide availability of products to attract price-sensitive end users. Retail online will further evolve incrementally driven by online grocery stores and click-and-collect offerings but will remain a subsidiary contributor compared to offline sales.

Health, wellness, and sustainability will be ongoing drivers of product development. end users are increasingly seeking out nutrient-dense, low-sugar foods, and brands must focus on sustainable sourcing, green packaging, and climate-neutral manufacturing practices. Plant-based cheese and other newer trends offer additional opportunity for growth as taste, texture, and nutrition trends converge with evolving end users preferences.

Denmark Plant-Based Dairy Market Growth DriverIncreasing Flexitarian Diets and Health Consciousness Driving Growth

The plant-based dairy category in Denmark remains underpinned by strong demand driven by flexitarian expansion and increasing health consciousness. End users seek alternatives to mainstream dairy that align with lower environmental impact, low intake of lactose, and healthy food options. Lead products such as oat milk remain strongly popular in daily usage due to their subtle taste, versatility, and nutritional value, which is encouraging overall category expansion. Price increases, supported by extension of products in mainstream ranges, have again bounced back value sales in the wake of a broader-market slowdown.

Key players like Naturli Foods have leveraged early market entry and a diversified portfolio to retain leadership, particularly in oat-based drinks and spoonable alternatives. Product innovation, such as improved taste, texture, and nutrient fortification, has helped maintain end users interest. Aggressive promotional campaigns by competitors like Arla Foods’ JÖRÐ have increased affordability and accessibility, extending the category’s reach among mainstream households while sustaining the momentum of plant-based dairy adoption.

Denmark Plant-Based Dairy Market ChallengePrice Sensitivity and Health Scrutiny Capping Growth

Market growth is under threat from price-conscious end userss and heightened examination of product health benefits. Private label competition on value propositions has also grown, and this has compelled branded players to balance price, quality, and taste. There has also been heightened comparison between plant-based products and traditional dairy in terms of sugar content, rates of additives, and nutrition, which has made health-driven motivations less conclusive among end users.

Slower category interest and gradual adoption of new subcategories, such as plant-based cheese, have also moderated growth. As long as mainstream plant-based drinks remain in fashion, manufacturers must overcome end users wariness through greater product transparency, improved nutritional offerings, and communication of benefits. Fostering loyalty in a more discerning market requires sustained investment in innovation, strategic marketing, and product differentiation in order to keep propositions in line with evolving expectations in taste, wellness, and perceived value.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Denmark Plant-Based Dairy Market TrendShaping End Users Preferences to Create Product Demand

End users in Denmark are increasingly favoring plant-based dairy alternatives with nutritional benefits combined with sensory attractiveness. Oat milk continues to lead because of its flexibility, with new alternatives like rye-based drinks being popularized for their unique flavor and natural sweetness. Growing demand for variety and dairy-free options is driving brands to experiment with taste, texture, and functional qualities so that products remain fresh in daily usage patterns. Flexitarian consumption is inspiring new formats discovery, including spoonable substitutes and nutrient-fortified drinks.

There is also an unmistakable trend away from simply judging plant-based products on ingredients, health value, and overall value. Although health and sustainability remain drivers, end userss today are now comparing these attributes to taste, convenience, and price. Those companies that can balance these factors with clear labelling, nutritional enhancement, and product innovation are well-situated to attract early adopters and mainstream end users alike, perpetuating steady market growth even in the presence of muted enthusiasm in the overall plant-based dairy category.

Denmark Plant-Based Dairy Market OpportunityInnovation and Sustainability Offering Future Opportunities

Denmark plant-based milk market has tremendous potential for growth on the basis of product innovation and sustainability-based endeavors. Companies can capitalize on end users' desire for new taste experiences, improved textures, and nutrient-rich compositions to target mainstream and flexitarian end users. Penetration into niches such as plant-based cheese is another avenue where companies can expand and diversify their categories in the longer term, especially with increasing local end users becoming more adventurous to try healthier alternatives.

Sustainability initiatives are also expected to significantly impact upcoming product innovation. Government support for plant-based protein manufacturing, climate labeling, and sustainable production makes it increasingly attractive for brands to use locally sourced ingredients, eco-friendly packaging, and transparent production processes. Companies that are integrating sustainability into products and brand voice will be able to establish trust with end users, differentiate their brands, and capture new market space, positioning themselves for long-term growth in a more health- and environmentally conscious marketplace.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Denmark Plant-Based Dairy Market Segmentation Analysis

By Product Type

- Plant-Based Milk

- Plant-Based Yoghurt

- Plant-Based Cheese

The segment with highest market share under Product Type is plant-based milk around 75% of the Denmark plant-based dairy market. The subcategory has remained highly relevant in everyday shopping due to sustained popularity of oat milk, which is valued for its neutral taste, use in coffee and cooking, and high shelf life.

Other plant milk varieties have also been driving growth on account of end users desire for free-from dairy products and diversification. Competitive prices, expanding ranges in discounters and supermarkets, and continuing interest from flexitarian end users have helped to maintain leadership of plant milk within the category, with it being the market's primary driver of growth.

By Sales Channel

- Retail Offline

- Retail Online

The segment with highest market share under Sales Channel is retail offline, around 95% share in the Denmark plant-based dairy market. Discounters control sales with price-conscious end users in pursuit of bargain offerings. Greater plant-based presence in beverages, private label lines, and low-labeled prices make Retail offline the primary channel for regular purchase in the category.

Retail Offline domination is contributed to by supermarkets through high shelf presence for branded as well as private label plant-based dairy. Despite retail online showing dynamism from a low base with the availability of online grocery platforms and click-and-collect services, Retail offline remains the leading channel for local end users, driven by convenience, price, and variety of plant-based dairy product availability.

Top Companies in Denmark Plant-Based Dairy Market

The top companies operating in the market include EVA GmbH, Arla Foods Amba, Bel Nordic AB, Naturli' Foods A/S, Danone AB, Oatly AB, Falengreen A/S, Upfield Danmark A/S, etc., are the top players operating in the denmark plant-based dairy market.

Frequently Asked Questions

Related Report

1. Market Segmentation

1.1. Research Scope

1.2. Research Methodology

1.3. Definitions and Assumptions

2. Executive Summary

3. Denmark Plant Based Dairy Market Policies, Regulations, and Standards

4. Denmark Plant Based Dairy Market Dynamics

4.1. Growth Factors

4.2. Challenges

4.3. Trends

4.4. Opportunities

5. Denmark Plant Based Dairy Market Statistics, 2022-2032F

5.1. Market Size & Growth Outlook

5.1.1.By Revenues in US$ Million

5.2. Market Segmentation & Growth Outlook

5.2.1.By Product Type

5.2.1.1. Plant-Based Milk- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.1. Soy Drinks- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.2. Almond- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.3. Blends- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.4. Coconut- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.5. Oat- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.6. Rice- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.7. Other Plant-Based Milk- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2. Plant-Based Yoghurt- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3. Plant-Based Cheese- Market Insights and Forecast 2022-2032, USD Million

5.2.2.By Sales Channel

5.2.2.1. Retail Offline- Market Insights and Forecast 2022-2032, USD Million

5.2.2.1.1. Grocery Retailers- Market Insights and Forecast 2022-2032, USD Million

5.2.2.1.2. Convenience Retailers- Market Insights and Forecast 2022-2032, USD Million

5.2.2.1.3. Supermarkets- Market Insights and Forecast 2022-2032, USD Million

5.2.2.1.4. Hypermarkets- Market Insights and Forecast 2022-2032, USD Million

5.2.2.2. Retail Online- Market Insights and Forecast 2022-2032, USD Million

5.2.3.By Competitors

5.2.3.1. Competition Characteristics

5.2.3.2. Market Share & Analysis

6. Denmark Plant-Based Milk Market Outlook, 2022-2032F

6.1. Market Size & Growth Outlook

6.1.1.By Revenues in US$ Million

6.2. Market Segmentation & Growth Outlook

6.2.1.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

7. Denmark Plant-Based Yoghurt Market Outlook, 2022-2032F

7.1. Market Size & Growth Outlook

7.1.1.By Revenues in US$ Million

7.2. Market Segmentation & Growth Outlook

7.2.1.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

8. Denmark Plant-Based Cheese Market Outlook, 2022-2032F

8.1. Market Size & Growth Outlook

8.1.1.By Revenues in US$ Million

8.2. Market Segmentation & Growth Outlook

8.2.1.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

9. Competitive Outlook

9.1. Company Profiles

9.1.1.Naturli' Foods A/S

9.1.1.1. Business Description

9.1.1.2. Product Portfolio

9.1.1.3. Collaborations & Alliances

9.1.1.4. Recent Developments

9.1.1.5. Financial Details

9.1.1.6. Others

9.1.2.Danone AB

9.1.2.1. Business Description

9.1.2.2. Product Portfolio

9.1.2.3. Collaborations & Alliances

9.1.2.4. Recent Developments

9.1.2.5. Financial Details

9.1.2.6. Others

9.1.3.Oatly AB

9.1.3.1. Business Description

9.1.3.2. Product Portfolio

9.1.3.3. Collaborations & Alliances

9.1.3.4. Recent Developments

9.1.3.5. Financial Details

9.1.3.6. Others

9.1.4.Falengreen A/S

9.1.4.1. Business Description

9.1.4.2. Product Portfolio

9.1.4.3. Collaborations & Alliances

9.1.4.4. Recent Developments

9.1.4.5. Financial Details

9.1.4.6. Others

9.1.5.Upfield Danmark A/S

9.1.5.1. Business Description

9.1.5.2. Product Portfolio

9.1.5.3. Collaborations & Alliances

9.1.5.4. Recent Developments

9.1.5.5. Financial Details

9.1.5.6. Others

9.1.6.EVA GmbH

9.1.6.1. Business Description

9.1.6.2. Product Portfolio

9.1.6.3. Collaborations & Alliances

9.1.6.4. Recent Developments

9.1.6.5. Financial Details

9.1.6.6. Others

9.1.7.Arla Foods Amba

9.1.7.1. Business Description

9.1.7.2. Product Portfolio

9.1.7.3. Collaborations & Alliances

9.1.7.4. Recent Developments

9.1.7.5. Financial Details

9.1.7.6. Others

9.1.8.Bel Nordic AB

9.1.8.1. Business Description

9.1.8.2. Product Portfolio

9.1.8.3. Collaborations & Alliances

9.1.8.4. Recent Developments

9.1.8.5. Financial Details

9.1.8.6. Others

9.1.9.Solhjulet A/S

9.1.9.1. Business Description

9.1.9.2. Product Portfolio

9.1.9.3. Collaborations & Alliances

9.1.9.4. Recent Developments

9.1.9.5. Financial Details

9.1.9.6. Others

9.1.10. NatureSource I/S

9.1.10.1. Business Description

9.1.10.2. Product Portfolio

9.1.10.3. Collaborations & Alliances

9.1.10.4. Recent Developments

9.1.10.5. Financial Details

9.1.10.6. Others

10. Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Product Type |

|

| By Sales Channel |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.