China Software-Defined Vehicle Platforms Market Report: Trends, Growth and Forecast (2026-2032)

By Component (Software, Services), By Software Application Domain (ADAS & Autonomous Driving Software, Infotainment & Digital Cockpit Software, Powertrain Control Software, Chassis & Vehicle Dynamics Software, Body & Comfort Software, Cross-Vehicle Enablers (Platform Infrastructure) (Vehicle OS & Middleware, OTA Update Management, Cybersecurity, DevOps & Toolchains)), By Deployment Mode (On-Board (Embedded), Cloud-Based, Hybrid (On-Board + Cloud)), By End-User (Automotive OEMs, Tier-1 Suppliers, Fleet Operators & Mobility Service Providers), By Vehicle Type (Passenger Vehicles, Commercial Vehicles), By Region (North, East, Southwest, Northwest, North East, South) ... Read more

|

Major Players

|

China Software-Defined Vehicle Platforms Market Statistics and Insights, 2026

- Market Size Statistics

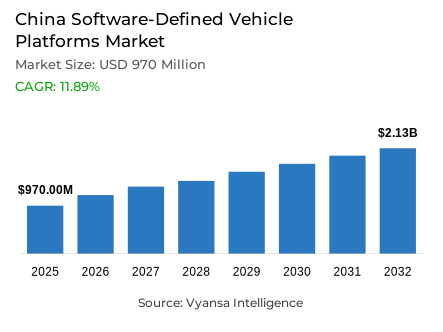

- Software-defined vehicle platforms market size in China was valued at USD 970 million in 2025 and is estimated at USD 1.16 billion in 2026.

- The market size is expected to grow to USD 2.13 billion by 2032.

- Market to register a CAGR of around 11.89% during 2026-32.

- Software Application Domain Shares

- Adas & autonomous driving software grabbed market share of 35%.

- Competition

- Software-defined vehicle platforms in China is currently being catered to by more than 10 companies.

- Top 5 companies acquired around 25% of the market share in 2026.

- Thunder Software Technology Co. Ltd. (ThunderSoft), Huizhou Desay SV Automotive Co. Ltd., Robert Bosch GmbH (Bosch Mobility), Qualcomm Technologies Inc. (Snapdragon Digital Chassis), NVIDIA Corporation (NVIDIA DRIVE) etc., are few of the top companies.

- Deployment Mode

- On-board (embedded) grabbed 45% of the market.

China Software-Defined Vehicle Platforms Market Outlook

The China software-defined vehicle platforms market covers vehicle operating systems, middleware, ADAS software, cockpit software, OTA management, cybersecurity, cloud orchestration, and embedded compute layers used by OEMs, Tier-1 suppliers, mobility fleets, and platform vendors. The China software-defined vehicle (SDV) platforms industry is moving from isolated ECU integration toward centralized software stacks. Valued at USD 970 million in 2025, the China software-defined vehicle platforms market is projected to reach USD 1.16 billion in 2026 and USD 2.13 billion by 2032, expanding at a 11.89% CAGR during 2026-2032.

Demand is strengthened by China’s high NEV scale, intelligent connected vehicle policy, and rising software content per vehicle. China software-defined vehicle platforms market adoption is tied to smart cockpit rollout, Level-2 assisted-driving penetration, C-V2X deployment, and over-the-air lifecycle management. State Council data published in January 2026 show China’s 2025 NEV production and sales reached 16.626 million and 16.49 million units, respectively, creating a large installed base for software-defined vehicle platforms and connected EV software services.

Industrial impact is concentrated in development efficiency, supplier localization, and platform reuse across model lines. The China software-defined vehicle (SDV) platforms industry improves OEM competitiveness because common software architectures reduce repeated engineering across vehicle portfolios while supporting feature updates, diagnostics, data governance, and cybersecurity compliance. It strengthens procurement visibility for automotive software platform China participants, since domain controllers, middleware, vehicle cloud, and ADAS software influence sourcing decisions before vehicle SOP.

Supplier positioning in 2026 is shaped by cockpit-driving integration, automotive middleware, vehicle operating system layers, and centralized E/E architecture. Platform demand is becoming a strategic control layer for OEM differentiation. Domestic players such as Huawei, Horizon Robotics, Baidu Apollo, ThunderSoft, and Desay SV are positioned to capture demand as Chinese automakers prioritize SDV software stack China capabilities, secure OTA software platform functions, and production-ready ADAS software platform integration.

China Software-Defined Vehicle Platforms Market Growth Driver

Intelligent Vehicle Software Becomes a Demand-Side Growth Engine

NEV model proliferation and intelligent connected vehicle adoption are expanding demand for reusable software architectures across China’s passenger-vehicle base. The China software-defined vehicle (SDV) platforms industry benefits as OEMs shift spending from hardware-only differentiation toward autonomous driving software, smart cockpit platforms, connected navigation, energy management software, and vehicle data platform functions. This raises procurement for software layers reused across trims, brands, regional variants, and model-year refreshes.

China’s State Council reported in September 2025 that 7.76 million new passenger cars sold from January to July 2025 were equipped with Level-2 driving-assistance functions, representing 62.58% penetration. That operating base supports the China software-defined vehicle platforms market by expanding recurring demand for perception software, path planning software, OTA validation, cybersecurity modules, and domain-controller software integration as OEMs scale assisted-driving features across mass-market vehicles.

China Software-Defined Vehicle Platforms Market Challenge

Safety Validation and Software Governance Slow Deployment Velocity

Software complexity, cybersecurity exposure, and validation cost pressure are slowing wider deployment of advanced assisted-driving and OTA functions. The China software-defined vehicle platforms market faces tighter certification expectations as software updates increasingly affect braking, steering, perception, and driver-monitoring functions. Multi-vendor stacks also complicate ASPICE alignment, functional safety testing, ISO 26262 compliance, and secure OTA update governance, raising integration workloads for OEMs and Tier-1 suppliers.

China is accelerating standards for combined driving-assistance systems, automated driving systems, and automatic emergency braking systems, according to the State Council’s September 2025 intelligent connected vehicle update. This policy direction supports safety but raises compliance readiness requirements for the China software-defined vehicle (SDV) platforms industry, especially where suppliers must validate automotive cybersecurity, software lifecycle management, and vehicle software security before wider deployment in production programs.

Unlock Market Intelligence

Explore the market potential with our data-driven report

China Software-Defined Vehicle Platforms Market Trend

Centralized Compute Pushes SDVs Toward AI-Defined Architectures

Centralized compute and cockpit-driving integration are reshaping vehicle platform design as OEMs consolidate functions from distributed ECUs into domain and central controllers. The China software-defined vehicle platforms market gains momentum from this shift because common compute platforms enable software reuse, AI model portability, faster feature rollout, and more coherent vehicle API platform design across model lines. This supports continuous upgrades without rebuilding every vehicle function around isolated hardware units.

Qualcomm stated in March 2026 that Snapdragon Digital Chassis provides a unified compute platform with heterogeneous CPUs, GPUs, and NPUs, enabling software reuse and efficient scaling across vehicle portfolios. This development strengthens SDV platform adoption by supporting high-performance vehicle compute, cloud-native development flows, model portability, and automotive central computing strategies required by Chinese OEMs competing on software-defined mobility.

China Software-Defined Vehicle Platforms Market Opportunity

Vehicle-Road-Cloud Pilots Open Platform-Scale Expansion

Vehicle-road-cloud integration creates an underpenetrated opportunity for platform suppliers linking onboard software, roadside infrastructure, and cloud intelligence. The China software-defined vehicle platforms market can capture demand from C-V2X technology, telematics software, intelligent transportation connectivity, and cloud-based vehicle intelligence as pilot infrastructure moves from testing to operational deployment. These programs expand addressable demand beyond the vehicle itself into data platforms, simulation, mapping, and remote diagnostics.

The State Council reported in September 2025 that China is fast-tracking 20 pilot cities for vehicle-road-cloud integration and has opened more than 35,000 kilometers of test and demonstration roads. This expands opportunity for the China software-defined vehicle (SDV) platforms industry by improving infrastructure readiness, strengthening market access for C-V2X enabled SDV platforms in China, and supporting vehicle-road-cloud integration software China procurement across city-level mobility ecosystems.

Unlock Market Intelligence

Explore the market potential with our data-driven report

China Software-Defined Vehicle Platforms Market Segmentation Analysis

By Software Application Domain

- ADAS & Autonomous Driving Software

- Infotainment & Digital Cockpit Software

- Powertrain Control Software

- Chassis & Vehicle Dynamics Software

- Body & Comfort Software

- Cross-Vehicle Enablers (Platform Infrastructure)

- Vehicle OS & Middleware

- OTA Update Management

- Cybersecurity

- DevOps & Toolchains

ADAS & Autonomous Driving Software holds 35% share under software application domain because Chinese OEMs are prioritizing assisted-driving features as a core differentiator across NEV and smart EV portfolios. The China software-defined vehicle platforms market benefits from demand for perception software, sensor fusion middleware, autonomous driving software stack, urban NOA, highway NOA, parking automation, and high-speed navigation functions that require embedded compute plus continuous software validation.

For instance, BYD released the DiPilot system in February 2025 with DiPilot 600, DiPilot 300, and DiPilot 100 versions, including LiDAR and tri-camera configurations across different model tiers. BYD also stated that its vehicle-cloud database covered more than 4.4 million vehicles equipped with L2 ADAS, which supports the China software-defined vehicle (SDV) platforms industry by expanding training, validation, OTA, and smart driving platform demand.

By Deployment Mode

- On-Board (Embedded)

- Cloud-Based

- Hybrid (On-Board + Cloud)

On-Board (Embedded) holds 45% share under deployment mode because safety-critical vehicle functions require low-latency execution inside the vehicle rather than cloud-only processing. The software-defined vehicle platforms market in China depends on embedded controllers for ADAS decisions, powertrain control, chassis execution, body control, cockpit response, and cybersecurity enforcement. Cloud layers remain important for DevOps, simulation, data ingestion, and OTA lifecycle management, but real-time execution remains vehicle-resident.

Huawei’s 2024 annual report stated that its intelligent automotive solution domain shipped more than 23 million sets of intelligent automotive components and worked with more than 600 value-chain partners. This operational scale supports the China software-defined vehicle (SDV) platforms industry by reinforcing demand for on-board compute, embedded software, automotive middleware, and vehicle cloud interfaces that coordinate production-ready software functions across OEM vehicle programs.

List of Companies Covered in China Software-Defined Vehicle Platforms Market

The companies listed below are highly influential in the China software-defined vehicle platforms market, with a significant market share and a strong impact on industry developments.

- Thunder Software Technology Co. Ltd. (ThunderSoft)

- Huizhou Desay SV Automotive Co. Ltd.

- Robert Bosch GmbH (Bosch Mobility)

- Qualcomm Technologies Inc. (Snapdragon Digital Chassis)

- NVIDIA Corporation (NVIDIA DRIVE)

- Beijing Horizon Information Technology Co. Ltd. (Horizon Robotics)

- Huawei Technologies Co. Ltd (Huawei Intelligent Automotive Solution BU)

- Baidu Apollo Network (Beijing) Limited (Baidu Apollo)

- BYD Company Limited

- XPeng Inc.

Market News & Updates

- Thunder Software Technology Co. Ltd. (ThunderSoft), 2025:

ThunderX selected QNX technology as the software foundation for its Cockpit-AD fusion domain controller for commercial vehicles in China. The controller combines instrumentation, infotainment, and in-cabin ADAS on one platform. The update supports China’s SDV shift toward cockpit-driving integration, domain controllers, and production-ready embedded software platforms.

- Beijing Horizon Information Technology Co. Ltd.(Horizon Robotics), 2025:

Horizon Robotics and ZF announced an ADAS system for the Chinese market supporting up to SAE Level 3 assisted driving and urban Navigate on Autopilot. The system uses Horizon’s Journey 6P processing hardware with ZF ProAI. The update supports China’s SDV demand for localized ADAS software, high-performance compute, and assisted-driving platforms.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- China Software-Defined Vehicle (SDV) Platforms Market Policies, Regulations, and Standards

- China Software-Defined Vehicle (SDV) Platforms Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- China Software-Defined Vehicle (SDV) Platforms Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Component

- Software- Market Insights and Forecast 2022-2032, USD Million

- Services- Market Insights and Forecast 2022-2032, USD Million

- By Software Application Domain

- ADAS & Autonomous Driving Software- Market Insights and Forecast 2022-2032, USD Million

- Infotainment & Digital Cockpit Software- Market Insights and Forecast 2022-2032, USD Million

- Powertrain Control Software- Market Insights and Forecast 2022-2032, USD Million

- Chassis & Vehicle Dynamics Software- Market Insights and Forecast 2022-2032, USD Million

- Body & Comfort Software- Market Insights and Forecast 2022-2032, USD Million

- Cross-Vehicle Enablers (Platform Infrastructure)- Market Insights and Forecast 2022-2032, USD Million

- Vehicle OS & Middleware- Market Insights and Forecast 2022-2032, USD Million

- OTA Update Management- Market Insights and Forecast 2022-2032, USD Million

- Cybersecurity- Market Insights and Forecast 2022-2032, USD Million

- DevOps & Toolchains- Market Insights and Forecast 2022-2032, USD Million

- By Deployment Mode

- On-Board (Embedded)- Market Insights and Forecast 2022-2032, USD Million

- Cloud-Based- Market Insights and Forecast 2022-2032, USD Million

- Hybrid (On-Board + Cloud)- Market Insights and Forecast 2022-2032, USD Million

- By End-User

- Automotive OEMs- Market Insights and Forecast 2022-2032, USD Million

- Tier-1 Suppliers- Market Insights and Forecast 2022-2032, USD Million

- Fleet Operators & Mobility Service Providers- Market Insights and Forecast 2022-2032, USD Million

- By Vehicle Type

- Passenger Vehicles- Market Insights and Forecast 2022-2032, USD Million

- Commercial Vehicles- Market Insights and Forecast 2022-2032, USD Million

- By Region

- North- Market Insights and Forecast 2022-2032, USD Million

- East- Market Insights and Forecast 2022-2032, USD Million

- Southwest- Market Insights and Forecast 2022-2032, USD Million

- Northwest- Market Insights and Forecast 2022-2032, USD Million

- North East- Market Insights and Forecast 2022-2032, USD Million

- South- Market Insights and Forecast 2022-2032, USD Million

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Component

- Market Size & Growth Outlook

- China ADAS & Autonomous Driving Software Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Software Application Domain- Market Insights and Forecast 2022-2032, USD Million

- By Deployment Mode- Market Insights and Forecast 2022-2032, USD Million

- By End-User- Market Insights and Forecast 2022-2032, USD Million

- By Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- China Infotainment & Digital Cockpit Software Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Software Application Domain- Market Insights and Forecast 2022-2032, USD Million

- By Deployment Mode- Market Insights and Forecast 2022-2032, USD Million

- By End-User- Market Insights and Forecast 2022-2032, USD Million

- By Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- China Powertrain Control Software Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Software Application Domain- Market Insights and Forecast 2022-2032, USD Million

- By Deployment Mode- Market Insights and Forecast 2022-2032, USD Million

- By End-User- Market Insights and Forecast 2022-2032, USD Million

- By Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- China Chassis & Vehicle Dynamics Software Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Software Application Domain- Market Insights and Forecast 2022-2032, USD Million

- By Deployment Mode- Market Insights and Forecast 2022-2032, USD Million

- By End-User- Market Insights and Forecast 2022-2032, USD Million

- By Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- China Body & Comfort Software Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Software Application Domain- Market Insights and Forecast 2022-2032, USD Million

- By Deployment Mode- Market Insights and Forecast 2022-2032, USD Million

- By End-User- Market Insights and Forecast 2022-2032, USD Million

- By Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- China Cross-Vehicle Enablers (Platform Infrastructure) Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Software Application Domain- Market Insights and Forecast 2022-2032, USD Million

- By Deployment Mode- Market Insights and Forecast 2022-2032, USD Million

- By End-User- Market Insights and Forecast 2022-2032, USD Million

- By Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Semiconductor & Computing Platform Providers

- Qualcomm Technologies Inc. (Snapdragon Digital Chassis)

- Business Description

- Service Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- NVIDIA Corporation (NVIDIA DRIVE)

- Business Description

- Service Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Beijing Horizon Information Technology Co. Ltd. (Horizon Robotics)

- Business Description

- Service Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Qualcomm Technologies Inc. (Snapdragon Digital Chassis)

- Vehicle OS, Middleware & Enabler Platform Providers

- Huawei Technologies Co. Ltd (Huawei Intelligent Automotive Solution BU)

- Business Description

- Service Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Baidu Apollo Network (Beijing) Limited (Baidu Apollo)

- Business Description

- Service Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Thunder Software Technology Co. Ltd. (ThunderSoft)

- Business Description

- Service Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Huawei Technologies Co. Ltd (Huawei Intelligent Automotive Solution BU)

- Tier-1 Suppliers with SDV Platform Capabilities

- Huizhou Desay SV Automotive Co. Ltd.

- Business Description

- Service Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Robert Bosch GmbH (Bosch Mobility)

- Business Description

- Service Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Huizhou Desay SV Automotive Co. Ltd.

- OEMs with Proprietary SDV Platforms

- BYD Company Limited

- Business Description

- Service Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- XPeng Inc.

- Business Description

- Service Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- BYD Company Limited

- Cloud & Technology Platform Providers

- Huawei Cloud Computing Technologies Co., Ltd. (Huawei Cloud)

- Business Description

- Service Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Alibaba Cloud Computing Co., Ltd. (Alibaba Cloud)

- Business Description

- Service Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Huawei Cloud Computing Technologies Co., Ltd. (Huawei Cloud)

- Semiconductor & Computing Platform Providers

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Component |

|

| By Software Application Domain |

|

| By Deployment Mode |

|

| By End-User |

|

| By Vehicle Type |

|

| By Region |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.