China Robotaxi Market Report: Trends, Growth and Forecast (2026-2032)

By Level of Autonomy (Level 4, Level 5), By Vehicle Type (Cars, Shuttles/Vans, Purpose-Built Pods, Others), By Propulsion Type (Electric Vehicles (BEV), Hybrid Electric Vehicles (HEV), Fuel Cell Vehicles (FCV)), By Application (Passenger Transportation, Goods Transportation, Others), By Service Type (Ride-Hailing (On-Demand), Station-Based Shuttles, Goods Delivery, Others), By Component Type (LiDAR, Radar (mmWave), Camera, Ultrasonic Sensors, Sensor Fusion Systems, Others), By Region (North, East, Southwest, Northwest, North East, South) ... Read more

|

Major Players

|

China Robotaxi Market Statistics and Insights, 2026

- Market Size Statistics

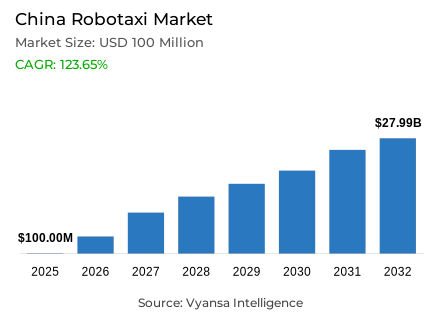

- Robotaxi market size in China was valued at USD 100 million in 2025 and is estimated at USD 110 million in 2026.

- The market size is expected to grow to USD 27.99 billion by 2032.

- Market to register a CAGR of around 123.65% during 2026-32.

- Application Shares

- Passenger transportation grabbed market share of 95%.

- Competition

- Robotaxi in China is currently being catered to by more than 10 companies.

- Top 5 companies acquired around 75% of the market share in 2026.

- AutoX Inc., DiDi Global Inc. (DiDi Autonomous Driving), CaoCao Inc. (CaoCao Mobility), Baidu Inc. (Apollo Go), Guangzhou Pony.ai Technology Co. Ltd. (PonyPilot) etc., are few of the top companies.

- Service Type

- Ride-hailing (on-demand) grabbed 90% of the market.

China Robotaxi Market Outlook

China robotaxi market covers autonomous passenger transport delivered through Level 4 vehicles, fleet platforms, remote assistance systems, and dispatch infrastructure. Users include urban commuters, airport and railway passengers, mobility platforms, transport authorities, and fleet operators. Valued at USD 100 million in 2025, the market is projected to reach USD 110 million in 2026 and USD 27.99 billion by 2032, representing a 123.65% CAGR during 2026-2032. The China robotaxi industry links autonomous driving commercialization with urban transport modernization.

Policy support and mobility infrastructure are accelerating commercial readiness. China is advancing vehicle-road-cloud integration across 20 pilot cities, with more than 35,000 kilometers of test and demonstration roads strengthening connectivity, roadside perception, and cloud-control capabilities. These foundations reduce operating uncertainty for electric autonomous vehicles and expand autonomous vehicle pilot zones. The China robotaxi industry benefits as municipalities convert controlled trials into commercial operating permits, enabling fleet utilization and coverage.

Commercial deployment changes transport economics by removing onboard driver requirements, improving utilization, and centralizing fleet supervision. The robotaxi market in China shifts procurement toward sensors, automotive computing, redundant controls, mapping, cybersecurity, and robotaxi fleet management software. Scaled operations create recurring demand for maintenance, charging, insurance, cleaning, and remote assistance operations. Localized hardware and software improve cost control, shorten replacement cycles, and strengthen platform integration.

Adoption momentum in 2026 centers on fleet expansion, purpose-built robotaxis, service availability, and city coverage. Apollo Go exceeded 22 million cumulative rides by April 2026, reinforcing procurement confidence and operational scale.

China Robotaxi Market Growth Driver

Urban Cost Efficiency Accelerates Commercial Demand

Rising demand for lower-cost, always-available urban transport is accelerating commercial autonomous ride-hailing services across dense metropolitan areas. Fleet operators can spread vehicle, sensor, computing, charging, and supervision costs across longer daily operating windows than conventional taxis. The China robotaxi market gains additional momentum from app-based booking, digital payment, established ride-hailing habits, and growing acceptance of unmanned passenger mobility. These conditions improve route density, shorten idle periods, and support higher asset utilization.

Pony.ai reported in November 2025 that its fleet had reached 961 robotaxis, including 667 seventh-generation vehicles, and remained on track to exceed 1,000 units by year-end. The deployment indicates that mass-produced platforms, lower autonomous driving kit costs, and optimized remote assistance can narrow the cost gap with driver-operated fleets. For the China robotaxi industry, improving robotaxi unit economics strengthens procurement visibility, supports production commitments, and gives operators a clearer pathway from demonstration fleets to scaled paid services.

China Robotaxi Market Challenge

Fragmented Permitting Slows Cross-City Replication

Fragmented municipal permitting, safety assurance requirements, and restricted operating zones slow replication between cities. Operators must validate vehicles, remote assistance procedures, mapping, insurance, data governance, and emergency-response protocols under different local frameworks. The China robotaxi market therefore carries substantial pre-commercial testing costs even when the autonomous driving stack is technically mature. Limited service areas also constrain ride density, reduce fleet utilization, and delay the operating data needed to price risk and prove performance.

Shanghai’s municipal government reported in September 2025 that the city had issued its first eight demonstration operation permits, while its operating model requires autonomous driving companies to partner with taxi operators. That structure supports commercialization but adds coordination, fleet-integration, and compliance obligations before services can scale. Across the China robotaxi industry, similar city-specific rules can extend deployment timelines, complicate standardized fleet procurement, and favor well-capitalized operators with regulatory teams, partners, and sufficient vehicles to absorb validation periods.

Unlock Market Intelligence

Explore the market potential with our data-driven report

China Robotaxi Market Trend

Purpose-Built Fleets Shift Toward Continuous Operations

Purpose-built robotaxis and 24/7 autonomous ride-hailing are reshaping fleet design and operating strategy. Operators increasingly prioritize spacious cabins, redundant control systems, automotive-grade computing, rapid cleaning, predictive maintenance, and software architectures that support continuous dispatch. The China robotaxi market is moving away from small test fleets toward standardized vehicles produced with automotive partners. This shift improves component purchasing leverage, reduces integration complexity, and enables consistent passenger experience across cities, operating windows, and high-demand transport corridors.

WeRide launched 24-hour fully driverless commercial operations with its mass-produced Robotaxi GXR in Guangzhou’s Huangpu District in September 2025. The deployment demonstrates how all-day service, production-ready vehicle platforms, and centralized autonomous fleet control can increase daily trip capacity without extending driver shifts. Within the China robotaxi industry, scaled 24/7 operations strengthen demand for durable sensors, cloud dispatch, charging optimization, cybersecurity, and predictive fleet maintenance, while differentiating operators through availability rather than limited pilot access.

China Robotaxi Market Opportunity

Transport-Hub Expansion Unlocks High-Utilization Routes

Airport, railway-station, and first-mile and last-mile mobility corridors offer an expansion path beyond neighborhood pilots. These routes combine predictable demand, defined pickup points, repeatable road environments, and willingness to pay for reliable transfers. The China robotaxi market can capture higher utilization by linking transport hubs with business districts, areas, and tourism destinations. Operators that secure hub access, integrate booking with mobility platforms, and deploy vehicles with luggage capacity can improve trip density and service differentiation.

Beijing’s government reported in February 2025 that WeRide’s GXR had entered fully driverless commercial service in E-Town, including connections to Beijing South Railway Station and Daxing International Airport, with the city fleet expected to reach several hundred vehicles. This operating model demonstrates scalable demand around transport nodes. For the China robotaxi industry, hub-based deployment expands market access, supports routes, improves vehicle productivity, and creates partnership opportunities with airports, rail operators, taxi groups, and transport authorities.

Unlock Market Intelligence

Explore the market potential with our data-driven report

China Robotaxi Market Segmentation Analysis

By Application

- Passenger Transportation

- Goods Transportation

- Others

Passenger transportation holds a 95% share under application because commercial deployments are structured primarily around urban ride-hailing, airport transfers, railway connections, and designated mobility corridors. Passenger demand offers frequent booking cycles, standardized pickup points, and stronger platform integration than goods-focused operations. The China robotaxi market therefore directs most fleet investment toward cabin safety, passenger interfaces, luggage accommodation, identity verification, route comfort, and emergency communication, reinforcing autonomous passenger transport as the principal revenue-generating application.

Shanghai launched a Level 4 driverless service connecting Shanghai Disney Resort with Pudong International Airport in August 2025, extending autonomous mobility into a high-volume tourism and aviation corridor. The route shows how robotaxis can serve structured passenger flows where origins, destinations, and demand periods are visible. Such deployments strengthen operator planning, support fleet scheduling, and encourage vehicle configurations optimized for passengers rather than cargo, while widening procurement demand for cameras, LiDAR, redundant controls, and in-cabin monitoring systems.

By Service Type

- Ride-Hailing (On-Demand)

- Station-Based Shuttles

- Goods Delivery

- Others

Ride-Hailing (On-Demand) holds a 90% share under service type because digital booking platforms match autonomous vehicles with urban demand. The model supports dynamic dispatch, route optimization, cashless payment, utilization tracking, and service-area expansion without fixed station infrastructure. The China robotaxi market consequently concentrates investment in mobile applications, cloud dispatch, identity verification, passenger support, and automated fleet allocation, giving on-demand services greater scalability and monetization potential than station-based shuttle or delivery formats.

Baidu reported in February 2026 that Apollo Go delivered 3.4 million fully driverless operational rides during the fourth quarter of 2025, with weekly rides exceeding 300,000 and cumulative public rides surpassing 20 million. These volumes demonstrate the operating leverage available through app-based autonomous ride-hailing at scale. High booking frequency generates route data, improves vehicle positioning, supports demand forecasting, and expands fare collection, strengthening platform economics and supplier demand for reliable sensors, automotive computing, connectivity, and fleet-management systems.

List of Companies Covered in China Robotaxi Market

The companies listed below are highly influential in the China robotaxi market, with a significant market share and a strong impact on industry developments.

- AutoX Inc.

- DiDi Global Inc. (DiDi Autonomous Driving)

- CaoCao Inc. (CaoCao Mobility)

- Baidu Inc. (Apollo Go)

- Guangzhou Pony.ai Technology Co. Ltd. (PonyPilot)

- Guangzhou WeRide Technologies Co. Ltd.

- Chenqi Technology Limited (OnTime)

- Enjoygo Technology Limited (SAIC Mobility)

- Shenzhen DeepRoute.ai Co. Ltd. (DeepRoute.ai)

- Nanjing Lingxing Technology Co. Ltd. (T3 Mobility)

Market News & Updates

- Guangzhou WeRide Technologies Co. Ltd., 2026:

WeRide launched the WeRide Go Robotaxi Mini Program on WeChat in China. Residents and visitors in its operating areas can book autonomous rides directly through WeChat without downloading a separate application. The service expands customer access and digital distribution for WeRide’s commercial robotaxi operations in Guangzhou’s Huangpu district and Beijing’s Yizhuang district.

- DiDi Global Inc. (DiDi Autonomous Driving), 2026:

DiDi Autonomous Driving and GAC Aion officially delivered the R2, their jointly developed next-generation robotaxi. The model adds a mass-production-ready vehicle platform designed around autonomous fleet operation rather than conventional private ownership. The delivery supports DiDi’s transition toward standardized robotaxi production, commercial fleet expansion, and integrated autonomous ride-hailing services in China.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- China Robotaxi Market Policies, Regulations, and Standards

- China Robotaxi Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- China Robotaxi Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Level of Autonomy

- Level 4- Market Insights and Forecast 2022-2032, USD Million

- Level 5- Market Insights and Forecast 2022-2032, USD Million

- By Vehicle Type

- Cars- Market Insights and Forecast 2022-2032, USD Million

- Shuttles/Vans- Market Insights and Forecast 2022-2032, USD Million

- Purpose-Built Pods- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Propulsion Type

- Electric Vehicles (BEV)- Market Insights and Forecast 2022-2032, USD Million

- Hybrid Electric Vehicles (HEV)- Market Insights and Forecast 2022-2032, USD Million

- Fuel Cell Vehicles (FCV)- Market Insights and Forecast 2022-2032, USD Million

- By Application

- Passenger Transportation- Market Insights and Forecast 2022-2032, USD Million

- Goods Transportation- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Service Type

- Ride-Hailing (On-Demand)- Market Insights and Forecast 2022-2032, USD Million

- Station-Based Shuttles- Market Insights and Forecast 2022-2032, USD Million

- Goods Delivery- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Component Type

- LiDAR- Market Insights and Forecast 2022-2032, USD Million

- Radar (mmWave)- Market Insights and Forecast 2022-2032, USD Million

- Camera- Market Insights and Forecast 2022-2032, USD Million

- Ultrasonic Sensors- Market Insights and Forecast 2022-2032, USD Million

- Sensor Fusion Systems- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Region

- North- Market Insights and Forecast 2022-2032, USD Million

- East- Market Insights and Forecast 2022-2032, USD Million

- Southwest- Market Insights and Forecast 2022-2032, USD Million

- Northwest- Market Insights and Forecast 2022-2032, USD Million

- North East- Market Insights and Forecast 2022-2032, USD Million

- South- Market Insights and Forecast 2022-2032, USD Million

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Level of Autonomy

- Market Size & Growth Outlook

- China Ride-Hailing (On-Demand) Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- By Propulsion Type- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Service Type- Market Insights and Forecast 2022-2032, USD Million

- By Component Type- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- China Station-Based Shuttles Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- By Propulsion Type- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Service Type- Market Insights and Forecast 2022-2032, USD Million

- By Component Type- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- China Goods Delivery Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- By Propulsion Type- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Service Type- Market Insights and Forecast 2022-2032, USD Million

- By Component Type- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Baidu Inc. (Apollo Go)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Guangzhou Pony.ai Technology Co. Ltd. (PonyPilot)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Guangzhou WeRide Technologies Co. Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Chenqi Technology Limited (OnTime)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Enjoygo Technology Limited (SAIC Mobility)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- AutoX Inc.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- DiDi Global Inc. (DiDi Autonomous Driving)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- CaoCao Inc. (CaoCao Mobility)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Shenzhen DeepRoute.ai Co. Ltd. (DeepRoute.ai)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Nanjing Lingxing Technology Co. Ltd. (T3 Mobility)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Baidu Inc. (Apollo Go)

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Level of Autonomy |

|

| By Vehicle Type |

|

| By Propulsion Type |

|

| By Application |

|

| By Service Type |

|

| By Component Type |

|

| By Region |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.