China Jet Fuel Market Report: Trends, Growth and Forecast (2026-2032)

By Fuel Type (Jet A, Jet B, Others), By Application (Commercial Aviation, Defense Aviation, General Aviation), By Distribution Channel (Into-Plane (On-Airport), Bulk Supply to Fixed-Base Operators (FBO), Military Direct Supply, Others), By Region (North, East, Southwest, Northwest, North East, South) ... Read more

|

Major Players

|

China Jet Fuel Market Statistics and Insights, 2026

- Market Size Statistics

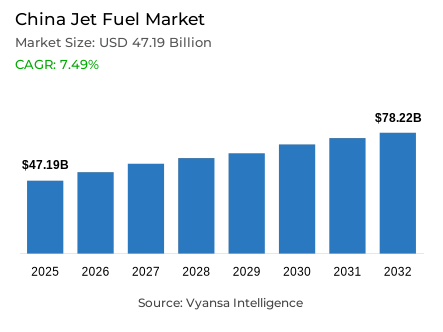

- Jet fuel market size in China was valued at USD 47.19 billion in 2025 and is estimated at USD 51.29 billion in 2026.

- The market size is expected to grow to USD 78.22 billion by 2032.

- Market to register a CAGR of around 7.49% during 2026-32.

- Fuel Type Shares

- Jet a grabbed market share of 90%.

- Competition

- More than 10 companies are actively engaged in producing jet fuel in China.

- Top 5 companies acquired around 50% of the market share in 2026.

- China National Aviation Fuel Group Corporation (including brands), Exxon Mobil Corporation, Shell plc, Sinopec (China Petroleum & Chemical Corporation), PetroChina Company Limited etc., are few of the top companies.

- Application

- Commercial aviation grabbed 80% of the market.

China Jet Fuel Market Outlook

The China jet fuel market size was valued at USD 47.19 billion in 2025 and is projected to grow from USD 51.29 billion in 2026 to USD 78.22 billion by 2032, exhibiting a CAGR of 7.49% during the forecast period. The market is supported by rising air passenger traffic, expanding airline fleets, increasing air cargo transportation, and continued investments in airport infrastructure. As one of the world's largest aviation markets, the China jet fuel market continues to generate substantial demand for aviation turbine fuel across commercial aviation, cargo aviation, defense aviation, and general aviation operations.

According to the US Energy Information Administration (EIA), China's aviation kerosene-type jet fuel consumption averaged approximately 1.27 million barrels per day (b/d) in 2024, increasing from 1.07 million b/d in 2023. This growth reflects the strong recovery of airline operations, higher aircraft utilization rates, and increasing aviation fuel demand across domestic and international routes. The continued expansion of aviation connectivity is strengthening the long-term outlook of the China jet fuel market.

From a fuel type perspective, Jet A accounts for 90% of the China jet fuel market, supported by its widespread use across commercial airline fleets and airport fueling infrastructure. The dominance of Jet A fuel reflects the country's extensive commercial aviation fuel network and established aviation fuel supply chain. The China jet fuel market continues to benefit from investments in airport hydrant fueling systems, aviation fuel storage terminals, and aviation fuel logistics networks that support efficient fuel distribution.

By application, Commercial Aviation holds 80% of the China jet fuel market, driven by rising passenger traffic, growing airline capacity, and extensive domestic and international route networks. The continued expansion of aviation energy infrastructure, airport modernization projects, and airline fleet modernization programs is expected to support sustained growth in the China jet fuel market throughout the forecast period.

China Jet Fuel Market Growth Driver

Rising Air Passenger Traffic

The continued recovery and expansion of air travel remain major growth drivers for the China jet fuel market. According to the Civil Aviation Administration of China (CAAC), China's civil aviation industry transported approximately 731 million passengers in 2024, representing a 17.9% year-on-year increase. Strong domestic travel demand and the gradual recovery of international aviation services continue to support aviation fuel consumption across the country.

The China jet fuel market benefits directly from higher passenger volumes because increased flight frequencies, route expansion, and aircraft utilization rates lead to greater jet fuel consumption. As airlines continue expanding operations and adding capacity, demand for commercial aviation fuel, aircraft fueling services, and aviation fuel distribution is expected to remain strong across China's aviation ecosystem.

China Jet Fuel Market Challenge

Oil Market Volatility and Decarbonization Pressures

A major challenge facing the China jet fuel market is exposure to crude oil price volatility and increasing aviation decarbonization requirements. According to the International Energy Agency (IEA) Oil Market Report June 2026, global oil demand is forecast to decline by 1.1 million barrels per day year-on-year in 2026 due to higher fuel prices and disruptions in fuel consumption patterns.

The China jet fuel market remains closely linked to global petroleum markets because aviation turbine fuel production depends on refinery output and crude oil availability. At the same time, environmental compliance requirements and carbon reduction targets are increasing pressure on airlines and fuel suppliers to invest in sustainable aviation fuel (SAF), renewable jet fuel, and low-carbon aviation fuel solutions. Balancing affordability, supply security, and sustainability objectives remains a significant challenge for the China jet fuel market.

Unlock Market Intelligence

Explore the market potential with our data-driven report

China Jet Fuel Market Trend

Sustainable Aviation Fuel Development

The rapid development of sustainable aviation fuel technologies is emerging as a major trend across the China jet fuel market. China is increasing investments in sustainable aviation fuel (SAF), renewable jet fuel, and alternative aviation fuels to support aviation decarbonization goals. Multiple technology pathways, including Hydroprocessed Esters and Fatty Acids (HEFA), Alcohol-to-Jet (AtJ), Fischer-Tropsch aviation fuel, and Power-to-Liquid (PtL) technologies, are gaining industry attention.

The China jet fuel market is benefiting from this trend because sustainable aviation fuel supports aviation emissions reduction while helping airlines comply with evolving environmental objectives. Growing investments in waste cooking oil aviation fuel production, biojet fuel technologies, and sustainable airline operations are expected to accelerate the transition toward greener aviation fuel solutions across China.

China Jet Fuel Market Opportunity

Expanding Airline Fleets

The continued expansion of commercial aircraft fleets is creating significant opportunities for the China jet fuel market. According to the Civil Aviation Administration of China (CAAC), China's civil aviation industry operated 4,394 registered transport aircraft in 2024, representing an increase of 124 aircraft compared with the previous year. Fleet expansion reflects rising passenger demand, growing cargo aviation activity, and increasing airline investments.

The China jet fuel market is well positioned to benefit from these developments because a larger aircraft fleet directly increases aviation fuel demand, aircraft refueling services, and aviation fuel logistics requirements. In addition, China operated 5,334 scheduled routes in 2024, including 821 international routes, creating long-term opportunities for aviation fuel suppliers, airport operators, and aviation fuel distribution companies throughout the aviation fuel supply chain.

Unlock Market Intelligence

Explore the market potential with our data-driven report

China Jet Fuel Market Segmentation Analysis

By Fuel Type

- Jet A

- Jet B

- Others

Jet A accounts for 90% of the China jet fuel market, making it the dominant fuel type segment. Jet A fuel remains the preferred aviation turbine fuel because it is widely utilized across commercial aviation fleets and supported by extensive airport fueling infrastructure. The fuel's operational reliability, broad availability, and compatibility with modern turbine-powered aircraft continue to support its leadership position.

The China jet fuel market continues to witness strong demand for Jet A fuel due to rising airline fuel consumption, increasing commercial aviation fuel requirements, and expanding aviation connectivity. Continued growth in aircraft operations fuel demand is expected to reinforce the segment's dominance throughout the forecast period.

By Application

- Commercial Aviation

- Defense Aviation

- General Aviation

Commercial aviation represents 80% of the China jet fuel market and remains the largest application segment. The segment benefits from extensive passenger transportation networks, strong airline activity, growing tourism demand, and increasing air cargo transportation volumes. Commercial airlines remain the largest consumers of aviation fuel across China.

The China jet fuel market continues to derive significant demand from commercial aviation because airline operations account for the majority of aircraft fueling activity and jet fuel consumption nationwide. Ongoing fleet modernization, airline route expansion, airport infrastructure development, and rising passenger traffic are expected to support continued growth in commercial aviation fuel demand across the market.

List of Companies Covered in China Jet Fuel Market

The companies listed below are highly influential in the China jet fuel market, with a significant market share and a strong impact on industry developments.

- China National Aviation Fuel Group Corporation (including brands)

- Exxon Mobil Corporation

- Shell plc

- Sinopec (China Petroleum & Chemical Corporation)

- PetroChina Company Limited

- China National Offshore Oil Corporation (including brands)

- Sinochem Holdings Corporation Ltd. (including brands)

- China Aviation Oil (Singapore) Corporation Ltd.

- BP p.l.c.

- TotalEnergies SE

Market News & Updates

- China Petroleum & Chemical Corporation (Sinopec), 2025:

Sinopec advanced the commercialization of Sustainable Aviation Fuel (SAF) produced at its biofuel facilities, supporting the supply of renewable jet fuel for commercial aviation applications. The company continued expanding SAF production capabilities and strengthening China's domestic aviation fuel decarbonization efforts through renewable feedstock processing and aviation fuel distribution initiatives.

- China National Aviation Fuel Group Corporation, 2025:

China National Aviation Fuel Group expanded its aviation fuel infrastructure and fueling operations through investments in airport fuel supply systems, storage facilities, and aviation fuel logistics networks serving major airports across China. The development enhances jet fuel distribution efficiency and strengthens fuel supply security for China's growing commercial aviation sector.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- China Jet Fuel Market Policies, Regulations, and Standards

- China Jet Fuel Production (Million Tons) Trend 2022-2032

- China Jet Fuel Production (Million Tons) Trend By Fuel Type

- Jet A

- Jet B

- Company Wise Production Plants and Statistics

- Installed Production Capacity

- Actual Production

- Planned Production Target

- China Jet Fuel Production (Million Tons) Trend By Fuel Type

- China Jet Fuel Pricing Analysis 2022-2032

- China Jet Fuel Pricing Trend (USD/Million Tons) 2022-2032

- China Jet Fuel Pricing Trend (USD/Million Tons) By Fuel Type 2022-2032

- Jet A

- Jet B

- China Jet Fuel Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- China Jet Fuel Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Tons

- Market Segmentation & Growth Outlook

- By Fuel Type

- Jet A- Market Insights and Forecast 2022-2032, USD Million

- Jet B- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Application

- Commercial Aviation- Market Insights and Forecast 2022-2032, USD Million

- Defense Aviation- Market Insights and Forecast 2022-2032, USD Million

- General Aviation- Market Insights and Forecast 2022-2032, USD Million

- By Distribution Channel

- Into-Plane (On-Airport)- Market Insights and Forecast 2022-2032, USD Million

- Bulk Supply to Fixed-Base Operators (FBO)- Market Insights and Forecast 2022-2032, USD Million

- Military Direct Supply- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Region

- North- Market Insights and Forecast 2022-2032, USD Million

- East- Market Insights and Forecast 2022-2032, USD Million

- Southwest- Market Insights and Forecast 2022-2032, USD Million

- Northwest- Market Insights and Forecast 2022-2032, USD Million

- North East- Market Insights and Forecast 2022-2032, USD Million

- South- Market Insights and Forecast 2022-2032, USD Million

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Fuel Type

- Market Size & Growth Outlook

- China Jet A Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Tons

- Market Segmentation & Growth Outlook

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Distribution Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- China Jet B Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Tons

- Market Segmentation & Growth Outlook

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Distribution Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- China Others Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Tons

- Market Segmentation & Growth Outlook

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Distribution Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Sinopec (China Petroleum & Chemical Corporation)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- PetroChina Company Limited

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- China National Offshore Oil Corporation (including brands)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Sinochem Holdings Corporation Ltd. (including brands)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- China Aviation Oil (Singapore) Corporation Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- China National Aviation Fuel Group Corporation (including brands)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Exxon Mobil Corporation

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Shell plc

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- BP p.l.c.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- TotalEnergies SE

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Sinopec (China Petroleum & Chemical Corporation)

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Fuel Type |

|

| By Application |

|

| By Distribution Channel |

|

| By Region |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.