China In-Vehicle Intrusion Detection Systems Market Report: Trends, Growth and Forecast (2026-2032)

By Component (Hardware, Software, Services), By Deployment (Centralized IDS, Distributed IDS, Hierarchical IDS), By Detection Layer (Network-Based IDS, Host-Based IDS, Hybrid IDS), By Detection Methodology (Signature-Based Detection, Anomaly-Based Detection, Specification-Based Detection, Hybrid Detection), By Vehicle Type (Passenger Cars, Light Commercial Vehicles (LCVs), Heavy Commercial Vehicles (HCVs)), By Communication Interface (CAN (Controller Area Network), LIN (Local Interconnect Network), FlexRay, Automotive Ethernet, Others), By Region (North, East, Southwest, Northwest, North East, South) ... Read more

|

Major Players

|

China In-Vehicle Intrusion Detection Systems Market Statistics and Insights, 2026

- Market Size Statistics

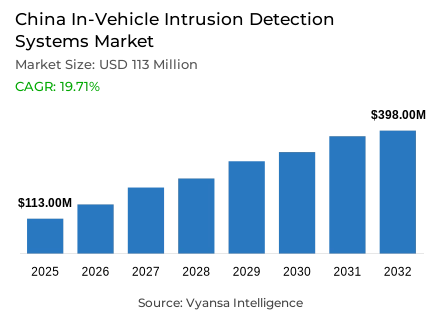

- In-vehicle intrusion detection systems market size in China was valued at USD 113 million in 2025 and is estimated at USD 129 million in 2026.

- The market size is expected to grow to USD 398 million by 2032.

- Market to register a CAGR of around 19.71% during 2026-32.

- Component Shares

- Software grabbed market share of 55%.

- Competition

- More than 10 companies are actively engaged in producing in-vehicle intrusion detection systems in China.

- Top 5 companies acquired around 25% of the market share in 2026.

- Harman International Industries Incorporated (Samsung Electronics Co. Ltd.), Karamba Security Ltd., Upstream Security Ltd., Robert Bosch GmbH (including brands), Continental AG (including brands) etc., are few of the top companies.

- Deployment

- Distributed ids grabbed 45% of the market.

China In-Vehicle Intrusion Detection Systems Market Outlook

The China In-Vehicle Intrusion Detection Systems (IDS) Market was valued at USD 113 million in 2025 and is projected to grow from USD 129 million in 2026 to USD 398 million by 2032, exhibiting a CAGR of 19.71% during the forecast period. Growth is being supported by rapid connected vehicle adoption, expanding electric vehicle production, and increasing integration of software-defined vehicle technologies across the automotive sector. As vehicles become more dependent on telematics, cloud connectivity, vehicle-to-everything communication, and over-the-air software updates, vehicle cybersecurity has become a critical requirement for automakers operating in China's evolving mobility ecosystem.

China's position as the world's largest automotive producer continues to strengthen demand for advanced connected vehicle security solutions. According to the China Association of Automobile Manufacturers (CAAM), vehicle production reached 31.28 million units in 2024. The growing scale of vehicle manufacturing, combined with increasing deployment of intelligent driving functions and connected platforms, is expanding the need for automotive intrusion detection, vehicle network security, and automotive cyber resilience capabilities throughout the industry.

Software holds the largest share of the component segment at 55%, reflecting the growing importance of automotive cybersecurity software, vehicle security analytics, and automotive threat detection platforms. Distributed IDS accounts for 45% of deployment demand, supported by its ability to provide continuous vehicle network monitoring across electronic control units, gateways, telematics modules, and connected applications. These architectures are becoming increasingly important as vehicle software complexity and connectivity continue to increase.

The In-Vehicle Intrusion Detection Systems (IDS) Market is also benefiting from China's investments in intelligent transportation systems, smart mobility initiatives, and software-defined vehicle security frameworks. Growing deployment of connected vehicle ecosystems, AI-enabled vehicle platforms, and secure mobility infrastructure is creating sustained demand for automotive threat intelligence, automotive anomaly detection, and connected vehicle protection solutions across passenger and commercial vehicle segments.

China In-Vehicle Intrusion Detection Systems Market Growth Driver

Connected Vehicle Expansion Increases Security Requirements

The rapid growth of connected and electrified vehicles is a major demand catalyst for the in-vehicle intrusion detection systems (IDS) market. According to China Association of Automobile Manufacturers (CAAM), China sold 12.866 million New Energy Vehicles (NEVs) in 2024, representing approximately 40.9% of total new vehicle sales. These vehicles increasingly rely on telematics, cloud services, software platforms, and connected communication systems, creating a larger cybersecurity attack surface across modern vehicle architectures.

As connected vehicle adoption accelerates, the in-vehicle intrusion detection systems (IDS) market is benefiting from growing requirements for automotive intrusion detection, vehicle cyber protection, and automotive cyber resilience. Automakers are increasingly deploying vehicle security monitoring solutions to identify suspicious activity, improve threat visibility, and strengthen protection across connected vehicle environments.

China In-Vehicle Intrusion Detection Systems Market Challenge

Managing Cybersecurity Across Complex Vehicle Architectures

The growing complexity of modern vehicle networks remains a significant challenge for the in-vehicle intrusion detection systems (IDS) market. Connected vehicles integrate multiple communication interfaces, electronic control units, cloud-connected services, telematics systems, and software platforms that must be continuously protected. Maintaining effective CAN bus security, ECU security, and secure vehicle communications becomes increasingly difficult as vehicle architectures evolve.

The in-vehicle intrusion detection systems (IDS) market also faces implementation challenges associated with regulatory compliance and cybersecurity lifecycle management. UNECE UN R155 requires manufacturers to establish Cyber Security Management Systems (CSMS) capable of identifying and mitigating cybersecurity risks throughout vehicle development and operation. Integrating intrusion detection capabilities while managing vehicle network complexity, validation requirements, and evolving cyber threats continues to increase operational and development burdens for automotive manufacturers.

Unlock Market Intelligence

Explore the market potential with our data-driven report

China In-Vehicle Intrusion Detection Systems Market Trend

AI-Powered Threat Detection Gains Wider Adoption

Artificial intelligence is becoming a defining trend across the in-vehicle intrusion detection systems (IDS) market. China's automotive cybersecurity ecosystem is increasingly adopting AI-powered automotive IDS solutions that combine machine learning cybersecurity, behavioral threat detection, and automotive threat analytics to improve visibility across connected vehicle networks. These technologies enhance the ability to identify both known and previously unseen attack patterns.

The in-vehicle intrusion detection systems (IDS) market is increasingly integrating real-time threat intelligence, vehicle network analytics, and automotive anomaly detection capabilities into vehicle cybersecurity platforms. As software-defined vehicles generate larger volumes of operational and communication data, AI-driven monitoring systems are becoming important tools for strengthening automotive cyber defense and improving cybersecurity response capabilities.

China In-Vehicle Intrusion Detection Systems Market Opportunity

Intelligent Driving Platforms Expand Cybersecurity Demand

The increasing deployment of intelligent driving technologies is creating substantial opportunities for the in-vehicle intrusion detection systems (IDS) market. According to Ministry of Industry and Information Technology (MIIT), the penetration rate of new passenger vehicles equipped with Level 2 driving-assistance functions reached 62.58%. The growing adoption of advanced driver assistance systems, connected mobility solutions, and autonomous driving technologies is increasing cybersecurity requirements throughout the vehicle ecosystem.

The in-vehicle intrusion detection systems (IDS) market is well positioned to benefit because intelligent driving systems depend heavily on software, connectivity, OTA update security, V2X cybersecurity, and real-time data exchange. As automakers continue expanding autonomous vehicle cybersecurity capabilities and smart vehicle protection frameworks, demand for advanced intrusion detection solutions is expected to strengthen significantly across China's automotive industry.

Unlock Market Intelligence

Explore the market potential with our data-driven report

China In-Vehicle Intrusion Detection Systems Market Segmentation Analysis

By Component

- Hardware

- Software

- Services

The segment with the highest share around the component category is software, accounting for approximately 55% of the market. Software-based solutions dominate because modern intrusion detection systems rely on automotive cybersecurity software, automotive threat intelligence engines, vehicle security analytics, and security event management capabilities to identify suspicious behavior across connected vehicle networks.

The in-vehicle intrusion detection systems (IDS) market continues to witness strong adoption of software-driven security platforms because they provide scalability, continuous updates, and enhanced threat visibility. These solutions support automotive threat detection, connected vehicle protection, and cybersecurity monitoring requirements while helping manufacturers maintain secure vehicle operations across increasingly connected environments.

By Deployment

- Centralized IDS

- Distributed IDS

- Hierarchical IDS

The segment with the highest share around the deployment category is distributed IDS, accounting for approximately 45% of the market. Distributed architectures provide localized monitoring across multiple vehicle subsystems, improving visibility into communication channels, gateways, electronic control units, and connected applications. This approach is increasingly important for managing cybersecurity risks across complex vehicle networks.

The in-vehicle intrusion detection systems (IDS) market benefits from distributed deployment models because they enhance vehicle network monitoring, strengthen ECU security, improve CAN bus security visibility, and support faster automotive anomaly detection. As connected vehicle ecosystems continue to expand, distributed IDS solutions remain well aligned with evolving cybersecurity requirements and connected vehicle protection objectives.

List of Companies Covered in China In-Vehicle Intrusion Detection Systems Market

The companies listed below are highly influential in the China in-vehicle intrusion detection systems market, with a significant market share and a strong impact on industry developments.

- Harman International Industries Incorporated (Samsung Electronics Co. Ltd.)

- Karamba Security Ltd.

- Upstream Security Ltd.

- Robert Bosch GmbH (including brands)

- Continental AG (including brands)

- NXP Semiconductors N.V.

- DENSO Corporation

- Aptiv PLC

- GuardKnox Cyber Technologies Ltd.

- Beijing Jingwei Hirain Technologies Co. Ltd.

Market News & Updates

- NXP Semiconductors N.V., 2025:

NXP expanded its automotive cybersecurity portfolio through enhancements to its S32 automotive platform, incorporating advanced intrusion detection, secure in-vehicle networking, and hardware-based security capabilities such as the EdgeLock Secure Enclave and MACsec-enabled communications. The platform is designed to support software-defined vehicles with real-time threat detection and secure vehicle communications. The development strengthens cybersecurity foundations for connected and intelligent vehicles, including deployments within China's rapidly growing software-defined vehicle ecosystem.

- Upstream Security Ltd., 2025:

Upstream Security expanded capabilities within its Cyber XDR platform, enhancing real-time vehicle threat detection, ECU monitoring, anomaly identification, and connected fleet cybersecurity management. The platform utilizes telematics, APIs, and AI-driven analytics to detect malicious activity across vehicle ecosystems. The enhancement supports increasing cybersecurity requirements associated with connected vehicles, electric vehicles, and intelligent mobility platforms across China.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- China In-Vehicle Intrusion Detection Systems (IDS) Market Policies, Regulations, and Standards

- China In-Vehicle Intrusion Detection Systems (IDS) Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- China In-Vehicle Intrusion Detection Systems (IDS) Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Component

- Hardware- Market Insights and Forecast 2022-2032, USD Million

- Software- Market Insights and Forecast 2022-2032, USD Million

- Services- Market Insights and Forecast 2022-2032, USD Million

- By Deployment

- Centralized IDS- Market Insights and Forecast 2022-2032, USD Million

- Distributed IDS- Market Insights and Forecast 2022-2032, USD Million

- Hierarchical IDS- Market Insights and Forecast 2022-2032, USD Million

- By Detection Layer

- Network-Based IDS- Market Insights and Forecast 2022-2032, USD Million

- Host-Based IDS- Market Insights and Forecast 2022-2032, USD Million

- Hybrid IDS- Market Insights and Forecast 2022-2032, USD Million

- By Detection Methodology

- Signature-Based Detection- Market Insights and Forecast 2022-2032, USD Million

- Anomaly-Based Detection- Market Insights and Forecast 2022-2032, USD Million

- Specification-Based Detection- Market Insights and Forecast 2022-2032, USD Million

- Hybrid Detection- Market Insights and Forecast 2022-2032, USD Million

- By Vehicle Type

- Passenger Cars- Market Insights and Forecast 2022-2032, USD Million

- Light Commercial Vehicles (LCVs)- Market Insights and Forecast 2022-2032, USD Million

- Heavy Commercial Vehicles (HCVs)- Market Insights and Forecast 2022-2032, USD Million

- By Communication Interface

- CAN (Controller Area Network)- Market Insights and Forecast 2022-2032, USD Million

- LIN (Local Interconnect Network)- Market Insights and Forecast 2022-2032, USD Million

- FlexRay- Market Insights and Forecast 2022-2032, USD Million

- Automotive Ethernet- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Region

- North- Market Insights and Forecast 2022-2032, USD Million

- East- Market Insights and Forecast 2022-2032, USD Million

- Southwest- Market Insights and Forecast 2022-2032, USD Million

- Northwest- Market Insights and Forecast 2022-2032, USD Million

- North East- Market Insights and Forecast 2022-2032, USD Million

- South- Market Insights and Forecast 2022-2032, USD Million

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Component

- Market Size & Growth Outlook

- China Hardware Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Deployment- Market Insights and Forecast 2022-2032, USD Million

- By Detection Layer- Market Insights and Forecast 2022-2032, USD Million

- By Detection Methodology- Market Insights and Forecast 2022-2032, USD Million

- By Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- By Communication Interface- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- China Software Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Deployment- Market Insights and Forecast 2022-2032, USD Million

- By Detection Layer- Market Insights and Forecast 2022-2032, USD Million

- By Detection Methodology- Market Insights and Forecast 2022-2032, USD Million

- By Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- By Communication Interface- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- China Services Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Deployment- Market Insights and Forecast 2022-2032, USD Million

- By Detection Layer- Market Insights and Forecast 2022-2032, USD Million

- By Detection Methodology- Market Insights and Forecast 2022-2032, USD Million

- By Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- By Communication Interface- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Robert Bosch GmbH (including brands)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Continental AG (including brands)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Forvia SE (including brands)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- NXP Semiconductors N.V.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- DENSO Corporation

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Aptiv PLC

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Harman International Industries Incorporated (Samsung Electronics Co. Ltd.)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Karamba Security Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Upstream Security Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- GuardKnox Cyber Technologies Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Robert Bosch GmbH (including brands)

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Component |

|

| By Deployment |

|

| By Detection Layer |

|

| By Detection Methodology |

|

| By Vehicle Type |

|

| By Communication Interface |

|

| By Region |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.