Australia Plant-Based Dairy Market Report: Trends, Growth and Forecast (2026-2032)

By Product Type (Plant-Based Milk (Soy Drinks, Almond, Blends, Coconut, Oat, Rice, Other Plant-Based Milk), Plant-Based Yoghurt, Plant-Based Cheese), By Sales Channel (Retail Offline (Grocery Retailers, Convenience Retailers, Supermarkets, Hypermarkets), Retail Online) ... Read more

|

Major Players

|

Australia Plant-Based Dairy Market Statistics and Insights, 2026

- Market Size Statistics

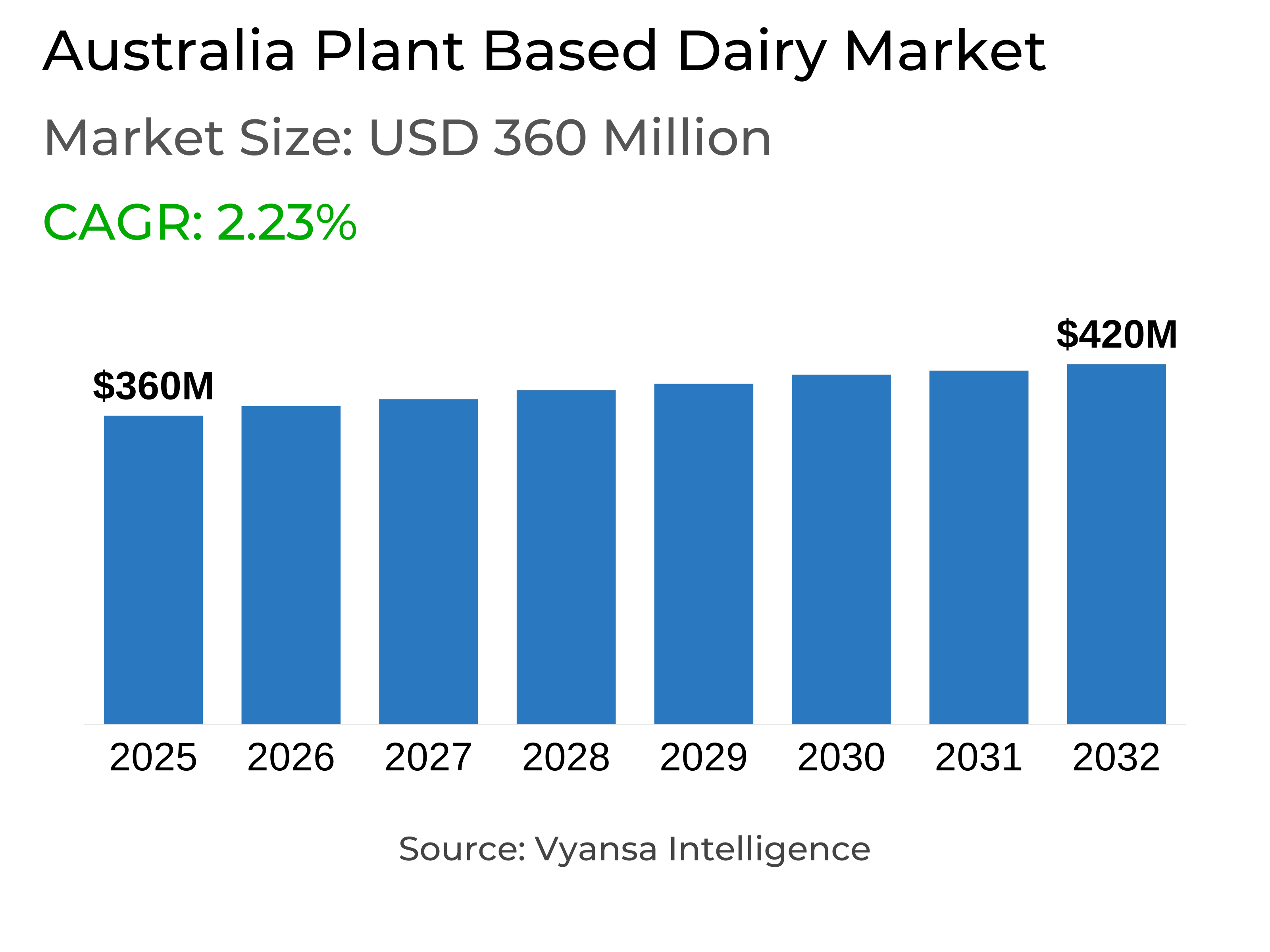

- Plant-Based Dairy in Australia is estimated at $ 360 Million.

- The market size is expected to grow to $ 420 Million by 2032.

- Market to register a CAGR of around 2.23% during 2026-32.

- Product Type Shares

- Plant-Based Milk grabbed market share of 75%.

- Competition

- More than 15 companies are actively engaged in producing Plant-Based Dairy in Australia.

- Top 5 companies acquired around 75% of the market share.

- Spiral Foods Pty Ltd, Woolworths Group Ltd, CO YO Pty Ltd, Sanitarium Health Food Co, The, Vitasoy Australia Products Pty Ltd etc., are few of the top companies.

- Sales Channel

- Retail Offline grabbed 80% of the market.

Australia Plant-Based Dairy Market Outlook

The plant-based dairy market in Australia is estimated at $360 million IN 2025 and is expected to grow to $420 million by 2032. More than 15 companies are actively engaged in producing plant-based dairy, with the top five players capturing around 75% of the market share. Retail offline channels dominate the market, accounting for approximately 80% of sales, supported by supermarkets such as Coles and Woolworths, which have expanded their plant-based offerings to meet rising consumer demand. Wood-based milk, oat, and coconut varieties remain popular, with functional health benefits and allergen-friendly options driving growth.

Plant-based milk continues to be the largest category, with barista-style oat milk emerging as a key growth driver. Consumers increasingly seek café-quality experiences at home, while fortified formulations offering bone, heart, and immune health benefits are attracting health-conscious buyers. Coconut milk and nut-based alternatives, such as walnut and tiger nut, are also gaining traction for their natural flavours, clean-label attributes, and digestive benefits. Brands like Sanitarium, Noumi, and Vitasoy are leading innovation in both functional and indulgent formats, strengthening the market’s credibility.

Plant-based yoghurt, cheese, and spreads are expanding beyond niche segments. Innovations in meltability, texture, and protein content are appealing to flexitarian consumers, while Greek-style and high-protein yoghurts are gaining popularity among gut health-focused shoppers. Convenience-driven formats, such as single-serve pouches and portion-controlled packs, are expected to support adoption in households and on-the-go occasions. Private labels are also expanding, offering nutrient-enriched and low-cholesterol options at competitive prices.

E-commerce is expected to play an increasingly important role in the plant-based dairy market, complementing offline retail. Online channels provide discovery, education, and personalised engagement, while fast-delivery services like MILKRUN and DoorDash enhance convenience. Looking ahead, the market is likely to benefit from innovations in functional nutrition, clean-label ingredients, and emerging technologies such as precision fermentation, further strengthening plant-based dairy as a mainstream, health-forward alternative in Australia.

Australia Plant-Based Dairy Market Growth Driver

Rising Focus on Health and Wellness Supporting Functional Innovation

Health and wellness remain the primary force driving growth in plant-based dairy, as end users increasingly seek products that provide tangible nutritional benefits. Brands like Sanitarium and Vitasoy strengthen their portfolios with fortified formulations addressing specific needs such as bone health, cholesterol management, and immune support. The growing preference for functional, science-backed products reflects a shift toward proactive wellness rather than simple substitution.

This focus on functionality enhances trust and positions plant-based dairy as a credible everyday nutrition source. The category’s success lies in its ability to merge health, taste, and convenience, appealing to a broad spectrum of consumers who prioritise wellbeing in their dietary choices. As brands continue to invest in clinically supported innovations, plant-based dairy secures its role as a mainstream health-focused alternative in Australia’s evolving food landscape.

Australia Plant-Based Dairy Market Challenge

Structural Instability in Traditional Dairy Supply Chains

The plant-based dairy sector faces challenges linked to the instability of traditional dairy supply chains, which shape market dynamics and consumer behaviour. Ongoing farm consolidation, rising production costs, and climate-related volatility continue to pressure Australia’s conventional dairy production, leading to higher prices and unstable supply conditions.

While this situation creates opportunities for plant-based alternatives, it also introduces competitive and operational hurdles. As traditional dairy becomes less reliable, plant-based producers must ensure scalability, cost efficiency, and consistent product quality to maintain momentum. The challenge lies in balancing growth with sustainable sourcing and efficient manufacturing, as the industry works to meet rising demand without compromising affordability or availability.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Australia Plant-Based Dairy Market Trend

Shift Toward Flexitarian and Function-Oriented Consumption

Flexitarian consumption patterns are shaping the plant-based dairy segment, with end users prioritizing health, sustainability, and taste in their diets. Instead of fully eliminating animal-based dairy, consumers are adopting plant-forward diets that integrate alternatives offering better nutrition and sensory performance.

Brands are responding with premium, function-led innovations such as oat-coconut yoghurt blends and plant-based spreads that replicate traditional dairy experiences while offering health benefits. This reflects a broader movement from simple substitution to value-driven, experience-based consumption. As flexitarian lifestyles expand, plant-based dairy is moving beyond niche appeal to become a regular part of mainstream diets, signalling deeper consumer engagement and long-term category maturity

Australia Plant-Based Dairy Market Opportunity

Technological Advancements Redefining Dairy Alternatives

Advancements in precision fermentation and lab-grown dairy proteins are expected to drive significant innovation within the plant-based dairy segment. These technologies allow the creation of bio-identical proteins like casein and whey without animal agriculture, offering benefits such as reduced carbon emissions, improved purity, and enhanced functionality.

Companies like Fonterra and All G are already investing in this space, signalling growing industry readiness for large-scale adoption. As regulatory frameworks mature and production costs decline, these innovations are likely to move from niche applications to mainstream manufacturing. This technological shift is expected to elevate plant-based dairy into a new era of sustainability and performance, strengthening Australia’s position as a global leader in advanced, science-driven dairy alternatives.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Australia Plant-Based Dairy Market Segmentation Analysis

By Product Type

- Plant-Based Milk

- Plant-Based Yoghurt

- Plant-Based Cheese

The segment with the highest market share under the Product Type is Plant-Based Milk, which grabbed a market share of 75%. Plant-based milk remains the largest and most established category in Australia, driven by the rising popularity of barista-style formats, particularly oat-based. These creamier, froth-friendly products allow consumers to replicate café-quality coffee at home, making them a key entry point for broader plant-based adoption. Health and wellness positioning, including functional benefits such as added calcium, protein, and cholesterol-lowering formulations, continues to underpin growth across branded and private label ranges.

Beyond traditional bases like soy, oat, and almond, emerging options such as walnut, tiger nut, and coconut are attracting health-conscious and allergen-friendly consumers. The category also benefits from strong innovation in formats and flavours, along with premium sensory appeal, ensuring that plant-based milk remains the primary driver of value in Australia plant-based dairy market during the forecast period.

By Sales Channel

- Retail Offline

- Retail Online

The segment with the highest market share under the sales channel is Retail Offline, which grabbed 80% of the market. Supermarkets and hypermarkets remain the dominant sales channels for plant-based dairy in Australia, offering wide product assortments, elevated shelf visibility, and strategic brand collaborations. Retailers such as Coles and Woolworths have expanded plant-based ranges to include nutrient-enriched SKUs, private label offerings, and innovative formats, helping meet the growing demand from flexitarians and health-conscious consumers.

Offline retail continues to benefit from consumer preference for immediate access, the ability to compare products, and in-store engagement with new formats and flavours. While e-commerce is growing in importance for convenience and personalised offerings, the physical store remains the key channel for driving trial, building trust, and securing repeat purchases in the Australian plant-based dairy market throughout the forecast period.

Top Companies in Australia Plant-Based Dairy Market

The top companies operating in the market include Spiral Foods Pty Ltd, Woolworths Group Ltd, CO YO Pty Ltd, Sanitarium Health Food Co, The, Vitasoy Australia Products Pty Ltd, Noumi Ltd, Made (Aust) Pty Ltd, Ceres Natural Foods Pty Ltd, Aldi Stores Supermarkets Pty Ltd, Cale & Daughters Pty Ltd, etc., are the top players operating in the Australia Plant-Based Dairy Market.

Frequently Asked Questions

Related Report

1. Market Segmentation

1.1. Research Scope

1.2. Research Methodology

1.3. Definitions and Assumptions

2. Executive Summary

3. Australia Plant-Based Dairy Market Policies, Regulations, and Standards

4. Australia Plant-Based Dairy Market Dynamics

4.1. Growth Factors

4.2. Challenges

4.3. Trends

4.4. Opportunities

5. Australia Plant-Based Dairy Market Statistics, 2022-2032F

5.1. Market Size & Growth Outlook

5.1.1.By Revenues in US$ Million

5.2. Market Segmentation & Growth Outlook

5.2.1.By Product Type

5.2.1.1. Plant-Based Milk- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.1. Soy Drinks- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.2. Almond- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.3. Blends- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.4. Coconut- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.5. Oat- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.6. Rice- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.7. Other Plant-Based Milk- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2. Plant-Based Yoghurt- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3. Plant-Based Cheese- Market Insights and Forecast 2022-2032, USD Million

5.2.2.By Sales Channel

5.2.2.1. Retail Offline- Market Insights and Forecast 2022-2032, USD Million

5.2.2.1.1. Grocery Retailers- Market Insights and Forecast 2022-2032, USD Million

5.2.2.1.2. Convenience Retailers- Market Insights and Forecast 2022-2032, USD Million

5.2.2.1.3. Supermarkets- Market Insights and Forecast 2022-2032, USD Million

5.2.2.1.4. Hypermarkets- Market Insights and Forecast 2022-2032, USD Million

5.2.2.2. Retail Online- Market Insights and Forecast 2022-2032, USD Million

5.2.3.By Competitors

5.2.3.1. Competition Characteristics

5.2.3.2. Market Share & Analysis

6. Australia Plant-Based Milk Market Outlook, 2022-2032F

6.1. Market Size & Growth Outlook

6.1.1.By Revenues in US$ Million

6.2. Market Segmentation & Growth Outlook

6.2.1.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

7. Australia Plant-Based Yoghurt Market Outlook, 2022-2032F

7.1. Market Size & Growth Outlook

7.1.1.By Revenues in US$ Million

7.2. Market Segmentation & Growth Outlook

7.2.1.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

8. Australia Plant-Based Cheese Market Outlook, 2022-2032F

8.1. Market Size & Growth Outlook

8.1.1.By Revenues in US$ Million

8.2. Market Segmentation & Growth Outlook

8.2.1.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

9. Competitive Outlook

9.1. Company Profiles

9.1.1.Sanitarium Health Food Co

9.1.1.1. Business Description

9.1.1.2. Product Portfolio

9.1.1.3. Collaborations & Alliances

9.1.1.4. Recent Developments

9.1.1.5. Financial Details

9.1.1.6. Others

9.1.2.The Vitasoy Australia Products Pty Ltd

9.1.2.1. Business Description

9.1.2.2. Product Portfolio

9.1.2.3. Collaborations & Alliances

9.1.2.4. Recent Developments

9.1.2.5. Financial Details

9.1.2.6. Others

9.1.3.Noumi Ltd

9.1.3.1. Business Description

9.1.3.2. Product Portfolio

9.1.3.3. Collaborations & Alliances

9.1.3.4. Recent Developments

9.1.3.5. Financial Details

9.1.3.6. Others

9.1.4.Made (Aust) Pty Ltd

9.1.4.1. Business Description

9.1.4.2. Product Portfolio

9.1.4.3. Collaborations & Alliances

9.1.4.4. Recent Developments

9.1.4.5. Financial Details

9.1.4.6. Others

9.1.5.Ceres Natural Foods Pty Ltd

9.1.5.1. Business Description

9.1.5.2. Product Portfolio

9.1.5.3. Collaborations & Alliances

9.1.5.4. Recent Developments

9.1.5.5. Financial Details

9.1.5.6. Others

9.1.6.Spiral Foods Pty Ltd

9.1.6.1. Business Description

9.1.6.2. Product Portfolio

9.1.6.3. Collaborations & Alliances

9.1.6.4. Recent Developments

9.1.6.5. Financial Details

9.1.6.6. Others

9.1.7.Woolworths Group Ltd

9.1.7.1. Business Description

9.1.7.2. Product Portfolio

9.1.7.3. Collaborations & Alliances

9.1.7.4. Recent Developments

9.1.7.5. Financial Details

9.1.7.6. Others

9.1.8.CO YO Pty Ltd

9.1.8.1. Business Description

9.1.8.2. Product Portfolio

9.1.8.3. Collaborations & Alliances

9.1.8.4. Recent Developments

9.1.8.5. Financial Details

9.1.8.6. Others

9.1.9.Aldi Stores Supermarkets Pty Ltd

9.1.9.1. Business Description

9.1.9.2. Product Portfolio

9.1.9.3. Collaborations & Alliances

9.1.9.4. Recent Developments

9.1.9.5. Financial Details

9.1.9.6. Others

9.1.10. Cale & Daughters Pty Ltd

9.1.10.1. Business Description

9.1.10.2. Product Portfolio

9.1.10.3. Collaborations & Alliances

9.1.10.4. Recent Developments

9.1.10.5. Financial Details

9.1.10.6. Others

10. Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Product Type |

|

| By Sales Channel |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.