Australia Jewellery Market Report: Trends, Growth and Forecast (2026-2032)

Category (Costume Jewellery, Fine Jewellery), Type (Earrings, Neckwear, Rings, Wristwear, Other), Collection (Diamond, Non-Diamond), Material Type (Gold, Platinum, Metal Combination, Silver), Sales Channel (Retail Offline, Retail Online), End User (Men, Women) ... Read more

|

Major Players

|

Australia Jewellery Market Statistics and Insights, 2026

- Market Size Statistics

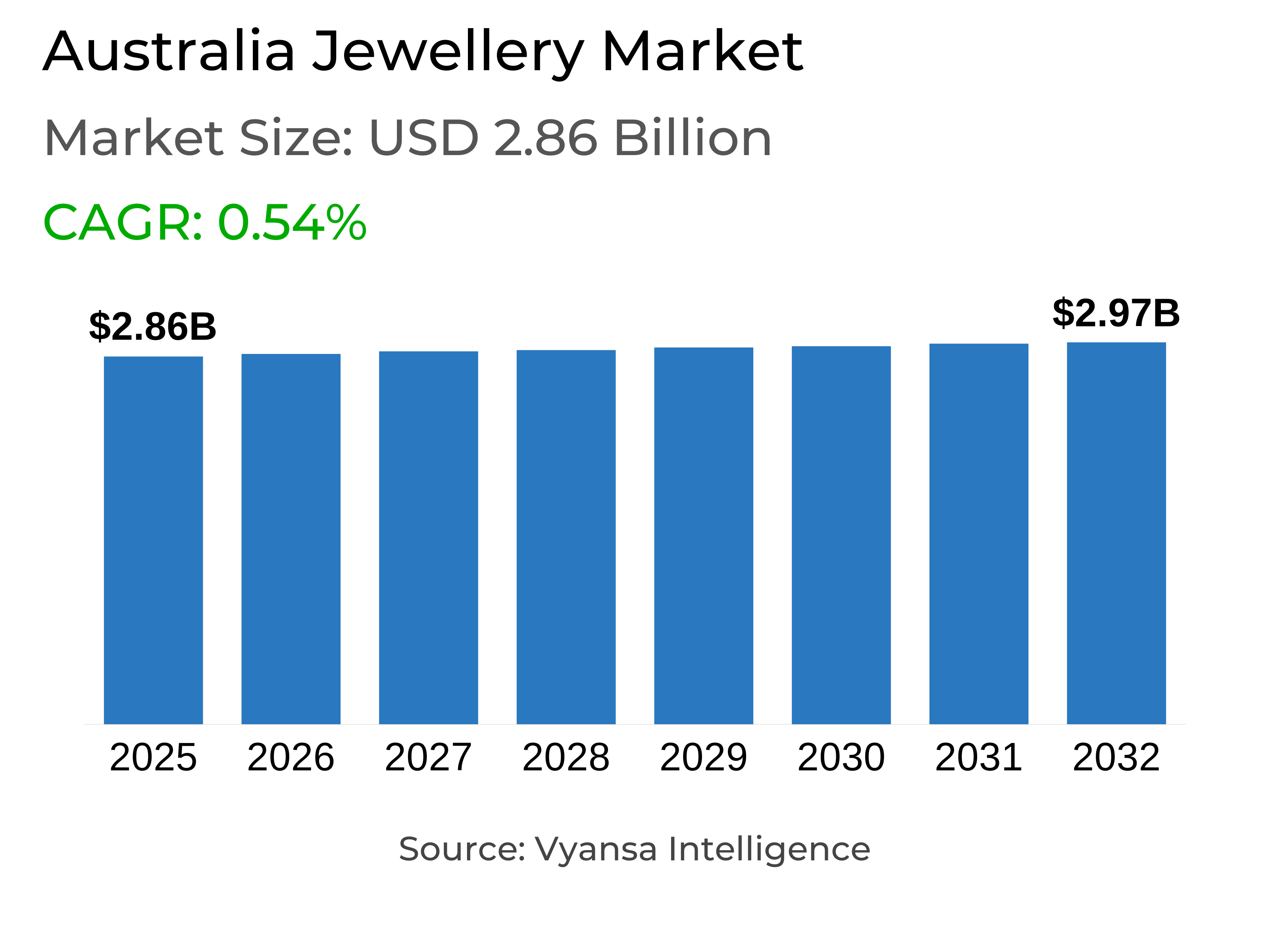

- Jewellery in australia is estimated at USD 2.86 billion.

- The market size is expected to grow to USD 2.97 billion by 2032.

- Market to register a cagr of around 0.54% during 2026-32.

- Category Shares

- Fine jewellery grabbed market share of 80%.

- Competition

- More than 15 companies are actively engaged in producing jewellery in australia.

- Top 5 companies acquired around 25% of the market share.

- Duraflex Group Australia, Tiffany & Co, The Jewellery Group Pty Ltd, Michael Hill Jeweller (Australia) Pty Ltd, Pandora Jewelry Pty Ltd etc., are few of the top companies.

- Sales Channel

- Retail offline grabbed 80% of the market.

Australia Jewellery Market Outlook

The jewellery market in Australia is worth around USD 2.86 billion and is anticipated to rise to around USD 2.97 billion by 2032, at a CAGR of around 0.54%. End users are becoming confident and are again spending on jewellery rather than saving. This recovery in buying habits shows a positive shift in demand. Fine jewellery, with around 80% market share, continues to lead the market as people prefer high quality, long lasting pieces that hold emotional value.

Rising prices of gold, diamonds, and labor continue to be a problem for most jewellers. The higher prices make it more difficult to maintain profit margins as well as plan production. Smaller brands struggle to cope with these variations, whereas larger players concentrate on premium collection in order to maintain sales. Nevertheless, consistent demand for luxury jewellery as well as emotional purchases such as engagement or bridal jewellery keep the market stable.

The competition in the Australia jewellery market is moderately concentrated, and the top five players control around 25% of the market. Local and international brands compete by selling diverse designs, new materials, and improved shopping experiences. Most brands are investing in digital tools as well as omnichannel approaches to enhance end user reach. This competitive environment promotes innovation, product quality, and stronger end user loyalty.

Retail offline channels continue to dominate, accounting for around 80% of overall jewellery sales, as end users still prefer in-store purchases for major occasions. Retail offline storesallow customers to see and personalise products with expert help. Moreover, retail online jewellery is growing with convenience and better platforms. While more casual purchases are shifting online, offline stores will continue to lead, supported by trust, service, and personalised experiences.

Australia Jewellery Market Growth DriverGrowing Interest in Jewellery Strengthens the Market

End users are becoming more confident as they spend more money on jewellery rather than saving, demonstrating an evident turn around in purchase habits and trust in the market. Retail sales are improving gradually, and fine jewellery is growing faster than costume jewellery as people opt for high quality products. Most end users are opting for nicely made and durable products that hold value over time. This shift in mindset indicates that end users are increasingly emphasizing significant purchases over short term savings.The steady rise in jewellery buying highlights growing confidence and a stronger base for market stability and demand.

Even though higher costs for materials, diamonds, and labour continue to affect the trade, interest in fine jewellery keeps increasing. End users are returning to planned, emotional, and celebratory purchases, helping retailers improve their overall performance. The steady expenditure by end users shows a stable recovery path that indicates better future prospects for the jewellery sector.

Australia Jewellery Market ChallengeRising Material Costs Reduce Profits

Jewellery manufacturers are struggling with increasing costs of gold, diamonds, and other materials. These costs keep fluctuating, making it difficult for them to plan production or keep stable prices for end users. As material prices rise all over the world, most retailers are unable to raise their prices at the same rate, and this lowers their profit margins. This problem hits every supply chain agent, including manufacturers and shopkeepers, and makes daily business planning more difficult.

The increasing price of materials and labor is also forcing most brands to reduce their product lines or concentrate on limited collections. Small companies are worst hit since they cannot easily adapt to large price fluctuations. These issues prevent firms from investing in new designs and make it more difficult for the jewellery sector to remain competitive in the market.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Australia Jewellery Market TrendChanging Fashion Preferences Influence Jewellery Demand

End users are showing new preferences that keep influencing the jewellery market. Most of them now seek affordable alternatives such as lab created diamonds, which are gaining strong interest due to their quality and reduced price tag. Their demand continues to increase, predominantly among young end users who find enjoyment in modern and affordable accessories. Companies are also creating more male and unisex jewellery, driven by changing fashion and gender norms. Most male end users aged 20 to 40 years today opt for simple yet fashion forward designs, usually purchasing through retail online platforms for convenience.

Retailers are becoming more responsive to short-term fashion ideas, inspired by popular styles such as the “Barbiecore” look or celebrity influence. Capsule and fast fashion jewellery collections are keeping brands in the spotlight. These changes illustrate how the industry continues to evolve to catch up with changing tastes of modern end users

Australia Jewellery Market OpportunityEconomic Revival to Encourage Jewellery Spending

The jewellery industry will experience new growth as the economy begins to recover. High quality jewellery will do well since more end users will be willing to spend. Since the price of diamonds is likely to stabilize and gold retains its value, brands will feel more confident in introducing new designs. The improved economic situations will contribute to greater sales and more equilibrium in the market in the next few years.

Moreover, with growing confidence levels of end users and a slow end to the retail slowdown will create favourable spending conditions. More numbers of end users will shift from saving to purchasing jewellery for special occasions and gifts. This shift will create strong business opportunities for retailers as well as producers as the market moves toward steady and healthy growth.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Australia Jewellery Market Segmentation Analysis

By Category

- Costume Jewellery

- Fine Jewellery

Fine jewellery segment has the largest market share, accounting for around 80% of the overall jewellery market. Fine jewellery is favored by end users due to its enhanced quality, longevity, and emotional value. The high demand for gold and diamond designs keeps this segment strong, as people often buy them for special events or gifts. More end users are now ready to spend on long-lasting and luxury pieces, helping fine jewellery stay ahead in the market.

Costume jewellery has a smaller share and faces more price pressure. It attracts younger end users who follow fashion trends, but frequent style changes and low profit margins make it less stable. Because of this, fine jewellery continues to lead the market and remains the main segment for overall growth.

By Sales Channel

- Retail Offline

- Retail Online

The retail offline segment has the highest share, holding around 80% of the total jewellery sales. The majority of end users continue to prefer purchasing jewellery offline, particularly for significant purchases such as engagement or bridal pieces. Retail offline enable the customer to see, feel, and personalise the product, with professional assistance from sales associates while making the decision. This personal connection and trust make retail offline stores the leading choice for many end users.

Meanwhile, retail online is expanding as more brands enhance their websites. End users today have the convenience of viewing collections or creating designs online before they go to the store. Although more relaxed or lower ticket purchases move online, retail offline will remain the dominant force for the jewellery industry, backed by strong customer relationships and personalised service.

Top Companies in Australia Jewellery Market

The top companies operating in the market include Duraflex Group Australia, Tiffany & Co, The Jewellery Group Pty Ltd, Michael Hill Jeweller (Australia) Pty Ltd, Pandora Jewelry Pty Ltd, Lovisa Holdings Ltd, Richemont Australia Pty Ltd, Swarovski International (Australia) Pty Ltd, Peter W Beck Pty Ltd, Bulgari Australia Pty Ltd, etc., are the top players operating in the australia jewellery market.

Frequently Asked Questions

Related Report

1. Market Segmentation

1.1. Research Scope

1.2. Research Methodology

1.3. Definitions and Assumptions

2. Executive Summary

3. Australia Jewellery Market Policies, Regulations, and Standards

4. Australia Jewellery Market Dynamics

4.1. Growth Factors

4.2. Challenges

4.3. Trends

4.4. Opportunities

5. Australia Jewellery Market Statistics, 2022-2032F

5.1. Market Size & Growth Outlook

5.1.1.By Revenues in US$ Million

5.2. Market Segmentation & Growth Outlook

5.2.1.By Category

5.2.1.1. Costume Jewellery- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2. Fine Jewellery- Market Insights and Forecast 2022-2032, USD Million

5.2.2.By Type

5.2.2.1. Earrings- Market Insights and Forecast 2022-2032, USD Million

5.2.2.2. Neckwear- Market Insights and Forecast 2022-2032, USD Million

5.2.2.3. Rings- Market Insights and Forecast 2022-2032, USD Million

5.2.2.4. Wristwear- Market Insights and Forecast 2022-2032, USD Million

5.2.2.5. Other- Market Insights and Forecast 2022-2032, USD Million

5.2.3.By Collection

5.2.3.1. Diamond- Market Insights and Forecast 2022-2032, USD Million

5.2.3.2. Non-Diamond- Market Insights and Forecast 2022-2032, USD Million

5.2.4.By Material Type

5.2.4.1. Gold- Market Insights and Forecast 2022-2032, USD Million

5.2.4.2. Platinum- Market Insights and Forecast 2022-2032, USD Million

5.2.4.3. Metal Combination- Market Insights and Forecast 2022-2032, USD Million

5.2.4.4. Silver- Market Insights and Forecast 2022-2032, USD Million

5.2.5.By Sales Channel

5.2.5.1. Retail Offline- Market Insights and Forecast 2022-2032, USD Million

5.2.5.2. Retail Online- Market Insights and Forecast 2022-2032, USD Million

5.2.6.By End User

5.2.6.1. Men- Market Insights and Forecast 2022-2032, USD Million

5.2.6.2. Women- Market Insights and Forecast 2022-2032, USD Million

5.2.7.By Competitors

5.2.7.1. Competition Characteristics

5.2.7.2. Market Share & Analysis

6. Australia Costume Jewellery Market Statistics, 2022-2032

6.1. Market Size & Growth Outlook

6.1.1.By Revenues in US$ Million

6.2. Market Segmentation & Growth Outlook

6.2.1.By Type- Market Insights and Forecast 2022-2032, USD Million

6.2.2.By Collection- Market Insights and Forecast 2022-2032, USD Million

6.2.3.By Material Type- Market Insights and Forecast 2022-2032, USD Million

6.2.4.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

6.2.5.By End User- Market Insights and Forecast 2022-2032, USD Million

7. Australia Fine Jewellery Market Statistics, 2022-2032

7.1. Market Size & Growth Outlook

7.1.1.By Revenues in US$ Million

7.2. Market Segmentation & Growth Outlook

7.2.1.By Type- Market Insights and Forecast 2022-2032, USD Million

7.2.2.By Collection- Market Insights and Forecast 2022-2032, USD Million

7.2.3.By Material Type- Market Insights and Forecast 2022-2032, USD Million

7.2.4.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

7.2.5.By End User- Market Insights and Forecast 2022-2032, USD Million

8. Competitive Outlook

8.1. Company Profiles

8.1.1.Michael Hill Jeweller (Australia) Pty Ltd

8.1.1.1. Business Description

8.1.1.2. Product Portfolio

8.1.1.3. Collaborations & Alliances

8.1.1.4. Recent Developments

8.1.1.5. Financial Details

8.1.1.6. Others

8.1.2.Pandora Jewelry Pty Ltd

8.1.2.1. Business Description

8.1.2.2. Product Portfolio

8.1.2.3. Collaborations & Alliances

8.1.2.4. Recent Developments

8.1.2.5. Financial Details

8.1.2.6. Others

8.1.3.Lovisa Holdings Ltd

8.1.3.1. Business Description

8.1.3.2. Product Portfolio

8.1.3.3. Collaborations & Alliances

8.1.3.4. Recent Developments

8.1.3.5. Financial Details

8.1.3.6. Others

8.1.4.Richemont Australia Pty Ltd

8.1.4.1. Business Description

8.1.4.2. Product Portfolio

8.1.4.3. Collaborations & Alliances

8.1.4.4. Recent Developments

8.1.4.5. Financial Details

8.1.4.6. Others

8.1.5.Swarovski International (Australia) Pty Ltd

8.1.5.1. Business Description

8.1.5.2. Product Portfolio

8.1.5.3. Collaborations & Alliances

8.1.5.4. Recent Developments

8.1.5.5. Financial Details

8.1.5.6. Others

8.1.6.Duraflex Group Australia

8.1.6.1. Business Description

8.1.6.2. Product Portfolio

8.1.6.3. Collaborations & Alliances

8.1.6.4. Recent Developments

8.1.6.5. Financial Details

8.1.6.6. Others

8.1.7.Tiffany & Co

8.1.7.1. Business Description

8.1.7.2. Product Portfolio

8.1.7.3. Collaborations & Alliances

8.1.7.4. Recent Developments

8.1.7.5. Financial Details

8.1.7.6. Others

8.1.8.Jewellery Group Pty Ltd, The

8.1.8.1. Business Description

8.1.8.2. Product Portfolio

8.1.8.3. Collaborations & Alliances

8.1.8.4. Recent Developments

8.1.8.5. Financial Details

8.1.8.6. Others

8.1.9.Peter W Beck Pty Ltd

8.1.9.1. Business Description

8.1.9.2. Product Portfolio

8.1.9.3. Collaborations & Alliances

8.1.9.4. Recent Developments

8.1.9.5. Financial Details

8.1.9.6. Others

8.1.10. Bulgari Australia Pty Ltd

8.1.10.1. Business Description

8.1.10.2. Product Portfolio

8.1.10.3. Collaborations & Alliances

8.1.10.4. Recent Developments

8.1.10.5. Financial Details

8.1.10.6. Others

9. Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Category |

|

| By Type |

|

| By Collection |

|

| By Material Type |

|

| By Sales Channel |

|

| By End User |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.