Asia Pacific Automotive Microcontrollers Market Report: Trends, Growth and Forecast (2026-2032)

By MCU Bit Size (8-bit Microcontrollers, 16-bit Microcontrollers, 32-bit Microcontrollers, Others), By Application (Powertrain and Engine Control, Body Electronics and Comfort Systems, Chassis and Safety Systems, ADAS and Autonomous Driving, Infotainment, Telematics and HMI, Battery Management and Electrification Control, Vehicle Networking, Gateway and Domain Control, Others), By Vehicle Type (Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles, Buses and Coaches, Two-Wheelers and Motorcycles, Others), By Propulsion Type (Internal Combustion Engine Vehicles, Hybrid Electric Vehicles, Plug-in Hybrid Electric Vehicles, Battery Electric Vehicles, Fuel Cell Electric Vehicles, Others), By Country (China, Japan, South Korea, India, Taiwan, Thailand, Rest of Asia Pacific) ... Read more

|

Major Players

|

Asia Pacific Automotive Microcontrollers Market Statistics and Insights, 2026

- Market Size Statistics

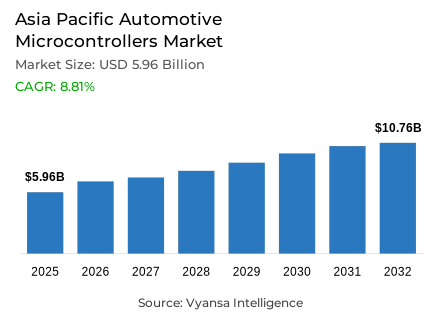

- Automotive microcontrollers market size in Asia Pacific was valued at USD 5.96 billion in 2025 and is estimated at USD 6.75 billion in 2026.

- The market size is expected to grow to USD 10.76 billion by 2032.

- Market to register a CAGR of around 8.81% during 2026-32.

- MCU Bit Size Shares

- 32-bit microcontrollers grabbed market share of 65%.

- Competition

- Automotive microcontrollers in Asia Pacific is currently being catered to by more than 10 companies.

- Top 5 companies acquired around 45% of the market share.

- Texas Instruments Incorporated, Toshiba Electronic Devices & Storage Corporation, ROHM Co. Ltd. (LAPIS TECHNOLOGY), Infineon Technologies AG, Renesas Electronics Corporation etc., are few of the top companies.

- Application

- Body Electronics and Comfort Systems grabbed 30% of the market.

- Country

- China leads with a 35% share of the Asia Pacific market.

Asia Pacific Automotive Microcontrollers Market Outlook

The Asia Pacific automotive microcontrollers market covers automotive-grade MCUs used in powertrain ECUs, body control modules, chassis systems, ADAS functions, infotainment, HMI, battery management and vehicle gateway architectures. The market is valued at USD 5.96 billion in 2025, USD 6.75 billion in 2026 and USD 10.76 billion by 2032. OEMs, Tier-1 suppliers and semiconductor vendors rely on these devices to manage embedded automotive electronics, real-time control, security and functional-safety workloads across increasingly software-intensive vehicles.

Electrification, ADAS penetration and zonal E/E architecture are intensifying semiconductor content per vehicle. The Asia Pacific automotive microcontrollers industry benefits from China’s EV scale, Japanese hybrid platforms, Korean safety electronics and India’s expanding vehicle production base. According to the IEA, more than 13 million electric cars were sold in China in 2025, while Southeast Asia electric car sales more than doubled to over half a million units, reinforcing demand for BMS controller, inverter control MCU and connected vehicle MCU platforms.

Automotive production concentration strengthens supply-chain visibility for the Asia Pacific automotive microcontrollers market. China, Japan, South Korea, India and Thailand support large vehicle assembly ecosystems, while local semiconductor packaging, testing and electronics manufacturing services improve design-in responsiveness. The Asia Pacific automotive microcontrollers industry also supports procurement stability because 32-bit automotive MCU programs increasingly align with ISO 26262, AEC-Q100 qualification and cybersecurity-enabled MCU requirements across multiple vehicle control modules.

Supplier positioning in 2026 is shifting toward scalable MCU families, integrated memory, hardware security and software-defined vehicle microcontrollers. The Asia Pacific automotive microcontrollers market is moving from discrete ECU expansion toward consolidated domain, zonal controller MCU and vehicle networking architectures. Infineon reported in March 2026 that its microcontroller share reached 23.2% in 2025 and that Automotive Ethernet integration strengthens its software-defined vehicle positioning, supporting competitive intensity across the Asia Pacific automotive microcontrollers industry.

Asia Pacific Automotive Microcontrollers Market Growth Driver

Electrification Loads Lift Embedded Control Demand

Vehicle electrification is increasing embedded control density across power electronics, thermal management, charging, body modules and safety systems. The Asia Pacific automotive microcontrollers market benefits as hybrid and battery-electric platforms require deterministic low-latency control for inverter, BMS, DC-DC conversion and motor-control functions. This demand pattern strengthens automotive MCU procurement across OEM and Tier-1 design cycles and expands the addressable base for automotive-grade MCUs.

Data from the IEA indicates that global electric car sales exceeded 17 million in 2024, with China accounting for more than 11 million units, supporting high-volume design-in requirements for automotive microcontrollers for electric vehicles. The Asia Pacific automotive microcontrollers industry gains from this production and adoption base because xEV platforms use more embedded automotive controllers than conventional architectures, particularly in battery management microcontrollers, powertrain control MCU, smart cockpit electronics and safety-certified vehicle microcontroller units, across passenger cars, electric buses, two-wheelers, and light commercial fleets at regional scale.

Asia Pacific Automotive Microcontrollers Market Challenge

Qualification Cycles and Demand Volatility Pressure Supply Visibility

Qualification complexity and cyclic vehicle demand are constraining faster MCU substitution across safety-critical electronics. Automotive-grade MCUs require AEC-Q100 reliability, ISO 26262 functional-safety evidence, secure boot, long lifecycle supply and software validation, which lengthens design-in schedules. The Asia Pacific automotive microcontrollers market therefore faces adoption delays when OEMs shift platforms, reduce inventories or pause lower-priority ECU upgrades during demand volatility, especially where domestic OEMs are optimizing inventories across model programs and semiconductor allocations.

Recent data reported by Reuters from CAAM shows that China’s January 2026 auto sales fell 19.5% to 1.4 million vehicles, while NEV sales dropped 22.9%, reflecting subsidy adjustments and softer demand. The Asia Pacific automotive microcontrollers industry is exposed to these swings because MCU orders track vehicle builds, platform launches and electronic module procurement. Short-term production softness can delay distributor replenishment, pressure pricing discipline and reduce visibility for smaller automotive microcontroller manufacturers across channels regionally.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Asia Pacific Automotive Microcontrollers Market Trend

Zonal Architectures Reshape MCU Platform Design

Zonal E/E architecture is shifting MCU demand from isolated low-memory controllers toward scalable devices that combine deterministic control, embedded security, high-bandwidth communication and software-update readiness. The Asia Pacific automotive microcontrollers market is being reshaped by this transition as OEMs consolidate ECUs and require zonal controller MCU platforms that can support software-defined vehicle microcontrollers without sacrificing latency across passenger cars, EVs, hybrid platforms and connected commercial vehicles.

NXP stated in March 2025 that its S32K5 family is the automotive industry’s first 16nm FinFET MCU with embedded MRAM and extends CoreRide with pre-integrated zonal and electrification solutions for scalable SDV architectures. The Asia Pacific automotive microcontrollers industry gains from this trend because zonal platforms improve ECU consolidation, strengthen vehicle networking, support OTA-ready electronics and position suppliers for higher-value automotive semiconductor controller programs. This directly changes supplier qualification priorities and creates stronger demand for cybersecurity-enabled MCU families across China, Japan and Korea.

Asia Pacific Automotive Microcontrollers Market Opportunity

Localized EV Electronics Create Supplier Expansion Space

Localization of EV and automotive electronics supply chains creates an expansion route for MCU vendors, design houses, distributors and OSAT-linked semiconductor partners. The Asia Pacific automotive microcontrollers market can capture higher design-in value where suppliers provide local technical support, functional-safety documentation, reference software and application-specific devices for BMS, smart lighting, motor control and digital cockpit platforms across China, Japan, India, South Korea and ASEAN manufacturing corridors.

STMicroelectronics introduced the Stellar P3E automotive MCU in February 2026 with real-time AI acceleration for hybrid and EV systems, X-in-1 ECUs and body zonal architectures. This launch signals an opportunity for automotive-grade semiconductor suppliers to combine real-time control, edge intelligence and electrification support in one platform. It improves demand capture by giving OEMs and Tier-1 suppliers a path to reduce ECU complexity while raising software-defined vehicle capability. The result strengthens supplier positioning in next-generation automotive control electronics, vehicle software management and embedded security programs.

Asia Pacific Automotive Microcontrollers Market Country Analysis

By Country

- China

- Japan

- South Korea

- India

- Taiwan

- Thailand

- Rest of Asia Pacific

China holds 35% share by country because its vehicle production scale, EV manufacturing base, local electronics ecosystem and fast software-defined vehicle adoption create the region’s largest MCU demand pool. The Asia Pacific automotive microcontrollers market benefits from China’s concentration of passenger cars, NEVs, smart cockpit platforms, ADAS programs and domestic semiconductor design activity, while the Asia Pacific automotive microcontrollers industry gains from dense OEM and Tier-1 sourcing networks.

CAAM data reported by China Daily shows that China’s automobile production reached 34.53 million units in 2025, with passenger vehicle production at 30.27 million units and commercial vehicle production at 4.26 million units. This production depth strengthens automotive MCU demand across body electronics, powertrain control, battery management systems, chassis safety and vehicle gateway control, improving supplier access to high-volume platform nominations and localized semiconductor procurement. It also supports faster qualification feedback across domestic model refresh cycles and export platforms.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Asia Pacific Automotive Microcontrollers Market Segmentation Analysis

By MCU Bit Size

- 8-bit Microcontrollers

- 16-bit Microcontrollers

- 32-bit Microcontrollers

- Others

32-bit microcontrollers lead by MCU bit size with 65% share because modern vehicle platforms need higher processing capability, larger embedded memory, richer connectivity and stronger safety functions than legacy 8-bit or 16-bit devices can provide. The Asia Pacific automotive microcontrollers market relies on 32-bit automotive MCU platforms for ADAS nodes, body control, EV control, gateway modules and chassis applications where deterministic response and software scalability are procurement priorities, especially as zonal architecture and electrification increase ECU software load.

Microchip states that its AEC-Q100-qualified 8-bit, 16-bit and 32-bit MCUs and DSCs are used in embedded control systems throughout the vehicle, supporting safety-critical and high-temperature automotive designs. This portfolio evidence reinforces why 32-bit devices dominate value share: they support more complex software, functional safety MCU requirements, automotive cybersecurity MCU features and mixed application coverage across vehicle electronic systems. This enables higher ASP potential, stronger design lock-in and broader reuse across supplier platforms.

By Application

- Powertrain and Engine Control

- Body Electronics and Comfort Systems

- Chassis and Safety Systems

- ADAS and Autonomous Driving

- Infotainment, Telematics and HMI

- Battery Management and Electrification Control

- Vehicle Networking, Gateway and Domain Control

- Others

Body electronics and comfort systems hold 30% share under application because cockpit convenience, lighting, HVAC, seat control, door modules and body control modules create broad, repeatable MCU demand across mass-market and premium vehicles. The Asia Pacific automotive microcontrollers market gains from this segment because body electronics require many distributed controllers, reliable LIN and CAN interfaces, and cost-effective devices that can scale across high-volume passenger car platforms, including electric two-wheelers and commercial vehicles.

NXP stated in April 2026 that its S32K3 series supports body and comfort, emerging domain and zone controllers and electrification, with the S32K389 offering 12 MB of flash, 2304 kB of SRAM and up to 12 CAN FD interfaces. These specifications support body-control consolidation, improve vehicle HMI controller capability and strengthen demand for automotive embedded microcontrollers across comfort-focused electronic modules in China, Japan, South Korea, India and Southeast Asian assembly hubs, improving supplier design reuse and localization advantages.

Various Market Players in Asia Pacific Automotive Microcontrollers Market

The companies mentioned below are highly active in the Asia Pacific automotive microcontrollers market, occupying a considerable portion of the market and shaping industry progress.

- Texas Instruments Incorporated

- Toshiba Electronic Devices & Storage Corporation

- ROHM Co. Ltd. (LAPIS TECHNOLOGY)

- Infineon Technologies AG

- Renesas Electronics Corporation

- NXP Semiconductors N.V.

- STMicroelectronics International N.V.

- Microchip Technology Inc.

- GigaDevice Semiconductor Inc.

- Beijing SemiDrive Technology Corporation

- AutoChips Inc.

- Nuvoton Technology Corporation

Market News & Updates

- Renesas Electronics Corporation, 2026:

Renesas expanded its automotive MCU portfolio in March 2026 with the 28nm RH850/U2C 32-bit microcontroller. The device targets chassis and safety systems, battery management systems, body control functions, lighting, motor control, and ASIL D applications, with CAN-XL, Ethernet TSN, security, and low-power architecture. The update strengthens Renesas’ automotive MCU offering for next-generation E/E architectures.

- Beijing SemiDrive Technology Corporation, 2026:

SemiDrive announced in May 2026 that its E3650 flagship automotive MCU passed TÜV Rheinland ISO 26262 ASIL D functional safety product certification. The company also stated that the MCU is supported by ASIL D-level MCAL drivers and FuSaLib functional safety libraries for next-generation automotive E/E architectures. The update strengthens China-based high-performance automotive MCU capability for zonal control and intelligent vehicle platforms.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- Asia Pacific Automotive Microcontrollers Market Policies, Regulations, and Standards

- Asia Pacific Automotive Microcontrollers Market Production (Thousand Units) Trend 2022-2032

- Asia Pacific Automotive Microcontrollers Market Production (Thousand Units) Trend By MCU Bit Size

-

- 8-bit Microcontrollers

- 16-bit Microcontrollers

- 32-bit Microcontrollers

- Others

-

- Company Wise Production Plants and Statistics

- Installed Production Capacity

- Actual Production

- Planned Production Target

- Asia Pacific Automotive Microcontrollers Market Production (Thousand Units) Trend By MCU Bit Size

- Asia Pacific Automotive Microcontrollers Market Pricing Analysis 2022-2032

- Asia Pacific Automotive Microcontrollers Market Pricing Trend (USD/ Thousand Units) 2022-2032

- Asia Pacific Automotive Microcontrollers Market Pricing Trend (USD/ Thousand Units) By Countries 2022-2032

- China

- Japan

- South Korea

- India

- Rest of Asia Pacific

- Asia Pacific Automotive Microcontrollers Market Pricing Trend (USD/Unit) By MCU Bit Size 2022-2032

-

- 8-bit Microcontrollers

- 16-bit Microcontrollers

- 32-bit Microcontrollers

- Others

-

- Asia Pacific Automotive Microcontrollers Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- Asia Pacific Automotive Microcontrollers Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Unit Sold in Thousand Units

- Market Segmentation & Growth Outlook

- By MCU Bit Size

- 8-bit Microcontrollers- Market Insights and Forecast 2022-2032, USD Million

- 16-bit Microcontrollers- Market Insights and Forecast 2022-2032, USD Million

- 32-bit Microcontrollers- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Application

- Powertrain and Engine Control- Market Insights and Forecast 2022-2032, USD Million

- Body Electronics and Comfort Systems- Market Insights and Forecast 2022-2032, USD Million

- Chassis and Safety Systems- Market Insights and Forecast 2022-2032, USD Million

- ADAS and Autonomous Driving- Market Insights and Forecast 2022-2032, USD Million

- Infotainment, Telematics and HMI- Market Insights and Forecast 2022-2032, USD Million

- Battery Management and Electrification Control- Market Insights and Forecast 2022-2032, USD Million

- Vehicle Networking, Gateway and Domain Control- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Vehicle Type

- Passenger Cars- Market Insights and Forecast 2022-2032, USD Million

- Light Commercial Vehicles- Market Insights and Forecast 2022-2032, USD Million

- Heavy Commercial Vehicles- Market Insights and Forecast 2022-2032, USD Million

- Buses and Coaches- Market Insights and Forecast 2022-2032, USD Million

- Two-Wheelers and Motorcycles- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Propulsion Type

- Internal Combustion Engine Vehicles- Market Insights and Forecast 2022-2032, USD Million

- Hybrid Electric Vehicles- Market Insights and Forecast 2022-2032, USD Million

- Plug-in Hybrid Electric Vehicles- Market Insights and Forecast 2022-2032, USD Million

- Battery Electric Vehicles- Market Insights and Forecast 2022-2032, USD Million

- Fuel Cell Electric Vehicles- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Country

- China

- Japan

- South Korea

- India

- Taiwan

- Thailand

- Rest of Asia Pacific

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By MCU Bit Size

- Market Size & Growth Outlook

- China Automotive Microcontrollers Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Unit Sold in Thousand Units

- Market Segmentation & Growth Outlook

- By MCU Bit Size- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- By Propulsion Type- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Japan Automotive Microcontrollers Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Unit Sold in Thousand Units

- Market Segmentation & Growth Outlook

- By MCU Bit Size- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- By Propulsion Type- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- South Korea Automotive Microcontrollers Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Unit Sold in Thousand Units

- Market Segmentation & Growth Outlook

- By MCU Bit Size- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- By Propulsion Type- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- India Automotive Microcontrollers Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Unit Sold in Thousand Units

- Market Segmentation & Growth Outlook

- By MCU Bit Size- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- By Propulsion Type- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Taiwan Automotive Microcontrollers Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Unit Sold in Thousand Units

- Market Segmentation & Growth Outlook

- By MCU Bit Size- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- By Propulsion Type- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Thailand Automotive Microcontrollers Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Unit Sold in Thousand Units

- Market Segmentation & Growth Outlook

- By MCU Bit Size- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- By Propulsion Type- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Infineon Technologies AG

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Renesas Electronics Corporation

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- NXP Semiconductors N.V.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- STMicroelectronics International N.V.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Microchip Technology Inc.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Texas Instruments Incorporated

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Toshiba Electronic Devices & Storage Corporation

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- ROHM Co. Ltd. (LAPIS TECHNOLOGY)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- GigaDevice Semiconductor Inc.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Beijing SemiDrive Technology Corporation

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- AutoChips Inc.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Infineon Technologies AG

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By MCU Bit Size |

|

| By Application |

|

| By Vehicle Type |

|

| By Propulsion Type |

|

| By Country |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.