Argentina Dog Food Market Report: Trends, Growth and Forecast (2026-2032)

By Product (Wet Dog Food, Dry Dog Food, Treats and Mixers), By Nature (Organic, Monoprotein, Conventional), By Ingredient (Animal Derivatives, Plant Derivatives), By Pet Type (Kitten/Pup, Adult, Senior), By Pricing (Economy, Mid-Priced, Premium), By Packaging (Pouches, Bags, Folding Cartons, Tubs & Cups, Can, Bottles & Jars), By Sales Channel (Retail Channels, Non-Retail Channels) ... Read more

|

Major Players

|

Argentina Dog Food Market Statistics and Insights, 2026

- Market Size Statistics

- Dog Food in Argentina is estimated at $ 700 Million.

- The market size is expected to grow to $ 1.54 Billion by 2032.

- Market to register a CAGR of around 11.92% during 2026-32.

- Product Shares

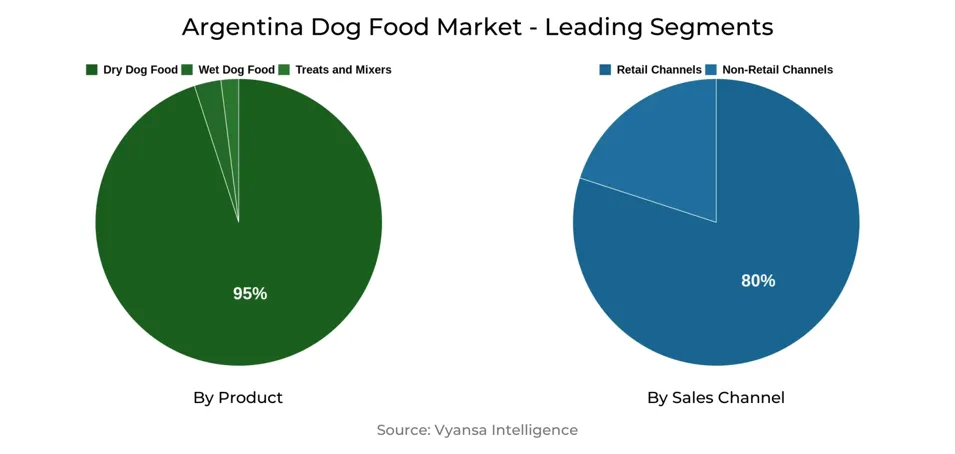

- Dry Dog Food grabbed market share of 95%.

- Dry Dog Food to witness a volume CAGR of around 4.13%.

- Competition

- More than 15 companies are actively engaged in producing Dog Food in Argentina.

- Top 5 companies acquired 65% of the market share.

- Royal Canin Argentina SA, Vitalcan SA, Molino Chacabuco SA, Nestlé Argentina SA, Agroindustrias Baires SA etc., are few of the top companies.

- Sales Channel

- Retail Channels grabbed 80% of the market.

Argentina Dog Food Market Outlook

The Argentina dog food market will continue to grow consistently between 2025 and 2030, after a challenging 2024, which was characterised by elevated inflation and decreased consumer expenditure. With the economy stabilising and incomes in households starting to recover, more consumers are likely to return to official selling channels and spend money on higher-quality products. But a definite trend towards depremiumisation was witnessed throughout the crisis, as consumers moved into economy and mid-brands across a number of categories, but specifically in dry dog food. This can be expected to slacken over time, particularly as consumers' confidence levels rise.

Economy dry dog food will continue to dominate in volume terms, but premium wet dog food and dog treats are expected to see the fastest growth, supported by a low base and rising interest in more specialised offerings. The humanisation of pets and increasing awareness of pet health are key growth drivers, encouraging demand for more natural and less processed products. Innovation in such areas as frozen dinner and BARF diet is also picking up steam, but cost continues to be the main obstacle to mainstream acceptance.

Distribution will continue to be predominantly informal, with forrajerías and other specialty non-grocery stores still dominant in sales. These distribution channels are particularly vital for smaller and local brands that enjoy convenient pricing flexibility. At the same time, supermarkets are likely to regain some of their lost share following the abolition of government price control, though high commercial standards continue to restrict entry for smaller competitors.

E-commerce will continue to grow on the back of convenience and shifting shopping patterns, especially by younger consumers. Still, high logistics and platform charges are an issue, capping profitability, particularly for deliveries beyond large cities.

Argentina Dog Food Market Growth Driver

Argentina economic recovery is contributing to the growth of consumer buying power, which is in turn fueling demand for dog food. As families become financially stable again, consumers are increasingly spending money on better-quality food for pets. This is also driven by the continued humanisation of pets, with the majority of dog owners looking at their pets as members of the family. Consequently, expenditures on premium products are going up steadily.

Besides, the number of domestic pet dogs is increasing with increased adoption rates, particularly among medium and small breeds. Large dog ownership is predicted to decline slightly, but overall dog numbers are still increasing. All categories of dog food are seeing increasing demand, but premium wet food and treats are increasing most rapidly. Their present low penetration in the country presents high potential for brands wishing to develop in Argentina.

Argentina Dog Food Market Challenge

The increasing trend of online shopping is fueling e-commerce expansion in Argentina, particularly among younger shoppers and those with inconvenient means of transport. Purchasing large quantities of dog food online is convenient and cheaper than doing it in-store. Better platforms and increased customer base are supporting this trend.

Yet, increasing delivery and logistics charges are squeezing brands and retailers. Several companies in the Buenos Aires metropolitan area have discontinued free delivery because it is now too costly. Exorbitant transaction charges on sites like Mercado Libre are also driving sellers out. Delivery to distant places is no longer viable, with some companies cutting down their web presence or withdrawing from regions altogether.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Argentina Dog Food Market Trend

Innovation within Argentina's dog food market is targeting more towards wet food and naturals. Although over 99% of volume remains in dry food, there is huge space to grow for wet food, treats, and mixers. Most brands still concentrate primarily on dry food, with newer alternatives tending to be more expensive. Still, trends such as frozen food and BARF (Biologically Appropriate Raw Food) diets are gaining traction, particularly as consumer incomes slowly improve.

Meanwhile, the increased human interest in health and wellness is also affecting how humans feed their pets. With more owners looking to minimize ultra-processed ingredients in their pets' diets, demand for natural products is likely to grow. Lamb protein typically used in dry food is gaining popularity although few manufacturers sell it because of expense and availability factors. Old Prince by Agroindustrias Baires is notable for emphasizing strongly lamb-based products.

| Report Coverage | Details |

|---|---|

| Market Forecast | 2026-32 |

| USD Value 2025 | $ 700 Million |

| USD Value 2032 | $ 1.54 Billion |

| CAGR 2026-2032 | 11.92% |

| Largest Category | Dry Dog Food segment leads with 95% market share |

| Top Drivers | Rising Disposable Incomes and Pet Humanisation Supporting Growth |

| Top Challenges | Rising Logistics Costs Impact Profitability of Online Sales |

| Top Trends | Rising Demand for Natural and Wet Formulations |

| Key Players | Royal Canin Argentina SA, Vitalcan SA, Molino Chacabuco SA, Nestlé Argentina SA, Agroindustrias Baires SA, Petfood Saladillo SA, Mars Southern Cone, Alimentos Ltda Metrive SA, Alican SA, Grupo Pilar SA and Others. |

Unlock Market Intelligence

Explore the market potential with our data-driven report

Argentina Dog Food Market Segmentation Analysis

By Sales Channel

- Retail Channels

- Non-Retail Channels

The most extensive market share within the sales channel is retail, dominated by other non-grocery specialists like forrajerías. These small-scale, independent stores continue to control the Argentina dog food distribution arena. Their unofficial selling methods and less stringent entry barriers make them more than suitable for smaller and local brands, particularly those providing inexpensive offerings. This sector gained more ground in 2024 as more consumers turned towards cost-effective alternatives under financial pressure—a trend likely to continue till 2025.

Pet stores, hypermarkets, and veterinary hospitals target higher-value buyers. Veterinary hospitals, in turn, sustain high-end brands through expert advice. Supermarkets and hypermarkets provide few brand options and consist predominantly of multinational brands such as Dog Chow and Pedigree. Local players like Raza and Sabrositos are also seen. Nonetheless, on the disappearance of the government's Precios Justos programme in 2024, these new retail formats lost value share but are predicted to recover incrementally in 2025.

Top Companies in Argentina Dog Food Market

The top companies operating in the market include Royal Canin Argentina SA, Vitalcan SA, Molino Chacabuco SA, Nestlé Argentina SA, Agroindustrias Baires SA, Petfood Saladillo SA, Mars Southern Cone, Alimentos Ltda Metrive SA, Alican SA, Grupo Pilar SA, etc., are the top players operating in the Argentina Dog Food Market.

Frequently Asked Questions

Related Report

1. Market Segmentation

1.1. Research Scope

1.2. Research Methodology

1.3. Definitions and Assumptions

2. Executive Summary

3. Argentina Dog Food Market Policies, Regulations, and Standards

4. Argentina Dog Food Market Dynamics

4.1. Growth Factors

4.2. Challenges

4.3. Trends

4.4. Opportunities

5. Argentina Dog Food Market Statistics, 2022-2032F

5.1. Market Size & Growth Outlook

5.1.1.By Revenues in US$ Million

5.1.2.By Quantity Sold in Kilo Tons

5.2. Market Segmentation & Growth Outlook

5.2.1.By Product

5.2.1.1. Wet Dog Food- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2. Dry Dog Food- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3. Treats and Mixers- Market Insights and Forecast 2022-2032, USD Million

5.2.2.By Nature

5.2.2.1. Organic- Market Insights and Forecast 2022-2032, USD Million

5.2.2.2. Monoprotein- Market Insights and Forecast 2022-2032, USD Million

5.2.2.3. Conventional- Market Insights and Forecast 2022-2032, USD Million

5.2.3.By Ingredient

5.2.3.1. Animal Derivatives- Market Insights and Forecast 2022-2032, USD Million

5.2.3.2. Plant Derivatives- Market Insights and Forecast 2022-2032, USD Million

5.2.4.By Pet Type

5.2.4.1. Kitten/Pup- Market Insights and Forecast 2022-2032, USD Million

5.2.4.2. Adult- Market Insights and Forecast 2022-2032, USD Million

5.2.4.3. Senior- Market Insights and Forecast 2022-2032, USD Million

5.2.5.By Pricing

5.2.5.1. Economy- Market Insights and Forecast 2022-2032, USD Million

5.2.5.2. Mid-Priced- Market Insights and Forecast 2022-2032, USD Million

5.2.5.3. Premium- Market Insights and Forecast 2022-2032, USD Million

5.2.6.By Packaging

5.2.6.1. Pouches- Market Insights and Forecast 2022-2032, USD Million

5.2.6.2. Bags- Market Insights and Forecast 2022-2032, USD Million

5.2.6.3. Folding Cartons- Market Insights and Forecast 2022-2032, USD Million

5.2.6.4. Tubs & Cups- Market Insights and Forecast 2022-2032, USD Million

5.2.6.5. Can- Market Insights and Forecast 2022-2032, USD Million

5.2.6.6. Bottles & Jars- Market Insights and Forecast 2022-2032, USD Million

5.2.7.By Sales Channel

5.2.7.1. Retail Channels- Market Insights and Forecast 2022-2032, USD Million

5.2.7.1.1. Retail Offline- Market Insights and Forecast 2022-2032, USD Million

5.2.7.1.2. Retail Online- Market Insights and Forecast 2022-2032, USD Million

5.2.7.2. Non-Retail Channels- Market Insights and Forecast 2022-2032, USD Million

5.2.7.2.1. Veterinary Clinics- Market Insights and Forecast 2022-2032, USD Million

5.2.8.By Competitors

5.2.8.1. Competition Characteristics

5.2.8.2. Market Share & Analysis

6. Argentina Wet Dog Food Market Statistics, 2022-2032F

6.1. Market Size & Growth Outlook

6.1.1.By Revenues in US$ Million

6.1.2.By Quantity Sold in Kilo Tons

6.2. Market Segmentation & Growth Outlook

6.2.1.By Nature- Market Insights and Forecast 2022-2032, USD Million

6.2.2.By Ingredient- Market Insights and Forecast 2022-2032, USD Million

6.2.3.By Pet Type- Market Insights and Forecast 2022-2032, USD Million

6.2.4.By Pricing- Market Insights and Forecast 2022-2032, USD Million

6.2.5.By Packaging- Market Insights and Forecast 2022-2032, USD Million

6.2.6.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

7. Argentina Dry Dog Food Market Statistics, 2022-2032F

7.1. Market Size & Growth Outlook

7.1.1.By Revenues in US$ Million

7.1.2.By Quantity Sold in Kilo Tons

7.2. Market Segmentation & Growth Outlook

7.2.1.By Nature- Market Insights and Forecast 2022-2032, USD Million

7.2.2.By Ingredient- Market Insights and Forecast 2022-2032, USD Million

7.2.3.By Pet Type- Market Insights and Forecast 2022-2032, USD Million

7.2.4.By Pricing- Market Insights and Forecast 2022-2032, USD Million

7.2.5.By Packaging- Market Insights and Forecast 2022-2032, USD Million

7.2.6.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

8. Argentina Treats and Mixers Dog Food Market Statistics, 2022-2032F

8.1. Market Size & Growth Outlook

8.1.1.By Revenues in US$ Million

8.1.2.By Quantity Sold in Kilo Tons

8.2. Market Segmentation & Growth Outlook

8.2.1.By Nature- Market Insights and Forecast 2022-2032, USD Million

8.2.2.By Ingredient- Market Insights and Forecast 2022-2032, USD Million

8.2.3.By Pet Type- Market Insights and Forecast 2022-2032, USD Million

8.2.4.By Pricing- Market Insights and Forecast 2022-2032, USD Million

8.2.5.By Packaging- Market Insights and Forecast 2022-2032, USD Million

8.2.6.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

9. Competitive Outlook

9.1. Company Profiles

9.1.1.Nestlé Argentina SA

9.1.1.1. Business Description

9.1.1.2. Product Portfolio

9.1.1.3. Collaborations & Alliances

9.1.1.4. Recent Developments

9.1.1.5. Financial Details

9.1.1.6. Others

9.1.2.Agroindustrias Baires SA

9.1.2.1. Business Description

9.1.2.2. Product Portfolio

9.1.2.3. Collaborations & Alliances

9.1.2.4. Recent Developments

9.1.2.5. Financial Details

9.1.2.6. Others

9.1.3.Petfood Saladillo SA

9.1.3.1. Business Description

9.1.3.2. Product Portfolio

9.1.3.3. Collaborations & Alliances

9.1.3.4. Recent Developments

9.1.3.5. Financial Details

9.1.3.6. Others

9.1.4.Mars Southern Cone Alimentos Ltda

9.1.4.1. Business Description

9.1.4.2. Product Portfolio

9.1.4.3. Collaborations & Alliances

9.1.4.4. Recent Developments

9.1.4.5. Financial Details

9.1.4.6. Others

9.1.5.Metrive SA

9.1.5.1. Business Description

9.1.5.2. Product Portfolio

9.1.5.3. Collaborations & Alliances

9.1.5.4. Recent Developments

9.1.5.5. Financial Details

9.1.5.6. Others

9.1.6.Royal Canin Argentina SA

9.1.6.1. Business Description

9.1.6.2. Product Portfolio

9.1.6.3. Collaborations & Alliances

9.1.6.4. Recent Developments

9.1.6.5. Financial Details

9.1.6.6. Others

9.1.7.Vitalcan SA

9.1.7.1. Business Description

9.1.7.2. Product Portfolio

9.1.7.3. Collaborations & Alliances

9.1.7.4. Recent Developments

9.1.7.5. Financial Details

9.1.7.6. Others

9.1.8.Molino Chacabuco SA

9.1.8.1. Business Description

9.1.8.2. Product Portfolio

9.1.8.3. Collaborations & Alliances

9.1.8.4. Recent Developments

9.1.8.5. Financial Details

9.1.8.6. Others

9.1.9.Alican SA

9.1.9.1. Business Description

9.1.9.2. Product Portfolio

9.1.9.3. Collaborations & Alliances

9.1.9.4. Recent Developments

9.1.9.5. Financial Details

9.1.9.6. Others

9.1.10. Grupo Pilar SA

9.1.10.1. Business Description

9.1.10.2. Product Portfolio

9.1.10.3. Collaborations & Alliances

9.1.10.4. Recent Developments

9.1.10.5. Financial Details

9.1.10.6. Others

10. Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Product |

|

| By Nature |

|

| By Ingredient |

|

| By Pet Type |

|

| By Pricing |

|

| By Packaging |

|

| By Sales Channel |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.