US Forestry Machinery Market Report: Trends, Growth and Forecast (2026-2032)

By Equipment Type (Felling Equipment (Chainsaw, Harvester, Feller Buncher), Extracting Equipment (Forwarder, Skidder), On-Site Processing Equipment (Chipper, Delimber), Other Forestry Equipment (Loader, Mulcher)), By Power Source (Diesel, Hybrid, Battery-Electric), By Automation Level (Manual, Semi-Autonomous, Fully Autonomous), By End User (Contract Logging Firms, Forest Ownership Groups, Pulp and Paper Companies), By Region (West, Midwest, South, North, Northeast) ... Read more

|

Major Players

|

US Forestry Machinery Market Statistics and Insights, 2026

- Market Size Statistics

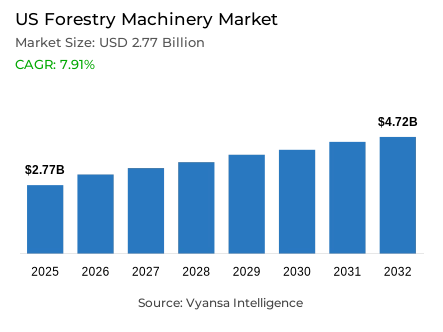

- Forestry machinery market size in US was valued at USD 2.77 billion in 2025 and is estimated at USD 2.98 billion in 2026.

- The market size is expected to grow to USD 4.72 billion by 2032.

- Market to register a CAGR of around 7.91% during 2026-32.

- Equipment Type Shares

- Felling equipment grabbed market share of 50%.

- Competition

- More than 10 companies are actively engaged in producing forestry machinery in US.

- Top 5 companies acquired around 55% of the market share.

- Husqvarna Group, STIHL, Volvo Construction Equipment, John Deere, Komatsu Forest etc., are few of the top companies.

- Power Source

- Diesel grabbed 80% of the market.

US Forestry Machinery Market Outlook

The US forestry machinery market is valued at USD 2.77 Billion in 2025 and is projected to reach USD 4.72 Billion by 2032, growing at 7.91% during 2026-2032. The market covers feller bunchers, skidders, harvesters, forwarders, loaders, attachments, and digital fleet tools used by logging contractors, timberland owners, sawmills, pulp producers, biomass operators, and public forest agencies. The US forestry machinery industry supports mechanized timber harvesting, thinning, extraction, and site preparation across commercial and public forest operations.

Domestic demand remains anchored in North American timber procurement, wildfire-risk work, and forest restoration, while global equipment strategies are being influenced by Europe’s low-impact harvesting systems, Asia-Pacific plantation mechanization, South American pulpwood logistics, and MEA land-clearing applications. For the United States, these external shifts mainly affect technology benchmarking, attachment design, emissions readiness, and supplier positioning, rather than replacing domestic demand fundamentals inside The US forestry machinery market. This reinforces a national market shaped by fleet modernization and reliability.

The economic impact is strongest where mechanized fleets improve harvested-wood throughput, reduce manual exposure in hazardous terrain, and support predictable log flows into sawmills and wood-processing sites. The industry also strengthens supply-chain continuity by aligning equipment replacement with contractor uptime, dealer service coverage, telematics adoption, and demand for machines that can operate across thinning, final felling, fuel reduction, and post-disaster salvage activity. These factors improve procurement planning for contractors.

The 2026 trajectory points toward productivity-focused procurement, diesel platform optimization, stronger felling-cycle efficiency, and selective adoption of connected machine systems. The US forestry machinery market is also influenced by federal timber-supply direction, hazardous-fuel reduction, and restoration-led site access needs. Supplier positioning is likely to depend on machine durability, dealer response capability, operator visibility, fuel efficiency, and integration of digital support systems across The US forestry machinery industry, as contractors prioritize field uptime certainty over speculative technology adoption.

US Forestry Machinery Market Growth Driver

Mechanized Timber Supply Is Strengthening Equipment Demand

Timber-supply expansion and forest-health operations are lifting demand for high-output machines that can cut, bunch, skid, load, and move logs under tight operating windows. The US forestry machinery market benefits when public and private forest managers seek stronger site utilization and safer handling of timber, storm-damaged trees, and hazardous fuels across dispersed forests. This demand force is visible where contractors must complete harvest plans, thinning work, and access clearing before seasonal weather restricts operations.

US Forest Service accomplishments reported 2.94 billion board feet sold and 3.1 billion board feet offered in fiscal 2025, which signals institutional support for timber availability and contracting pipelines. That activity improves procurement visibility for feller bunchers, skidders, harvesters, and forwarders, supporting The US forestry machinery industry through replacement demand and fleet utilization. Higher timber availability also encourages contractors to standardize machine platforms, protect uptime, and select equipment that can shift between harvesting and forest-health assignments.

US Forestry Machinery Market Challenge

Operator Scarcity and Harsh Terrain Increase Ownership Pressure

Skilled operator scarcity, maintenance intensity, and harsh terrain conditions constrain equipment adoption, particularly among smaller logging contractors with thin maintenance capacity. The US forestry machinery market faces a bottleneck when contractors must absorb higher training needs, downtime risk, diesel servicing, and specialized parts requirements while maintaining production schedules across remote, steep, wet, or wildfire-affected sites. These constraints can delay replacement decisions, widen utilization gaps, and increase dependence on diagnostics and field service.

Data from the U.S. Bureau of Labor Statistics indicates that overall logging-worker employment is projected to decline 2% from 2024 to 2034, even as about 6,000 openings are expected annually from workforce replacement. This labor profile raises the value of automation, visibility systems, and dealer support, but it pressures the market through slower fleet expansion among operators lacking trained crews. The shortage increases demand for intuitive controls, cab ergonomics, monitoring, and training support that reduce skill-related downtime.

Unlock Market Intelligence

Explore the market potential with our data-driven report

US Forestry Machinery Market Trend

Connected and High-Stability Platforms Are Reshaping Fleet Priorities

Connected machines, higher-stability platforms, and operator-assistance systems are reshaping procurement priorities as contractors target uptime, production consistency, and safer operation in difficult terrain. The US forestry machinery market is moving beyond mechanical horsepower alone, with buyers comparing cab visibility, telematics, machine diagnostics, crane control, load capacity, and terrain stability before committing to replacement cycles. Digital support is becoming a procurement filter as contractors seek faster troubleshooting, predictable maintenance, and better coordination between woods operations and dealer service networks.

Komatsu introduced its 895-3 forwarder to the North American market in January 2026, describing the machine as purpose-built for demanding forestry operations and suited to final felling and large-scale forwarding. This launch strengthens The US forestry machinery industry by reinforcing the shift toward integrated harvester-forwarder systems that improve extraction efficiency and contractor competitiveness. It also demonstrates how OEMs are positioning new platforms around smarter designs, stronger structures, and productivity gains in 2026.

US Forestry Machinery Market Opportunity

Restoration, Salvage, and Fuel-Reduction Work Open New Demand Pools

Restoration, salvage logging, and community fuel-reduction work create underpenetrated opportunities for suppliers serving contractors and partners that need versatile machines beyond conventional timber harvesting. The US forestry machinery market can capture incremental demand through felling equipment, mulchers, loaders, telematics, and service models designed for disaster recovery, access restoration, and hazardous-fuel removal. Suppliers that bundle attachments, maintenance support, and training can improve demand capture where crews are mobilized for restoration and thinning projects.

In May 2026, the U.S. Forest Service reported ongoing disaster recovery across national forests and grasslands, including salvage logging, prescribed fire, road restoration, and community equipment support for hazardous-fuel reduction in Utah and Nevada. These activities expand operational uptake for The US forestry machinery industry by linking machine demand to resilience programs, access repair, and contractor participation. The opportunity is strongest for equipment providers that can support mixed-duty applications, rapid parts availability, and contractor networks near forest communities.

Unlock Market Intelligence

Explore the market potential with our data-driven report

US Forestry Machinery Market Segmentation Analysis

By Equipment Type

- Felling Equipment

- Chainsaw

- Harvester

- Feller Buncher

- Extracting Equipment

- Forwarder

- Skidder

- On-Site Processing Equipment

- Chipper

- Delimber

- Other Forestry Equipment

- Loader

- Mulcher

Felling Equipment holds 50% share under Equipment Type, supported by its central role in the production step of mechanized harvesting. The US forestry machinery market depends on feller bunchers and harvesting heads to convert timber into bunches that improve downstream skidding and transport. This segment leads because cycle speed, cutting precision, visibility, and stability determine crew productivity and site economics. Strong felling capacity also reduces bottlenecks across the harvesting chain, giving contractors control over machine sequencing and log flow.

Tigercat stated in September 2025 that its H-series drive-to-tree feller bunchers would enter production in October 2025, with 720H, 724H, and 726H models and improved wheelbase, visibility, and hydraulic options. This product update strengthens The US forestry machinery industry by showing OEM investment in felling performance, operator control, and logging applications. The update supports segment leadership by aligning equipment design with tighter stands, larger timber, and demand for faster saw recovery.

By Power Source

- Diesel

- Hybrid

- Battery-Electric

Diesel holds 80% share under Power Source, reflecting the torque, range, and service infrastructure required in remote forest operations. The US forestry machinery market still relies on diesel platforms because logging sites need long duty cycles, hydraulic output, and field support across uneven terrain and limited charging infrastructure. Diesel dominance also shapes parts supply and technician capability. Procurement teams continue to prioritize fuel availability, emissions compliance, and machine endurance over alternatives lacking comparable field readiness.

Tigercat’s 720H product specifications list a Tier 4f Tigercat FPT N67 engine rated at 203 hp, with 90 US gallons of fuel capacity and 12 US gallons of DEF capacity. These specifications support The US forestry machinery industry by aligning diesel performance with emissions compliance, field operation, and contractor expectations for high-use felling equipment. The specification profile reinforces why diesel remains embedded in heavy forestry fleets where hydraulic power and serviceability directly influence uptime.

List of Companies Covered in US Forestry Machinery Market

The companies listed below are highly influential in the US forestry machinery market, with a significant market share and a strong impact on industry developments.

- Husqvarna Group

- STIHL

- Volvo Construction Equipment

- John Deere

- Komatsu Forest

- Caterpillar

- Tigercat Industries

- Ponsse

- Hitachi Construction Machinery

- Barko Hydraulics

Market News & Updates

- John Deere, 2025:

John Deere enhanced its 900 M-Series tracked feller bunchers, 900 MH-Series tracked harvesters, and 900 ML-Series shovel loggers in March 2025. The update added an enhanced Dedicated Travel System, one-touch Return-To-Level functionality, and undercarriage improvements for leveling-system durability. The release supports productivity and operator-assistance upgrades in U.S. forestry harvesting fleets.

- John Deere, 2025:

John Deere launched Operations Center PRO Service in July 2025 as a digital support tool for connected and non-connected machines across agriculture, turf, construction, and forestry equipment. The tool supports maintenance, diagnostics, repair, and equipment protection workflows. The update adds service and uptime-management capability for forestry contractors operating mixed equipment fleets.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- The US Forestry Machinery Market Policies, Regulations, and Standards

- The US Forestry Machinery Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- The US Forestry Machinery Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold (Thousand Units)

- Market Segmentation & Growth Outlook

- By Equipment Type

- Felling Equipment- Market Insights and Forecast 2022-2032, USD Million

- Chainsaw- Market Insights and Forecast 2022-2032, USD Million

- Harvester- Market Insights and Forecast 2022-2032, USD Million

- Feller Buncher- Market Insights and Forecast 2022-2032, USD Million

- Extracting Equipment- Market Insights and Forecast 2022-2032, USD Million

- Forwarder- Market Insights and Forecast 2022-2032, USD Million

- Skidder- Market Insights and Forecast 2022-2032, USD Million

- On-Site Processing Equipment- Market Insights and Forecast 2022-2032, USD Million

- Chipper- Market Insights and Forecast 2022-2032, USD Million

- Delimber- Market Insights and Forecast 2022-2032, USD Million

- Other Forestry Equipment- Market Insights and Forecast 2022-2032, USD Million

- Loader- Market Insights and Forecast 2022-2032, USD Million

- Mulcher- Market Insights and Forecast 2022-2032, USD Million

- Felling Equipment- Market Insights and Forecast 2022-2032, USD Million

- By Power Source

- Diesel- Market Insights and Forecast 2022-2032, USD Million

- Hybrid- Market Insights and Forecast 2022-2032, USD Million

- Battery-Electric- Market Insights and Forecast 2022-2032, USD Million

- By Automation Level

- Manual- Market Insights and Forecast 2022-2032, USD Million

- Semi-Autonomous- Market Insights and Forecast 2022-2032, USD Million

- Fully Autonomous- Market Insights and Forecast 2022-2032, USD Million

- By End User

- Contract Logging Firms- Market Insights and Forecast 2022-2032, USD Million

- Forest Ownership Groups- Market Insights and Forecast 2022-2032, USD Million

- Pulp and Paper Companies- Market Insights and Forecast 2022-2032, USD Million

- By Region

- West

- Midwest

- South

- North

- Northeast

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Equipment Type

- Market Size & Growth Outlook

- The US Felling Equipment Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold (Thousand Units)

- Market Segmentation & Growth Outlook

- By Power Source- Market Insights and Forecast 2022-2032, USD Million

- By Automation Level- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- The US Extracting Equipment Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold (Thousand Units)

- Market Segmentation & Growth Outlook

- By Power Source- Market Insights and Forecast 2022-2032, USD Million

- By Automation Level- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- The US On-Site Processing Equipment Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold (Thousand Units)

- Market Segmentation & Growth Outlook

- By Power Source- Market Insights and Forecast 2022-2032, USD Million

- By Automation Level- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- The US Other Forestry Equipment Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold (Thousand Units)

- Market Segmentation & Growth Outlook

- By Power Source- Market Insights and Forecast 2022-2032, USD Million

- By Automation Level- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- John Deere

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Komatsu Forest

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Caterpillar

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Tigercat Industries

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Ponsse

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Husqvarna Group

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- STIHL

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Volvo Construction Equipment

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Hitachi Construction Machinery

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Barko Hydraulics

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- John Deere

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Equipment Type |

|

| By Power Source |

|

| By Automation Level |

|

| By End User |

|

| By Region |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.