China Forestry Machinery Market Report: Trends, Growth and Forecast (2026-2032)

By Equipment Type (Felling Equipment (Chainsaw, Harvester, Feller Buncher), Extracting Equipment (Forwarder, Skidder), On-Site Processing Equipment (Chipper, Delimber), Other Forestry Equipment (Loader, Mulcher)), By Power Source (Diesel, Hybrid, Battery-Electric), By Automation Level (Manual, Semi-Autonomous, Fully Autonomous), By End User (Contract Logging Firms, Forest Ownership Groups, Pulp and Paper Companies), By Region (North, East, Southwest, Northwest, North East, South) ... Read more

|

Major Players

|

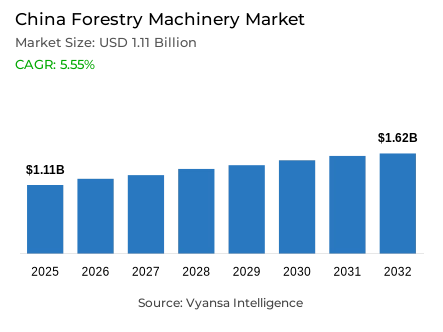

China Forestry Machinery Market Statistics and Insights, 2026

- Market Size Statistics

- Forestry machinery market size in China was valued at USD 1.11 billion in 2025 and is estimated at USD 1.55 billion in 2026.

- The market size is expected to grow to USD 1.62 billion by 2032.

- Market to register a CAGR of around 5.55% during 2026-32.

- Equipment Type Shares

- Felling equipment grabbed market share of 45%.

- Competition

- More than 10 companies are actively engaged in producing forestry machinery in China.

- Top 5 companies acquired around 40% of the market share.

- STIHL China, XCMG Construction Machinery Co. Ltd., SANY Heavy Industry, John Deere China, Komatsu Forest China etc., are few of the top companies.

- Power Source

- Diesel grabbed 90% of the market.

China Forestry Machinery Market Outlook

China forestry machinery market covers felling equipment, skidders, forwarders, loaders, forestry tractors, wood chippers, mulchers, tree planting machines, and support systems used across commercial forestry, plantation management, timber extraction, reforestation, and ecological restoration. Valued at USD 1.11 Billion in 2025, the China forestry machinery Industry is projected to reach USD 1.62 Billion by 2032, growing at a CAGR of 5.55% from 2026 to 2032. Demand is anchored in mechanized harvesting, forest residue handling, plantation maintenance, and land greening programs.

Domestic demand patterns are shaped by large-scale forest resource expansion, state forestry farm modernization, forest road upgrades, and operating conditions across hilly, mountainous, and plantation zones. China’s forestry agencies are linking forest quality improvement, carbon sequestration, degraded land restoration, and rural infrastructure with higher equipment intensity. This supports procurement of tracked machinery, diesel-powered units, compact planting systems, and smart forestry equipment for varied terrain and long-cycle restoration work.

Industrial impact is visible in equipment localization, aftersales servicing, operator productivity, and forest supply-chain efficiency. The China forestry machinery market benefits when forestry contractors and local forestry bureaus replace labor-intensive operations with felling, skidding, chipping, pruning, and residue processing machinery. Procurement is also influenced by emissions compliance, fuel reliability, spare-parts availability, and the need to keep wood extraction and restoration work aligned with ecological protection standards.

The 2026 trajectory points toward selective modernization rather than broad equipment replacement. Smart forestry systems, GPS forestry systems, remote sensing forestry equipment, and rapid forest-stock measurement tools are becoming more important as land greening programs move from expansion to quality improvement. Suppliers able to combine durable diesel platforms, terrain adaptability, localized service, operator training, parts continuity, and digital monitoring can strengthen positioning across commercial forestry, conservation contracting, and state forestry farm operations across procurement cycles where durability, operator efficiency, terrain readiness, and lifecycle support shape purchase decisions.

China Forestry Machinery Market Growth Driver

Mechanized Forest Operations Are Expanding Procurement Momentum

Mechanized harvesting and restoration workload is increasing equipment adoption as forestry agencies, contractors, and plantation operators manage larger forest areas with stricter productivity and ecological performance requirements. The China forestry machinery market is moving beyond basic logging machinery toward integrated forest harvesting equipment, skidding machinery, pruning systems, chippers, and reforestation machinery that improve labor efficiency, reduce downtime, support safer workflows, and support standardized forest management.

According to the State Council, China’s forest area has reached 3.614 billion mu, about 241 million hectares, while forest coverage has risen to 25.09%. This land base directly expands work volumes for planting, thinning, forest road maintenance, residue utilization, and timber harvesting, supporting the China forestry machinery Industry through sustained demand for mechanized forestry equipment, fleet renewal, dealer service coverage, and forest management machinery across provincial projects, plantation work, conservation contracts, timber extraction sites, and rural service networks requiring reliable high-utilization assets through 2026 cycles.

China Forestry Machinery Market Challenge

Terrain, Compliance and Service Gaps Restrain Faster Mechanization

Hilly terrain, fragmented operating sites, high maintenance requirements, and operator-skill gaps limit faster equipment penetration, especially for small forestry contractors and remote plantation operators. The China forestry machinery market faces procurement friction where felling equipment, skidders, and loaders require terrain-specific configurations, stronger service networks, and higher upfront capital commitments. These barriers slow adoption even when mechanization improves output consistency, equipment safety, utilization planning, and workforce safety.

Data from the Association of Equipment Manufacturers’ 2024 China compliance review indicates that China listed forestry facilities and equipment such as 240KW forest operation chassis, tree planting, care, logging, skidding, forest residue collection, pruning, and rapid forest-stock measurement equipment among encouraged manufacturing items. This policy direction strengthens the China forestry machinery Industry, but also raises technical thresholds for suppliers competing on compliance, localization, parts availability, and field reliability as buyers prioritize proven uptime, operator support, warranty coverage, and accessible workshop capacity across remote counties.

Unlock Market Intelligence

Explore the market potential with our data-driven report

China Forestry Machinery Market Trend

Smart Forestry Systems Are Reshaping Equipment Specifications

Smart forestry equipment is shifting procurement criteria toward integrated data capture, navigation, telematics, and precision operation rather than standalone mechanical capacity. The China forestry machinery market is therefore seeing stronger alignment between timber harvesting machinery, forest road construction equipment, digital forestry machinery, and remote monitoring systems. This trend supports fleet visibility, improves utilization, strengthens maintenance planning, and helps forestry agencies monitor ecological restoration and forest-stock improvement outcomes more consistently.

The State Council reported that China’s forestry and grassland systems now provide annual ecosystem service value exceeding 30 trillion yuan, while forest food production surpassed 240 million tonnes each year. These scale indicators strengthen the China forestry machinery Industry by encouraging equipment that supports quality improvement, stock measurement, maintenance planning, traceable operations, and low-waste forest operations across high-value ecological and production assets while improving procurement visibility for agencies balancing ecological outcomes with commercial forest productivity during planning cycles and performance reviews.

China Forestry Machinery Market Opportunity

State Forestry Farm Modernization Opens Supplier White Space

State forestry farm modernization creates a procurement opportunity for suppliers of compact felling systems, tree planting machines, difficult-site afforestation machinery, brush-clearing tools, skidders, and forest residue processing equipment. The China forestry machinery market can capture demand where legacy fleets are insufficient for higher-quality ecological management, standardized safety procedures, and digital supervision. Local distributors with service capability can improve demand capture in remote forestry operating zones.

The State Council stated that new guidelines aim to establish a preliminary modernized state forestry farm system by 2030 and a more complete system by 2035, supported by upgraded essential infrastructure. This gives the China forestry machinery industry a clearer institutional demand base, particularly for forestry tractors, tracked forestry equipment, precision forestry tools, spare-parts networks, and maintenance machinery aligned with state farm modernization plans and creates room for domestic OEMs, attachment makers, and service providers with terrain-specific capabilities across long-cycle modernization programs and supplier tenders.

Unlock Market Intelligence

Explore the market potential with our data-driven report

China Forestry Machinery Market Segmentation Analysis

By Equipment Type

- Felling Equipment

- Chainsaw

- Harvester

- Feller Buncher

- Extracting Equipment

- Forwarder

- Skidder

- On-Site Processing Equipment

- Chipper

- Delimber

- Other Forestry Equipment

- Loader

- Mulcher

Felling equipment holds 45% share by equipment type, supported by its role at the start of timber harvesting, thinning, plantation renewal, and forest clearing workflows. In the China forestry machinery market, felling systems lead because contractors need machinery that improves cutting precision, reduces manual exposure, and feeds downstream skidding, loading, chipping, and wood extraction operations. The segment also supports forest productivity improvement where planned thinning and regeneration require repeatable field performance.

AEM’s 2024 compliance review identified multi-functional machinery covering land preparation, tree planting, care, logging, skidding, and small to medium-sized forestry machines within encouraged forestry equipment manufacturing categories. This strengthens the China forestry machinery Industry by reinforcing product development around felling-linked operations, including forest harvesting equipment, skidders, pruning tools, localized attachments, and residue-processing machinery used in integrated forestry workflows and supports procurement planning around cutting heads, hydraulic systems, operator cabins, and safety controls across harvesting schedules and service plans today.

By Power Source

- Diesel

- Hybrid

- Battery-Electric

Diesel holds 90% share by power source because forestry operations require high torque, long operating range, mobile refueling, and resilience across remote forest roads, steep terrain, and continuous harvesting cycles. In the China forestry machinery market, diesel machinery remains influential for feller bunchers, skidders, log loaders, forestry tractors, and wood chippers where battery charging infrastructure, payload requirements, cold-start reliability, dealer support, and high-load electric platforms remain operationally constrained.

AEM’s 2024 China regulatory review highlights diesel engines meeting China non-road mobile machinery emission Stage IV requirements within agricultural machinery manufacturing categories and lists forestry equipment manufacturing priorities immediately after. This supports the China forestry machinery Industry by linking diesel platform continuity with emissions compliance, component upgrading, aftertreatment integration, maintenance discipline, and supplier differentiation across high-duty forestry machinery applications while preserving operational continuity for contractors working beyond grid-connected depots and controlled plantation yards during peak harvesting windows and remote assignments daily operations.

List of Companies Covered in China Forestry Machinery Market

The companies listed below are highly influential in the China forestry machinery market, with a significant market share and a strong impact on industry developments.

- STIHL China

- XCMG Construction Machinery Co. Ltd.

- SANY Heavy Industry

- John Deere China

- Komatsu Forest China

- Ponsse China

- Caterpillar China

- Husqvarna China

- Zoomlion Heavy Industry

- China National Machinery Industry Corporation (Sinomach)

Market News & Updates

- Guangxi Xuvol Engineering Machinery Equipment Co. Ltd., 2025:

Guangxi Xuvol highlighted its XVF-500E felling machine for China’s autumn harvesting season in October 2025. The machine is designed for tree felling, delimbing, precise fixed-length cutting, and harvested-volume calculation with data feedback. The update adds a mechanized forestry harvesting option for Chinese operators seeking faster, data-supported cutting workflows.

- Guangxi Xuvol Engineering Machinery Equipment Co. Ltd., 2025:

Guangxi Xuvol showcased multiple intelligent forestry machines at the 2025 Guangxi International Forest Products and Wood Products Exhibition in November 2025. The displayed equipment included log collectors, felling machines, wheeled excavators, grapple saws, tree shears, and circular saws covering forestry harvesting and handling workflows. The update supports China-based supplier visibility across full-process forestry mechanization.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- China Forestry Machinery Market Policies, Regulations, and Standards

- China Forestry Machinery Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- China Forestry Machinery Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold (Thousand Units)

- Market Segmentation & Growth Outlook

- By Equipment Type

- Felling Equipment- Market Insights and Forecast 2022-2032, USD Million

- Chainsaw- Market Insights and Forecast 2022-2032, USD Million

- Harvester- Market Insights and Forecast 2022-2032, USD Million

- Feller Buncher- Market Insights and Forecast 2022-2032, USD Million

- Extracting Equipment- Market Insights and Forecast 2022-2032, USD Million

- Forwarder- Market Insights and Forecast 2022-2032, USD Million

- Skidder- Market Insights and Forecast 2022-2032, USD Million

- On-Site Processing Equipment- Market Insights and Forecast 2022-2032, USD Million

- Chipper- Market Insights and Forecast 2022-2032, USD Million

- Delimber- Market Insights and Forecast 2022-2032, USD Million

- Other Forestry Equipment- Market Insights and Forecast 2022-2032, USD Million

- Loader- Market Insights and Forecast 2022-2032, USD Million

- Mulcher- Market Insights and Forecast 2022-2032, USD Million

- Felling Equipment- Market Insights and Forecast 2022-2032, USD Million

- By Power Source

- Diesel- Market Insights and Forecast 2022-2032, USD Million

- Hybrid- Market Insights and Forecast 2022-2032, USD Million

- Battery-Electric- Market Insights and Forecast 2022-2032, USD Million

- By Automation Level

- Manual- Market Insights and Forecast 2022-2032, USD Million

- Semi-Autonomous- Market Insights and Forecast 2022-2032, USD Million

- Fully Autonomous- Market Insights and Forecast 2022-2032, USD Million

- By End User

- Contract Logging Firms- Market Insights and Forecast 2022-2032, USD Million

- Forest Ownership Groups- Market Insights and Forecast 2022-2032, USD Million

- Pulp and Paper Companies- Market Insights and Forecast 2022-2032, USD Million

- By Region

- North

- East

- Southwest

- Northwest

- North East

- South

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Equipment Type

- Market Size & Growth Outlook

- China Felling Equipment Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold (Thousand Units)

- Market Segmentation & Growth Outlook

- By Power Source- Market Insights and Forecast 2022-2032, USD Million

- By Automation Level- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- China Extracting Equipment Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold (Thousand Units)

- Market Segmentation & Growth Outlook

- By Power Source- Market Insights and Forecast 2022-2032, USD Million

- By Automation Level- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- China On-Site Processing Equipment Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold (Thousand Units)

- Market Segmentation & Growth Outlook

- By Power Source- Market Insights and Forecast 2022-2032, USD Million

- By Automation Level- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- China Other Forestry Equipment Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold (Thousand Units)

- Market Segmentation & Growth Outlook

- By Power Source- Market Insights and Forecast 2022-2032, USD Million

- By Automation Level- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- John Deere China

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Komatsu Forest China

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Ponsse China

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Caterpillar China

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Husqvarna China

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- STIHL China

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- XCMG Construction Machinery Co. Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- SANY Heavy Industry

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Zoomlion Heavy Industry

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- China National Machinery Industry Corporation (Sinomach)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- John Deere China

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Equipment Type |

|

| By Power Source |

|

| By Automation Level |

|

| By End User |

|

| By Region |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.