US Bottled Water Market Report: Trends, Growth and Forecast (2026-2032)

By Type of Water (Carbonated Bottled Water, Flavoured Bottled Water, Functional Bottled Water, Still Bottled Water), By Sub Types (Purified (Desalinated, Atmospheric Generated, Others), Mineral, Other (Spring, Alkaline, Other)), By Packaging Material (Flexible Packaging (Aluminium, Pouches), Glass, Rigid Plastic (PET Bottles, Thin Wall Plastic Containers, Others)), By Price Category (Budget, Economy, Premium), By Pack Size (100 ml, 125 ml, 200 ml, 250 ml, 330 ml, 370 ml, 450 ml, 500 ml, 591 ml, 750 ml, 1,000 ml, 1,500 ml, 4,000 ml, 5,000 ml, Others), By Sales Channel (On Trade (Restaurants, Hotels, Cafes, Others), Off Trade (Grocery Retailers (Convenience Retail, Supermarkets, Hypermarkets, Small Local Grocer), Non-Grocery Retailers (General Merchandise Stores, Health and Beauty Specialists), Vending, E-commerce)), By Region (West, Midwest, South, North, Northeast) ... Read more

|

Major Players

|

US Bottled Water Market Statistics and Insights, 2026

- Market Size Statistics

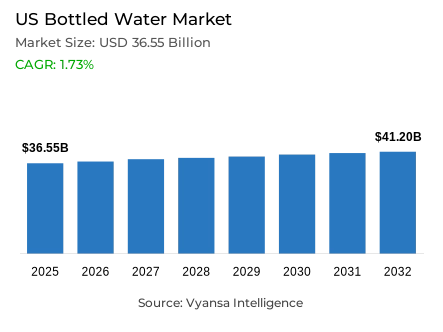

- Bottled water market size in US was estimated at USD 36.55 billion in 2025.

- The market size is expected to grow to USD 41.2 billion by 2032.

- Market to register a CAGR of around 1.73% during 2026-32.

- Type of Water Shares

- Still bottled water grabbed market share of 65%.

- Competition

- More than 15 companies are actively engaged in producing bottled water in US.

- Top 5 companies acquired around 30% of the market share.

- National Beverage Corp, Gatorade Co Ltd The, Fiji Water LLC, BlueTriton Brands Inc, PepsiCo Inc etc., are few of the top companies.

- Sales Channel

- Off trade grabbed 90% of the market.

US Bottled Water Market Outlook

The United States bottled water market is estimated to grow to USD 36.55 billion USD in 2025 and to USD 41.2 billion USD in 2032, indicating a CAGR of about 1.73% in 2026-2032. The increasing awareness related to health remains the foundation of growth. According to the Centers for Disease Control and Prevention, 63% of adults in the US drink minimum one sugar-sweetened beverage daily, and 40% of adults are obese. These indicators related to health continue to change the consumer preference to calorie-free hydration, making bottled water a convenient and healthier substitute to sugary beverages.

At the same time, competitive dynamics are being influenced by sustainability pressures. According to the US Environmental Protection Agency, the recycling rate of plastic containers and packaging is 13.3%, which increases regulatory and environmental scrutiny of single-use plastics. Because of which, manufacturers are focusing on circular packaging and incorporation of recycled material to meet the changing compliance requirements expected in 2026.

The category is also strengthened by innovation in the functional hydration. According to the International Food Information Council, 52 % of Americans follow a particular diet or eating pattern, which proves the increasing popularity of personalized nutrition. Also, e-commerce represents 15.6% of all US retail sales in 2024 (US Census Bureau, 2025), which facilitates convenient bulk buying and repeat purchasing.

65% of the market share by segment is held by still bottled water, fueled by daily drinking habits and clean-label appeal. Distribution wise, the off-trade channel takes the largest share of 90%, which is supported by the vast network of supermarkets and omnichannel retailing infrastructure in the United States.

US Bottled Water Market Growth DriverRising Health & Sugar Reduction Awareness Drives Hydration Demand

Increasing health awareness is still contributing to the growing demand for bottled water in the US, with people becoming more active in minimizing their consumption of sugary drinks. According to the Centers for Disease Control and Prevention, 63% of adults in the US make sure to consume at least one sweetened drink every day, according to the US Centers for Disease Control and Prevention (CDC) reports, which undoubtedly emphasizes health concerns for the consumption of sugars each day. At the same time, the Food and Drug Administration (FDA) updates its guidelines for minimizing the consumption of sugars for the health of people.

Moreover, the reality that 40% of adults within the United States exhibit obesity characteristics is confirmed by the CDC. This reality maintains interest in healthy alternatives to drinks containing calories, making bottled water the easiest zero-calorie drink by which to replace carbonates and juices as consumer behaviors continue to seek weight and wellness benefits.

US Bottled Water Market ChallengePlastic Waste & Recycling Pressure Constrains Industry Perception

The management of plastic waste is still a structural problem to the bottled water manufacturers. According to the US Environmental Protection Agency (EPA), the recycling rate of plastic containers and packaging is 13.3%, which indicates a consistent sustainability issue. The low recycling rates keep putting single-use plastic bottles under more scrutiny and mount regulatory and reputational pressure on manufacturers.

Moreover, EPA notes that plastic packaging is a major source of municipal solid waste. With the increasing demands on environmental responsibility in 2026, brands will face high expenses related to recycled content requirements and recycled packaging programs. The purchasing decisions are becoming more and more dependent on the sustainability performance, which makes environmental stewardship one of the fundamental operational challenges.

Unlock Market Intelligence

Explore the market potential with our data-driven report

US Bottled Water Market TrendFunctional & Enhanced Hydration Gains Mainstream Acceptance

Functional hydration is becoming a trend in 2026. According to the International Food Information Council (IFIC), 52% of Americans adhere to a particular diet or eating style, which indicates a high level of consumer interest in individual nutrition and health. This trend favors the demand of beverages that are enriched with electrolytes, vitamins, and other functional ingredients.

At the same time, the National Institutes of Health (NIH) highlights the importance of hydration in metabolic processes and health in general. Functional bottled water is increasingly accepted outside of niche markets as consumers demand value-added beverages that help them maintain energy, immunity, and recovery. Product development is further enhanced by innovation in flavorless and soluble ingredients throughout the category.

US Bottled Water Market OpportunityExpanding E-Commerce Adoption Supports Purchase Frequency

The growth of digital groceries is a significant prospect in 2026. According to the US Census Bureau (2025 release), e-commerce is expected to make up 15.6% of all retail sales in 2024, indicating a long-term trend of digital buying. The growing use of online grocery services facilitates the repetition of heavy and bulk hydration products by home delivery convenience.

Moreover, the US Department of Commerce (2025) also attests to the further increase in online retailing in food and beverage categories. Omnichannel grocery platforms and subscription-based models increase accessibility and promote a higher purchase rate. With the growing strength of digital infrastructure, online retail is a strategic growth channel of packaged hydration products.

Unlock Market Intelligence

Explore the market potential with our data-driven report

US Bottled Water Market Segmentation Analysis

By Type of Water

- Carbonated Bottled Water

- Flavoured Bottled Water

- Functional Bottled Water

- Still Bottled Water

The segment has the highest share in general: the product-type segment of still bottled water occupies 65% of the market share. Still water is the leader because of its regular use in homes, offices, and on-the-go events. Its zero calorie and neutral taste profile make it a better choice compared to sweet drinks.

The high consumer interest in clean-label hydration and simplicity maintains steady demand. The other advantage of still bottled water is the extensive retail presence and the ability to purchase in large quantities. Its superiority is an indication of daily hydration practices and wide demographic coverage across age groups.

By Sales Channel

- On Trade

- Off Trade

The segment has the largest share in general: the sales-channel segment of off-trade has 90% of the market. The distribution of bottled water is dominated by supermarkets, hypermarkets, mass merchandisers, and warehouse clubs because they have a wide coverage throughout the country and offer competitive pricing systems.

Physical stores are structurally significant as bottled water is often sold in multipacks and bulk. The coordinated retail system, along with the growing omnichannel potential, strengthens the off-trade leadership in the total product supply and consumer buying patterns.

List of Companies Covered in US Bottled Water Market

The companies listed below are highly influential in the US bottled water market, with a significant market share and a strong impact on industry developments.

- National Beverage Corp

- Gatorade Co Ltd The

- Fiji Water LLC

- BlueTriton Brands Inc

- PepsiCo Inc

- Energy Brands Inc

- Coca-Cola Co The

- DS Services of America Inc

- Crystal Geyser Roxane Water Co LLC

- Essentia Water LLC

Competitive Landscape

The competitive landscape of bottled water in the US is led by Primo Brands Corp through its subsidiary BlueTriton Brands, which holds a 14% share of the market. Following the late 2024 merger between BlueTriton Brands and Primo Water, the company strengthened its leadership with an extensive portfolio of regional brands such as Poland Spring, Arrowhead and Deer Park. BlueTriton maintains strong positioning in both bulk and convenience formats while offering a mix of economy and premium still and sparkling bottled waters. However, its core regional spring and purified bottled water segments faced pressure in 2025 as demand for commodity beverages weakened, although premium brands like Mountain Valley and Saratoga performed better due to organic marketing and social media promotion. Meanwhile, The Coca-Cola Co recorded mixed performance in bottled water. Its flagship Dasani brand lost ground as consumers increasingly shifted towards either lower-priced or premium still water options. However, the company saw stronger momentum in premium and functional hydration products, including Topo Chico, which has grown beyond its regional origins and gained popularity nationally. At the same time, PepsiCo Inc remains another major competitor in the category with a 7% market share, contributing to a competitive environment shaped by premiumisation, functional hydration and shifting consumer price preferences

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- US Bottled Water Market Policies, Regulations, and Standards

- US Bottled Water Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- US Bottled Water Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Volume (Million Litres)

- Market Segmentation & Growth Outlook

- By Type of Water

- Carbonated Bottled Water- Market Insights and Forecast 2022-2032, USD Million

- Flavoured Bottled Water- Market Insights and Forecast 2022-2032, USD Million

- Functional Bottled Water- Market Insights and Forecast 2022-2032, USD Million

- Still Bottled Water- Market Insights and Forecast 2022-2032, USD Million

- By Sub Types

- Purified- Market Insights and Forecast 2022-2032, USD Million

- Desalinated- Market Insights and Forecast 2022-2032, USD Million

- Atmospheric Generated- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- Mineral- Market Insights and Forecast 2022-2032, USD Million

- Other (Spring, Alkaline, Other) - Market Insights and Forecast 2022-2032, USD Million

- Purified- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material

- Flexible Packaging- Market Insights and Forecast 2022-2032, USD Million

- Aluminium- Market Insights and Forecast 2022-2032, USD Million

- Pouches- Market Insights and Forecast 2022-2032, USD Million

- Glass- Market Insights and Forecast 2022-2032, USD Million

- Rigid Plastic- Market Insights and Forecast 2022-2032, USD Million

- PET Bottles- Market Insights and Forecast 2022-2032, USD Million

- Thin Wall Plastic Containers- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- Flexible Packaging- Market Insights and Forecast 2022-2032, USD Million

- By Price Category

- Budget- Market Insights and Forecast 2022-2032, USD Million

- Economy- Market Insights and Forecast 2022-2032, USD Million

- Premium- Market Insights and Forecast 2022-2032, USD Million

- By Pack Size

- 100 ml- Market Insights and Forecast 2022-2032, USD Million

- 125 ml- Market Insights and Forecast 2022-2032, USD Million

- 200 ml- Market Insights and Forecast 2022-2032, USD Million

- 250 ml- Market Insights and Forecast 2022-2032, USD Million

- 330 ml- Market Insights and Forecast 2022-2032, USD Million

- 370 ml- Market Insights and Forecast 2022-2032, USD Million

- 450 ml- Market Insights and Forecast 2022-2032, USD Million

- 500 ml- Market Insights and Forecast 2022-2032, USD Million

- 591 ml- Market Insights and Forecast 2022-2032, USD Million

- 750 ml- Market Insights and Forecast 2022-2032, USD Million

- 1,000 ml- Market Insights and Forecast 2022-2032, USD Million

- 1,500 ml- Market Insights and Forecast 2022-2032, USD Million

- 4,000 ml- Market Insights and Forecast 2022-2032, USD Million

- 5,000 ml- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel

- On Trade- Market Insights and Forecast 2022-2032, USD Million

- Restaurants- Market Insights and Forecast 2022-2032, USD Million

- Hotels- Market Insights and Forecast 2022-2032, USD Million

- Cafes- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- Off Trade- Market Insights and Forecast 2022-2032, USD Million

- Grocery Retailers- Market Insights and Forecast 2022-2032, USD Million

- Convenience Retail- Market Insights and Forecast 2022-2032, USD Million

- Supermarkets- Market Insights and Forecast 2022-2032, USD Million

- Hypermarkets- Market Insights and Forecast 2022-2032, USD Million

- Small Local Grocer- Market Insights and Forecast 2022-2032, USD Million

- Non-Grocery Retailers- Market Insights and Forecast 2022-2032, USD Million

- General Merchandise Stores- Market Insights and Forecast 2022-2032, USD Million

- Health and Beauty Specialists- Market Insights and Forecast 2022-2032, USD Million

- Vending- Market Insights and Forecast 2022-2032, USD Million

- E-commerce- Market Insights and Forecast 2022-2032, USD Million

- Grocery Retailers- Market Insights and Forecast 2022-2032, USD Million

- On Trade- Market Insights and Forecast 2022-2032, USD Million

- By Region

- West

- Midwest

- South

- North

- Northeast

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Type of Water

- Market Size & Growth Outlook

- US Carbonated Bottled Water Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Volume (Million Litres)

- Market Segmentation & Growth Outlook

- By Sub Types- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Pack Size- Market Insights and Forecast 2022-2032, USD Million

- By Price Category- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- US Flavoured Bottled Water Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Volume (Million Litres)

- Market Segmentation & Growth Outlook

- By Sub Types- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Pack Size- Market Insights and Forecast 2022-2032, USD Million

- By Price Category- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- US Functional Bottled Water Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Volume (Million Litres)

- Market Segmentation & Growth Outlook

- By Sub Types- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Pack Size- Market Insights and Forecast 2022-2032, USD Million

- By Price Category- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- US Still Bottled Water Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Volume (Million Litres)

- Market Segmentation & Growth Outlook

- By Sub Types- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Pack Size- Market Insights and Forecast 2022-2032, USD Million

- By Price Category- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- BlueTriton Brands Inc

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- PepsiCo Inc

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Energy Brands Inc

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Coca-Cola Co The

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- DS Services of America Inc

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- National Beverage Corp

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Gatorade Co Ltd The

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Fiji Water LLC

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Crystal Geyser Roxane Water Co LLC

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Essentia Water LLC

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- BlueTriton Brands Inc

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Type of Water |

|

| By Sub Types |

|

| By Packaging Material |

|

| By Price Category |

|

| By Pack Size |

|

| By Sales Channel |

|

| By Region |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.