UK Industrial Gases Market Report: Trends, Growth and Forecast (2026-2032)

By Gas Type (Nitrogen Gas, Oxygen Gas, Carbon Dioxide Gas, Argon Gas, Helium Gas, Hydrogen Gas, Other), By Supply Mode (Cylinders, Bulk, On-Site Production, Captive, Other), By Application (Combustion and Process Oxygen, Welding and Metal Fabrication, Inerting Blanketing and Heat Treating, Cryogenics and liquefaction, Chemical Synthesis and Hydrogenation, Purging and Purifications, Analytical and Calibration), By End User Industry (General Manufacturing, Food, Metallurgy, Chemicals, Healthcare, Electronics, Refining & Energy, Glass, Pulp & Paper, Others) ... Read more

|

Major Players

|

UK Industrial Gases Market Statistics and Insights, 2026

- Market Size Statistics

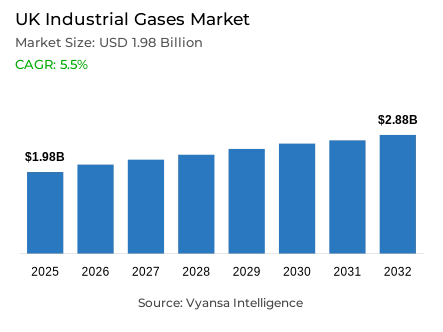

- Industrial gases in UK is estimated at USD 1.98 billion in 2025.

- The market size is expected to grow to USD 2.88 billion by 2032.

- Market to register a cagr of around 5.5% during 2026-32.

- Gas Type Shares

- Oxygen gas grabbed market share of 30%.

- Competition

- More than 5 companies are actively engaged in producing industrial gases in UK.

- Top 5 companies acquired around 60% of the market share.

- Air Product; SOL; NSHD; Linde; Air Liquide etc., are few of the top companies.

- Supply Mode

- Cylinders grabbed 40% of the market.

UK Industrial Gases Market Outlook

UK industrial gases market is likely to show a steady growth expansion between 2026 and 2032 due to the rapid progress the nation has made toward the net-zero aim and its continuously modernizing industrial base. The market was valued at approximately USD 1.98 billion in 2025 and expected to reach nearly USD 2.88 billion by 2032, with a compound annual growth rate of 5.5% during the forecast period. Compelling national decarbonization commitments, including plans and targets for deploying wide-scale low-carbon hydrogen and investing in cleaner steelmaking technologies, are reordering gas demand patterns throughout the economy. Healthcare infrastructure underpins solid baseline consumption due to the fact that hospitals have a massive volume requirement for oxygen every year for routine and critical care.

Manufacturing strength remains another key contributor to market growth. Expanding output in aerospace, electronics, metals, and pharmaceuticals continues to drive the need for oxygen, nitrogen, argon, and specialty gases used in welding, thermal processing, precision fabrication, formulation, and packaging. At the same time, growth in renewable energy and biogas facilities increases demand for the gases employed in purification, compression, and material treatment, reinforcing the long-term consumption trends.

The emerging adoption of hydrogen lies at the center of future momentum. While gigawatt-scale hydrogen projects progress, industries are preparing for long-term fuel switching, thus developing needs for specialty gases, high-pressure cylinders, and cryogenic storage. Additional demand comes from healthcare modernization and pharmaceutical expansion, driven by changed post-Brexit regulations on both high-purity medical and inert gases.

In such a scenario, oxygen continues to lead the gases type with 30% of overall share, precisely for being an essential raw material across steelmaking, healthcare, chemical workflows, and high-precision making. Cylinder distribution remains the leading supply mode, with a 40% share, owing to flexibility, widespread availability, and suitability for hospitals, laboratories, hydrogen projects, and small-scale manufacturing units all over the UK.

UK Industrial Gases Market Growth DriverStrengthening Demand Fundamentals Driven by Decarbonisation and Sectoral Expansion

The UK industrial gasses market is drive by the growing pace of the net zero transition in the country, with the Industrial Decarbonisation Strategy of reducing two-thirds of greenhouse gas emissions by 2035 and as much as 90% by 2050. Industry-driven change is a result of these regulations, with the focus now shifting towards hydrogen, electrification, and low-carbon production methods. Stringent commitments, such as realizing 10GW of low-carbon hydrogen capacity by 2030 and spending £2.5 billion on steel industry decarbonization, have a specific and positive demand-driving effect on the demand for hydrogen, oxygen, and other specialty gases. Healthcare infrastructure is a source of base demand, with hospitals requiring 350 cubic meters of oxygen per bed capacity per year, thus underlining the paramount significance of oxygen demand in the healthcare sectors.

Additionally, a continuously expanding UK manufacturing industry can be seen, where output touched £156.5 billion in Q3 2025. In addition, pharmaceutical production at an annual rate of 1.3% until 2026 strengthens the need for high purity gases applied in formulation, processing, and packaging in pharmaceutical applications. From welding and fabrication, through chemical and electronics manufacturing, rising industry volumes ensure a steady demand stream for gases. These conditions represent a strong foundation for market growth, shaped by policy directives, industry dynamics, and healthcare evolution.

UK Industrial Gases Market ChallengePersistent Supply Chain Pressures and Regulatory Requirements Constrain Expansion

Inefficiencies in the supply side are significant deterrents for the UK industrial gases market. High-pressure cylinders require involved logistics, creating operational overheads, including specialist fleets with skilled handling and high transportation costs, which limit scalability for suppliers at the regional level. Market volatility is apparent, as UK crude steel production was down 29% in 2024 due to key blast furnace closures-most recently at Port Talbot-directly impacting industrial oxygen demand. The manufacturing output of the three months to September 2025 was down 0.8%, with chemical products declining 5.6%, and food and drink producers saw a rise in operational costs of 4.5% set against lower price rises of 2.7%, restricting capital investment in gas-dependent equipment.

Added to this are operational compliance requirements that further raise the cost of suppliers. For example, the Gas Safety Management Regulations impose stringent monitoring of quality specifications, thus increasing technical and financial burdens. Problems with coordination continue to exist in almost 15,000 cylinder stockists and distributors in the country, causing inefficiency in inventories and reordering. Smaller suppliers are especially under stress due to fragmented distribution channels, a rise in operational costs, and economic uncertainty. This structural limitation ultimately affects supply reliability and bounds the rate at which the market can capitalize on the growth of basic underlying demand in healthcare, specialty uses, and emerging clean-energy industries.

Unlock Market Intelligence

Explore the market potential with our data-driven report

UK Industrial Gases Market TrendAccelerating Hydrogen Integration and Clean-Energy Shifts Reshape Market Patterns

Hydrogen's rapid integration into the UK industrial ecosystem redefines demand profiles across gas categories. With 2GW of low-carbon hydrogen projected to be in operation or under construction by 2025, and further progress toward the target of 10GW by 2030, demand for specialty gases, high-pressure cylinders, and cryogenic storage continues to increase. Industry already consumes nearly 20% of national natural gas volumes, placing hydrogen as a substitute fuel for long-term decarbonization. Parallel growth in anaerobic digestion-now at 720 plants with 3.2GW capacity, up 16.7% year-on-year-opens new opportunities in biogas purification, compression, and distribution systems.

Health modernization along with shaping the market's evolution course goes further. Oxygen demand varies from 20-40% concentrations for COPD management to 100% in serious conditions, reinforcing structural reliance on high-purity medical gases. The pharmaceutical industry, growing 1.3% per year through 2026, uses inert gases in formulation, handling, and preservation. These emerging patterns, together with clean-energy investments and sustainability mandates, complete hydrogen and specialty gases as central parts of the UK Industrial Transformation.

UK Industrial Gases Market OpportunityExpanding Healthcare and High-Value Manufacturing Unlock New Market Potential

Improvements in healthcare infrastructure and pharmaceuticals manufacturing consequently act as strong demand catalysts for the UK industrial gases market. Medical gas systems report an average annual consumption of 350 cubic meters of oxygen per hospital bed, thus sustaining continuous demand across therapeutic, respiratory, and emergency applications. Pharmaceutical production, meanwhile, is growing steadily at 1.3% per year, contributing £13 billion to the national economy and employing one in every 121 workers. Regulatory revisions following Brexit have accelerated domestic manufacturing capacity further, expanding inert gas requirements for sterilization, packaging, and formulation processes.

High-value manufacturing, especially aerospace and electronics, is creating extra long-term growth vectors. Indeed, aerospace output was up 26.5% year-on-year in Q3 2025, while electronics production climbed 5.9%, both of which rely on nitrogen, argon, and oxygen for precision fabrication. The wider renewable energy transition-including biogas expansion, EV manufacturing, and wind turbine production-extends thermal processing and advanced material engineering requiring oxygen, nitrogen, and argon. Together, sustained regulatory commitment to decarbonization and rapid adoption of modern manufacturing technologies create attractive avenues for integrated gas solutions, combining traditional supplies with low-carbon hydrogen offerings.

Unlock Market Intelligence

Explore the market potential with our data-driven report

UK Industrial Gases Market Segmentation Analysis

By Gas Type

- Nitrogen Gas

- Oxygen Gas

- Carbon Dioxide Gas

- Argon Gas

- Helium Gas

- Hydrogen Gas

- Other

Oxygen remains the leading gas type in the UK industrial gases market, holding approximately 30% market share as provided. This dominance stems from oxygen’s indispensable role across steelmaking, healthcare, chemical processes, and precision manufacturing. Despite long-term structural challenges in the steel sector, oxygen demand remains foundational due to its critical role in both blast furnace operations and electric arc furnace optimization. Hospitals and care facilities add substantial structural demand, with each bed requiring an estimated 350 cubic metres of oxygen annually for diverse therapeutic uses, from COPD management to acute respiratory care.

Manufacturing industries continue to reinforce oxygen consumption across welding, cutting, thermal treatment, and fabrication processes. High-growth sectors such as aerospace—which expanded 26.5% in Q3 2025—and electronics manufacturing, growing 5.9%, rely heavily on oxygen for high-precision applications. Chemical processing, pharmaceutical production, and food-grade operations also incorporate oxygen as an integral component of oxidation, fermentation, and sterilisation workflows. This broad industrial utilisation ensures oxygen’s long-term market prominence, while rising activity in high-value manufacturing sectors further strengthens its segment position.

By Supply Mode

- Cylinders

- Bulk

- On-Site Production

- Captive

- Other

Cylinder distribution remains the dominant supply mode in the UK industrial gases market, accounting for approximately 40% of market share as provided. Its widespread adoption is driven by flexibility, portability, and suitability for diverse end users, including hospitals, laboratories, welding shops, and small manufacturing units. The country’s extensive distribution network—comprising roughly 15,000 stockists and dealers—enables rapid replenishment and accessibility across both urban and regional locations. Healthcare settings particularly benefit from cylinder delivery for medical oxygen transport across emergency services, care homes, and hospital systems.

The model’s adaptability supports growing hydrogen sector requirements as well, with emerging low-carbon hydrogen facilities demanding specialised cylinders designed for high-pressure storage and safe mobility. Small and medium-scale manufacturers continue to prefer cylinders due to minimal upfront investment relative to bulk tanks or on-site generation systems. The ability to switch between oxygen, nitrogen, argon, and specialty gases enhances operational flexibility for varied industrial processes. This entrenched infrastructure, combined with supplier expertise in medical-grade compliance and specialty gas handling, reinforces cylinder supply as the market’s most resilient and widely adopted distribution method.

List of Companies Covered in UK Industrial Gases Market

The companies listed below are highly influential in the UK industrial gases market, with a significant market share and a strong impact on industry developments.

- Air Product

- SOL

- NSHD

- Linde

- Air Liquide

Market News & Updates

- Linde, 2025:

Linde reported strong Q3 2025 results, with its Europe, Middle East, and Africa business earning $2.178 billion in sales, a 3% increase from last year. The company also has major operations in the UK, with Woking serving as its European headquarters. In addition, Linde is investing over $400 million in a new air separation plant in Louisiana that will start operating in 2029. This plant will supply nitrogen and oxygen for a major low-carbon ammonia project, helping expand Linde’s role in clean energy production.

- Air Liquide, 2025:

Air Liquide is strengthening its clean-energy activities in the UK and Benelux region. The company is also planning to sell its global biomethane assets, valued at around €500 million (about $585 million). It has hired JPMorgan as an advisor for this process. Air Liquide operates 29 biomethane production plants worldwide and wants to focus more on its core industrial gases business.

Frequently Asked Questions

Related Report

1. Market Segmentation

1.1. Research Scope

1.2. Research Methodology

1.3. Definitions and Assumptions

2. Executive Summary

3. The UK Industrial Gases Market Policies, Regulations, and Standards

4. The UK Industrial Gases Market Dynamics

4.1. Growth Factors

4.2. Challenges

4.3. Trends

4.4. Opportunities

5. The UK Industrial Gases Market Statistics, 2022-2032F

5.1. Market Size & Growth Outlook

5.1.1.By Revenues in USD Million

5.1.2.By Quantity Sold in Tons

5.2. Market Segmentation & Growth Outlook

5.2.1.By Gas Type

5.2.1.1. Nitrogen Gas- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

5.2.1.2. Oxygen Gas- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

5.2.1.3. Carbon Dioxide Gas- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

5.2.1.4. Argon Gas- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

5.2.1.5. Helium Gas- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

5.2.1.6. Hydrogen Gas- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

5.2.1.7. Other- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

5.2.2.By Supply Mode

5.2.2.1. Cylinders- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

5.2.2.2. Bulk- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

5.2.2.3. On-Site Production- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

5.2.2.4. Captive- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

5.2.2.5. Other- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

5.2.3.By Application

5.2.3.1. Combustion and Process Oxygen- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

5.2.3.2. Welding and Metal Fabrication- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

5.2.3.3. Inerting Blanketing and Heat Treating- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

5.2.3.4. Cryogenics and liquefaction- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

5.2.3.5. Chemical Synthesis and Hydrogenation- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

5.2.3.6. Purging and Purifications- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

5.2.3.7. Analytical and Calibration- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

5.2.4.By End User Industry

5.2.4.1. General Manufacturing- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

5.2.4.2. Food- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

5.2.4.3. Metallurgy- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

5.2.4.4. Chemicals- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

5.2.4.5. Healthcare- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

5.2.4.6. Electronics- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

5.2.4.7. Refining & Energy- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

5.2.4.8. Glass- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

5.2.4.9. Pulp & Paper- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

5.2.4.10. Others- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

5.2.5.By Competitors

5.2.5.1. Competition Characteristics

5.2.5.2. Market Share & Analysis

6. The UK Nitrogen Gas Market Statistics, 2022-2032

6.1. Market Size & Growth Outlook

6.1.1.By Revenues in USD Million

6.1.2.By Quantity Sold in Tons

6.2. Market Segmentation & Growth Outlook

6.2.1.By Supply Mode- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

6.2.2.By Application- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

6.2.3.By End User Industry- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

7. The UK Oxygen Gas Market Statistics, 2022-2032

7.1. Market Size & Growth Outlook

7.1.1.By Revenues in USD Million

7.1.2.By Quantity Sold in Tons

7.2. Market Segmentation & Growth Outlook

7.2.1.By Supply Mode- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

7.2.2.By Application- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

7.2.3.By End User Industry- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

8. The UK Carbon Dioxide Gas Market Statistics, 2022-2032

8.1. Market Size & Growth Outlook

8.1.1.By Revenues in USD Million

8.1.2.By Quantity Sold in Tons

8.2. Market Segmentation & Growth Outlook

8.2.1.By Supply Mode- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

8.2.2.By Application- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

8.2.3.By End User Industry- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

9. The UK Argon Gas Market Statistics, 2022-2032

9.1. Market Size & Growth Outlook

9.1.1.By Revenues in USD Million

9.1.2.By Quantity Sold in Tons

9.2. Market Segmentation & Growth Outlook

9.2.1.By Supply Mode- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

9.2.2.By Application- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

9.2.3.By End User Industry- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

10. The UK Helium Gas Market Statistics, 2022-2032

10.1. Market Size & Growth Outlook

10.1.1. By Revenues in USD Million

10.1.2. By Quantity Sold in Tons

10.2. Market Segmentation & Growth Outlook

10.2.1. By Supply Mode- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

10.2.2. By Application- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

10.2.3. By End User Industry- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

11. The UK Hydrogen Gas Market Statistics, 2022-2032

11.1. Market Size & Growth Outlook

11.1.1. By Revenues in USD Million

11.1.2. By Quantity Sold in Tons

11.2. Market Segmentation & Growth Outlook

11.2.1. By Supply Mode- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

11.2.2. By Application- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

11.2.3. By End User Industry- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

12. Competitive Outlook

12.1. Company Profiles

12.1.1. Linde

12.1.1.1. Business Description

12.1.1.2. Product Portfolio

12.1.1.3. Collaborations & Alliances

12.1.1.4. Recent Developments

12.1.1.5. Financial Details

12.1.1.6. Others

12.1.2. Air Liquide

12.1.2.1. Business Description

12.1.2.2. Product Portfolio

12.1.2.3. Collaborations & Alliances

12.1.2.4. Recent Developments

12.1.2.5. Financial Details

12.1.2.6. Others

12.1.3. Air Product

12.1.3.1. Business Description

12.1.3.2. Product Portfolio

12.1.3.3. Collaborations & Alliances

12.1.3.4. Recent Developments

12.1.3.5. Financial Details

12.1.3.6. Others

12.1.4. SOL

12.1.4.1. Business Description

12.1.4.2. Product Portfolio

12.1.4.3. Collaborations & Alliances

12.1.4.4. Recent Developments

12.1.4.5. Financial Details

12.1.4.6. Others

12.1.5. NSHD

12.1.5.1. Business Description

12.1.5.2. Product Portfolio

12.1.5.3. Collaborations & Alliances

12.1.5.4. Recent Developments

12.1.5.5. Financial Details

12.1.5.6. Others

13. Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Gas Type |

|

| By Supply Mode |

|

| By Application |

|

| By End User Industry |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.