Europe Membrane Water and Wastewater Treatment Market Report: Trends, Growth and Forecast (2026-2032)

By Product (Microfiltration, Ultrafiltration, Nanofiltration, Reverse Osmosis, Others), By Material (Polymeric, Ceramic, Others), By Application (Water Treatment, Wastewater Treatment, Desalination, Water Reuse/Reclamation, Industrial Process Water), By End User (Municipal, Industrial, Food & Beverage, Pharmaceuticals, Chemicals, Power, Oil & Gas, Others), By Sales Channel (Retail Offline (Direct Sales, Distributors/Dealers, OEM/System Integrator Sales, EPC/Project-Based Sales), Retail Online (Company-Owned Websites, Distributor Online Portals, B2B E-Marketplaces, E-Procurement/Tender Platforms)), By Country (Germany, UK, France, Spain, Italy, Netherland, Rest of Europe) ... Read more

|

Major Players

|

Europe Membrane Water and Wastewater Treatment Market Statistics and Insights, 2026

- Market Size Statistics

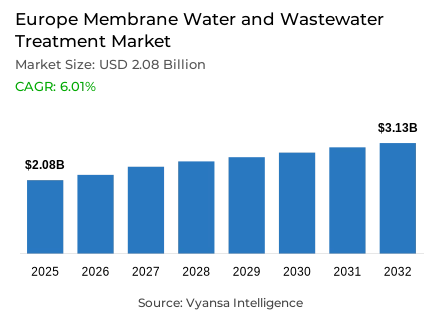

- Membrane water and wastewater treatment market size in Europe was valued at USD 2.08 billion in 2025 and is estimated at USD 2.2 billion in 2026.

- The market size is expected to grow to USD 3.13 billion by 2032.

- Market to register a CAGR of around 6.01% during 2026-32.

- Product Shares

- Reverse osmosis grabbed market share of 35%.

- Competition

- More than 10 companies are actively engaged in producing membrane water and wastewater treatment in Europe.

- Top 5 companies acquired around 40% of the market share.

- MANN+HUMMEL Water & Membrane Solutions, Alfa Laval, Nitto Hydranautics Europe, Veolia Water Technologies & Solutions, Xylem Europe etc., are few of the top companies.

- End User

- Municipal grabbed 35% of the market.

- Country

- Germany leads with a 20% share of the Europe market.

Europe Membrane Water and Wastewater Treatment Market Outlook

The Europe membrane water and wastewater treatment market was valued at USD 2.08 billion in 2025, establishing a commercially stable and operationally well-anchored foundation within one of the world's most demanding and environmentally progressive water infrastructure ecosystems. Projected to advance from USD 2.2 billion in 2026 to USD 3.13 billion by 2032, the sector registers a compound annual growth rate of 6.01% across the forecast horizon. This steady and structurally supported expansion trajectory reflects the systematic deepening of European institutional commitment to water quality improvement, advanced wastewater treatment deployment, and circular water resource management whose escalating compliance requirements and environmental performance standards are driving consistent upgrades across municipal and industrial treatment infrastructure throughout the continent. Growth is anchored in genuine regulatory necessity and environmental imperative rather than discretionary technology adoption, giving this market a commercial resilience that sustains consistent membrane treatment investment across diverse geographic and application contexts.

The product architecture defining this membrane water and wastewater treatment commercial structure is anchored in reverse osmosis technology. Reverse Osmosis commands approximately 35% of total product category market share, reflecting the consistent and deeply embedded institutional preference for membrane separation platforms whose filtration performance, treatment reliability, and multi-application versatility make them the reference technology across municipal wastewater treatment, industrial water purification, and decentralized water reuse projects throughout Europe. This product concentration confirms that water utilities and treatment system operators continue to prioritize proven reverse osmosis-based approaches whose performance credentials and operational familiarity sustain disproportionate procurement share across both new facility development and existing system upgrade contexts within Europe's mature water treatment landscape.

The end-user architecture reinforces the structural centrality of municipal applications as the category's dominant market segment. Municipal Applications account for approximately 35% of total end-user vertical market share, reflecting the foundational role of public water and wastewater systems in supporting urban populations, enabling environmental compliance, and sustaining public health across Europe's cities and towns. This municipal concentration signals that government-led and publicly managed water infrastructure investment remains the primary commercial driver of membrane treatment technology adoption across the region, where large-scale deployment requirements, continuous operational demands, and escalating regulatory standards generate the highest-value and most strategically important procurement activity.

The future outlook is defined by four converging structural forces whose combined commercial impact creates a water treatment market of sustained and well-grounded expansion momentum. The European Commission's implementation of the revised Urban Wastewater Treatment Directive on January 1, 2025, establishing mandatory wastewater collection and treatment requirements across all urban areas above 1,000 inhabitants alongside stricter tertiary and quaternary treatment standards, creates a regulatory expansion pathway whose compliance timelines will systematically drive municipal infrastructure upgrade investment and advanced treatment technology procurement across the continent. The European Commission's documentation of 10 million Europeans still lacking access to basic sanitation services, combined with 30,354 existing urban wastewater treatment plants across the EU, establishes the infrastructure expansion and upgrade scale that will sustain consistent municipal membrane treatment procurement throughout the forecast period. The European Environment Agency's documentation of water stress affecting 30% of European land area and 34% of the population annually, with 2023 water scarcity affecting 28% of EU land and 32% of the population, creates an environmental operating environment that is systematically elevating system reliability requirements and driving infrastructure modernization investment toward more resilient and adaptive treatment technologies. The European Commission's identification of approximately 1 billion cubic metres of treated urban wastewater reused annually within the EU, alongside quantification that six times more treated water could be reused at current quality levels, establishes a circular economy and resource efficiency momentum whose implementation requires advanced membrane treatment infrastructure deployment and system integration across municipal and industrial treatment networks over the forecast period.

Europe Membrane Water and Wastewater Treatment Market Growth Driver

Regulatory Tightening Sustains Municipal Infrastructure Upgrade Investment

The systematic tightening of Europe's wastewater treatment regulatory framework, anchored in the revised Urban Wastewater Treatment Directive effective January 1, 2025, represents the primary structural driver of membrane water treatment demand, functioning as a persistent municipal infrastructure upgrade imperative that sustains consistent treatment technology procurement and system modernization investment across public water utilities throughout the continent. This regulatory-driven demand dynamic transcends funding cycle fluctuations, reflecting a durable compliance necessity whose infrastructure investment generation is structurally anchored in the irreducible requirement for advanced wastewater treatment capability and tertiary treatment performance that municipal utilities must achieve to satisfy expanding regulatory obligations across collection systems, treatment plants, and discharge standards.

The quantitative evidence validating this regulatory-driven demand dynamic is documented with precision by the European Commission and municipal water infrastructure data. The European Commission confirms that 30,354 urban wastewater treatment plants currently operate across the EU, establishing the existing infrastructure base whose systematic upgrade is now mandated by revised regulatory requirements. The Commission further documents that 10 million Europeans still lack access to basic sanitation services, confirming that the regulatory expansion toward universal wastewater collection and treatment coverage will require substantial infrastructure development investment throughout the forecast period. The directive's requirement that all urban areas above 1,000 inhabitants implement wastewater collection and treatment creates a specific timeline and scope definition that is progressively driving municipal capital investment planning and procurement activity toward advanced membrane treatment technology deployment. These regulatory metrics validate an infrastructure upgrade demand dynamic of sufficient scope and timeline certainty to sustain structural membrane treatment market growth over the forecast period.

Europe Membrane Water and Wastewater Treatment Market Challenge

Water Stress and Climate Volatility Elevate System Complexity

The progressively more demanding water stress conditions and climate-driven variability affecting European water systems represent the most consequential structural challenge confronting municipal water utilities and treatment system operators, creating systematic operational complexity, infrastructure resilience requirements, and treatment reliability management burdens that elevate the performance and adaptability demands placed on water treatment systems across the continent. In an operating environment where water availability is becoming increasingly variable, source water quality is subject to greater seasonal and event-driven fluctuations, and treatment system uptime requirements remain non-negotiable, the operational margin for error has contracted significantly, making advanced treatment technologies and resilient system architecture essential rather than discretionary investments for responsible water utility management.

The structural depth and geographic breadth of this water stress challenge are quantified with precision by the European Environment Agency and European Commission sources. The European Environment Agency documents that water stress affects approximately 30% of European land area and 34% of the population annually, while 2023 water scarcity conditions impacted 28% of EU land and 32% of the population, confirming the scale and persistence of water availability pressures across the continent. The EEA further documents that Europe's water management practices are poorly adapted to rapid and extensive environmental change, establishing that current treatment system designs and operational protocols are increasingly insufficient for the changing operating conditions that climate pressure is creating. For membrane treatment technology providers and water utilities, navigating this challenge demands sustained investment in treatment system resilience, operational flexibility, and adaptive capacity enhancement that positions advanced membrane technologies as essential rather than optional infrastructure investments over the forecast period.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Europe Membrane Water and Wastewater Treatment Market Trend

Water Reuse and Circular Economy Integration Reshape Treatment Standards

The systematic shift toward water reuse and integrated circular water management across Europe represents the defining structural trend reshaping wastewater treatment technology priorities, system architecture expectations, and competitive differentiation parameters across the municipal and industrial treatment market. This water reuse trend is progressively transforming the functional role of wastewater treatment from terminal discharge into resource recovery, where treated wastewater becomes a valued source input for agricultural irrigation, industrial processes, and potable water supply augmentation rather than an environmental liability to be managed. The commercial implications of this functional transformation are significant, as treatment technology providers whose systems cannot demonstrate reliable treated-water quality consistency and integration with distributed reuse applications are progressively disadvantaged in competitive evaluations among municipalities implementing circular water management strategies.

The institutional momentum and regulatory specificity of this water reuse trend are documented with authority by the European Commission. The Commission documents that approximately 1 billion cubic metres of treated urban wastewater are currently reused annually within the EU, confirming that water reuse has transitioned from emerging concept into mainstream operational practice across European water management. The Commission further documents that six times more treated water could be reused than current levels, establishing an enormous expansion opportunity whose implementation depends on advanced treatment infrastructure and quality assurance capability that membrane technologies uniquely provide. The adoption of Delegated Regulation (EU) 2024/1765 establishing technical specifications for water reuse risk management confirms that regulatory frameworks are progressively standardizing the treatment performance and quality assurance requirements for reuse applications, creating institutional expectations that favor advanced membrane treatment infrastructure. As water reuse projects expand across water-stressed regions and circular water management becomes institutionalized within municipal planning frameworks, membrane treatment technology providers whose systems support reliable and verified treated-water quality will capture disproportionate share of municipal infrastructure upgrade and water reuse project investment over the forecast period.

Europe Membrane Water and Wastewater Treatment Market Opportunity

Municipal Infrastructure Modernization Creates Sustained High-Value Retrofit Cycles

The ongoing implementation of the revised Urban Wastewater Treatment Directive and the expanded municipal infrastructure upgrade requirements it establishes create a structurally significant and commercially compelling opportunity for advanced membrane treatment technology providers whose solutions align with the treatment performance, environmental compliance, and operational efficiency requirements of municipal infrastructure modernization programs across Europe. This municipal retrofit opportunity is distinguished from routine maintenance and replacement demand by its scale, its alignment with regulatory compliance timelines, its multi-year project horizon, and its integration with broader municipal infrastructure modernization strategies whose successful implementation directly impacts public health, environmental quality, and municipal service quality outcomes.

The quantitative scale and regulatory specificity of this municipal retrofit opportunity are documented with precision by the European Commission and municipal water authority planning data. The European Commission documents that the revised Urban Wastewater Treatment Directive can deliver EUR 6.6 billion in annual economic benefits by 2045 through implementation of required upgrades, confirming that municipal infrastructure investment is not discretionary but economically justified and institutionally prioritized across European local governments. The Commission further establishes a regulatory requirement timeline requiring wastewater collection and treatment implementation across all urban areas above 1,000 inhabitants, creating specific geographic scope and compliance deadlines that are progressively driving municipal procurement activity toward advanced treatment solutions. The directive's expansion of focus toward nutrient removal, micropollutant elimination, and treatment plant energy efficiency creates a broader technological requirement scope that rewards vendors whose membrane treatment solutions address multiple regulatory objectives simultaneously. For advanced membrane treatment providers that invest in municipal retrofit project support, regulatory compliance documentation, and integrated treatment system design capability, this municipal modernization cycle represents a commercially attractive and durably sustainable growth opportunity whose expansion is directly proportional to municipal infrastructure upgrade timelines and regulatory compliance requirements over the forecast period.

Europe Membrane Water and Wastewater Treatment Market Country Analysis

By Country

- Germany

- UK

- France

- Spain

- Italy

- Netherland

- Rest of Europe

The segment with highest market share under the Country is Germany, accounting for approximately 20% of the total European market. This dominant position reflects the convergence of Europe's largest municipal and industrial wastewater treatment infrastructure base, the most advanced water management regulatory framework, and the strongest institutional commitment to circular water resource management and environmental protection across the continent. With one-fifth of total regional market value concentrated within a single national market, Germany defines the commercial scale, technology adoption trajectory, and competitive intensity parameters of the Europe membrane water and wastewater treatment market.

The structural dominance of Germany is sustained by infrastructure and demand characteristics operating across multiple commercial dimensions simultaneously. The German federal statistical office's documentation of 8.3 billion cubic metres of annual wastewater quantity and 1,666,268 tonnes of sewage sludge disposal confirms the scale of the water treatment infrastructure whose operational requirements and compliance obligations generate continuous membrane treatment technology procurement across municipal utilities and industrial operators. Germany's population of 83.5 million in the first quarter of 2025 establishes one of Europe's largest public service and municipal infrastructure bases, creating proportionally significant demand for advanced water treatment solutions across both urban and regional water systems. The country's leading position in wastewater treatment technology innovation and the concentration of Europe's most sophisticated water utility operators within Germany's borders create a competitive and commercially attractive market environment that sustains disproportionate investment in advanced membrane treatment technology development and deployment. Germany's structural position as the regional market's dominant geographic and commercial center is expected to remain intact over the forecast period.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Europe Membrane Water and Wastewater Treatment Market Segmentation Analysis

By Product

- Microfiltration

- Ultrafiltration

- Nanofiltration

- Reverse Osmosis

- Others

The segment with highest market share under the Product Category is reverse osmosis, accounting for approximately 35% of the total market. This commanding position reflects the deep structural alignment between reverse osmosis membrane separation capabilities and the specific water purification and wastewater treatment requirements of Europe's most institutionally significant water utility and industrial operator segments, where advanced filtration performance, reliable treatment consistency, and multi-application deployment flexibility make reverse osmosis the reference technology standard across municipal wastewater systems, industrial water reuse projects, and decentralized treatment installations throughout the continent. With more than one-third of total market value concentrated within a single product category, Reverse Osmosis defines the technology investment priorities, system integration frameworks, and competitive positioning strategies of the Europe membrane water and wastewater treatment market.

The structural leadership of Reverse Osmosis is sustained by the treatment performance and operational reliability that have established this technology as the gold standard for advanced water purification across municipal and industrial applications. As Europe's regulatory framework tightens around tertiary and quaternary treatment requirements and water reuse applications expand across stressed regions, reverse osmosis platforms are progressively evolving to support higher throughput capacity, improved energy efficiency, and more seamless integration with decentralized and circular water management system architectures. This technological evolution positions established reverse osmosis membrane providers to capture both sustained replacement demand and expanding application breadth procurement across Europe's municipal utility and industrial treatment operator base. The segment's structural dominance as the market's primary product category revenue contributor is expected to consolidate over the forecast period.

By End User

- Municipal

- Industrial

- Food & Beverage

- Pharmaceuticals

- Chemicals

- Power

- Oil & Gas

- Others

The segment with highest market share under the end-User is municipal, accounting for approximately 35% of the total market. This dominant position reflects the foundational role of public water and wastewater systems in supporting urban populations, enabling environmental compliance, and sustaining public health infrastructure across Europe's cities and municipalities, where reliable treatment performance, continuous operational availability, and consistent water quality delivery are non-negotiable operational requirements linked directly to public service quality and regulatory compliance standing. With more than one-third of total market value anchored in municipal applications, this segment defines the treatment performance standards, system reliability expectations, and procurement evaluation criteria that shape membrane technology development and supplier competitive advantage across the regional market.

The structural leadership of Municipal Applications is being actively sustained by the accelerating implementation of the revised Urban Wastewater Treatment Directive and the expanding scope of regulatory requirements across tertiary treatment, nutrient removal, and micropollutant elimination. The European Commission's quantification of EUR 6.6 billion in annual economic benefits deliverable by 2045 through directive implementation confirms that municipal treatment infrastructure upgrade investment is not discretionary but economically justified and institutionally prioritized across European local governments. As regulatory compliance timelines mature and municipal utilities systematically evaluate treatment technology upgrades to satisfy increasingly stringent discharge and output quality standards, the commercial importance of advanced reverse osmosis and complementary membrane technologies in supporting municipal infrastructure modernization is driving sustained and expanding investment across Europe's local government water management budgets. The Municipal Applications segment's position as the market's dominant end-user anchor and primary revenue driver is expected to strengthen over the forecast period.

Various Market Players in Europe Membrane Water and Wastewater Treatment Market

The companies mentioned below are highly active in the Europe membrane water and wastewater treatment market, occupying a considerable portion of the market and shaping industry progress.

- MANN+HUMMEL Water & Membrane Solutions

- Alfa Laval

- Nitto Hydranautics Europe

- Veolia Water Technologies & Solutions

- Xylem Europe

- DuPont Water Solutions

- Toray Membrane Europe

- Pentair X-Flow

- Kubota Water and Environment Europe

- Kovalus Separation Solutions

- Mitsubishi Chemical Aqua Solutions

- Asahi Kasei Microza

Market News & Updates

- Veolia Water Technologies & Solutions, 2025:

Veolia announced that it would equip France’s largest treated wastewater reuse project in Argelès-sur-Mer, a facility expected to reuse 1.3 million cubic meters of treated wastewater annually and irrigate nearly 700 hectares of farmland, with Veolia specifically stating it will deploy an innovative membrane ultrafiltration solution to achieve Category A water quality under French regulations. For the European water and wastewater treatment membrane market, this is one of the most important verified developments because it demonstrates how membrane reuse systems are moving into large, policy-relevant municipal applications where climate resilience, agricultural water security, and regulatory-grade recycled water quality are becoming central procurement drivers.

- Alfa Laval, 2026:

Alfa Laval disclosed its role in Denmark’s EXTRACT project, a three-year, publicly supported initiative launched in February 2026 to recover biopolymers from sewage sludge using advanced separation technologies including membrane filtration, with Alfa Laval serving as the sole technology supplier and the project estimating potential residual sludge reductions of 15–25 percent and annual carbon dioxide savings of up to 20,000 tons if scaled across Denmark. For the European membrane market, this is a significant strategic development because it expands the role of membrane systems beyond conventional water purification into higher-value resource recovery and circular wastewater treatment, an area likely to gain traction as European utilities and industries pursue decarbonization and recovery-led treatment models.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- Europe Membrane Water and Wastewater Treatment Market Policies, Regulations, and Standards

- Europe Membrane Water and Wastewater Treatment Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- Europe Membrane Water and Wastewater Treatment Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Product

- Microfiltration- Market Insights and Forecast 2022-2032, USD Million

- Ultrafiltration- Market Insights and Forecast 2022-2032, USD Million

- Nanofiltration- Market Insights and Forecast 2022-2032, USD Million

- Reverse Osmosis- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Material

- Polymeric- Market Insights and Forecast 2022-2032, USD Million

- Ceramic- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Application

- Water Treatment- Market Insights and Forecast 2022-2032, USD Million

- Wastewater Treatment- Market Insights and Forecast 2022-2032, USD Million

- Desalination- Market Insights and Forecast 2022-2032, USD Million

- Water Reuse/Reclamation- Market Insights and Forecast 2022-2032, USD Million

- Industrial Process Water- Market Insights and Forecast 2022-2032, USD Million

- By End User

- Municipal- Market Insights and Forecast 2022-2032, USD Million

- Industrial- Market Insights and Forecast 2022-2032, USD Million

- Food & Beverage- Market Insights and Forecast 2022-2032, USD Million

- Pharmaceuticals- Market Insights and Forecast 2022-2032, USD Million

- Chemicals- Market Insights and Forecast 2022-2032, USD Million

- Power- Market Insights and Forecast 2022-2032, USD Million

- Oil & Gas- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel

- Retail Offline- Market Insights and Forecast 2022-2032, USD Million

- Direct Sales- Market Insights and Forecast 2022-2032, USD Million

- Distributors/Dealers- Market Insights and Forecast 2022-2032, USD Million

- OEM/System Integrator Sales- Market Insights and Forecast 2022-2032, USD Million

- EPC/Project-Based Sales- Market Insights and Forecast 2022-2032, USD Million

- Retail Online- Market Insights and Forecast 2022-2032, USD Million

- Company-Owned Websites- Market Insights and Forecast 2022-2032, USD Million

- Distributor Online Portals- Market Insights and Forecast 2022-2032, USD Million

- B2B E-Marketplaces- Market Insights and Forecast 2022-2032, USD Million

- E-Procurement/Tender Platforms- Market Insights and Forecast 2022-2032, USD Million

- Retail Offline- Market Insights and Forecast 2022-2032, USD Million

- By Country

- Germany

- UK

- France

- Spain

- Italy

- Netherland

- Rest of Europe

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Product

- Market Size & Growth Outlook

- Germany Membrane Water and Wastewater Treatment Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Product- Market Insights and Forecast 2022-2032, USD Million

- By Material- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- UK Membrane Water and Wastewater Treatment Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Product- Market Insights and Forecast 2022-2032, USD Million

- By Material- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- France Membrane Water and Wastewater Treatment Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Product- Market Insights and Forecast 2022-2032, USD Million

- By Material- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Spain Membrane Water and Wastewater Treatment Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Product- Market Insights and Forecast 2022-2032, USD Million

- By Material- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Italy Membrane Water and Wastewater Treatment Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Product- Market Insights and Forecast 2022-2032, USD Million

- By Material- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Netherland Membrane Water and Wastewater Treatment Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Product- Market Insights and Forecast 2022-2032, USD Million

- By Material- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Veolia Water Technologies & Solutions

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Xylem Europe

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- DuPont Water Solutions

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Toray Membrane Europe

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Pentair X-Flow

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- MANN+HUMMEL Water & Membrane Solutions

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Alfa Laval

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Nitto Hydranautics Europe

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Kubota Water and Environment Europe

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Kovalus Separation Solutions

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Mitsubishi Chemical Aqua Solutions

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Asahi Kasei Microza

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Veolia Water Technologies & Solutions

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Product |

|

| By Material |

|

| By Application |

|

| By End User |

|

| By Sales Channel |

|

| By Country |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.