UAE Heat Exchangers Market Report: Trends, Growth and Forecast (2026-2032)

By Product Type (Shell & Tube Heat Exchangers, Plate Heat Exchangers, Air Cooled Heat Exchangers, Finned Tube Heat Exchangers, Others), By Industry (Power Generation, Chemical & Petrochemical, Oil & Gas, Automotive & Manufacturing, Food & Beverage/Pharma, HVAC/Building Services, Others), By Application (Process Heating/Cooling, Energy Recovery/Waste Heat Recovery, Refrigeration & Air Conditioning, Steam Condensation/Boiler Systems, Others), By Material Type (Stainless Steel, Carbon Steel, Copper, Aluminum, Others), By Region (Dubai, Abu Dhabi, Sharjah, Northern Emirates) ... Read more

|

Major Players

|

UAE Heat Exchangers Market Statistics and Insights, 2026

- Market Size Statistics

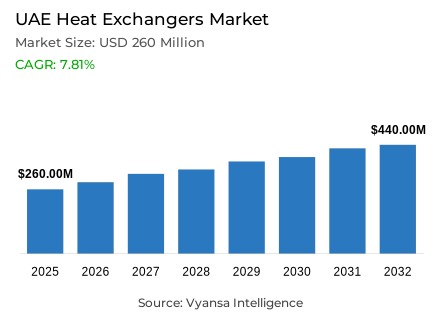

- Heat exchangers market size in UAE was valued at USD 260 million in 2025 and is estimated at USD 275 million in 2026.

- The market size is expected to grow to USD 440 million by 2032.

- Market to register a CAGR of around 7.81% during 2026-32.

- Product Type Shares

- Shell & tube heat exchangers grabbed market share of 40%.

- Competition

- More than 10 companies are actively engaged in producing heat exchangers in UAE.

- Top 5 companies acquired around 50% of the market share.

- Xylem, SPX FLOW, Dolphin Heat Transfer, Alfa Laval, Kelvion etc., are few of the top companies.

- Industry

- Oil & gas grabbed 30% of the market.

UAE Heat Exchangers Market Outlook

The UAE heat exchangers market size was valued at USD 260 million in 2025 and is projected to grow from USD 275 million in 2026 to USD 440 million by 2032, exhibiting a CAGR of 7.81% during the forecast period. This growth path reflects a steady expansion phase, supported by ongoing industrial activity, energy infrastructure demand, and the need for reliable thermal management across major operating sectors in the country.

A significant part of current demand remains concentrated in the product landscape, where Shell & Tube heat exchangers account for 40% of the overall market. Their leading position reflects broad industrial preference for equipment that can support continuous operations and dependable performance in process-heavy environments. Across the broader industry structure, heat exchangers continue to play an important role in helping operators manage temperature control, process stability, equipment efficiency, and maintenance reliability across essential industrial installations.

Demand is also shaped by end-use concentration, with the Oil & Gas industry holding 30% of the total market. This shows that thermal equipment requirements remain closely tied to hydrocarbon processing, refining, and related industrial operations. In practical terms, heat exchangers remain relevant because they support essential heat transfer functions across systems where uptime, safety, operating consistency, and reliable thermal circulation remain important to daily performance and project continuity.

The overall outlook remains positive through 2032 as industrial users continue investing in efficient and dependable thermal systems. Growth is supported by product preference, strong industrial end use, and the wider need for stable heat transfer across operating environments. With these conditions remaining favorable, heat exchangers are expected to strengthen their role in plant efficiency, process reliability, replacement demand, operational continuity, export-linked industrial development, and long-term industrial performance across the UAE’s evolving energy, utility, and manufacturing landscape over the forecast period ahead for end users nationwide.

UAE Heat Exchangers Market Growth Driver

Core Energy Assets Keep Equipment Demand Active

Strong demand from hydrocarbon processing remains the primary growth driver. The UAE continues to expand and modernise large energy assets. These assets depend on stable thermal systems to maintain output. According to ADNOC, its refining facilities can process nearly one million barrels of crude oil and condensates per day. They also supply more than 40 million tons of refined products every year. This scale keeps replacement and new equipment demand active. Heat transfer reliability directly affects throughput and process continuity across these environments.

The same pull comes from upstream and national energy planning. According to Emirates News Agency, the Ministry of Energy and Infrastructure confirms the UAE targets crude production capacity of 5 million barrels per day by 2027. As energy capacity deepens, heat exchanger demand stays well supported. Dependable thermal control across refining, processing, and associated industrial systems remains essential to meeting this target.

UAE Heat Exchangers Market Challenge

Efficiency Pressures Raise the Performance Bar

Tighter efficiency and water-performance requirements are becoming the main challenge. Suppliers and end users must now align thermal systems with more demanding standards. According to the Ministry of Energy and Infrastructure, the UAE National Demand Side Management Program 2050 targets energy savings of 40% and water savings of 50% by 2050 compared with business as usual. This raises the bar for conventional thermal equipment. Applications where water use, energy loss, and operating efficiency are closely monitored face the greatest pressure.

Compliance pressure is also becoming more formal across utility-linked systems. According to the Abu Dhabi Department of Energy, the Water Quality Regulations 2025 supersede the 2021 edition and took effect from 1 January 2025. As performance expectations tighten, manufacturers and buyers face a harder balance. Reliability, redesign needs, and compliance costs must all be managed together. This applies across desalination, cooling, and process-heavy industrial installations across the country.

Unlock Market Intelligence

Explore the market potential with our data-driven report

UAE Heat Exchangers Market Trend

Low-Carbon Utility Systems Shape Technology Direction

A clear market trend is the shift toward low-carbon desalination and energy-efficient cooling infrastructure. This shift increases demand for advanced thermal equipment. According to EWEC, the Taweelah Reverse Osmosis plant is the world's largest RO desalination facility. It supplies 909,000 cubic metres of water per day. According to EWEC, the under-construction Mirfa 2 RO project will add up to 546,000 cubic metres per day. The UAE is clearly moving toward large-scale, efficiency-led water infrastructure. Dependable heat transfer and process control are central to these systems.

The pattern extends further through future project planning. According to EWEC, the Future Reverse Osmosis project in Abu Dhabi is planned to desalinate up to 273,000 cubic metres per day. As more low-carbon and water-efficient systems enter the pipeline, heat exchanger demand shifts accordingly. Equipment must support stronger thermal performance, durability, and operating efficiency. This applies across new utility and industrial assets being developed across the Emirates.

UAE Heat Exchangers Market Opportunity

Local Manufacturing Opens a New Value Corridor

Localised manufacturing is creating the strongest opportunity in this market. It can shorten delivery cycles and position the UAE as a regional supply hub. According to the Government of Dubai Media Office, Jafza and A-HEAT are developing the largest heat exchanger production facility in the GCC. According to the announcement, the plant will span 1.2 million square feet. The built-up area will cover 400,000 square feet. This investment opens room for domestic production and faster order fulfilment. It also enables closer customer access across energy, cooling, and industrial applications.

The opportunity grows further because the project targets higher-efficiency product lines. According to the Government of Dubai Media Office, the facility will manufacture heat exchangers using natural refrigerants such as CO2 and ammonia. According to the same source, its aicore smart control solutions can cut energy use by up to 30%. Water consumption reductions of up to 90% are also projected.

Unlock Market Intelligence

Explore the market potential with our data-driven report

UAE Heat Exchangers Market Segmentation Analysis

By Product Type

- Shell & Tube Heat Exchangers

- Plate Heat Exchangers

- Air Cooled Heat Exchangers

- Finned Tube Heat Exchangers

- Others

The segment with highest market share under the product type category is Shell and Tube heat exchangers, accounting for 40% of the overall industry. This makes it the leading product segment in the UAE heat exchangers market. Its strong position reflects wide industrial use of designs known for dependable operation. Practical maintenance and suitability across demanding process conditions also contribute to this leadership. Steady thermal transfer remains essential in daily plant operations and cycles.

This leadership shows that buyers continue to prefer products that fit industrial environments without adding complexity. Shell and Tube heat exchangers are widely used across facilities that value durability and stable heat transfer. Long service life is another key reason buyers choose this product type. With a 40% share, the segment continues to shape product demand and purchasing patterns. It also drives the broader competitive structure of the industry across the UAE during the forecast period.

By Industry

- Power Generation

- Chemical & Petrochemical

- Oil & Gas

- Automotive & Manufacturing

- Food & Beverage/Pharma

- HVAC/Building Services

- Others

The segment with highest market share under the industry category is Oil and Gas, accounting for 30% of the overall industry. This makes it the leading end-use segment in the UAE heat exchangers market. Its strong position reflects the close link between thermal equipment demand and the country's large hydrocarbon base. Refining, processing, and related activities require dependable temperature control. Efficient heat transfer across major operating environments and systems is equally critical to sustained performance.

This dominance also highlights how industrial demand stays supported by sectors where process continuity matters most. The Oil and Gas segment creates regular need for equipment that performs under demanding conditions. With a 30% share, this segment continues to influence end-user demand and investment focus. It also shapes the wider application pattern for heat exchangers across the UAE through the forecast period, supporting long-term commercial relevance and equipment demand.

List of Companies Covered in UAE Heat Exchangers Market

The companies listed below are highly influential in the UAE heat exchangers market, with a significant market share and a strong impact on industry developments.

- Xylem

- SPX FLOW

- Dolphin Heat Transfer

- Alfa Laval

- Kelvion

- Danfoss

- GEA

- HISAKA WORKS

- NASH Engineering FZCO

- Techno Futura

Market News & Updates

- Alfa Laval, 2026:

Alfa Laval launched FreeWaterLoop, an external cooling system for data center facility loops that combines pump engineering, heat exchanger technology, and filtration in one integrated system, and the company said it is designed to reduce footprint, support high-density computing, and minimize net water consumption by using natural water sources. For the UAE heat exchanger market, this is a significant development because the country’s cooling-intensive built environment and expanding data-center ecosystem favor integrated thermal systems that save space, improve efficiency, and reduce water stress under demanding operating conditions.

- Danfoss, 2026:

Danfoss’s February 2026 launch of the B3-260C brazed plate heat exchanger adds a high-efficiency option for CDU-based cooling, with the company emphasizing precise temperature control, low pumping losses, and improved PUE for mission-critical environments. This is especially relevant to the UAE heat exchanger market because advanced plate heat exchangers are increasingly important in high-performance cooling networks, including data centers and other temperature-sensitive applications where energy efficiency, system compactness, and continuous uptime are critical purchasing factors

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- UAE Heat Exchanger Market Policies, Regulations, and Standards

- UAE Heat Exchanger Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- UAE Heat Exchanger Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Product Type

- Shell & Tube Heat Exchangers- Market Insights and Forecast 2022-2032, USD Million

- Plate Heat Exchangers- Market Insights and Forecast 2022-2032, USD Million

- Air Cooled Heat Exchangers- Market Insights and Forecast 2022-2032, USD Million

- Finned Tube Heat Exchangers- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Industry

- Power Generation- Market Insights and Forecast 2022-2032, USD Million

- Chemical & Petrochemical- Market Insights and Forecast 2022-2032, USD Million

- Oil & Gas- Market Insights and Forecast 2022-2032, USD Million

- Automotive & Manufacturing- Market Insights and Forecast 2022-2032, USD Million

- Food & Beverage/Pharma- Market Insights and Forecast 2022-2032, USD Million

- HVAC/Building Services- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Application

- Process Heating/Cooling- Market Insights and Forecast 2022-2032, USD Million

- Energy Recovery/Waste Heat Recovery- Market Insights and Forecast 2022-2032, USD Million

- Refrigeration & Air Conditioning- Market Insights and Forecast 2022-2032, USD Million

- Steam Condensation/Boiler Systems- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Material Type

- Stainless Steel- Market Insights and Forecast 2022-2032, USD Million

- Carbon Steel- Market Insights and Forecast 2022-2032, USD Million

- Copper- Market Insights and Forecast 2022-2032, USD Million

- Aluminum- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Region

- Dubai

- Abu Dhabi

- Sharjah

- Northern Emirates

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Product Type

- Market Size & Growth Outlook

- UAE Shell & Tube Heat Exchangers Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Industry- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Material Type- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- UAE Plate Heat Exchangers Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Industry- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Material Type- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- UAE Air Cooled Heat Exchangers Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Industry- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Material Type- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- UAE Finned Tube Heat Exchangers Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Industry- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Material Type- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Alfa Laval

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Kelvion

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Danfoss

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- GEA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- HISAKA WORKS

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Xylem

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- SPX FLOW

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Dolphin Heat Transfer

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- NASH Engineering FZCO

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Techno Futura

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Alfa Laval

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Product Type |

|

| By Industry |

|

| By Application |

|

| By Material Type |

|

| By Region |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.