Saudi Arabia Heat Exchangers Market Report: Trends, Growth and Forecast (2026-2032)

By Product Type (Shell & Tube Heat Exchangers, Plate Heat Exchangers, Air Cooled Heat Exchangers, Finned Tube Heat Exchangers, Others), By Industry (Power Generation, Chemical & Petrochemical, Oil & Gas, Automotive & Manufacturing, Food & Beverage/Pharma, HVAC/Building Services, Others), By Application (Process Heating/Cooling, Energy Recovery/Waste Heat Recovery, Refrigeration & Air Conditioning, Steam Condensation/Boiler Systems, Others), By Material Type (Stainless Steel, Carbon Steel, Copper, Aluminum, Others), By Region (East, West, South, Central) ... Read more

|

Major Players

|

Saudi Arabia Heat Exchangers Market Statistics and Insights, 2026

- Market Size Statistics

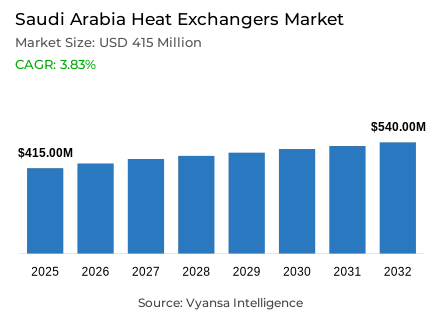

- Heat exchangers market size in Saudi Arabia was valued at USD 415 million in 2025 and is estimated at USD 440 million in 2026.

- The market size is expected to grow to USD 540 million by 2032.

- Market to register a CAGR of around 3.83% during 2026-32.

- Product Type Shares

- Shell & tube heat exchangers grabbed market share of 40%.

- Competition

- More than 10 companies are actively engaged in producing heat exchangers in Saudi Arabia.

- Top 5 companies acquired around 50% of the market share.

- Xylem, Zamil Process Equipment, Arabian Gulf Metal Factory (AGMF), Alfa Laval, Kelvion etc., are few of the top companies.

- Industry

- Oil & gas grabbed 35% of the market.

Saudi Arabia Heat Exchangers Market Outlook

Saudi Arabia heat exchangers market size was valued at USD 415 million in 2025 and is projected to grow from USD 440 million in 2026 to USD 540 million by 2032, exhibiting a CAGR of 3.83% during the forecast period. This reflects a stable demand environment where industrial users continue to rely on thermal equipment for core processing, cooling, and heat recovery applications across major sectors.

A large part of the outlook remains tied to established product demand. Shell & Tube heat exchangers account for 40% of the overall share, showing that end users continue to prefer designs that can handle demanding operating conditions and support reliable performance over long operating cycles. In many industrial settings, heat exchangers remain essential where pressure handling, durability, and steady thermal transfer are important.

market demand also stays concentrated in the Kingdom’s core processing base. Oil & Gas accounts for 35% of the market, highlighting the continued importance of thermal systems in upstream, refining, and related operations. Across these applications, heat exchangers support temperature control, process stability, and operational efficiency, making them a regular part of plant infrastructure and maintenance planning.

Overall, the market outlook remains steady over the forecast period, supported by ongoing use across established industrial operations rather than rapid structural change. The combination of strong product concentration in Shell & Tube systems and the continued leadership of Oil & Gas shows that heat exchangers remain closely linked to the Kingdom’s long-standing energy and process market base.

Saudi Arabia Heat Exchangers Market Growth Driver

Industrial Processing Momentum Sustains Core Thermal Equipment Procurement Demand

The sustained and institutionally documented expansion of Saudi Arabia's industrial processing activity across oil and gas, refining, petrochemical, and manufacturing sectors represents the primary structural driver of heat exchanger demand. This processing-driven demand dynamic functions as a persistent procurement imperative that sustains consistent equipment installation, replacement, and maintenance investment across the Kingdom's most thermally intensive industrial plant environments. Growth is anchored in operational necessity rather than discretionary capital expenditure, confirming that heat exchanger demand will remain commercially resilient across economic cycles whose impact on Saudi industrial activity is moderated by the Kingdom's structural commitment to hydrocarbon processing and industrial capacity maintenance.

The quantitative evidence validating this processing-driven demand dynamic is documented with precision by GASTAT. The Industrial Production Index rises 7.9% year on year in June 2025, with manufacturing activity growing 11.1%, refined petroleum products increasing 15.3%, and chemicals and chemical products rising 18.7% across the same period. These throughput growth rates confirm that the processing intensity of Saudi Arabia's most thermally demanding industrial sectors is expanding at a pace that generates consistent and compounding heat exchanger procurement requirements across both new installation and active replacement demand cycles. Oil production reaching 9.36 million barrels per day in June 2025, up from 8.83 million barrels per day a year earlier, further validates the upstream operational momentum that sustains thermal equipment demand across the full hydrocarbon value chain over the forecast period.

Saudi Arabia Heat Exchangers Market Challenge

Import Dependence Creates Procurement Timing and Supply Chain Exposure

The Saudi Arabia heat exchangers market's substantial reliance on imported industrial equipment and components represents the most consequential supply-side challenge confronting operators and procurement planners, creating systematic sourcing timeline, cost management, and supply availability vulnerabilities that can affect project execution, maintenance cycle adherence, and replacement planning across the Kingdom's most operationally critical industrial environments. In a procurement context where specialized thermal management equipment and critical spare parts may require international sourcing across extended lead times, the concentration of import dependency among a limited number of origin countries creates compounding supply chain risk that is particularly consequential for operators managing tight maintenance windows and production continuity obligations.

The structural depth and concentration specificity of this import dependency challenge are quantified with precision by GASTAT. Machinery, electrical equipment, and parts account for 30.6% of total Saudi Arabian imports in June 2025 and rise 29.0% compared with June 2024, confirming the scale and growth trajectory of industrial equipment import reliance across the Kingdom's procurement environment. China alone accounts for 27.9% of total imports in June 2025, while the top ten import source countries together represent 66.5% of all imports into Saudi Arabia. This sourcing concentration confirms that procurement planning across the heat exchangers market carries meaningful exposure to supply conditions, shipping timelines, and commercial terms within a relatively narrow set of international supplier markets. For procurement teams and equipment suppliers operating in this environment, supply chain diversification and strategic inventory management represent critical risk mitigation investments over the forecast period.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Saudi Arabia Heat Exchangers Market Trend

Water Sector Efficiency Advancement Reshapes Thermal Equipment Specifications

The progressive advancement of efficiency benchmarks and technology standards across Saudi Arabia's world-scale desalination and water processing infrastructure represents the defining structural trend reshaping heat exchanger product specifications, material requirements, and performance expectations across the Kingdom's most rapidly evolving thermal management equipment application domain. This water sector efficiency trend is moving the procurement conversation around heat exchangers in desalination environments beyond standard equipment replacement decisions into the domain of measurable thermal performance improvement, energy intensity optimization, and corrosion resistance under demanding saline operating conditions, dimensions that are progressively redefining how water sector operators evaluate and specify heat exchanger procurement requirements.

The technical specificity and operational scale of this water sector efficiency trend are documented with authority by the Saudi Water Authority. Saudi Arabia's desalinated water output exceeds 11.1 million cubic meters per day, confirming the Kingdom's position as the world's largest producer of desalinated water and validating the scale of water processing infrastructure whose thermal management equipment requirements are generating consistent procurement activity across the heat exchangers market. Shuaiba-5 operates with a production capacity of 664,000 cubic meters per day and an energy consumption rate of only 2.34 kWh per cubic meter, setting a performance benchmark that is progressively elevating thermal efficiency expectations across new and modernized desalination facility procurement specifications. As these efficiency standards become more prominent across the Kingdom's water infrastructure development program, heat exchangers capable of supporting lower energy consumption and stronger materials performance will attract disproportionate procurement share over the forecast period.

Saudi Arabia Heat Exchangers Market Opportunity

Desalination Infrastructure Scale Creates Durable Thermal Equipment Demand

The continued expansion and performance-driven modernization of Saudi Arabia's desalination and water processing infrastructure creates a structurally significant and commercially durable opportunity for heat exchanger suppliers whose products combine the corrosion resistance, thermal efficiency credentials, and operational durability required across the Kingdom's most technologically advanced water sector installations. This desalination opportunity is distinguished from conventional oil and gas replacement demand by its growth trajectory, its advancing performance specification requirements, and its alignment with the Kingdom's strategic Vision 2030 water security objectives, creating procurement conditions where engineering quality and materials performance capability carry disproportionate commercial weight relative to price considerations alone.

The quantitative scale and project specificity of this desalination opportunity are documented with precision by the Saudi Water Authority. Daily desalinated water output exceeding 11.1 million cubic meters confirms an installed base of world-scale water processing infrastructure whose operational continuity, performance maintenance, and capacity expansion requirements generate consistent and commercially significant heat exchanger procurement activity. AlKhafji's capacity of up to 90,000 cubic meters per day using solar-supported technology and Shuaiba-5's delivery of 664,000 cubic meters per day for a strategically important supply zone confirm that both advanced technology integration and large-scale operational performance are defining the next generation of Saudi desalination infrastructure whose thermal management equipment requirements favor suppliers with proven credentials across high-efficiency and corrosion-resistant heat exchanger design. Suppliers that align product development, materials engineering, and commercial positioning with the advancing efficiency and sustainability expectations of Saudi Arabia's water sector will capture disproportionate value from this structurally significant and policy-supported market opportunity over the forecast period.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Saudi Arabia Heat Exchangers Market Segmentation Analysis

By Product Type

- Shell & Tube Heat Exchangers

- Plate Heat Exchangers

- Air Cooled Heat Exchangers

- Finned Tube Heat Exchangers

- Others

The segment with highest market share under the Product Type is Shell and Tube heat exchangers, accounting for approximately 40% of the total market. This leading position reflects the deep structural alignment between shell and tube design characteristics and the specific thermal management requirements of Saudi Arabia's most industrially active processing sectors, where operational reliability under continuous high-load conditions, robust pressure containment performance, and broad compatibility with diverse process fluids and temperature ranges make this configuration the unambiguous product of choice across oil and gas, refining, petrochemical, and water desalination procurement contexts. With two-fifths of total market value concentrated within a single product category, Shell and Tube heat exchangers define the commercial priorities, fabrication investment frameworks, and competitive dynamics of the Saudi Arabia heat exchangers market.

The structural leadership of Shell and Tube heat exchangers is sustained by the industrial familiarity and application breadth that have established this configuration as the default thermal management specification across the Kingdom's most capital-intensive and operationally demanding process industries. As efficiency expectations in water desalination facilities advance toward the benchmark set by Shuaiba-5's energy consumption rate of only 2.34 kWh per cubic meter, the performance specification requirements placed on heat exchanger equipment are progressively elevating the engineering quality threshold that all competing configurations must meet. Shell and tube designs, with their established performance credibility and well-documented maintenance economics across demanding corrosion-sensitive environments, are well positioned to satisfy these advancing specifications. The segment's structural market leadership is expected to remain intact over the forecast period.

By Industry

- Power Generation

- Chemical & Petrochemical

- Oil & Gas

- Automotive & Manufacturing

- Food & Beverage/Pharma

- HVAC/Building Services

- Others

The segment with highest market share under the market is Oil and Gas, accounting for approximately 35% of the total market. This dominant position reflects the foundational role of thermal management systems in the Kingdom's most commercially significant and operationally complex industrial sector, where upstream production operations, refinery processing systems, and petrochemical manufacturing facilities generate continuous and compounding demand for heat transfer equipment whose reliable performance is directly linked to plant output consistency and operational safety. With more than one-third of total market value anchored in oil and gas sector demand, this market segment defines the procurement specification standards, service life expectations, and maintenance investment frameworks of the Saudi Arabia heat exchangers market.

The structural leadership of the Oil and Gas segment is being actively sustained by the processing activity momentum that GASTAT documents across the Kingdom's refining and petrochemical sectors. Refined petroleum products rising 15.3% and chemicals and chemical products growing 18.7% year on year in June 2025 confirm the throughput expansion that generates consistent replacement, upgrade, and new installation demand across the heat exchanger product base serving these industries. Oil production reaching 9.36 million barrels per day in June 2025 further confirms the upstream operational scale that sustains consistent equipment procurement across the Kingdom's producing and processing infrastructure. The Oil and Gas segment's position as the dominant commercial demand anchor of the Saudi Arabia heat exchangers market is expected to remain structurally intact.

List of Companies Covered in Saudi Arabia Heat Exchangers Market

The companies listed below are highly influential in the Saudi Arabia heat exchangers market, with a significant market share and a strong impact on industry developments.

- Xylem

- Zamil Process Equipment

- Arabian Gulf Metal Factory (AGMF)

- Alfa Laval

- Kelvion

- Danfoss

- GEA

- HISAKA WORKS

- Al Gaswa Steel Industries

- MIS Arabia

Market News & Updates

- Kelvion, 2025:

Kelvion launched its next-generation hybrid cooling solutions for data centres, highlighting optimized energy and water efficiency, advanced controls, and reliable performance even in high ambient temperatures through dry-mode and wet-mode operation. For the Saudi Arabia heat exchanger market, this is highly relevant because the Kingdom’s industrial and digital infrastructure projects operate in extremely hot conditions where water use, power efficiency, and cooling resilience are central buying criteria, making hybrid heat-rejection technologies especially attractive for future deployments.

- Danfoss, 2026:

Danfoss introduced the B3-260C brazed plate heat exchanger for data center cooling, emphasizing its low-pressure-drop design, high heat-transfer efficiency, and support for up to 1 MW capacities in CDU applications. For Saudi Arabia, the launch matters because the market is increasingly shaped by energy-efficient cooling requirements across industrial facilities and emerging digital infrastructure, and compact, high-efficiency plate heat exchangers are well aligned with the Kingdom’s push toward more sustainable and higher-performance thermal systems.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- Saudi Arabia Heat Exchanger Market Policies, Regulations, and Standards

- Saudi Arabia Heat Exchanger Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- Saudi Arabia Heat Exchanger Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Product Type

- Shell & Tube Heat Exchangers- Market Insights and Forecast 2022-2032, USD Million

- Plate Heat Exchangers- Market Insights and Forecast 2022-2032, USD Million

- Air Cooled Heat Exchangers- Market Insights and Forecast 2022-2032, USD Million

- Finned Tube Heat Exchangers- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Industry

- Power Generation- Market Insights and Forecast 2022-2032, USD Million

- Chemical & Petrochemical- Market Insights and Forecast 2022-2032, USD Million

- Oil & Gas- Market Insights and Forecast 2022-2032, USD Million

- Automotive & Manufacturing- Market Insights and Forecast 2022-2032, USD Million

- Food & Beverage/Pharma- Market Insights and Forecast 2022-2032, USD Million

- HVAC/Building Services- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Application

- Process Heating/Cooling- Market Insights and Forecast 2022-2032, USD Million

- Energy Recovery/Waste Heat Recovery- Market Insights and Forecast 2022-2032, USD Million

- Refrigeration & Air Conditioning- Market Insights and Forecast 2022-2032, USD Million

- Steam Condensation/Boiler Systems- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Material Type

- Stainless Steel- Market Insights and Forecast 2022-2032, USD Million

- Carbon Steel- Market Insights and Forecast 2022-2032, USD Million

- Copper- Market Insights and Forecast 2022-2032, USD Million

- Aluminum- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Region

- East

- West

- South

- Central

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Product Type

- Market Size & Growth Outlook

- Saudi Arabia Shell & Tube Heat Exchangers Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Industry- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Material Type- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Saudi Arabia Plate Heat Exchangers Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Industry- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Material Type- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Saudi Arabia Air Cooled Heat Exchangers Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Industry- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Material Type- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Saudi Arabia Finned Tube Heat Exchangers Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Industry- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Material Type- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Alfa Laval

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Kelvion

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Danfoss

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- GEA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- HISAKA WORKS

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Xylem

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Zamil Process Equipment

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Arabian Gulf Metal Factory (AGMF)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Al Gaswa Steel Industries

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- MIS Arabia

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Alfa Laval

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Product Type |

|

| By Industry |

|

| By Application |

|

| By Material Type |

|

| By Region |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.