UK Footwear Market Report: Trends, Growth and Forecast (2026-2032)

By Category (Children's Footwear (Infants (0-9 Months) Foot Length (CM) (8.3-8.9, 9.2-9.5, 10.1-10.5), Toddlers (9 Months - 4 Years) Foot Length (CM) (10.8, 11.4-11.7, 12.1-12.7, 13.0-13.3, 14.0-14.3, 14.6-15.2, 15.6-15.9, 16.5), Little Kids (4-7 Years) Foot Length (CM) (16.8, 17.1-17.8, 18.1-18.4, 19.1-19.4, 19.7-20.6, 21.0-21.6), Big Kids (7-12 Years) Foot Length (CM) (21.9, 22.2-23.5, 24.1-24.8)), Women's Footwear (Foot Length (CM) (20.8, 21.3-21.6, 22.2-22.5, 23.0-23.8, 24.1-24.6, 25.1-25.9, 26.2-26.7, 27.6)), Men's Footwear (Foot Length (CM) (23.5, 24.1-24.8, 25.4-25.7, 26.0-26.7, 27.0-27.9, 28.3-28.6, 29.4, 30.2, 31.0-31.8))), By Product Type (Casual, Athletic/Sports, Formal, Others), By Sales Channel (Retail Online, Retail Offline), By Material (Leather, Textile, Rubber, Synthetic, Canvas), By Price (Mass, Premium), By Footwear Type (Shoes (Sneakers, Boots), Sandals & Slippers (Flip-Flops)), By Application (Conventional Footwear (Daily Wear, Work/Office Wear, Outdoor & Adventure, Sports & Fitness, Party/Occasion Wear), Functional/Therapeutic Footwear (Therapeutic/Orthopedic, Medicated Slippers, Acupressure Slippers)) ... Read more

|

Major Players

|

UK Footwear Market Statistics and Insights, 2026

- Market Size Statistics

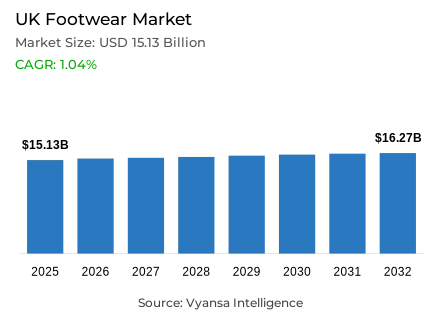

- Footwear market size in UK was estimated at USD 15.13 billion in 2025.

- The market size is expected to grow to USD 16.27 billion by 2032.

- Market to register a CAGR of around 1.04% during 2026-32.

- Category Shares

- Women's footwear grabbed market share of 40%.

- Competition

- More than 20 companies are actively engaged in producing footwear in UK.

- Top 5 companies acquired around 35% of the market share.

- Next Plc, Skechers USA Ltd, Cinven Ltd, Nike (UK) Ltd, adidas (UK) Ltd etc., are few of the top companies.

- Sales Channel

- Retail online grabbed 53% of the market.

UK Footwear Market Outlook

The UK footwear market is expected to record a stable, average growth over the forecast period of 2026–2032, which is backed by the ongoing demand of quality, durability and valuebased products. The UK footwear sales are estimated to be USD 15.13 billion in 2025 and are expected to grow to USD 16.27 billion in 2032, which is a compound annual growth rate of about 1.04% in the forecast period. The growth will be slow, with end users still being wary of discretionary spending, but footwear will still enjoy the benefits of being a necessity and replacement demand, especially in casual and sportswear.

Market performance will be influenced by end user preference of longlasting and versatile footwear. The relaxed nature of dress codes and the longterm popularity of sports and outdoor activities contribute to demand in men, women, and children footwear. Women footwear is a cornerstone of the market, with a significant interest in campusstyle footwear and everyday casual footwear, whereas children footwear enjoys a higher emphasis on health, fit, and value factors.

Purchasing decisions will be more affected by sustainability and inclusivity. The pressure of regulations and the growing awareness of the environment force brands to use recycled materials, circular economic models and repair services. At the same time, programs on adaptive footwear, larger size collections and inclusive design reinforce brand trust and loyalty, especially among valueconscious UK end users.

The market will keep being transformed by digitalisation. Retail online is already playing a dominant role, which is enhanced by improved delivery services, return policies and digital solutions like sizing technology. With brands striking a balance between affordability, sustainability and innovation, the UK footwear market will continue to experience stable growth over the forecast period.

UK Footwear Market Growth Driver

Value and Quality Focus Sustains Footwear Demand

The end users across the United Kingdom are valueconscious and qualityconscious in their footwear purchases, hence maintaining stable demand amidst the wider economic forces. According to the data provided by the Office for National Statistics (ONS), the price inflation of the clothing and footwear sector has been growing over the past years, which is a sign of real demand and cost pressures, and not a distortion of transactions. The end user Price Index (CPI) of clothing and footwear increased to about 3.6% in December 2025, which shows that end users are still actively involved in this category.

This quality and longevity focus in the buying process forces the brands to strike a balance between longevity and price sensitivity, which is in line with the end user preference of footwear that provides comfort and value. The UK households have also shown a modest increase in total expenditure on goods, including footwear. According to the ONS, household final consumption, including clothing and footwear, grew by 0.3% in Q3 2025 relative to the previous quarter.These trends justify the longterm demand of footwear, as customers consider such products as the necessary goods that should be both functional and longlasting.

UK Footwear Market Challenge

Inflationary Pressures Constrain Discretionary Footwear Spending

The continued inflation limits the discretionary spending of the UK end users on nonessential goods like shoes. According to official statistics released by the Office for National Statistics, the wider end user Prices Index (CPI) was around 3.5% in 2025, with clothing and footwear adding to the price growth in the overall basket. High prices of basic goods and services decrease the amount of disposable income that can be used to buy fashion items, thus making end users more discriminating in their buying behaviour.

Despite the fact that inflation has since eased since postpandemic highs, costofliving pressures still affect purchasing behaviour. Increasing costs of necessities like food and utilities, as shown by expanded CPI reporting, increase budgetary pressure, leading some households to postpone or reduce purchases that are considered nonurgent. As a result, footwear companies are pressed to keep end user interest without eliciting price opposition, particularly among pricesensitive end user groups.

Unlock Market Intelligence

Explore the market potential with our data-driven report

UK Footwear Market Trend

Sustainability and Inclusive Practices Reshape Footwear Choices

The most noticeable tendencies that influence the UK footwear market is the growing significance of sustainability and inclusivity concerns. The regulatory demands of UK and European Union institutions are pushing towards environmental responsibility, and brands are reacting with sustainable materials and circulareconomy actions, including recycling and repair services. Although the official sustainability indicators of footwear are changing, the governmental indicators and the general policy trends emphasize the environmental pledges in the retail market.

This transition is supported by end user behaviour data. The general UK spending patterns show that people are more involved in products that are seen to be environmentally friendly. Indicatively, households have shown greater spending on services and goods that are in line with longterm value, implying openness to sustainably positioned categories. The changing end user expectations are also reflected in inclusive practices, including extended size ranges and adaptive designs, which require brands to be creative in product development and marketing to capture diversity and accessibility.

UK Footwear Market Opportunity

Digital Retail and Tech Innovation Expand Market Reach

Retail Online is a significant prospect to the UK footwear market, with online platforms still defining the way end users learn about and buy products. The official UK statistics show that clothing and footwear retail are major contributors to the growth of household spending. According to the ONS, household spending on goods such as footwear grew by 0.7% yearonyear in Q3 2025, indicating the growth of online activity and the development of new channels of purchase.

retail online and technological advances, including virtual fitting with augmented reality and personalised recommendations based on artificial intelligence, can improve the customer experience and decrease friction in online shopping experiences. With the growing power of digital infrastructure and the increasing penetration of mobile commerce, footwear brands can use these opportunities to expand market reach, increase conversion rates, and provide more personalised experiences that satisfy end user demands of convenience and customisation.

Unlock Market Intelligence

Explore the market potential with our data-driven report

UK Footwear Market Segmentation Analysis

By Category

- Children's Footwear

- Infants (0-9 Months) Foot Length (CM)

- 8.3-8.9

- 9.2-9.5

- 10.1-10.5

- Toddlers (9 Months - 4 Years) Foot Length (CM)

- 10.8

- 11.4-11.7

- 12.1-12.7

- 13.0-13.3

- 14.0-14.3

- 14.6-15.2

- 15.6-15.9

- 16.5

- Little Kids (4-7 Years) Foot Length (CM)

- 16.8

- 17.1-17.8

- 18.1-18.4

- 19.1-19.4

- 19.7-20.6

- 21.0-21.6

- Big Kids (7-12 Years) Foot Length (CM)

- 21.9

- 22.2-23.5

- 24.1-24.8

- Infants (0-9 Months) Foot Length (CM)

- Women's Footwear

- Foot Length (CM)

- 20.8

- 21.3-21.6

- 22.2-22.5

- 23.0-23.8

- 24.1-24.6

- 25.1-25.9

- 26.2-26.7

- 27.6

- Foot Length (CM)

- Men's Footwear

- Foot Length (CM)

- 23.5

- 24.1-24.8

- 25.4-25.7

- 26.0-26.7

- 27.0-27.9

- 28.3-28.6

- 29.4

- 30.2

- 31.0-31.8

- Foot Length (CM)

Women's footwear constitutes the segment with the highest share within the category segmentation, accounting for approximately 40% of the UK footwear market. This leading position is supported by substantial and consistent demand for casual, campusstyle, and everyday footwear, which continues to resonate with female end users. Women's footwear benefits from elevated purchase frequency, greater fashion sensitivity, and a comprehensive range of styles suited to work, leisure, and social occasions.

Throughout the 2026–32 forecast period, women's footwear is expected to retain its dominant market share as casualisation of dress codes and demand for durable, comfortable designs persist. Brands are focusing on combining stylistic appeal with longevity and value propositions, which aligns effectively with current end user priorities. Sustainability initiatives and inclusive sizing are additionally particularly relevant within this segment, further reinforcing its importance within the overall UK footwear market.

By Sales Channel

- Retail Online

- Retail Offline

Retail online represents the segment with the highest share within the sales channel segmentation, maintaining approximately 53% of total footwear sales in the UK. Retail online has established itself as the preferred channel for numerous end users due to convenience factors, extensive product choice, competitive pricing, and flexible delivery and returns policies. The ability to compare brands and prices efficiently has strengthened the position of online platforms.

Throughout the 2026–32 forecast period, retail online is expected to maintain its leadership position as brands continue to invest in retail online infrastructure, digital marketing, and enhanced online experiences. Innovations such as virtual tryon technologies, improved sizing tools, and artificial intelligencedriven recommendations will further support online purchasing behaviour. While physical retail establishments remain important for fitting experiences and experiential shopping, Retail online will continue to be the primary growth driver within the UK footwear market.

List of Companies Covered in UK Footwear Market

The companies listed below are highly influential in the UK footwear market, with a significant market share and a strong impact on industry developments.

- Next Plc

- Skechers USA Ltd

- Cinven Ltd

- Nike (UK) Ltd

- adidas (UK) Ltd

- Clarks Footwear Ltd

- Primark Stores Ltd

- Marks & Spencer Plc

- Fila Holding SpA

- Asics UK Ltd

Competitive Landscape

The UK footwear market is characterised by intense competition between established global leaders, fast-growing challengers, and value-focused specialists. Nike remains the leading player despite sales decline and share erosion, reflecting product fatigue and the delayed effects of changes to its distribution strategy. adidas strengthened its competitive position, driven largely by strong demand for women’s footwear, particularly heritage styles such as Samba, Gazelle, and Handball Spezial, alongside newer incubator models. Challenger brands including Hoka One One, ASICS, On, and Puma gained traction by offering innovation-led designs, differentiated pricing, and greater individuality. In children’s footwear, retailers such as Deichmann and Clarks reinforced competitiveness through value-led promotions and fit guarantees. Overall, competition increasingly centres on product innovation, sustainability credentials, value-for-money positioning, and responsiveness to evolving consumer priorities.

Frequently Asked Questions

Related Report

1. Market Segmentation

1.1. Research Scope

1.2. Research Methodology

1.3. Definitions and Assumptions

2. Executive Summary

3. UK Footwear Market Policies, Regulations, and Standards

4. UK Footwear Market Dynamics

4.1. Growth Factors

4.2. Challenges

4.3. Trends

4.4. Opportunities

5. UK Footwear Market Statistics, 2022-2032F

5.1. Market Size & Growth Outlook

5.1.1.By Revenues in USD Million

5.1.2.By Units Sold in Thousand Units

5.2. Market Segmentation & Growth Outlook

5.2.1.By Category

5.2.1.1. Children's Footwear- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.1. Infants (0-9 Months) Foot Length (CM)- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.1.1. 8.3-8.9- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.1.2. 9.2-9.5- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.1.3. 10.1-10.5- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.2. Toddlers (9 Months - 4 Years) Foot Length (CM)- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.2.1. 10.8- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.2.2. 11.4-11.7- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.2.3. 12.1-12.7- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.2.4. 13.0-13.3- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.2.5. 14.0-14.3- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.2.6. 14.6-15.2- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.2.7. 15.6-15.9- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.2.8. 16.5- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.3. Little Kids (4-7 Years) Foot Length (CM)- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.3.1. 16.8- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.3.2. 17.1-17.8- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.3.3. 18.1-18.4- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.3.4. 19.1-19.4- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.3.5. 19.7-20.6- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.3.6. 21.0-21.6- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.4. Big Kids (7-12 Years) Foot Length (CM)- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.4.1. 21.9- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.4.2. 22.2-23.5- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.4.3. 24.1-24.8- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2. Women's Footwear- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.1. Foot Length (CM)- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.1.1. 20.8- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.1.2. 21.3-21.6- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.1.3. 22.2-22.5- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.1.4. 23.0-23.8- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.1.5. 24.1-24.6- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.1.6. 25.1-25.9- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.1.7. 26.2-26.7- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.1.8. 27.6- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3. Men's Footwear- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3.1. Foot Length (CM)- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3.1.1. 23.5- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3.1.2. 24.1-24.8- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3.1.3. 25.4-25.7- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3.1.4. 26.0-26.7- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3.1.5. 27.0-27.9- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3.1.6. 28.3-28.6- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3.1.7. 29.4- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3.1.8. 30.2- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3.1.9. 31.0-31.8- Market Insights and Forecast 2022-2032, USD Million

5.2.2.By Product Type

5.2.2.1. Casual- Market Insights and Forecast 2022-2032, USD Million

5.2.2.2. Athletic/Sports- Market Insights and Forecast 2022-2032, USD Million

5.2.2.3. Formal- Market Insights and Forecast 2022-2032, USD Million

5.2.2.4. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.3.By Sales Channel

5.2.3.1. Retail Online- Market Insights and Forecast 2022-2032, USD Million

5.2.3.2. Retail Offline- Market Insights and Forecast 2022-2032, USD Million

5.2.4.By Material

5.2.4.1. Leather- Market Insights and Forecast 2022-2032, USD Million

5.2.4.2. Textile- Market Insights and Forecast 2022-2032, USD Million

5.2.4.3. Rubber- Market Insights and Forecast 2022-2032, USD Million

5.2.4.4. Synthetic- Market Insights and Forecast 2022-2032, USD Million

5.2.4.5. Canvas- Market Insights and Forecast 2022-2032, USD Million

5.2.5.By Price

5.2.5.1. Mass- Market Insights and Forecast 2022-2032, USD Million

5.2.5.2. Premium- Market Insights and Forecast 2022-2032, USD Million

5.2.6.By Footwear Type

5.2.6.1. Shoes- Market Insights and Forecast 2022-2032, USD Million

5.2.6.1.1. Sneakers- Market Insights and Forecast 2022-2032, USD Million

5.2.6.1.2. Boots- Market Insights and Forecast 2022-2032, USD Million

5.2.6.2. Sandals & Slippers- Market Insights and Forecast 2022-2032, USD Million

5.2.6.2.1. Flip-Flops- Market Insights and Forecast 2022-2032, USD Million

5.2.7.By Application

5.2.7.1. Conventional Footwear- Market Insights and Forecast 2022-2032, USD Million

5.2.7.1.1. Daily Wear- Market Insights and Forecast 2022-2032, USD Million

5.2.7.1.2. Work/Office Wear- Market Insights and Forecast 2022-2032, USD Million

5.2.7.1.3. Outdoor & Adventure- Market Insights and Forecast 2022-2032, USD Million

5.2.7.1.4. Sports & Fitness- Market Insights and Forecast 2022-2032, USD Million

5.2.7.1.5. Party/Occasion Wear- Market Insights and Forecast 2022-2032, USD Million

5.2.7.2. Functional/Therapeutic Footwear- Market Insights and Forecast 2022-2032, USD Million

5.2.7.2.1. Therapeutic/Orthopedic- Market Insights and Forecast 2022-2032, USD Million

5.2.7.2.2. Medicated Slippers- Market Insights and Forecast 2022-2032, USD Million

5.2.7.2.3. Acupressure Slippers- Market Insights and Forecast 2022-2032, USD Million

5.2.8.By Competitors

5.2.8.1. Competition Characteristics

5.2.8.2. Market Share & Analysis

6. UK Children's Footwear Market Statistics, 2022-2032

6.1. Market Size & Growth Outlook

6.1.1.By Revenues in USD Million

6.1.2.By Units Sold in Thousand Units

6.2. Market Segmentation & Growth Outlook

6.2.1.By Category- Market Insights and Forecast 2022-2032, USD Million

6.2.2.By Product Type- Market Insights and Forecast 2022-2032, USD Million

6.2.3.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

6.2.4.By Material- Market Insights and Forecast 2022-2032, USD Million

6.2.5.By Price- Market Insights and Forecast 2022-2032, USD Million

6.2.6.By Footwear Type- Market Insights and Forecast 2022-2032, USD Million

6.2.7.By Application- Market Insights and Forecast 2022-2032, USD Million

7. UK Women's Footwear Market Statistics, 2022-2032

7.1. Market Size & Growth Outlook

7.1.1.By Revenues in USD Million

7.1.2.By Units Sold in Thousand Units

7.2. Market Segmentation & Growth Outlook

7.2.1.By Category- Market Insights and Forecast 2022-2032, USD Million

7.2.2.By Product Type- Market Insights and Forecast 2022-2032, USD Million

7.2.3.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

7.2.4.By Material- Market Insights and Forecast 2022-2032, USD Million

7.2.5.By Price- Market Insights and Forecast 2022-2032, USD Million

7.2.6.By Footwear Type- Market Insights and Forecast 2022-2032, USD Million

7.2.7.By Application- Market Insights and Forecast 2022-2032, USD Million

8. UK Men's Footwear Market Statistics, 2022-2032

8.1. Market Size & Growth Outlook

8.1.1.By Revenues in USD Million

8.1.2.By Units Sold in Thousand Units

8.2. Market Segmentation & Growth Outlook

8.2.1.By Category- Market Insights and Forecast 2022-2032, USD Million

8.2.2.By Product Type- Market Insights and Forecast 2022-2032, USD Million

8.2.3.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

8.2.4.By Material- Market Insights and Forecast 2022-2032, USD Million

8.2.5.By Price- Market Insights and Forecast 2022-2032, USD Million

8.2.6.By Footwear Type- Market Insights and Forecast 2022-2032, USD Million

8.2.7.By Application- Market Insights and Forecast 2022-2032, USD Million

9. Competitive Outlook

9.1. Company Profiles

9.1.1.Nike (UK) Ltd

9.1.1.1. Business Description

9.1.1.2. Product Portfolio

9.1.1.3. Collaborations & Alliances

9.1.1.4. Recent Developments

9.1.1.5. Financial Details

9.1.1.6. Others

9.1.2.adidas (UK) Ltd

9.1.2.1. Business Description

9.1.2.2. Product Portfolio

9.1.2.3. Collaborations & Alliances

9.1.2.4. Recent Developments

9.1.2.5. Financial Details

9.1.2.6. Others

9.1.3.Clarks Footwear Ltd

9.1.3.1. Business Description

9.1.3.2. Product Portfolio

9.1.3.3. Collaborations & Alliances

9.1.3.4. Recent Developments

9.1.3.5. Financial Details

9.1.3.6. Others

9.1.4.Primark Stores Ltd

9.1.4.1. Business Description

9.1.4.2. Product Portfolio

9.1.4.3. Collaborations & Alliances

9.1.4.4. Recent Developments

9.1.4.5. Financial Details

9.1.4.6. Others

9.1.5.Marks & Spencer Plc

9.1.5.1. Business Description

9.1.5.2. Product Portfolio

9.1.5.3. Collaborations & Alliances

9.1.5.4. Recent Developments

9.1.5.5. Financial Details

9.1.5.6. Others

9.1.6.Next Plc

9.1.6.1. Business Description

9.1.6.2. Product Portfolio

9.1.6.3. Collaborations & Alliances

9.1.6.4. Recent Developments

9.1.6.5. Financial Details

9.1.6.6. Others

9.1.7.Skechers USA Ltd

9.1.7.1. Business Description

9.1.7.2. Product Portfolio

9.1.7.3. Collaborations & Alliances

9.1.7.4. Recent Developments

9.1.7.5. Financial Details

9.1.7.6. Others

9.1.8.Cinven Ltd

9.1.8.1. Business Description

9.1.8.2. Product Portfolio

9.1.8.3. Collaborations & Alliances

9.1.8.4. Recent Developments

9.1.8.5. Financial Details

9.1.8.6. Others

9.1.9.Fila Holding SpA

9.1.9.1. Business Description

9.1.9.2. Product Portfolio

9.1.9.3. Collaborations & Alliances

9.1.9.4. Recent Developments

9.1.9.5. Financial Details

9.1.9.6. Others

9.1.10. Asics UK Ltd

9.1.10.1. Business Description

9.1.10.2. Product Portfolio

9.1.10.3. Collaborations & Alliances

9.1.10.4. Recent Developments

9.1.10.5. Financial Details

9.1.10.6. Others

10. Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Category |

|

| By Product Type |

|

| By Sales Channel |

|

| By Material |

|

| By Price |

|

| By Footwear Type |

|

| By Application |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.