UK Bottled Water Market Report: Trends, Growth and Forecast (2026-2032)

By Type of Water (Carbonated Bottled Water, Flavoured Bottled Water, Functional Bottled Water, Still Bottled Water), By Sub Types (Purified (Desalinated, Atmospheric Generated, Others), Mineral, Other (Spring, Alkaline, Other)), By Packaging Material (Flexible Packaging (Aluminium, Pouches), Glass, Rigid Plastic (PET Bottles, Thin Wall Plastic Containers, Others)), By Price Category (Budget, Economy, Premium), By Pack Size (100 ml, 125 ml, 200 ml, 250 ml, 330 ml, 370 ml, 450 ml, 500 ml, 591 ml, 750 ml, 1,000 ml, 1,500 ml, 4,000 ml, 5,000 ml, Others), By Sales Channel (On Trade (Restaurants, Hotels, Cafes, Others), Off Trade (Grocery Retailers (Convenience Retail, Supermarkets, Hypermarkets, Small Local Grocer), Non-Grocery Retailers (General Merchandise Stores, Health and Beauty Specialists), Vending, E-commerce)), By Region (England, Wales, Scotland, Northern Ireland) ... Read more

|

Major Players

|

UK Bottled Water Market Statistics and Insights, 2026

- Market Size Statistics

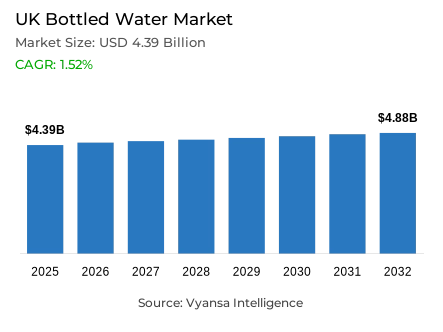

- Bottled water market size in UK was estimated at USD 4.39 billion in 2025.

- The market size is expected to grow to USD 4.88 billion by 2032.

- Market to register a CAGR of around 1.52% during 2026-32.

- Type of Water Shares

- Still bottled water grabbed market share of 55%.

- Competition

- More than 20 companies are actively engaged in producing bottled water in UK.

- Top 5 companies acquired around 40% of the market share.

- Asda Group Ltd, Clearly Drinks Ltd, Coca-Cola Enterprises Ltd, Danone Waters (UK & Ireland) Ltd, Nestle Waters UK Ltd etc., are few of the top companies.

- Sales Channel

- Off trade grabbed 90% of the market.

UK Bottled Water Market Outlook

The United Kingdom bottled water market is projected to be USD 4.39 billion in 2025 and is expected to increase to USD 4.88 billion by 2032 with a CAGR of about 1.52% between 2026 and 2032. The growth is backed by the growing health awareness and the growing end user preference to clean-label hydration. The issue of drinking water quality and the implementation of strict PFAS limits starting January 2025 only strengthen the focus of end users on safety and purity. At the same time, the fact that the sugar consumption in the country is decreasing nationwide highlights the fact that bottled water is a healthier, calorie-free substitute to sugary beverages.

The competitive environment is still influenced by regulatory trends and environmental forces. The next Deposit Return Scheme (DRS), which will be implemented in October 2027, will require producers to change their packaging policies and invest in recycling compliance. As the recycling rate of plastic packaging waste was estimated between 64.1% and 75.2% in 2024, sustainability demands are high, and companies are turning to recycled materials and are trying to develop circular packaging.

Innovation of products is also one of the major market forces. Still water is the dominant market segment with a market share of 60%, which shows high daily usage and low prices. Functional and flavoured versions are on the rise as end users want more health benefits.

90% of the market in terms of distribution is constituted by off-trade channels, which is supported by supermarkets, hypermarkets, and the growing e-commerce market. The trends of digital grocery adoption and bulk purchasing are expected to sustain consistent category growth up to 2032.

UK Bottled Water Market Growth DriverRising Health and Safety Concerns Supporting Consumption

The increase in the concern of quality of drinking water is serving as a major growth driver. In January 2025, the UK Drinking Water Inspectorate announced a new cumulative limit of 100 nanograms per litre (ng/L) of 48 PFAS chemicals. This shows the increased attention to water safety and contamination monitoring. This trend reinforces consumer awareness of the possible pollutants, including microplastics and chemical residues, directing households to focus on safer hydration choices. The introduction of stricter safety standards strengthens consumer confidence in packaged hydration options, as people are becoming more concerned about purity and transparency in their daily consumption decisions.

The growth of demand is also supported by health-conscious behaviour, with end users still cutting down on their sugar consumption. According to the UK Government, the Soft Drinks Industry Levy has contributed to a 47% reduction in the sugar content of soft drinks between 2015 and 2024, which is a long-term change in favor of healthier beverage options. This shift is directly beneficial to bottled water, which is generally perceived as a calorie-free, clean-label hydration choice that supports long-term population health objectives.

UK Bottled Water Market ChallengeGrowing Environmental and Packaging Compliance Pressures

The growing environmental regulations pose operational difficulties to producers. The UK Government has affirmed the implementation of a Deposit Return Scheme (DRS), to be implemented in October 2027, which will entail deposits on single-use drink containers to enhance recycling performance. This policy requires manufacturers to repackage, invest in collection systems, and meet circular-economy goals. These new compliance requirements increase the cost of production and the complexity of operations, especially to small manufacturers who have limited sustainability investment capacity.

The issue of plastic waste management is still a significant issue, which affects brand image and industry responsibility. According to the UK Department for Environment, Food and Rural Affairs, the recycling of plastic packaging waste in 2024 was estimated between 64.1% and 75.2%, which indicates that the use of plastic bottles continues to be scrutinized by the environment. End users are increasingly seeking sustainable packaging options, which poses reputational risks to brands that do not live up to sustainability expectations and forces manufacturers to hasten their investment in recycled materials and packaging innovation.

Unlock Market Intelligence

Explore the market potential with our data-driven report

UK Bottled Water Market TrendExpansion of Digital Grocery and Home Delivery Channels

The demand of end users is shifting towards drinks that provide additional health value other than simple hydration. According to NHS England, 64.5% of adults in England were overweight or living with obesity as of 2024, which reinforces the interest of the population in healthier beverage options that can help manage weight and maintain health. This increasing health consciousness is driving a positive demand towards functional hydration products that include vitamins, minerals, and electrolytes that aid in immunity, energy and recovery advantages.

The wider wellness movement also enhances the use of improved hydration products. The Office for Health Improvement and Disparities states that the UK is still undertaking national measures to enhance dietary practices and promote healthier beverage consumption among all age groups. end users are also demanding natural flavouring, additive-free, and products that promote lifestyle health objectives. These tastes are transforming product-innovation strategies and prompting brands to diversify with portfolios around health-oriented hydration experiences.

UK Bottled Water Market OpportunityShift Toward Functional and Enhanced Hydration Preferences

The high rate of online grocery adoption presents a good growth potential of packaged hydration products. According to the UK Office for National Statistics, internet sales constitute 32.4% of total retail sales in 2025, which indicates the high end user preference to digital purchasing behaviour. This transition is advantageous to bottled hydration products, especially bulk and multipack products, because online delivery eliminates transport inconvenience on heavy products and increases purchasing frequency.

Digital retail growth is still supported by convenience-based end user lifestyles. The UK Department of Business and Trade confirms that the adoption of e-commerce is still the most active among younger populations and urban families, which stimulates the demand of fast delivery services and grocery models based on subscriptions. Retailers are still increasing the range of products, customised promotions and fast delivery systems thus providing good environment where more end users can access the products and repeat buying behaviour to packaged hydration products.

Unlock Market Intelligence

Explore the market potential with our data-driven report

UK Bottled Water Market Segmentation Analysis

By Type of Water

- Carbonated Bottled Water

- Flavoured Bottled Water

- Functional Bottled Water

- Still Bottled Water

The largest share segment is still bottled water under the type category with 60% of the market share. Still water has a high level of end user preference because it is commonly viewed as a simple, natural and daily hydration choice. The segment has the advantage of mass consumption in the household, high availability in the retail outlets and the fact that it is a healthier substitute to the sugary drinks. Its flexibility in home and mobile consumption also enhances end user acceptance in various age groups and lifestyle categories.

Affordability and high penetration of the private-label also favor still bottled water. Retailers are also increasing multipack products and value-based product lines, making them more accessible to price-sensitive families. The segment has a steady demand because end users are focusing on clean-label hydration and minimise sugar consumption. Also, the ability of still water to be used with functional and enhanced formulations allows manufacturers to launch vitamin-enriched and mineral-enriched versions, which will help sustain end user interest and product development.

By Sales Channel

- On Trade

- Off Trade

The off-trade distribution segment, which constitutes 90% of the market, is the segment with the largest share under the sales-channel category. The off-trade channels prevail because of the large networks of supermarkets and hypermarkets with competitive prices, a broader range of brands and the ability to buy in bulk. Megastores are still increasing shelf space, advertising, and multipack options, enabling end users to buy hydration products effectively to use on a regular basis.

The increase in adoption of e-commerce groceries and discount retail also contributes to off-trade dominance. Online grocery stores make it easy to access bulk packaged hydration items, and discount stores appeal to cost-sensitive customers with low-priced with products having their own label. These channels increase accessibility in both urban and rural areas and this helps end users to enjoy promotional prices and subscription-based delivery services. The dominance of value-based retail channels has remained to support the leadership of off-trade distribution in the total product availability and end user buying behaviour.

List of Companies Covered in UK Bottled Water Market

The companies listed below are highly influential in the UK bottled water market, with a significant market share and a strong impact on industry developments.

- Asda Group Ltd

- Clearly Drinks Ltd

- Coca-Cola Enterprises Ltd

- Danone Waters (UK & Ireland) Ltd

- Nestle Waters UK Ltd

- Highland Spring Ltd

- Tesco Plc

- J Sainsbury Plc

- Britvic Soft Drinks Ltd

- Dash Brands Ltd

Competitive Landscape

In 2025, Nestle Waters UK Ltd remains the leading player in the UK bottled water market, supported by the strong performance of its Buxton and Nestle Pure Life brands. These brands benefit from wide distribution coverage and a strong reputation for local sourcing. Although Nestle’s share has declined slightly, it continues to lead ahead of Danone Waters (UK & Ireland) Ltd, whose Evian and Volvic brands retain strong premium appeal. Both companies continue investing in sustainability initiatives, including the rollout of 100% PET bottles and premium collaborations, reinforcing their environmental and lifestyle positioning.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- UK Bottled Water Market Policies, Regulations, and Standards

- UK Bottled Water Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- UK Bottled Water Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Volume (Million Litres)

- Market Segmentation & Growth Outlook

- By Type of Water

- Carbonated Bottled Water- Market Insights and Forecast 2022-2032, USD Million

- Flavoured Bottled Water- Market Insights and Forecast 2022-2032, USD Million

- Functional Bottled Water- Market Insights and Forecast 2022-2032, USD Million

- Still Bottled Water- Market Insights and Forecast 2022-2032, USD Million

- By Sub Types

- Purified- Market Insights and Forecast 2022-2032, USD Million

- Desalinated- Market Insights and Forecast 2022-2032, USD Million

- Atmospheric Generated- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- Mineral- Market Insights and Forecast 2022-2032, USD Million

- Other (Spring, Alkaline, Other) - Market Insights and Forecast 2022-2032, USD Million

- Purified- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material

- Flexible Packaging- Market Insights and Forecast 2022-2032, USD Million

- Aluminium- Market Insights and Forecast 2022-2032, USD Million

- Pouches- Market Insights and Forecast 2022-2032, USD Million

- Glass- Market Insights and Forecast 2022-2032, USD Million

- Rigid Plastic- Market Insights and Forecast 2022-2032, USD Million

- PET Bottles- Market Insights and Forecast 2022-2032, USD Million

- Thin Wall Plastic Containers- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- Flexible Packaging- Market Insights and Forecast 2022-2032, USD Million

- By Price Category

- Budget- Market Insights and Forecast 2022-2032, USD Million

- Economy- Market Insights and Forecast 2022-2032, USD Million

- Premium- Market Insights and Forecast 2022-2032, USD Million

- By Pack Size

- 100 ml- Market Insights and Forecast 2022-2032, USD Million

- 125 ml- Market Insights and Forecast 2022-2032, USD Million

- 200 ml- Market Insights and Forecast 2022-2032, USD Million

- 250 ml- Market Insights and Forecast 2022-2032, USD Million

- 330 ml- Market Insights and Forecast 2022-2032, USD Million

- 370 ml- Market Insights and Forecast 2022-2032, USD Million

- 450 ml- Market Insights and Forecast 2022-2032, USD Million

- 500 ml- Market Insights and Forecast 2022-2032, USD Million

- 591 ml- Market Insights and Forecast 2022-2032, USD Million

- 750 ml- Market Insights and Forecast 2022-2032, USD Million

- 1,000 ml- Market Insights and Forecast 2022-2032, USD Million

- 1,500 ml- Market Insights and Forecast 2022-2032, USD Million

- 4,000 ml- Market Insights and Forecast 2022-2032, USD Million

- 5,000 ml- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel

- On Trade- Market Insights and Forecast 2022-2032, USD Million

- Restaurants- Market Insights and Forecast 2022-2032, USD Million

- Hotels- Market Insights and Forecast 2022-2032, USD Million

- Cafes- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- Off Trade- Market Insights and Forecast 2022-2032, USD Million

- Grocery Retailers- Market Insights and Forecast 2022-2032, USD Million

- Convenience Retail- Market Insights and Forecast 2022-2032, USD Million

- Supermarkets- Market Insights and Forecast 2022-2032, USD Million

- Hypermarkets- Market Insights and Forecast 2022-2032, USD Million

- Small Local Grocer- Market Insights and Forecast 2022-2032, USD Million

- Non-Grocery Retailers- Market Insights and Forecast 2022-2032, USD Million

- General Merchandise Stores- Market Insights and Forecast 2022-2032, USD Million

- Health and Beauty Specialists- Market Insights and Forecast 2022-2032, USD Million

- Vending- Market Insights and Forecast 2022-2032, USD Million

- E-commerce- Market Insights and Forecast 2022-2032, USD Million

- Grocery Retailers- Market Insights and Forecast 2022-2032, USD Million

- On Trade- Market Insights and Forecast 2022-2032, USD Million

- By Region

- England

- Wales

- Scotland

- Northern Ireland

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Type of Water

- Market Size & Growth Outlook

- UK Carbonated Bottled Water Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Volume (Million Litres)

- Market Segmentation & Growth Outlook

- By Sub Types- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Pack Size- Market Insights and Forecast 2022-2032, USD Million

- By Price Category- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- UK Flavoured Bottled Water Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Volume (Million Litres)

- Market Segmentation & Growth Outlook

- By Sub Types- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Pack Size- Market Insights and Forecast 2022-2032, USD Million

- By Price Category- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- UK Functional Bottled Water Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Volume (Million Litres)

- Market Segmentation & Growth Outlook

- By Sub Types- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Pack Size- Market Insights and Forecast 2022-2032, USD Million

- By Price Category- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- UK Still Bottled Water Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Volume (Million Litres)

- Market Segmentation & Growth Outlook

- By Sub Types- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Pack Size- Market Insights and Forecast 2022-2032, USD Million

- By Price Category- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Danone Waters (UK & Ireland) Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Nestle Waters UK Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Highland Spring Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Tesco Plc

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- J Sainsbury Plc

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Asda Group Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Clearly Drinks Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Coca-Cola Enterprises Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Britvic Soft Drinks Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Dash Brands Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Danone Waters (UK & Ireland) Ltd

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Type of Water |

|

| By Sub Types |

|

| By Packaging Material |

|

| By Price Category |

|

| By Pack Size |

|

| By Sales Channel |

|

| By Region |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.