UK Baby and Child-Specific Products Market Report: Trends, Growth and Forecast (2026-2032)

By Product (Hair Care, Skin Care, Sun Care, Toiletries, Baby Wipes, Diapers, Medicated), By Category (Premium, Mass), By Sales Channel (Retail Online, Retail Offline) ... Read more

|

Major Players

|

UK Baby and Child-Specific Products Market Statistics and Insights, 2026

- Market Size Statistics

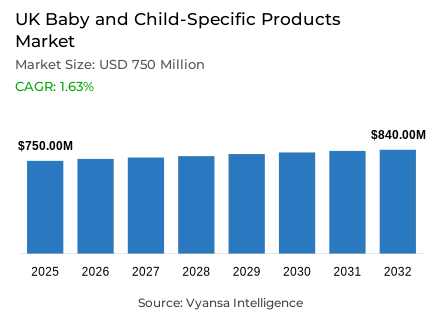

- Baby and child-specific products in UK is estimated at USD 750 million in 2025.

- The market size is expected to grow to USD 840 million by 2032.

- Market to register a cagr of around 1.63% during 2026-32.

- Product Shares

- Baby wipes grabbed market share of 45%.

- Competition

- More than 20 companies are actively engaged in producing baby and child-specific products in UK.

- Top 5 companies acquired around 45% of the market share.

- L'Oréal (UK) Ltd; Teva UK Ltd; Beiersdorf UK Ltd; Procter & Gamble UK Ltd; Johnson & Johnson Ltd etc., are few of the top companies.

- Sales Channel

- Retail online grabbed 55% of the market.

UK Baby and Child-Specific Products Market Outlook

The UK Baby and Child-Specific Products Market is valued at USD 750 million in 2025 and is projected to reach USD 840 million by 2032, registering a CAGR of around 1.63% during 2026-2032. As birth rates decline and limit demand, growth is projected to be relatively slow. According to Office for National Statistics (ONS) data, the number of births fell to 591072, which is the lowest number recorded since 1997. Governments are expected to mitigate declining demand through initiatives like expanding free childcare hours for working parents starting in September 2025 that impact household spend on baby & childcare essentials, sustaining category performance over the next several years.

Baby wipes-the most indispensable and resilient type of product at about 45% total market share-are viewed as an absolute necessity rather than as discretionary. Baby and child-specific sun care products are projected to grow fastest as awareness about the need for sun protection rises and as retailers respond to VAT exemptions for sun care products. Increased demand for dermocosmetics, which offer dermatological benefits as well as aesthetic appeal, is also expected to drive sales in the baby-care segment as parents increasingly focus on gentle, microbiome safe products.

Online retail sales are at the head of the market, accounting for a large portion - approximately 55% - of total sales due to convenience, subscription purchases, and confidence in competitive pricing. Nevertheless, bricks-and mortar retail is still significant; brands such as Childs Farm continue to grow their partnerships with market leaders, such as Marks & Spencer and Holland & Barrett, to cater to the needs of in-store shoppers. Discounters are placing themselves higher in the market with an affordable low-cost alternative as the cost-of-living crisis in the UK weighs heavily on budgets.

As competition heats up brand differentiation will be more paramount. Companies are likely to look beyond online to focus on natural and paraben-free ingredients, and licensed character partnerships to drive a reason to buy. For example, Childs Farm's introduction of Bluey themed products has illustrated how the premise of engaging and character-led branding can engage parents and children to drive brand loyalty in an increasingly busy marketplace.

UK Baby and Child-Specific Products Market Growth Driver

Premiumisation and Innovation Supporting Market Stability

The UK Baby and Child-Specific Products Market continues to develop through premiumisation and innovation. Brands are working towards launching high-quality products using natural and safer ingredients that appeal to health-conscious parents. Companies such as Childs Farm Ltd have gained traction through products like OatDerma and extensive availability through major retailers. The acceptance of dermatologically tested and mild formulations while preserving market value in light of increased price sensitivity.

Parents in UK desire to spend significantly on trusted brands for their children stimulates product development and differentiation. Paraben-free, natural and clean-label items provides stability to the market and continues to grow even if overall volume growth has gone through a slowdown. Innovation-focused strategies combined with premium positioning emboldens consumer confidence and keeps categories relevant over the long-term.

UK Baby and Child-Specific Products Market Challenge

Declining Birth Rate Hindering Market Expansion

The UK Baby and Child-specific Products sector experiences a significant challenge because of the ongoing decline in birth rates, which reduces demand for essential baby care products. With a reduced number of births, future demand will decline more significantly due to a reduced consumer base, which will affect the volume growth opportunities for brands. High childcare costs along with the financial strain on families provide further disincentives to bear children and exacerbates the issue.

Thus, manufacturers are facing a decreased ability to deliver growth in their established product lines. Increased prices and value-added products are relied upon to manage income, but this does not sufficiently replace the demand lost from a decreased target population or to offer an adequate buffer against adverse demographic shifts and long-term decline.

Unlock Market Intelligence

Explore the market potential with our data-driven report

UK Baby and Child-Specific Products Market Trend

Rising Demand for Natural and Dermocosmetic Formulations

An emerging force impacting the UK Baby and Child-Specific Products Market is the growing interest in natural, chemical-free, and dermo-cosmetic-grade formulations. Parents are becoming more aware and cautious about how and what they use on their children; they prefer products containing gentle ingredients that support and maintain skin health. As a result, this shift has led to the presence of more targeted brands like Mustela, which are both dermatologically safe and effective.

The intersection of wellness with skincare regimens, equally supports this trend, as parents view the care of baby skin as a moment of emotional connection and fulfilment, as much as wellbeing. Brands offering and demonstrating potency, safety, and science will continue to flourish. This evolution towards safe, functional, and studied products represents an increased focus towards mindful parenting.

UK Baby and Child-Specific Products Market Opportunity

Character Licensing to Strengthen Brand Appeal

Collaborative agreements for licensing present strong future opportunities in the UK Baby and Child-Specific Products Market. Character-themed product collections are growing in popularity again as brands realize they engage children while also providing a level of trust with parents. Collaborations, such as Childs Farm's Bluey-themed offerings, should appeal to existing consumers and attract new consumers based on previous contact and emotional appeal.

Collaborative agreements increase visibility for a product, while providing brands the ability to differentiate themselves in a crowded marketplace. To take advantage of the popularity of a character, brands can refresh their identity and add desirability to their products by associating themselves with edible and child-friendly brands. The marriage of entertainment value and functional, credible baby care products will generate future growth opportunities for collaboration.

Unlock Market Intelligence

Explore the market potential with our data-driven report

UK Baby and Child-Specific Products Market Segmentation Analysis

By Product

- Hair Care

- Skin Care

- Sun Care

- Toiletries

- Baby Wipes

- Diapers

- Medicated

The segment with highest market share under product category is Baby Wipes, which held approximately 45% of the market. Baby wipes continue to dominate as they are a staple for parents on a daily basis for childcare and are seen as an essential product. Even in the face of inflation and retail prices for Baby Wipes increasing, their popularity is indicative of affordability and the fact that families have baseline price thresholds - baby wipes tend to be seen more as an essential than say personal care products.

Additionally, Baby Wipes are quick, hygienic, and can be used frequently, all the while retaining their leading market position.The demand within this category is also due to innovation and the increase in popularity of natural- and low-ingredient based formulas. Brands that offer mild, chemical free, and hypoallergenic Baby Wipes are seeing a steady flow of sales as parents feel safer about products for their children's skin. With the focus on skin health becoming ever more mainstream, it is likely the Baby Wipe segment will retain strong status as a staple product.

By Sales Channel

- Retail Online

- Retail Offline

The segment with highest market share under sales channel is Retail Online, which held approximately 55% of the market share. Parents have embraced e-commerce due to its convenience, broad assortment, and the ease of subscription-based delivery models that automatically replenish essential products, such as baby wipes and skin care. Online retailers find appeal as many offer discounted prices and promotional bundles, especially during rising cost-of-living pressures.

While retail online are most popular, physical retail remains relevant. Many parents, particularly stay-at-home or part-time workers, prefer in-store shopping to assess the safety and ingredients of baby products before buying. Retailers like Tesco and Marks & Spencer’s have also expanded their in-store offerings of baby products while contributing to the overall experience. The trend toward online purchasing is expected to continue to dominate the category as parents prioritize ease and trustworthiness in meeting their childcare purchasing needs.

List of Companies Covered in UK Baby and Child-Specific Products Market

The companies listed below are highly influential in the UK baby and child-specific products market, with a significant market share and a strong impact on industry developments.

- L'Oréal (UK) Ltd

- Teva UK Ltd

- Beiersdorf UK Ltd

- Procter & Gamble UK Ltd

- Johnson & Johnson Ltd

- Kimberly-Clark Holding Ltd

- Childs Farm Ltd

- Irish Breeze UC

- Boots UK Ltd

- Superdrug Stores Plc

Frequently Asked Questions

Related Report

1. Market Segmentation

1.1. Research Scope

1.2. Research Methodology

1.3. Definitions and Assumptions

2. Executive Summary

3. UK Baby and Child-Specific Product Market Policies, Regulations, and Standards

4. UK Baby and Child-Specific Product Market Dynamics

4.1. Growth Factors

4.2. Challenges

4.3. Trends

4.4. Opportunities

5. UK Baby and Child-Specific Product Market Statistics, 2022-2032F

5.1. Market Size & Growth Outlook

5.1.1.By Revenues in US$ Million

5.2. Market Segmentation & Growth Outlook

5.2.1.By Product

5.2.1.1. Hair Care- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2. Skin Care- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3. Sun Care- Market Insights and Forecast 2022-2032, USD Million

5.2.1.4. Toiletries- Market Insights and Forecast 2022-2032, USD Million

5.2.1.5. Baby Wipes- Market Insights and Forecast 2022-2032, USD Million

5.2.1.6. Diapers- Market Insights and Forecast 2022-2032, USD Million

5.2.1.7. Medicated- Market Insights and Forecast 2022-2032, USD Million

5.2.2.By Category

5.2.2.1. Premium- Market Insights and Forecast 2022-2032, USD Million

5.2.2.2. Mass- Market Insights and Forecast 2022-2032, USD Million

5.2.3.By Sales Channel

5.2.3.1. Retail Online- Market Insights and Forecast 2022-2032, USD Million

5.2.3.2. Retail Offline- Market Insights and Forecast 2022-2032, USD Million

5.2.4.By Competitors

5.2.4.1. Competition Characteristics

5.2.4.2. Market Share & Analysis

6. UK Baby and Child-Specific Hair Care Product Market Statistics, 2022-2032F

6.1. Market Size & Growth Outlook

6.1.1.By Revenues in US$ Million

6.2. Market Segmentation & Growth Outlook

6.2.1.By Category- Market Insights and Forecast 2022-2032, USD Million

6.2.2.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

7. UK Baby and Child-Specific Skin Care Product Market Statistics, 2022-2032F

7.1. Market Size & Growth Outlook

7.1.1.By Revenues in US$ Million

7.2. Market Segmentation & Growth Outlook

7.2.1.By Category- Market Insights and Forecast 2022-2032, USD Million

7.2.2.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

8. UK Baby and Child-Specific Sun Care Product Market Statistics, 2022-2032F

8.1. Market Size & Growth Outlook

8.1.1.By Revenues in US$ Million

8.2. Market Segmentation & Growth Outlook

8.2.1.By Category- Market Insights and Forecast 2022-2032, USD Million

8.2.2.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

9. UK Baby and Child-Specific Toiletries Product Market Statistics, 2022-2032F

9.1. Market Size & Growth Outlook

9.1.1.By Revenues in US$ Million

9.2. Market Segmentation & Growth Outlook

9.2.1.By Category- Market Insights and Forecast 2022-2032, USD Million

9.2.2.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

10. UK Baby and Child-Specific Baby Wipes Market Statistics, 2022-2032F

10.1. Market Size & Growth Outlook

10.1.1. By Revenues in US$ Million

10.2. Market Segmentation & Growth Outlook

10.2.1. By Category- Market Insights and Forecast 2022-2032, USD Million

10.2.2. By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

11. UK Baby and Child-Specific Diapers Market Statistics, 2022-2032F

11.1. Market Size & Growth Outlook

11.1.1. By Revenues in US$ Million

11.2. Market Segmentation & Growth Outlook

11.2.1. By Category- Market Insights and Forecast 2022-2032, USD Million

11.2.2. By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

12. UK Baby and Child-Specific Medicated Product Market Statistics, 2022-2032F

12.1. Market Size & Growth Outlook

12.1.1. By Revenues in US$ Million

12.2. Market Segmentation & Growth Outlook

12.2.1. By Category- Market Insights and Forecast 2022-2032, USD Million

12.2.2. By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

13. Competitive Outlook

13.1. Company Profiles

13.1.1. Procter & Gamble UK Ltd

13.1.1.1. Business Description

13.1.1.2. Product Portfolio

13.1.1.3. Collaborations & Alliances

13.1.1.4. Recent Developments

13.1.1.5. Financial Details

13.1.1.6. Others

13.1.2. Johnson & Johnson Ltd

13.1.2.1. Business Description

13.1.2.2. Product Portfolio

13.1.2.3. Collaborations & Alliances

13.1.2.4. Recent Developments

13.1.2.5. Financial Details

13.1.2.6. Others

13.1.3. Kimberly-Clark Holding Ltd

13.1.3.1. Business Description

13.1.3.2. Product Portfolio

13.1.3.3. Collaborations & Alliances

13.1.3.4. Recent Developments

13.1.3.5. Financial Details

13.1.3.6. Others

13.1.4. Childs Farm Ltd

13.1.4.1. Business Description

13.1.4.2. Product Portfolio

13.1.4.3. Collaborations & Alliances

13.1.4.4. Recent Developments

13.1.4.5. Financial Details

13.1.4.6. Others

13.1.5. Irish Breeze UC

13.1.5.1. Business Description

13.1.5.2. Product Portfolio

13.1.5.3. Collaborations & Alliances

13.1.5.4. Recent Developments

13.1.5.5. Financial Details

13.1.5.6. Others

13.1.6. L'Oréal (UK) Ltd

13.1.6.1. Business Description

13.1.6.2. Product Portfolio

13.1.6.3. Collaborations & Alliances

13.1.6.4. Recent Developments

13.1.6.5. Financial Details

13.1.6.6. Others

13.1.7. Teva UK Ltd

13.1.7.1. Business Description

13.1.7.2. Product Portfolio

13.1.7.3. Collaborations & Alliances

13.1.7.4. Recent Developments

13.1.7.5. Financial Details

13.1.7.6. Others

13.1.8. Beiersdorf UK Ltd

13.1.8.1. Business Description

13.1.8.2. Product Portfolio

13.1.8.3. Collaborations & Alliances

13.1.8.4. Recent Developments

13.1.8.5. Financial Details

13.1.8.6. Others

13.1.9. Boots UK Ltd

13.1.9.1. Business Description

13.1.9.2. Product Portfolio

13.1.9.3. Collaborations & Alliances

13.1.9.4. Recent Developments

13.1.9.5. Financial Details

13.1.9.6. Others

13.1.10. Superdrug Stores Plc

13.1.10.1.Business Description

13.1.10.2.Product Portfolio

13.1.10.3.Collaborations & Alliances

13.1.10.4.Recent Developments

13.1.10.5.Financial Details

13.1.10.6.Others

14. Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Product |

|

| By Category |

|

| By Sales Channel |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.