Turkey Beer Market Report: Trends, Growth and Forecast (2026-2032)

By Product Type (Dark Beer (Ale, Sorghum Beer, Weissbier/Weizen/Wheat Beer), Lager (Flavoured/Mixed Lager, Standard Lager (Premium Lager (Domestic Premium Lager, Imported Premium Lager), Mid-Priced Lager (Domestic Mid-Priced Lager, Imported Mid-Priced Lager), Economy Lager (Domestic Economy Lager, Imported Economy Lager))), Non/Low Alcohol Beer (Low Alcohol Beer, Non Alcoholic Beer), Stout, Others (Porter, Malt etc.)), By Production (Macro Brewery, Micro Brewery, Craft Brewery), By Packaging Type (Bottles, Cans, Others), By Sales Channel (On-Trade, Off-Trade) ... Read more

|

Major Players

|

Turkey Beer Market Statistics and Insights, 2026

- Market Size Statistics

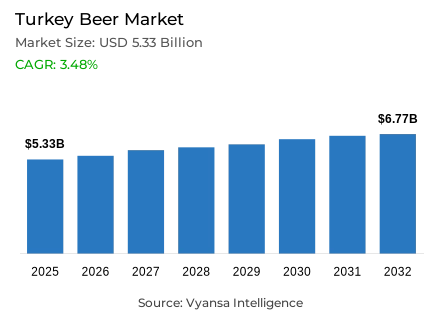

- Beer market size in Turkey was estimated at USD 5.33 billion in 2025.

- The market size is expected to grow to USD 6.77 billion by 2032.

- Market to register a CAGR of around 3.48% during 2026-32.

- Product Type Shares

- Lager grabbed market share of 95%.

- Competition

- More than 5 companies are actively engaged in producing beer in Turkey.

- Top 3 companies acquired around 95% of the market share.

- Karagözoglu Dis Ticaret AS, Efes Pilsen AS, Türk Tuborg Bira ve Malt Sanayii AS etc., are few of the top companies.

- Sales Channel

- Off-trade grabbed 65% of the market.

Turkey Beer Market Outlook

The Turkey beer market was estimated to be USD 5.33 billion in 2025 and is expected to grow to USD 6.77 billion by 2032 with a compound annual growth rate of about 3.48% in the period 2026–2032. This perspective is reinforced by the fact that beer has a high value-for-money image, which has helped the category to be resilient even during high inflation and low end user buying power.

The beer demand will be favourable in the forecast period due to the gradual economic stabilisation and the recovery of social consumption. Domestic premium and mid-priced beers will probably continue to be the core of the growth, supported by the price advantage over imported products and high brand loyalty. It is also estimated that beer will keep on capturing market share of other alcoholic drinks like wine and cider/perry as people will be looking at cheaper alternatives with wider flavour range.

Diversification of products will be one of the competitive strategies. The major competitors like Efes Pilsen AS and Turk Tuborg Bira ve Malt Sanayii AS are likely to keep on adding new formats and seasonal versions to their portfolios. New styles, including ale, weissbier and speciality beers will create incremental volume growth with a low base, and premiumisation will build up slowly as end user confidence rises and tourism grows.

In terms of channel, off-trade will remain the leading channel in the sale of beer, as people will prefer to consume beer at home due to the pressure of costs. But since the second half of the forecast period, on-trade growth will pick up pace as inflation will ease, disposable incomes will recover and tourism will increase. In general, the Turkey beer market is likely to experience a stable growth until 2032 due to innovation, low prices, and the enhancement of the economic situation.

Turkey Beer Market Growth Driver

Value positioning sustains demand amid inflationary pressure

Beer consumption in Turkey remains underpinned by its relative affordability compared to other alcoholic beverages, despite the continued erosion of household purchasing power due to persistent inflationary pressures. According to TurkStat, the average end user inflation rate was 64.8% in 2023, and it is still high in 2024, transforming the household spending patterns. In such circumstances, end users focus on alcoholic beverages with better value, thus maintaining beer consumption as compared to more expensive substitutes.

At the same time, the price competitiveness is improved by domestic production. The Ministry of Industry and Technology of Turkey emphasizes the role of local production in reducing the exposure to imported prices in the food and beverage industry. This structure keeps the beer affordable even in the times of long-term inflation and supports the stable consumption rates even in the times of economic pressure.

Turkey Beer Market Challenge

High inflation constrains discretionary spending and on-trade frequency

Elevated inflationary pressures continue to constrain discretionary spending, posing a sustained challenge for the Turkey market. According to TurkStat, the growth of real household consumption is still modest in 2024, with the growth of income falling behind the growth of prices. This dynamic constrains the rate of social spending, especially in on-trade environments like bars and restaurants, where price elasticity is increased.

Similarly, low disposable income affects end user behaviour in the leisure industries. The Central Bank of the Republic of Turkey reported that tight financial conditions and cost-of-living pressures remain, and they are burdening end user confidence in 2024. As a result, the consumption of beer is becoming more and more oriented on controlled, value-based events instead of spontaneous social events.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Turkey Beer Market Trend

Premium experimentation within domestic beer offerings

Turkey end users are experimenting with more premium and differentiated beer styles in domestic brands despite economic pressure. According to TurkStat, the output of food and beverage manufacturing increased positively in 2024, which is an indication of the continued product development. This helps in the growth of flavour-based and specialty beer variants targeting experience-based end users.

This behaviour is in line with the larger consumption patterns. According to the OECD, middle-income end users in Turkey are increasingly demanding quality differentiation in limited budgets, as opposed to completely downgrading their decisions. Consequently, the concept of premium positioning in domestic beer portfolios becomes topical, particularly with the help of limited-edition or seasonal products.

Turkey Beer Market Opportunity

Tourism recovery strengthens on-trade consumption potential

Beer consumption in Turkey presents a structural growth opportunity, supported by the country’s sustained tourism activity and its role in driving on-trade beverage demand. According to the Ministry of Culture and Tourism of Turkey, the country received 56.7 million foreigners in 2023, which is higher than the pre-pandemic rates and contributes to the foodservice and hospitality industry. This inflow has a direct positive impact on on-trade beer consumption in urban and coastal destinations.

Moreover, the UN World Tourism Organization also confirms that Turkey is one of the top tourism destinations in the world in 2024, which supports the contribution of foreign tourists to alcohol consumption in licensed establishments. This is a conducive environment that favors both mainstream and premium beer products in on-trade environments.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Turkey Beer Market Segmentation Analysis

By Product Type

- Dark Beer

- Ale

- Sorghum Beer

- Weissbier/Weizen/Wheat Beer

- Lager

- Flavoured/Mixed Lager

- Standard Lager

- Premium Lager

- Domestic Premium Lager

- Imported Premium Lager

- Mid-Priced Lager

- Domestic Mid-Priced Lager

- Imported Mid-Priced Lager

- Economy Lager

- Domestic Economy Lager

- Imported Economy Lager

- Premium Lager

- Non/Low Alcohol Beer

- Low Alcohol Beer

- Non Alcoholic Beer

- Stout

- Others (Porter, Malt etc.)

Lager represents the dominant segment under product type classification, accounting for approximately 95% of the Turkey beer market value. Lager's dominance is driven by its broad end user acceptance, affordability, and strong presence across both domestic premium and mid-priced offerings. Local lager brands benefit from established drinking habits and a clear price advantage over imported alternatives, making them resilient during periods of economic pressure.

Over the forecast period, lager is expected to retain its leading position, supported by ongoing brand investment and incremental premiumisation within the segment. While categories such as ale and wheat beer are projected to record faster growth rates, their contribution will remain limited due to their small base. As a result, lager will continue to anchor overall beer sales and shape market performance in Turkey.

By Sales Channel

- On-Trade

- Off-Trade

Off-trade channels constitute the dominant segment under sales channel classification, holding approximately 65% of total beer sales. Off-trade growth has been driven by end users shifting towards home consumption in response to high inflation and reduced discretionary spending. Supermarkets and large retail chains have benefited the most, offering competitive pricing, wider product assortments, and greater convenience.

During the forecast period, off-trade is expected to maintain its leadership, supported by beer's affordability and expanding product variety. However, on-trade sales are projected to grow at a faster pace from 2026 onwards as economic conditions improve and tourism activity strengthens. Despite this shift, off-trade will remain the dominant channel, continuing to play a central role in Turkey's beer consumption patterns.

List of Companies Covered in Turkey Beer Market

The companies listed below are highly influential in the Turkey beer market, with a significant market share and a strong impact on industry developments.

- Karagözoglu Dis Ticaret AS

- Efes Pilsen AS

- Türk Tuborg Bira ve Malt Sanayii AS

Frequently Asked Questions

Related Report

1. Market Segmentation

1.1. Research Scope

1.2. Research Methodology

1.3. Definitions and Assumptions

2. Executive Summary

3. Turkey Beer Market Policies, Regulations, and Standards

4. Turkey Beer Market Dynamics

4.1. Growth Factors

4.2. Challenges

4.3. Trends

4.4. Opportunities

5. Turkey Beer Market Statistics, 2022-2032F

5.1. Market Size & Growth Outlook

5.1.1.By Revenues in US$ Million

5.1.2.By Quantity Sold in Million Litres

5.2. Market Segmentation & Growth Outlook

5.2.1.By Product Type

5.2.1.1. Dark Beer- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.1. Ale- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.2. Sorghum Beer- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.3. Weissbier/Weizen/Wheat Beer- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2. Lager- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.1. Flavoured/Mixed Lager- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.2. Standard Lager- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.2.1. Premium Lager- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.2.1.1. Domestic Premium Lager- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.2.1.2. Imported Premium Lager- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.2.2. Mid-Priced Lager- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.2.2.1. Domestic Mid-Priced Lager- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.2.2.2. Imported Mid-Priced Lager- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.2.3. Economy Lager- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.2.3.1. Domestic Economy Lager- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.2.3.2. Imported Economy Lager- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3. Non/Low Alcohol Beer- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3.1. Low Alcohol Beer- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3.2. Non Alcoholic Beer- Market Insights and Forecast 2022-2032, USD Million

5.2.1.4. Stout- Market Insights and Forecast 2022-2032, USD Million

5.2.1.5. Others (Porter, Malt etc.) - Market Insights and Forecast 2022-2032, USD Million

5.2.2.By Production

5.2.2.1. Macro Brewery- Market Insights and Forecast 2022-2032, USD Million

5.2.2.2. Micro Brewery- Market Insights and Forecast 2022-2032, USD Million

5.2.2.3. Craft Brewery- Market Insights and Forecast 2022-2032, USD Million

5.2.3.By Packaging Type

5.2.3.1. Bottles- Market Insights and Forecast 2022-2032, USD Million

5.2.3.2. Cans- Market Insights and Forecast 2022-2032, USD Million

5.2.3.3. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.4.By Sales Channel

5.2.4.1. On-Trade- Market Insights and Forecast 2022-2032, USD Million

5.2.4.2. Off-Trade- Market Insights and Forecast 2022-2032, USD Million

5.2.5.By Competitors

5.2.5.1. Competition Characteristics

5.2.5.2. Market Share & Analysis

6. Turkey Dark Beer Market Statistics, 2022-2032F

6.1. Market Size & Growth Outlook

6.1.1.By Revenues in US$ Million

6.1.2.By Quantity Sold in Million Litres

6.2. Market Segmentation & Growth Outlook

6.2.1.By Product Type- Market Insights and Forecast 2022-2032, USD Million

6.2.2.By Production- Market Insights and Forecast 2022-2032, USD Million

6.2.3.By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

6.2.4.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

7. Turkey Lager Beer Market Statistics, 2022-2032F

7.1. Market Size & Growth Outlook

7.1.1.By Revenues in US$ Million

7.1.2.By Quantity Sold in Million Litres

7.2. Market Segmentation & Growth Outlook

7.2.1.By Product Type- Market Insights and Forecast 2022-2032, USD Million

7.2.2.By Production- Market Insights and Forecast 2022-2032, USD Million

7.2.3.By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

7.2.4.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

8. Turkey Non/Low Alcohol Beer Market Statistics, 2022-2032F

8.1. Market Size & Growth Outlook

8.1.1.By Revenues in US$ Million

8.1.2.By Quantity Sold in Million Litres

8.2. Market Segmentation & Growth Outlook

8.2.1.By Production- Market Insights and Forecast 2022-2032, USD Million

8.2.2.By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

8.2.3.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

9. Turkey Stout Beer Market Statistics, 2022-2032F

9.1. Market Size & Growth Outlook

9.1.1.By Revenues in US$ Million

9.1.2.By Quantity Sold in Million Litres

9.2. Market Segmentation & Growth Outlook

9.2.1.By Production- Market Insights and Forecast 2022-2032, USD Million

9.2.2.By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

9.2.3.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

10. Competitive Outlook

10.1. Company Profiles

10.1.1. Efes Pilsen AS

10.1.1.1. Business Description

10.1.1.2. Product Portfolio

10.1.1.3. Collaborations & Alliances

10.1.1.4. Recent Developments

10.1.1.5. Financial Details

10.1.1.6. Others

10.1.2. Türk Tuborg Bira ve Malt Sanayii AS

10.1.2.1. Business Description

10.1.2.2. Product Portfolio

10.1.2.3. Collaborations & Alliances

10.1.2.4. Recent Developments

10.1.2.5. Financial Details

10.1.2.6. Others

10.1.3. Karagözoglu Dis Ticaret AS

10.1.3.1. Business Description

10.1.3.2. Product Portfolio

10.1.3.3. Collaborations & Alliances

10.1.3.4. Recent Developments

10.1.3.5. Financial Details

10.1.3.6. Others

11. Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Product Type |

|

| By Production |

|

| By Packaging Type |

|

| By Sales Channel |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.