Thailand Construction Equipment Market Report: Trends, Growth and Forecast (2026-2032)

By Type of Equipment (Earthmoving Equipment (Excavator, Loaders, Bulldozers, Skid Steer Loaders, Motor Graders, Crawler Loader, Trenchers, Dump Trucks, Others), Material Handling Equipment (Cranes, Forklift, Tipper, Others), Other construction equipment (Road Roller, Diesel Generator, Others)), By Propulsion (Diesel, Gas, CNG, LPG, Electric), By Application (Power & Utilities, Mining, Hospitality, Residential, Healthcare & Educational, Roads & Highway, Manufacturing Units, Others), By Engine Capacity (< 5 L, 5–10 L, 10 L), By Power Output (< 100 HP, 101–200 HP, 201–400 HP, >400 HP) ... Read more

|

Major Players

|

Thailand Construction Equipment Market Statistics and Insights, 2026

- Market Size Statistics

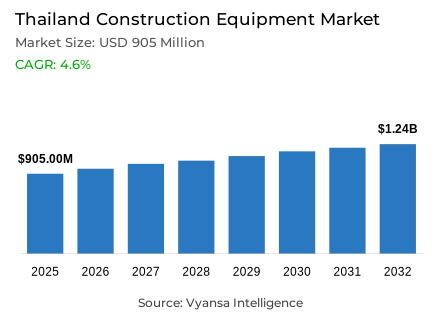

- Construction equipment market size in Thailand was valued at USD 905 million in 2025 and is estimated at USD 945 million in 2026.

- The market size is expected to grow to USD 1.24 billion by 2032.

- Market to register a CAGR of around 4.6% during 2026-32.

- Type of Equipment Shares

- Earthmoving equipment grabbed market share of 40%.

- Competition

- More than 10 companies are actively engaged in producing construction equipment in Thailand.

- Top 5 companies acquired around 45% of the market share.

- Kobelco Construction Machinery, XCMG, Zoomlion Heavy Industry, Caterpillar Inc., Komatsu Ltd. etc., are few of the top companies.

- Application

- Roads & highway grabbed 30% of the market.

Thailand Construction Equipment Market Outlook

Thailand construction equipment market was valued at USD 905 million in 2025 and is projected to advance from USD 945 million in 2026 to USD 1.24 billion by 2032, registering a CAGR of 4.6% across the forecast period. This measured and infrastructure-anchored expansion reflects a commercially stable growth environment within the Thailand construction equipment market , where continuous activity across road development, highway expansion, rail infrastructure, airport upgrades, port modernisation, and urban transport improvement is collectively sustaining consistent and broad-based machinery demand across earthmoving, road construction, lifting, and material handling equipment categories. Growth is not speculative but execution-driven, shaped by a nationally coordinated transport investment programme that converts public capital allocation into direct and phase-variable machine deployment across contractor operations throughout the country.

The scale and diversity of Thailand's transport infrastructure pipeline provide the market with a structurally dependable and multi-year demand foundation. As per data published by the Thailand Government Public Relations Department, the 2025 to 2026 transport plan encompasses 223 projects in 2025 with a budget of 136.49 billion baht and 64 projects in 2026 with investment of 116.96 billion baht, covering road, rail, water, air, and public transport asset categories that collectively generate rotating fleet requirements for excavators, loaders, motor graders, bulldozers, cranes, road rollers, asphalt pavers, and concrete equipment across sequential construction phases.

Earthmoving equipment market Thailand commands the leading share of approximately 40% within the equipment type segment, reflecting the foundational and sequentially non-negotiable role of site clearance, soil removal, foundation preparation, trenching, grading, and bulk material handling at the earliest and most capital-intensive phases of every infrastructure project category active within Thailand's development pipeline. The segment's wide application range across roadwork, rail embankments, airport land development, port preparation, and urban civil works gives it a commercial durability and project-cycle breadth that no other equipment category currently matches across the Thailand heavy equipment market.

Road and highway construction equipment applications lead the application segment at approximately 30%, anchored in Thailand's extensive national road network and active highway expansion, expressway improvement, and traffic decongestion programme that generates both new construction and recurring maintenance-linked machinery demand across the country. Together, earthmoving equipment leadership and roads and highway application dominance confirm that the Thailand construction equipment market is shaped by civil infrastructure intensity, project-phase variability, and a structural dependence on heavy machinery across land preparation, pavement, drainage, and connectivity works throughout the forecast period.

Thailand Construction Equipment Market Growth Driver

Transport Infrastructure Investment Scale and Project Diversity Are Creating Durable Multi-Category Equipment Demand

Thailand's nationally coordinated and multi-modal transport investment programme is the most commercially significant demand driver within the Thailand construction equipment market , sustaining equipment utilisation across road, rail, airport, port, and urban mobility project categories simultaneously with a project-phase consistency that benefits suppliers capable of rotating fleet combinations across successive construction stages. As per data published by the Thailand Government Public Relations Department, the 2025 to 2026 transport plan encompasses 50 road projects including the Chalong Rat Expressway extension and Bangkok Outer Ring Road, 69 rail construction machinery projects including new Red Line suburban train routes, 26 water transport projects including Laem Chabang Port Phase 3, and 37 airport projects covering capacity expansion at Chiang Mai, Phuket, and Suvarnabhumi, each generating distinct fleet requirements across earthmoving, lifting, concrete, road surfacing, and site logistics equipment categories.

Infrastructure diversity reinforces this driver by ensuring that demand is distributed across equipment types and geographies rather than concentrated in a single project category or corridor. According to statistics released by the Department of Highways, Thailand's total road network covers approximately 703,899 kilometres including 52,323 kilometres of national highways and 49,654 kilometres of rural roads, a network scale that generates continuous resurfacing, drainage repair, slope stabilisation, and pavement rehabilitation demand that sustains road construction equipment rental and procurement activity independently of new mega-project awards, providing equipment suppliers with a structurally resilient baseline demand floor throughout the forecast period.

Thailand Construction Equipment Market Challenge

Budget Constraints and Macroeconomic Pressure Are Compressing Fleet Expansion and Procurement Confidence

The most commercially consequential structural challenge within the Thailand construction machinery market is the gap between the scale of infrastructure ambition and the financing depth, execution capacity, and macroeconomic momentum required to convert large headline project pipelines into continuous and high-utilisation equipment deployment at the pace that market demand projections imply. Based on data from the World Bank, Thailand's GDP growth is expected to slow to 1.8% in 2025 and 1.7% in 2026, with risks linked to trade uncertainty, weaker exports, slowing consumption, and moderating tourism recovery, creating an environment where private construction investment, contractor confidence, and fleet expansion decisions are more cautious and payment-cycle sensitive than in higher-growth periods.

Project execution complexity compounds this macroeconomic challenge by creating structural friction between awarded project volumes and active machinery deployment. As indicated by authoritative sources at the Department of Highways, Thailand's infrastructure execution environment is shaped by the need to prioritise projects within limited budget frameworks, manage rising traffic volumes from urban expansion, strengthen work-zone safety, address disaster and climate risks, and improve environmental compliance across highway development, all of which extend project mobilisation timelines, increase contractor operating requirements, and create periods of fleet utilization risk and equipment idling that compress ownership returns and shift procurement preference toward phased fleet replacement or rental arrangements.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Thailand Construction Equipment Market Trend

Sustainable Road Construction and Reclaimed Asphalt Adoption Are Creating Specialised Equipment Demand

A well-defined and commercially consequential structural trend is reshaping machinery demand composition within the Thailand road construction equipment market , as the Department of Highways' accelerating adoption of reclaimed asphalt pavement practices progressively elevates the technical specification requirements for road construction equipment beyond conventional general-purpose machinery toward more precise, fuel-efficient, and recycling-capable specialist equipment. Evidence drawn from public data released by the Department of Highways confirms that RAP activity increased from 115 contracts in fiscal year 2024 to 152 contracts in fiscal year 2025, with output rising from 3.04 million square metres and 365,017 tons to 4.47 million square metres and 537,011 tons, directly creating stronger demand for cold milling machines, asphalt recycling systems, hot mix plant upgrades, and high-precision compactors across Thailand's national road maintenance programme.

The sustainability trend extends beyond reclaimed asphalt into digital monitoring, climate-resilient design, and greener material adoption across Thailand's highway development framework. In line with findings from the Department of Highways, IoT slope monitoring, bioengineering practices, highway disaster management systems, and machine-learning-based flood risk tools are being incorporated into project planning and maintenance operations, while hydraulic cement substitution is reducing carbon dioxide intensity from 910 kilogrammes per ton of ordinary Portland cement to 871 kilogrammes per ton, collectively elevating contractor demand for low-emission machinery, concrete batching equipment, and GPS-enabled equipment that can operate with tighter technical specifications and lower environmental impact across climate-sensitive and conservation-adjacent construction zones.

Thailand Construction Equipment Market Opportunity

PPP Infrastructure and High-Value Transport Corridors Are Creating Long-Duration Specialist Equipment Opportunities

The most commercially compelling growth opportunity within the Thailand construction equipment market lies in the public-private partnership infrastructure pipeline and high-value transport corridor programme, where large-scale civil engineering commitments, multi-year construction schedules, and diversified machinery requirements across expressway, rail, port, and airport project categories are creating sustained and high-intensity equipment demand that suppliers with specialist fleets, financing flexibility, and strong service networks are best positioned to capture. As per official figures from the Trade Commissioner Service, Thailand's revised PPP delivery plan for 2020 to 2027 encompasses 77 projects with a total value of approximately CAD 45 billion, including the Expressway Sai Kathu-Patong Phuket project valued at CAD 400 million with construction beginning in 2026, and the MRT Orange Line Bang Khun Non-Min Buri route valued at CAD 8.71 billion extending 35.9 kilometres through a dual underground and elevated transit system requiring Bangkok metro construction equipment, piling machinery, concrete batching, underground excavation support, and compact urban material handling systems.

The opportunity deepens further as transport corridor development creates second-order construction demand beyond the primary project site across industrial estates, logistics hubs, warehouses, tourism assets, and commercial developments that benefit from improved connectivity. Data compiled from internationally recognised public authorities at the Trade Commissioner Service confirms that PPP projects consistently involve multiple packages, long contract durations, and diversified machinery rotations, creating recurring demand for equipment rental, maintenance contracts, spare parts supply, telematics, operator training, and fleet management services that sustain supplier revenue streams well beyond initial equipment procurement windows throughout the multi-year Eastern Economic Corridor construction machinery and transport corridor execution environment.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Thailand Construction Equipment Market Segmentation Analysis

By Type of Equipment

- Earthmoving Equipment

- Excavator

- Loaders

- Bulldozers

- Skid Steer Loaders

- Motor Graders

- Crawler Loader

- Trenchers

- Dump Trucks

- Others

- Material Handling Equipment

- Cranes

- Forklift

- Tipper

- Others

- Other construction equipment

- Road Roller

- Diesel Generator

- Others

Earthmoving Equipment commands the highest share within the equipment type category at approximately 40%, reflecting the foundational and phase-initiating role of excavation, grading, bulk material handling, and site preparation machinery across every active infrastructure project category within the Thailand construction equipment market . Contractors across road, rail, airport, port, and urban construction projects consistently require excavators, bulldozers, loaders, motor graders, crawler loaders, trenchers, and dump trucks before any structural, pavement, or finishing equipment becomes operationally relevant, creating a structurally front-loaded demand pattern reinforced by the 2025 to 2026 transport plan's 223 projects in 2025 and 64 projects in 2026 spanning road, rail, water, and air transport categories that all commence with machinery-intensive ground preparation and civil works phases.

The segment's commercial durability is further reinforced by the network maintenance dimension of Thailand's road infrastructure, which generates recurring earthmoving machinery demand independent of new project awards. Validated reports from the Department of Highways confirm a national road network of approximately 703,899 kilometres requiring continuous widening, drainage improvement, slope stabilisation, and pavement reconstruction across national highways, rural roads, motorways, and expressways, while the shift toward sustainable road construction through reclaimed asphalt pavement practices creates additional demand for milling machines, crushers, and specialist earthmoving equipment that supports material recovery and roadbed preparation across Thailand's expanding green highway programme throughout the forecast period.

By Application

- Power & Utilities

- Mining

- Hospitality

- Residential

- Healthcare & Educational

- Roads & Highway

- Manufacturing Units

- Others

Roads and Highway commands the highest share within the application category at approximately 30%, establishing transport infrastructure construction and maintenance as the most equipment-intensive and commercially dependable end-use context within the Thailand construction equipment market . Contractors executing highway, expressway, and road corridor projects consistently generate multi-category fleet demand across sequential phases, from excavators and bulldozers during land clearance and earthworks, through motor graders, compactors, and rollers during subgrade and roadbed preparation, to road and highway construction equipment including asphalt pavers, milling machines, concrete equipment, and cranes during pavement, bridge, and interchange construction, creating a phase-variable rotation pattern that benefits suppliers capable of serving diverse machinery requirements across the full project lifecycle rather than single-phase demand windows.

The segment's structural durability is reinforced by both the scale of Thailand's road asset base and the policy commitment to sustained highway investment across new construction and maintenance cycles. Evidence drawn from public data released by the Department of Highways confirms RAP activity expanding to 152 contracts in fiscal year 2025, while the Thailand Government Public Relations Department confirms 50 road projects within the 2025 to 2026 transport plan including the Chalong Rat Expressway extension and Bangkok Outer Ring Road, collectively sustaining strong and broadly distributed Thailand earthmoving equipment market and road machinery demand that extends well beyond any single project corridor and supports the segment's position as the most consistent and highest-machinery-intensity application base throughout the forecast period.

List of Companies Covered in Thailand Construction Equipment Market

The companies listed below are highly influential in the Thailand construction equipment market, with a significant market share and a strong impact on industry developments.

- Kobelco Construction Machinery

- XCMG

- Zoomlion Heavy Industry

- Caterpillar Inc.

- Komatsu Ltd.

- SANY Heavy Industry

- Hitachi Construction Machinery

- Volvo Construction Equipment

- HD Hyundai Construction Equipment

- LiuGong Machinery

Market News & Updates

- SANY Heavy Industry, 2026:

SANY delivered SM4602T0BEV electric terminal tractors to a customer in Thailand in April 2026. The vehicles use rapid battery swapping, with swaps completed in less than 5 minutes, and carry a 282 kWh battery pack with more than 120 km range. The equipment is already operating in Thai port logistics.

- Hitachi Construction Machinery, 2026:

Hitachi Construction Machinery and Leadway Construction and Mining Machinery held the 7G Next Generation Grand Opening in Pattaya, Thailand, in January 2026. The event displayed Hitachi construction equipment and parts solutions and confirmed LCM as Hitachi Construction Machinery’s new authorized distributor in Thailand. The update strengthens local equipment access and service coverage.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- Thailand Construction Equipment Market Policies, Regulations, and Standards

- Thailand Construction Equipment Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- Thailand Construction Equipment Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Unit Sold (Thousand Units)

- Market Segmentation & Growth Outlook

- By Type of Equipment

- Earthmoving Equipment- Market Insights and Forecast 2022-2032, USD Million

- Excavator- Market Insights and Forecast 2022-2032, USD Million

- Loaders- Market Insights and Forecast 2022-2032, USD Million

- Bulldozers- Market Insights and Forecast 2022-2032, USD Million

- Skid Steer Loaders- Market Insights and Forecast 2022-2032, USD Million

- Motor Graders- Market Insights and Forecast 2022-2032, USD Million

- Crawler Loader- Market Insights and Forecast 2022-2032, USD Million

- Trenchers- Market Insights and Forecast 2022-2032, USD Million

- Dump Trucks- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- Material Handling Equipment- Market Insights and Forecast 2022-2032, USD Million

- Cranes- Market Insights and Forecast 2022-2032, USD Million

- Forklift- Market Insights and Forecast 2022-2032, USD Million

- Tipper- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- Other construction equipment- Market Insights and Forecast 2022-2032, USD Million

- Road Roller- Market Insights and Forecast 2022-2032, USD Million

- Diesel Generator- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- Earthmoving Equipment- Market Insights and Forecast 2022-2032, USD Million

- By Propulsion

- Diesel- Market Insights and Forecast 2022-2032, USD Million

- Gas- Market Insights and Forecast 2022-2032, USD Million

- CNG- Market Insights and Forecast 2022-2032, USD Million

- LPG- Market Insights and Forecast 2022-2032, USD Million

- Electric- Market Insights and Forecast 2022-2032, USD Million

- By Application

- Power & Utilities- Market Insights and Forecast 2022-2032, USD Million

- Mining- Market Insights and Forecast 2022-2032, USD Million

- Hospitality- Market Insights and Forecast 2022-2032, USD Million

- Residential- Market Insights and Forecast 2022-2032, USD Million

- Healthcare & Educational- Market Insights and Forecast 2022-2032, USD Million

- Roads & Highway- Market Insights and Forecast 2022-2032, USD Million

- Manufacturing Units- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Engine Capacity

- < 5 L- Market Insights and Forecast 2022-2032, USD Million

- 5–10 L- Market Insights and Forecast 2022-2032, USD Million

- 10 L- Market Insights and Forecast 2022-2032, USD Million

- By Power Output

- < 100 HP- Market Insights and Forecast 2022-2032, USD Million

- 101–200 HP- Market Insights and Forecast 2022-2032, USD Million

- 201–400 HP- Market Insights and Forecast 2022-2032, USD Million

- >400 HP- Market Insights and Forecast 2022-2032, USD Million

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Type of Equipment

- Market Size & Growth Outlook

- Thailand Earthmoving Equipment Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Unit Sold (Thousand Units)

- Market Segmentation & Growth Outlook

- By Propulsion- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Engine Capacity- Market Insights and Forecast 2022-2032, USD Million

- By Power Output- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Thailand Material Handling Equipment Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Unit Sold (Thousand Units)

- Market Segmentation & Growth Outlook

- By Propulsion- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Engine Capacity- Market Insights and Forecast 2022-2032, USD Million

- By Power Output- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Thailand Other Construction Equipment Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Unit Sold (Thousand Units)

- Market Segmentation & Growth Outlook

- By Propulsion- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Engine Capacity- Market Insights and Forecast 2022-2032, USD Million

- By Power Output- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Caterpillar Inc.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Komatsu Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- SANY Heavy Industry

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Hitachi Construction Machinery

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Volvo Construction Equipment

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Kobelco Construction Machinery

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- XCMG

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Zoomlion Heavy Industry

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- HD Hyundai Construction Equipment

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- LiuGong Machinery

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Caterpillar Inc.

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Type of Equipment |

|

| By Propulsion |

|

| By Application |

|

| By Engine Capacity |

|

| By Power Output |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.