Southeast Asia Construction Equipment Market Report: Trends, Growth and Forecast (2026-2032)

By Type of Equipment (Earthmoving Equipment (Excavator, Loaders, Bulldozers, Skid Steer Loaders, Motor Graders, Crawler Loader, Trenchers, Dump Trucks, Others), Material Handling Equipment (Cranes, Forklift, Tipper, Others), Other construction equipment (Road Roller, Diesel Generator, Others)), By Propulsion (Diesel, Gas, CNG, LPG, Electric), By Application (Power & Utilities, Mining, Hospitality, Residential, Healthcare & Educational, Roads & Highway, Manufacturing Units, Others), By Engine Capacity (< 5 L, 5–10 L, 10 L), By Power Output (< 100 HP, 101–200 HP, 201–400 HP, >400 HP), By Country (Singapore, Indonesia, Malaysia, Thailand, Vietnam, Philippines, Rest of Southeast Asia) ... Read more

|

Major Players

|

Southeast Asia Construction Equipment Market Statistics and Insights, 2026

- Market Size Statistics

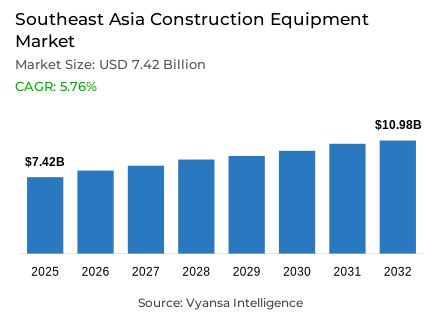

- Construction equipment market size in Southeast Asia was valued at USD 7.42 billion in 2025 and is estimated at USD 7.72 billion in 2026.

- The market size is expected to grow to USD 10.98 billion by 2032.

- Market to register a CAGR of around 5.76% during 2026-32.

- Type of Equipment Shares

- Earthmoving equipment grabbed market share of 45%.

- Competition

- More than 15 companies are actively engaged in producing construction equipment in Southeast Asia.

- Top 5 companies acquired around 40% of the market share.

- Kobelco Construction Machinery, HD Hyundai Construction Equipment, LiuGong Machinery Co. Ltd., Caterpillar Inc., Hitachi Construction Machinery Co. Ltd. etc., are few of the top companies.

- Application

- Roads & Highway grabbed 30% of the market.

- Country

- Indonesia leads with a 35% share of the Southeast Asia market.

Southeast Asia Construction Equipment Market Outlook

The Southeast Asia construction equipment market was valued at USD 7.42 billion in 2025 and is projected to advance from USD 7.72 billion in 2026 to USD 10.98 billion by 2032, registering a CAGR of 5.76% across the forecast period. This steady and structurally supported expansion reflects the durable machinery demand generated across infrastructure development, roads, highways, mining sites, utilities, manufacturing facilities, residential projects, and urban construction as the region's governments and private developers continue mobilising capital investment into physical assets that require heavy, reliable, and efficiently operated equipment throughout multi-phase project cycles. The Southeast Asia construction equipment market is not driven by speculative demand but by the practical necessity of machine-intensive project execution across one of the world's most commercially active infrastructure development corridors.

Earthmoving Equipment commands 45% of the equipment type segment, anchoring the ASEAN construction equipment market with the broadest project-phase relevance of any machinery category. Excavators, loaders, bulldozers, motor graders, crawler loaders, trenchers, and dump trucks collectively serve the land clearing, excavation, grading, trenching, soil movement, and site preparation functions that must precede every other construction activity, making this equipment category the operational foundation from which all subsequent project stages depend. Its dominance is not cyclical but structural, rooted in the sequential nature of construction project execution across the region's diverse geography.

Roads and Highway accounts for 30% of the market by application, reflecting the central role of transport infrastructure in sustaining equipment deployment across Southeast Asia's most commercially significant and machine-intensive construction category. Road and highway projects require simultaneous use of excavators for earthworks, graders for leveling, rollers for compaction, loaders for material handling, tippers for haulage, and cranes for bridge-related works, creating multi-machine fleet demand that extends across the full project cycle from ground preparation through pavement finishing and sustains equipment utilization well beyond what single-application project categories can generate.

Indonesia leads the regional market with a 35% country share, supported by population scale, island geography, mining activity, road development, urban expansion, and industrial construction requirements that collectively generate deeper and more geographically distributed equipment demand than any other national market in Southeast Asia. As per data published by the Asian Development Bank, gross fixed capital formation in Indonesia strengthened to 5.1% in 2025 from 4.6% in 2024, driven by a sharp acceleration in machinery and equipment investment, confirming that the macro conditions sustaining Indonesia construction equipment market demand are strengthening rather than moderating as the forecast period progresses.

Southeast Asia Construction Equipment Market Growth Driver

Infrastructure Investment Scale and Project Sequencing Are Creating Structurally Durable Equipment Deployment Demand

The primary commercial driver within the Southeast Asia construction equipment market is the region's large and multi-sector infrastructure investment requirement, which creates physically machine-intensive demand that cannot be satisfied without sustained deployment of earthmoving machinery, road-building equipment, material handling systems, and site-support machinery across overlapping project phases that collectively sustain fleet utilisation across months or years per major project. As per data published by the Asian Development Bank, Southeast Asia requires approximately USD 210 billion annually, equal to around 5% of regional GDP, to build new infrastructure and close development gaps, and this investment imperative translates directly into equipment demand because roads need graders, excavators, compactors, and dump trucks, ports need cranes and heavy-duty site vehicles, and power projects need trenchers, lifting systems, and site generators across every phase of execution.

Public works execution is reinforcing this driver with confirmed project mobilisation rather than pipeline forecasts alone. According to statistics released by the Asian Development Bank in its September 2025 regional assessment, Southeast Asia's investment pickup is consistent with demonstrated growth in construction and machinery investment supported by continuing public works, confirming that equipment demand is being generated by actual site mobilisation across the region rather than representing only aspirational budget allocations that may face delayed execution.

Southeast Asia Construction Equipment Market Challenge

Fuel Cost Volatility and Project Execution Delays Are Compressing Contractor Margins and Fleet Utilisation Returns

The most commercially consequential structural challenge within the ASEAN heavy equipment market is the combined pressure of fuel cost volatility, financing constraints, and project execution delays that collectively compress contractor margins, weaken new equipment purchase decisions, and create uneven fleet utilisation across the region's diverse national markets. Based on data from the World Bank's 2026 East Asia and Pacific update, regional growth is projected to slow from 5.0% in 2025 to 4.2% in 2026 due to energy shocks, trade barriers, policy uncertainty, and domestic economic pressures, creating a more demanding operating environment for fleet owners, rental providers, and OEM distributors whose commercial performance depends on consistent project cash flow, predictable fuel costs, and reliable public infrastructure budget execution.

Project execution delays compound this challenge by creating a disconnect between pipeline visibility and actual equipment deployment. Land clearance obligations, environmental approvals, tendering processes, right-of-way acquisitions, and contractor mobilisation requirements must all be sequenced before excavators, dump trucks, graders, and rollers can begin productive work, and delays at any stage create idle capacity that imposes holding costs on fleet owners without generating offsetting utilisation revenue. The World Bank's analysis confirming that a sustained 50% increase in fuel prices could reduce household incomes by 3% to 4% across East Asia and Pacific further signals that energy cost exposure creates demand-side risk alongside the direct operating cost pressure that makes fuel price volatility one of the most significant near-term constraints on Southeast Asia construction equipment market performance.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Southeast Asia Construction Equipment Market Trend

Connected, Fuel-Efficient, and Lower-Emission Equipment Is Reshaping Procurement Priorities Across the Southeast Asia construction equipment Market

A well-defined and commercially consequential structural trend is reshaping contractor procurement behaviour across the Southeast Asia construction equipment Market, as buyers increasingly evaluate machines on telematics visibility, fuel efficiency, total cost of ownership, and uptime performance rather than on purchase price and engine power alone. Evidence drawn from public data released by the Asian Development Bank confirms that the organisation announced a USD 70 billion investment push in 2026 to connect Asia's power grids and digital networks by 2035, including USD 50 billion for the Pan-Asia Power Grid Initiative and USD 20 billion for the Asia-Pacific Digital Highway, creating sustained demand for smart construction machinery in grid works, fiber routes, data infrastructure corridors, substation construction, and utility access roads that require telematics-enabled fleets capable of operating efficiently across both conventional civil sites and specialised infrastructure environments.

The competitive implications of this trend are extending beyond product specifications into after-sales capability positioning. Suppliers offering only machines without service contracts, digital monitoring, operator training, parts assurance, and uptime guarantees are progressively losing ground to providers that bundle telematics-enabled equipment with fleet analytics, preventive maintenance, and performance documentation, transforming after-sales capability into a primary competitive differentiator across fragmented Southeast Asian markets where project sites span islands, industrial zones, border corridors, and urban centres simultaneously.

Southeast Asia Construction Equipment Market Opportunity

Industrial FDI Momentum and Climate-Resilient Infrastructure Are Opening Multi-Category Equipment Demand Windows

The most commercially significant and structurally durable growth opportunity within the Southeast Asia heavy equipment market lies in the convergence of industrial foreign direct investment momentum and climate-resilient infrastructure development, both of which generate multi-machine, multi-phase equipment demand that benefits OEMs, rental providers, and after-sales service organisations simultaneously. As per official figures from UNCTAD's ASEAN Investment Report 2025, FDI inflows into ASEAN rose 8% to USD 226 billion in 2024 while global FDI declined 11%, with manufacturing FDI specifically growing nearly 150% to USD 44 billion driven by supply-chain-intensive industries and the digital economy, confirming that the investment-led construction pipeline supporting infrastructure machinery demand across industrial parks, logistics corridors, warehouses, substations, and worker facilities is expanding at an exceptional pace relative to broader global investment trends.

The climate-resilient infrastructure dimension of this opportunity adds a geographically dispersed and phase-based demand layer that is particularly well-suited to rental fleet strategies. Flood-control systems, coastal resilience works, urban drainage networks, and resilient road programmes require excavation, trenching, grading, compaction, lifting, and material transport across multiple sites and execution phases, creating recurring equipment deployment cycles that favour flexible rental access over outright ownership and position well-capitalised rental providers with maintained fleets, fast service response, and attachment availability as strategically advantaged partners for contractors executing climate-linked infrastructure across Indonesia, Vietnam, Thailand, Malaysia, the Philippines, and Singapore.

Southeast Asia Construction Equipment Market Country Analysis

By Country

- Singapore

- Indonesia

- Malaysia

- Thailand

- Vietnam

- Philippines

- Rest of Southeast Asia

Indonesia commands the most commercially influential position within the Southeast Asia construction equipment market with a 35% country share, a concentration that reflects the nation's unique combination of population scale, island geography, mining activity, industrial expansion, and public infrastructure requirements that distribute equipment demand across a wider range of project types, site locations, and operational contexts than any other Southeast Asian national market. As per data published by the Asian Development Bank, Indonesia's economy is projected to grow 5.2% in both 2026 and 2027 supported by improving investment and stable consumption, while gross fixed capital formation strengthened to 5.1% in 2025 driven by accelerated machinery and equipment investment, confirming that the macroeconomic conditions sustaining Indonesia construction equipment market demand are structurally positive and commercially well-founded rather than dependent on single-project or single-sector concentration.

The broader Southeast Asia regional demand structure reinforces Indonesia's leadership while confirming that the market's commercial depth extends across multiple high-growth national economies. Vietnam generates significant demand through industrial parks, road infrastructure, and logistics corridor development; Thailand and Malaysia contribute through manufacturing, logistics hubs, and energy projects; the Philippines requires machinery for transport, utilities, and urban resilience; and Singapore generates specialised demand for compact urban infrastructure, port works, and facility redevelopment. The Asian Development Bank's commitment of USD 6.2 billion in Southeast Asia in 2024, including USD 4.8 billion in sovereign financing and USD 1.4 billion in non-sovereign investments, confirms the institutional capital flows supporting infrastructure equipment demand across the region's diverse national markets and sustaining the Southeast Asia construction equipment Market's stable growth trajectory through 2032.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Southeast Asia Construction Equipment Market Segmentation Analysis

By Type of Equipment

- Earthmoving Equipment

- Excavator

- Loaders

- Bulldozers

- Skid Steer Loaders

- Motor Graders

- Crawler Loader

- Trenchers

- Dump Trucks

- Others

- Material Handling Equipment

- Cranes

- Forklift

- Tipper

- Others

- Other construction equipment

- Road Roller

- Diesel Generator

- Others

Earthmoving Equipment commands the highest share within the equipment type category at 45%, reflecting the structural necessity of excavation, grading, trenching, soil movement, and material handling at the earliest and most capital-intensive phase of every major construction, infrastructure, mining, industrial, and road project across the Southeast Asia construction equipment Market. Excavators serve foundations, drainage, utility lines, road cuts, and mining-linked works simultaneously; loaders move aggregates and construction materials across project sites; bulldozers reshape land during early civil works; motor graders support road leveling for highways and industrial estate roads; and dump trucks provide the haulage link between excavation, material supply, and disposal, collectively creating a product family whose combined relevance across multiple project phases sustains the segment's commercial leadership within the regional market through the forecast period.

Its dominance is further reinforced by the rental model dynamics that characterise construction equipment access across Southeast Asia, where contractors adjust machine count, attachment type, and usage duration based on project stage rather than maintaining owned fleets that generate idle capacity during the transitions between earthworks, structural work, and finishing phases. Rental providers with well-maintained earthmoving fleets, spare-parts access, mobile service teams, and compact construction equipment for urban and tight-access sites are positioned to capture consistent fleet rotation revenue as the region's infrastructure, industrial, and climate-resilience project pipeline sustains continuous but phase-variable earthmoving demand throughout the forecast period.

By Application

- Power & Utilities

- Mining

- Hospitality

- Residential

- Healthcare & Educational

- Roads & Highway

- Manufacturing Units

- Others

Roads and Highway commands the highest share within the application category at 30%, establishing transport infrastructure construction as the most machine-intensive, phase-persistent, and commercially resilient application context within the Southeast Asia construction equipment Market. Road projects generate fleet demand that rotates through multiple machine categories across the full project cycle, with excavators and bulldozers serving early earth cuts and drainage, graders and compactors serving roadbed preparation and pavement layers, road rollers and water tankers ensuring surface quality and durability, and cranes supporting bridge beams, culverts, and elevated interchange sections, creating a multi-machine deployment pattern that sustains equipment utilisation well beyond the initial site mobilisation phase. Its 30% application share reflects this equipment intensity rather than simply the volume of road contracts awarded.

The segment's commercial durability is further supported by the indirectly linked demand it generates from manufacturing, trade, and urbanisation investment. When industrial parks are developed, road access becomes a prerequisite; when ports expand, cargo routes must be improved; and when cities grow, urban road networks require widening and maintenance that sustains contractor demand for road construction machinery across both greenfield and rehabilitation project categories. This structural linkage between road infrastructure and nearly every other economic development activity confirms that Roads and Highway will remain the most commercially significant and repeat-demand-generating application segment within the Southeast Asia construction equipment market throughout the forecast period.

Various Market Players in Southeast Asia Construction Equipment Market

The companies mentioned below are highly active in the Southeast Asia construction equipment market, occupying a considerable portion of the market and shaping industry progress.

- Kobelco Construction Machinery

- HD Hyundai Construction Equipment

- LiuGong Machinery Co. Ltd.

- Caterpillar Inc.

- Hitachi Construction Machinery Co. Ltd.

- SANY Heavy Industry Co. Ltd.

- XCMG (Xuzhou Construction Machinery Group)

- Volvo Construction Equipment

- Liebherr Group

- Mitsubishi Corporation

- CNH Industrial N.V. (Case Construction)

- Sumitomo Construction Machinery

Market News & Updates

- Hitachi Construction Machinery, 2026:

Hitachi Construction Machinery established the WIXIM brand for emerging markets in April 2026, with rollout planned first in Southeast Asia. The brand offers region-specific OEM products and expands the company’s lineup beyond hydraulic excavators, dump trucks, and wheel loaders through partner products. The update adds more product choices and after-sales coverage for Southeast Asian dealers and customers.

- Hitachi Construction Machinery, 2025:

Hitachi Construction Machinery Asia and Pacific launched the ZX550LC-7G, a new 50-ton class hydraulic excavator for Southeast Asia, in September 2025. The machine was unveiled at Mining Indonesia 2025 in Jakarta and combines the ZAXIS490-7G upper structure with a 60-ton undercarriage. The launch expands heavy construction and mining equipment availability across Southeast Asia.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- Southeast Asia Construction Equipment Market Policies, Regulations, and Standards

- Southeast Asia Construction Equipment Pricing Analysis 2022-2032

- Southeast Asia Construction Equipment Pricing Trend (USD/ Equipment) 2022-2032

- Southeast Asia Construction Equipment Trend (USD/Equipment) By Country 2022-2032

- Singapore

- Indonesia

- Malaysia

- Thailand

- Vietnam

- Philippines

- Southeast Asia Feed Probiotics Pricing Trend (USD/ Equipment) By Type of Equipment 2022-2032

- Excavator

- Loaders

- Bulldozers

- kid Steer Loaders

- Motor Graders

- Crawler Loader

- Dump Trucks

- Cranes

- Forklift

- Tipper

- Road Roller

- Diesel Generator

- Southeast Asia Construction Equipment Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- Southeast Asia Construction Equipment Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Unit Sold (Thousand Units)

- Market Segmentation & Growth Outlook

- By Type of Equipment

- Earthmoving Equipment- Market Insights and Forecast 2022-2032, USD Million

- Excavator- Market Insights and Forecast 2022-2032, USD Million

- Loaders- Market Insights and Forecast 2022-2032, USD Million

- Bulldozers- Market Insights and Forecast 2022-2032, USD Million

- Skid Steer Loaders- Market Insights and Forecast 2022-2032, USD Million

- Motor Graders- Market Insights and Forecast 2022-2032, USD Million

- Crawler Loader- Market Insights and Forecast 2022-2032, USD Million

- Trenchers- Market Insights and Forecast 2022-2032, USD Million

- Dump Trucks- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- Material Handling Equipment- Market Insights and Forecast 2022-2032, USD Million

- Cranes- Market Insights and Forecast 2022-2032, USD Million

- Forklift- Market Insights and Forecast 2022-2032, USD Million

- Tipper- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- Other construction equipment- Market Insights and Forecast 2022-2032, USD Million

- Road Roller- Market Insights and Forecast 2022-2032, USD Million

- Diesel Generator- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- Earthmoving Equipment- Market Insights and Forecast 2022-2032, USD Million

- By Propulsion

- Diesel- Market Insights and Forecast 2022-2032, USD Million

- Gas- Market Insights and Forecast 2022-2032, USD Million

- CNG- Market Insights and Forecast 2022-2032, USD Million

- LPG- Market Insights and Forecast 2022-2032, USD Million

- Electric- Market Insights and Forecast 2022-2032, USD Million

- By Application

- Power & Utilities- Market Insights and Forecast 2022-2032, USD Million

- Mining- Market Insights and Forecast 2022-2032, USD Million

- Hospitality- Market Insights and Forecast 2022-2032, USD Million

- Residential- Market Insights and Forecast 2022-2032, USD Million

- Healthcare & Educational- Market Insights and Forecast 2022-2032, USD Million

- Roads & Highway- Market Insights and Forecast 2022-2032, USD Million

- Manufacturing Units- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Engine Capacity

- < 5 L- Market Insights and Forecast 2022-2032, USD Million

- 5–10 L- Market Insights and Forecast 2022-2032, USD Million

- 10 L- Market Insights and Forecast 2022-2032, USD Million

- By Power Output

- < 100 HP- Market Insights and Forecast 2022-2032, USD Million

- 101–200 HP- Market Insights and Forecast 2022-2032, USD Million

- 201–400 HP- Market Insights and Forecast 2022-2032, USD Million

- >400 HP- Market Insights and Forecast 2022-2032, USD Million

- By Country

- Singapore

- Indonesia

- Malaysia

- Thailand

- Vietnam

- Philippines

- Rest of Southeast Asia

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Type of Equipment

- Market Size & Growth Outlook

- Singapore Construction Equipment Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Unit Sold (Thousand Units)

- Market Segmentation & Growth Outlook

- By Type of Equipment- Market Insights and Forecast 2022-2032, USD Million

- By Propulsion- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Engine Capacity- Market Insights and Forecast 2022-2032, USD Million

- By Power Output- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Indonesia Construction Equipment Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Unit Sold (Thousand Units)

- Market Segmentation & Growth Outlook

- By Type of Equipment- Market Insights and Forecast 2022-2032, USD Million

- By Propulsion- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Engine Capacity- Market Insights and Forecast 2022-2032, USD Million

- By Power Output- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Malaysia Construction Equipment Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Unit Sold (Thousand Units)

- Market Segmentation & Growth Outlook

- By Type of Equipment- Market Insights and Forecast 2022-2032, USD Million

- By Propulsion- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Engine Capacity- Market Insights and Forecast 2022-2032, USD Million

- By Power Output- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Thailand Construction Equipment Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Unit Sold (Thousand Units)

- Market Segmentation & Growth Outlook

- By Type of Equipment- Market Insights and Forecast 2022-2032, USD Million

- By Propulsion- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Engine Capacity- Market Insights and Forecast 2022-2032, USD Million

- By Power Output- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Vietnam Construction Equipment Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Unit Sold (Thousand Units)

- Market Segmentation & Growth Outlook

- By Type of Equipment- Market Insights and Forecast 2022-2032, USD Million

- By Propulsion- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Engine Capacity- Market Insights and Forecast 2022-2032, USD Million

- By Power Output- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Philippines Construction Equipment Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Unit Sold (Thousand Units)

- Market Segmentation & Growth Outlook

- By Type of Equipment- Market Insights and Forecast 2022-2032, USD Million

- By Propulsion- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Engine Capacity- Market Insights and Forecast 2022-2032, USD Million

- By Power Output- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Komatsu Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Caterpillar Inc.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Hitachi Construction Machinery Co. Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- SANY Heavy Industry Co. Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- XCMG (Xuzhou Construction Machinery Group)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Volvo construction equipment

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Kobelco Construction Machinery

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- HD Hyundai construction equipment

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- LiuGong Machinery Co. Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Liebherr Group

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Mitsubishi Corporation

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- CNH Industrial N.V. (Case Construction)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Komatsu Ltd.

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Type of Equipment |

|

| By Propulsion |

|

| By Application |

|

| By Engine Capacity |

|

| By Power Output |

|

| By Country |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.