Singapore Construction Equipment Market Report: Trends, Growth and Forecast (2026-2032)

By Type of Equipment (Earthmoving Equipment (Excavator, Loaders, Bulldozers, Skid Steer Loaders, Motor Graders, Crawler Loader, Trenchers, Dump Trucks, Others), Material Handling Equipment (Cranes, Forklift, Tipper, Others), Other construction equipment (Road Roller, Diesel Generator, Others)), By Propulsion (Diesel, Gas, CNG, LPG, Electric), By Application (Power & Utilities, Mining, Hospitality, Residential, Healthcare & Educational, Roads & Highway, Manufacturing Units, Others), By Engine Capacity (< 5 L, 5–10 L, 10 L), By Power Output (< 100 HP, 101–200 HP, 201–400 HP, >400 HP) ... Read more

|

Major Players

|

Singapore Construction Equipment Market Statistics and Insights, 2026

- Market Size Statistics

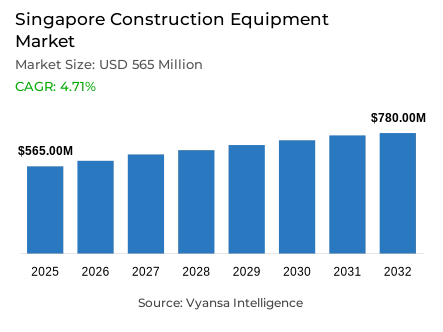

- Construction equipment market size in Singapore was valued at USD 565 million in 2025 and is estimated at USD 590 million in 2026.

- The market size is expected to grow to USD 780 million by 2032.

- Market to register a CAGR of around 4.71% during 2026-32.

- Type of Equipment Shares

- Material handling equipment grabbed market share of 40%.

- Competition

- More than 15 companies are actively engaged in producing construction equipment in Singapore.

- Top 5 companies acquired around 45% of the market share.

- Liebherr Group, JCB, SANY Group, Caterpillar Inc., Komatsu Ltd. etc., are few of the top companies.

- Application

- Residential grabbed 30% of the market.

Singapore Construction Equipment Market Outlook

Singapore construction equipment market was valued at USD 565 million in 2025 and is projected to advance from USD 590 million in 2026 to USD 780 million by 2032, registering a CAGR of 4.71% across the forecast period. This measured and structurally supported expansion reflects a commercially resilient growth environment within the Singapore construction equipment market, where continuous residential development, institutional infrastructure delivery, commercial redevelopment, and urban renewal are collectively sustaining consistent equipment demand across lifting, material movement, temporary power, and site support categories. Growth is anchored not in speculative procurement but in the phased execution requirements of a project pipeline that rewards equipment efficiency, mechanised site coordination, and productivity-led machinery adoption over manual-intensive construction approaches.

Singapore's compact and regulation-intensive built environment shapes both the composition and commercial logic of equipment demand across the market. As per data published by the Building and Construction Authority, medium-term construction demand is projected to average SGD 39 billion to SGD 46 billion per year from 2027 to 2030, supported by Changi Terminal 5 construction, HDB Build-To-Order housing delivery, redevelopment of the National University Hospital at Kent Ridge, various Junior Colleges, and the new Singapore University of Social Sciences City Campus, each generating distinct and phase-variable heavy machinery market Singapore requirements across earthmoving, lifting, logistics, and finishing equipment categories.

Material handling equipment Singapore commands the highest share within the equipment type segment at approximately 40%, reflecting the logistics-intensive and vertically complex character of Singapore's high-rise construction environment where safe and efficient movement of steel, concrete components, prefabricated parts, MEP systems, and finishing materials across constrained multi-contractor sites is as operationally critical as structural execution itself. The segment's wider usage cycle across structural, MEP, façade, and finishing project phases gives it a commercial durability that early-stage-only equipment categories cannot match across Singapore's multi-phase project environment.

Residential applications lead the application segment at approximately 30%, anchored in Singapore's policy-backed public housing delivery programme that generates recurring and multi-stage HDB construction equipment demand across site preparation, structural works, vertical lifting, utility installation, and interior finishing phases simultaneously across multiple concurrent estates. Together, material handling equipment leadership and residential application dominance confirm that the Singapore construction equipment market is shaped by high-frequency, productivity-driven, and safety-conscious equipment needs that favour modern, well-maintained, and operator-supported machinery throughout the forecast period.

Singapore Construction Equipment Market Growth Driver

Public-Sector Pipeline Continuity and Productivity Pressure Are Creating Durable Multi-Year Equipment Demand

Singapore's institutionally coordinated and multi-sector construction pipeline is the most commercially significant demand driver within the Singapore construction equipment Market, sustaining equipment procurement and fleet deployment across residential, transport, healthcare, education, and commercial project categories with a project-phase consistency that benefits suppliers capable of serving changing machinery requirements across successive construction stages. As per data published by BCA, medium-term construction demand is projected to average SGD 39 billion to SGD 46 billion annually from 2027 to 2030, with Changi T5 construction equipment, HDB BTO housing, hospital redevelopment, and university campus construction all contributing to a diversified and multi-year demand base that gives equipment suppliers forward visibility well beyond individual contract awards.

Productivity pressure reinforces this driver by elevating the functional value of machinery investment across contractor decision-making. According to statistics released by the Ministry of Manpower, construction employment reached 566,800 in December 2025 with non-resident workers accounting for 443,700, confirming that the sector remains highly labour-dependent even as project complexity rises, making manpower-saving machinery and productivity-enhancing equipment increasingly central to contractor competitiveness. As Singapore continues advancing long-duration infrastructure and housing programmes, suppliers with reliable fleets, strong maintenance networks, operator support capabilities, and modern handling systems are structurally better positioned to capture sustained procurement demand throughout the forecast period.

Singapore Construction Equipment Market Challenge

Labour Dependency and Safety Compliance Obligations Are Elevating Equipment Performance Expectations

The most commercially consequential structural challenge within the Singapore heavy equipment market is the sector's persistent reliance on trained operators, certified lifting teams, safety supervisors, and maintenance-qualified personnel whose availability directly determines whether deployed equipment can deliver full productive value on space-constrained and schedule-intensive urban construction sites. Based on data from the Ministry of Manpower, total employment grew by 55,500 in 2025 with non-resident employment excluding migrant domestic workers rising by 43,900, driven by continued Work Permit hiring in construction, confirming that machinery deployment capacity remains structurally linked to workforce policy, levy costs, safety training cycles, and operator mobilisation timelines that rental and procurement planning must accommodate.

Safety compliance expectations compound this operational challenge by raising the minimum performance standard that equipment must meet before contractors will commit to procurement or extended deployment arrangements. As indicated by authoritative sources at the Ministry of Manpower, Singapore's overall workplace fatal injury rate fell to a record low of 0.96 per 100,000 workers in 2025, while the construction sector's major injury rate declined to 26.3 per 100,000 workers, improvements that raise the baseline expectation for telematics-enabled construction equipment, certified inspection records, preventive maintenance documentation, and operator-assist functionality across every machinery category deployed on active Singapore construction sites throughout the forecast period.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Singapore Construction Equipment Market Trend

Robotics Adoption and Smart Equipment Integration Are Redefining Productivity Standards Across the Market

A well-defined and commercially consequential structural trend is reshaping equipment demand composition within the Singapore construction machinery market, as BCA's formal built-environment productivity strategy progressively shifts contractor preferences from standard machine supply toward advanced, automation-integrated, and digitally documented equipment arrangements that deliver measurable labour savings, safety improvements, and schedule acceleration across high-density urban project sites. Evidence drawn from public data released by BCA confirms that more than 20 ready-to-deploy robotic construction equipment Singapore solutions are available across structural, architectural, mechanical, electrical, and plumbing trades, with more than 50 deployed projects and 40 early adopters confirmed, signalling that automated construction machinery is moving from pilot activity into commercially normalised site practice across Singapore's built environment.

The public funding architecture reinforcing this trend provides institutional depth and durable commercial momentum for equipment suppliers capable of offering productivity-differentiated products. In line with findings from BCA, the enhanced Productivity Solutions Grant for the Built Environment, open from April 2026 to March 2031, co-funds up to 50% of qualifying costs for local SMEs with caps of SGD 300,000 per firm for pre-approved advanced equipment and SGD 50,000 per firm for smart construction machinery and digital solutions, creating a structured incentive environment that rewards suppliers bundling machinery access with telematics integration, operator training, maintenance records, and deployment support rather than offering standard equipment on price alone.

Singapore Construction Equipment Market Opportunity

HDB Housing Volume and Urban Redevelopment Are Creating Broad and Recurring Equipment Demand Pools

The most commercially significant and structurally dependable growth opportunity within the Singapore construction equipment market lies in the public housing delivery and urban redevelopment pipeline, where HDB's sustained programme creates multi-stage, geographically distributed, and continuously replenished equipment demand that suppliers with diversified and productivity-aligned fleets are best positioned to serve. As per official figures from HDB, approximately 19,600 BTO flats are planned for launch in 2026 within a 55,000-flat supply commitment for 2025 to 2027, with the February 2026 exercise alone delivering 9,012 units across six projects, confirming that the residential construction machinery base generating recurring crane, hoist, forklift, compact loader, generator, and material handling equipment demand is both substantial and continuously renewed across multiple concurrent estate construction programmes.

Urban redevelopment extends this opportunity beyond new housing supply into a separately significant demand layer characterised by tighter access constraints, noise-sensitive environments, and stricter community impact requirements that structurally favour compact construction equipment Singapore suppliers offering low-noise, space-efficient, telematics-monitored, and safety-compliant machinery. Data compiled from internationally recognised public authorities at BCA confirms that the urban redevelopment machinery demand environment rewards suppliers offering compact designs, certified operator-assist functions, clean temporary power systems, and smart material handling solutions that can operate efficiently within the constrained footprint and strict scheduling requirements of Singapore's dense and continuously evolving built environment throughout the forecast period.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Singapore Construction Equipment Market Segmentation Analysis

By Type of Equipment

- Earthmoving Equipment

- Excavator

- Loaders

- Bulldozers

- Skid Steer Loaders

- Motor Graders

- Crawler Loader

- Trenchers

- Dump Trucks

- Others

- Material Handling Equipment

- Cranes

- Forklift

- Tipper

- Others

- Other construction equipment

- Road Roller

- Diesel Generator

- Others

Material Handling Equipment commands the highest share within the equipment type category at approximately 40%, reflecting the logistics-intensive, vertically complex, and space-constrained character of Singapore's urban construction environment that makes organised and efficient material movement as operationally critical as structural execution itself within the Singapore construction equipment Market. Contractors across HDB construction machinery, transport, healthcare, and institutional project types consistently require cranes, forklifts, hoists, tippers, lifting platforms, and compact material transporters for the repeated movement of prefabricated elements, steel, MEP systems, façade components, and finishing materials across sequential project phases, creating a demand pattern with a wider usage cycle than early-stage-only equipment categories and sustaining the segment's commercial leadership across the full project lifecycle.

The segment's relevance is deepening as Singapore's productivity agenda elevates quality and capability expectations within the material handling category. BCA's identification of smart fleet management hoists and material transporters among its ready-to-deploy robotics and automation solutions confirms that this segment is evolving from basic fleet provision toward smarter, safer, and more productivity-documented equipment that suppliers can differentiate through telematics integration, load-tracking systems, digital maintenance records, and operator support programmes, making material handling equipment the most commercially dynamic and technologically advancing product category within the Singapore construction equipment market throughout the forecast period.

By Application

- Power & Utilities

- Mining

- Hospitality

- Residential

- Healthcare & Educational

- Roads & Highway

- Manufacturing Units

- Others

Residential commands the highest share within the application category at approximately 30%, establishing Singapore's public housing construction programme as the most commercially dependable, broad-based, and multi-stage demand context within the Singapore construction equipment Market. Contractors executing HDB BTO housing demand and estate renewal projects generate equipment requirements across every project phase, from compact earthmoving machines and generators during site preparation, through cranes, hoists, and tippers during structural works, to forklifts, material transporters, airport construction equipment class access platforms, and temporary power systems during MEP, façade, and interior finishing stages, creating a phase-variable fleet demand pattern that favours suppliers capable of serving successive machinery needs within the same project rather than single-phase equipment providers.

The segment's structural durability is reinforced by both the depth of Singapore's housing delivery commitment and the productivity-driven equipment preference shift that is elevating machinery performance expectations across residential contractors. Validated reports from HDB confirm the 55,000-flat supply commitment for 2025 to 2027, while BCA's medium-term construction demand projections averaging SGD 39 billion to SGD 46 billion annually from 2027 to 2030 confirm that the residential and institutional project base sustaining equipment demand is both policy-anchored and multi-year in duration, creating a commercially stable and continuously replenished demand foundation for well-positioned equipment suppliers throughout the forecast period.

List of Companies Covered in Singapore Construction Equipment Market

The companies listed below are highly influential in the Singapore construction equipment market, with a significant market share and a strong impact on industry developments.

- Liebherr Group

- JCB

- SANY Group

- Caterpillar Inc.

- Komatsu Ltd.

- Hitachi Construction Machinery Co., Ltd.

- Kobelco Construction Machinery Co., Ltd.

- Volvo Construction Equipment

- XCMG Group

- CASE Construction Equipment

Market News & Updates

- Hitachi Construction Machinery, 2025:

Hitachi Construction Machinery Asia and Pacific delivered its first electric excavator in Singapore in 2025. The ZX55U-6EB compact electric hydraulic excavator began operations on 2 May 2025 under rental by Quek & Quek Civil Engineering at a Tengah jobsite. The machine adds a zero-exhaust, lower-noise option for Singapore’s urban construction worksites.

- Caterpillar Inc./Tractors Singapore Limited, 2026:

Tractors Singapore published enhanced Cat ECS 100 and Cat ECS 200 generator controller features in April 2026. The update includes advanced overcurrent protection, arc-flash maintenance mode, programmable logic, real-time clock, maintenance tracking, event logging, generator scheduling, and HMI web-server access. The features support generator monitoring and control for Singapore construction and power applications.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- Singapore Construction Equipment Market Policies, Regulations, and Standards

- Singapore Construction Equipment Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- Singapore Construction Equipment Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Unit Sold (Thousand Units)

- Market Segmentation & Growth Outlook

- By Type of Equipment

- Earthmoving Equipment- Market Insights and Forecast 2022-2032, USD Million

- Excavator- Market Insights and Forecast 2022-2032, USD Million

- Loaders- Market Insights and Forecast 2022-2032, USD Million

- Bulldozers- Market Insights and Forecast 2022-2032, USD Million

- Skid Steer Loaders- Market Insights and Forecast 2022-2032, USD Million

- Motor Graders- Market Insights and Forecast 2022-2032, USD Million

- Crawler Loader- Market Insights and Forecast 2022-2032, USD Million

- Trenchers- Market Insights and Forecast 2022-2032, USD Million

- Dump Trucks- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- Material Handling Equipment- Market Insights and Forecast 2022-2032, USD Million

- Cranes- Market Insights and Forecast 2022-2032, USD Million

- Forklift- Market Insights and Forecast 2022-2032, USD Million

- Tipper- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- Other construction equipment- Market Insights and Forecast 2022-2032, USD Million

- Road Roller- Market Insights and Forecast 2022-2032, USD Million

- Diesel Generator- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- Earthmoving Equipment- Market Insights and Forecast 2022-2032, USD Million

- By Propulsion

- Diesel- Market Insights and Forecast 2022-2032, USD Million

- Gas- Market Insights and Forecast 2022-2032, USD Million

- CNG- Market Insights and Forecast 2022-2032, USD Million

- LPG- Market Insights and Forecast 2022-2032, USD Million

- Electric- Market Insights and Forecast 2022-2032, USD Million

- By Application

- Power & Utilities- Market Insights and Forecast 2022-2032, USD Million

- Mining- Market Insights and Forecast 2022-2032, USD Million

- Hospitality- Market Insights and Forecast 2022-2032, USD Million

- Residential- Market Insights and Forecast 2022-2032, USD Million

- Healthcare & Educational- Market Insights and Forecast 2022-2032, USD Million

- Roads & Highway- Market Insights and Forecast 2022-2032, USD Million

- Manufacturing Units- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Engine Capacity

- < 5 L- Market Insights and Forecast 2022-2032, USD Million

- 5–10 L- Market Insights and Forecast 2022-2032, USD Million

- 10 L- Market Insights and Forecast 2022-2032, USD Million

- By Power Output

- < 100 HP- Market Insights and Forecast 2022-2032, USD Million

- 101–200 HP- Market Insights and Forecast 2022-2032, USD Million

- 201–400 HP- Market Insights and Forecast 2022-2032, USD Million

- >400 HP- Market Insights and Forecast 2022-2032, USD Million

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Type of Equipment

- Market Size & Growth Outlook

- Singapore Earthmoving Equipment Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Unit Sold (Thousand Units)

- Market Segmentation & Growth Outlook

- By Propulsion- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Engine Capacity- Market Insights and Forecast 2022-2032, USD Million

- By Power Output- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Singapore Material Handling Equipment Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Unit Sold (Thousand Units)

- Market Segmentation & Growth Outlook

- By Propulsion- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Engine Capacity- Market Insights and Forecast 2022-2032, USD Million

- By Power Output- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Singapore Other Construction Equipment Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Unit Sold (Thousand Units)

- Market Segmentation & Growth Outlook

- By Propulsion- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Engine Capacity- Market Insights and Forecast 2022-2032, USD Million

- By Power Output- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Caterpillar Inc.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Komatsu Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Hitachi Construction Machinery Co., Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Kobelco Construction Machinery Co., Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Volvo Construction Equipment

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Liebherr Group

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- JCB

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- SANY Group

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- XCMG Group

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- CASE Construction Equipment

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Caterpillar Inc.

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Type of Equipment |

|

| By Propulsion |

|

| By Application |

|

| By Engine Capacity |

|

| By Power Output |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.