Thailand Childrenswear Market Report: Trends, Growth and Forecast (2026-2032)

Product Type (Apparel (Baby and Toddler Wear, Boys Apparel, Girls Apparel), Footwear (Boys Footwear, Girls Footwear), Accessories (Boys Accessories, Girls Accessories), Others), Age Group (Infant/Toddler (Below 2 years), Kids/Children (2 - 14 years)), Price Category (Mass, Premium), Sales Channel (Retail Offline, Retail Online) ... Read more

|

Major Players

|

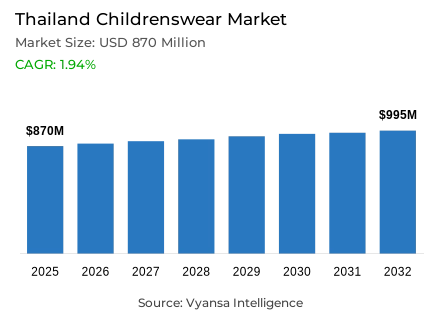

Thailand Childrenswear Market Statistics and Insights, 2026

- Market Size Statistics

- Childrenswear in Thailand is estimated at USD 870 million.

- The market size is expected to grow to USD 995 million by 2032.

- Market to register a cagr of around 1.94% during 2026-32.

- Product Type Shares

- Apparel grabbed market share of 70%.

- Competition

- More than 15 companies are actively engaged in producing childrenswear in Thailand.

- Top 5 companies acquired around 10% of the market share.

- Thai Wacoal PCL; Jaspal Co Ltd; H&M Hennes & Mauritz AB; Central Group; ICC International PCL etc., are few of the top companies.

- Sales Channel

- Retail offline grabbed 85% of the market.

Thailand Childrenswear Market Outlook

The Thailand childrenswear market was valued at approximately USD 870 million in 2025 and is expected to reach approximately USD 995 million by 2032, growing at a CAGR of about 1.94% during 2026–2032. Constant demand due to the speed at which children outgrow their clothes, particularly school uniforms and shoes, sustains the growth of the market. Comfort, functionality, and affordability remain central priorities for Thai parents, with a strong demand for garments made from organic cotton, muslin, and breathable fabrics. At the same time, aesthetics are becoming important, and impulse purchases, both online and in stores, are driven by items featuring popular cartoon and internet characters.

Although parents' purchase habits have become increasingly more sophisticated, from an economic perspective, escalating living costs and household debt are factoring into purchasing habits. Unbranded, local, and inexpensive imported brands from China are gaining popularity. These offer value for money for families who seek quality but also affordability. At an overall level, the category leader continues to be apparel, with 70% market share, but here too, affordability is a factor in maintaining this activity-especially for middle- and lower-income families.

Second-hand childrenswear is expected to expand further over the forecast period, with parents becoming increasingly cost-conscious and sustainable in their choices. Online and social media-based resale platforms, especially Facebook and Instagram, make access to pre-owned clothes so much easier, including high-quality second-hand imports from Japan and South Korea. This might, however, bring challenges for new apparel sales growth, which would push brands to integrate more sustainable fabrics and circular fashion models into their operations.

While online channels have been on the rise, 85% of total sales are still made offline due to end userss' preference for inspecting fabric quality and fit. E-commerce and omnichannel retailing are, however, rapidly expanding, as social media, livestreaming, and influencer-led marketing continue to shape parents' purchasing decisions. Going forward, affordability, design appeal, and innovative retailing will be the keys to strategic market growth in Thailand's childrenswear market.

Thailand Childrenswear Market Growth Driver

Growing parental emphasis on quality and functionality

The trend in Thailand childrenswear market shows continuous growth, with both functionality and style gaining prominence from parents. Repeated replacement of clothes and a strong demand for breathable, soft fabrics like 100% cotton and muslin keeps demand steady for all age groups. Parents, especially those of infants and toddlers, are more inclined to choose garments that balance comfort and durability-a factor embraced by Thailand growing middle-income population. Urbanization in Thailand has reached 52.2% in 2024, indicating an increasingly broader end users group that appreciates practicality and modern design.

Furthermore, improving economic conditions are giving a boost to purchasing power and thereby shaping more discerning buying behaviour. Thailand GDP per capita grew by 3.1% in 2024 as shown by the IMF, indicating stronger financial capacity in urban families. As parents increasingly seek apparel that blends safety, softness, and aesthetic appeal, brands offering functional yet fashionable designs are well-placed to strengthen their market presence in the evolving retail landscape.

Thailand Childrenswear Market Trend

Popularity of Licensed Characters Boosts Apparel Appeal

A highly fashion-driven trend in Thailand childrenswear market is the rise of licensed character apparel. Designs from global icons such as Disney Princesses, Barbie, and Marvel superheroes have gained immense popularity among young Thai children. These characters strike a chord with young audiences, and they describe the essence of both entertainment and self-expression. Thailand has a 15% population of under-15-year-olds (UNICEF Thailand), making it highly relevant for such character-driven designs to tap into this huge customer base.

Moreover, the entertainment and media market increased by 4.2% in 2024 (UNESCO Institute for Statistics), increasing exposure to animation and film content that directly influences children's fashion trends. As parents continue to give in to the fashion demands of their kids, character licensing has emerged as a major differentiator for brands. This creates an emotional bond, boosts brand visibility, and strengthens the connection between popular culture and apparel consumption.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Thailand Childrenswear Market Opportunity

Expanding Second-Hand and Circular Fashion Market

Looking ahead, increasing acceptance of second-hand childrenswear creates great opportunities in Thailand circular fashion movement. Many parents today are increasingly aware of the more affordable and sustainable options available through resale platforms like Facebook Marketplace and Shopee. According to the National Statistical Office of Thailand, the average Thailand household spends 14% of its monthly budget on clothing and footwear, thus encouraging further participation in the resale economy.

Simultaneously, the country’s waste recycling rate increased to 36% in 2024, a fact indicative of stronger environmental consciousness. This transition presents an opportunity for brands to introduce resale programs, recycling partnerships, and eco-friendly materials that align with global circular fashion initiatives. Apparel makers could attract eco-aware parents and strengthen their long-term brand relevance within Thailand’s evolving retail ecosystem by embracing sustainable production and buy-back schemes.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Thailand Childrenswear Market Segmentation Analysis

By Product Type

- Apparel

- Footwear

- Accessories

- Others

The segment with highest market share under Product Type Apparel is the category that holds a market share of about 70% in the Thailand childrenswear market under Product Type. This segment of the market is dominated by apparel because parents are constantly replacing outgrown garments, especially school uniforms and day-to-day wear. This has been further cemented with the growing interest in quality fabrics like 100% cotton, organic material, and muslin, which mirror Thai parents' increasing awareness of comfort, safety, and durability. Moreover, clothing with cartoon characters, such as Labubu, Baby Three, and Sanrio, remain firm drivers of sales, combining design appeal with functionality.

Moreover, apparel continues to attract attention through its versatility and frequent need for replacement as children grow. With the expansion of both branded and unbranded options, affordable and durable apparel is gaining traction among middle- and low-income families. This broad demand base, from functional wear to character-themed wear, secures apparel's leading position in Thailand childrenswear market.

By Sales Channel

- Retail Offline

- Retail Online

The segment with highest market share under Sales Channel is Retail offline alone contributes to about 85% of the market share in the Thailand childrenswear market. Parents still prefer physical stores when it comes to shopping, as hands-on evaluation of the overall quality, fabric texture, and size matters. Generally, department stores, hypermarkets, and local shops dominate the retail channels, offering discounts, bundle deals, and promotional offers that appeal to budget-oriented families.

The revival of in-store shopping post-pandemic has also revived impulse buying, usually initiated by kids. Besides, most parents still put their trust in offline retail for kids' clothes because of quality assurance and the convenience brought by immediate purchases. Although online platforms are expanding fast-primarily through Shopee and Lazada-retail offline still dominates through familiarity, the strong brand presence it has, and blending affordability with real-time tangible shopping.

List of Companies Covered in Thailand Childrenswear Market

The companies listed below are highly influential in the Thailand childrenswear market, with a significant market share and a strong impact on industry developments.

- Thai Wacoal PCL

- Jaspal Co Ltd

- H&M Hennes & Mauritz AB

- Central Group

- ICC International PCL

- Roadget Business Pte Ltd

- Reno (Thailand) Co Ltd

- Uniqlo (Thailand) Co Ltd

- Nike Inc

- LVMH Moët Hennessy Louis Vuitton SA

Frequently Asked Questions

Related Report

1. Market Segmentation

1.1. Research Scope

1.2. Research Methodology

1.3. Definitions and Assumptions

2. Executive Summary

3. Thailand Childrenswear Market Policies, Regulations, and Standards

4. Thailand Childrenswear Market Dynamics

4.1. Growth Factors

4.2. Challenges

4.3. Trends

4.4. Opportunities

5. Thailand Childrenswear Market Statistics, 2022-2032F

5.1. Market Size & Growth Outlook

5.1.1.By Revenues in USD Million

5.2. Market Segmentation & Growth Outlook

5.2.1.By Product Type

5.2.1.1. Apparel- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.1. Baby and Toddler Wear- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.2. Boys Apparel- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.3. Girls Apparel- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2. Footwear- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.1. Boys Footwear- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.2. Girls Footwear- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3. Accessories- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3.1. Boys Accessories- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3.2. Girls Accessories- Market Insights and Forecast 2022-2032, USD Million

5.2.1.4. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.2.By Age Group

5.2.2.1. Infant/Toddler (Below 2 years)- Market Insights and Forecast 2022-2032, USD Million

5.2.2.2. Kids/Children (2 - 14 years)- Market Insights and Forecast 2022-2032, USD Million

5.2.3.By Price Category

5.2.3.1. Mass- Market Insights and Forecast 2022-2032, USD Million

5.2.3.2. Premium- Market Insights and Forecast 2022-2032, USD Million

5.2.4.By Sales Channel

5.2.4.1. Retail Offline- Market Insights and Forecast 2022-2032, USD Million

5.2.4.2. Retail Online- Market Insights and Forecast 2022-2032, USD Million

5.2.5.By Competitors

5.2.5.1. Competition Characteristics

5.2.5.2. Market Share & Analysis

6. Thailand Apparel Childrenswear Market Statistics, 2022-2032

6.1. Market Size & Growth Outlook

6.1.1.By Revenues in USD Million

6.2. Market Segmentation & Growth Outlook

6.2.1.By Age Group- Market Insights and Forecast 2022-2032, USD Million

6.2.2.By Price Category- Market Insights and Forecast 2022-2032, USD Million

6.2.3.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

7. Thailand Footwear Childrenswear Market Statistics, 2022-2032

7.1. Market Size & Growth Outlook

7.1.1.By Revenues in USD Million

7.2. Market Segmentation & Growth Outlook

7.2.1.By Age Group- Market Insights and Forecast 2022-2032, USD Million

7.2.2.By Price Category- Market Insights and Forecast 2022-2032, USD Million

7.2.3.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

8. Thailand Accessories Childrenswear Market Statistics, 2022-2032

8.1. Market Size & Growth Outlook

8.1.1.By Revenues in USD Million

8.2. Market Segmentation & Growth Outlook

8.2.1.By Age Group- Market Insights and Forecast 2022-2032, USD Million

8.2.2.By Price Category- Market Insights and Forecast 2022-2032, USD Million

8.2.3.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

9. Competitive Outlook

9.1. Company Profiles

9.1.1.Central Group

9.1.1.1. Business Description

9.1.1.2. Product Portfolio

9.1.1.3. Collaborations & Alliances

9.1.1.4. Recent Developments

9.1.1.5. Financial Details

9.1.1.6. Others

9.1.2.ICC International PCL

9.1.2.1. Business Description

9.1.2.2. Product Portfolio

9.1.2.3. Collaborations & Alliances

9.1.2.4. Recent Developments

9.1.2.5. Financial Details

9.1.2.6. Others

9.1.3.Roadget Business Pte Ltd

9.1.3.1. Business Description

9.1.3.2. Product Portfolio

9.1.3.3. Collaborations & Alliances

9.1.3.4. Recent Developments

9.1.3.5. Financial Details

9.1.3.6. Others

9.1.4.Reno (Thailand) Co Ltd

9.1.4.1. Business Description

9.1.4.2. Product Portfolio

9.1.4.3. Collaborations & Alliances

9.1.4.4. Recent Developments

9.1.4.5. Financial Details

9.1.4.6. Others

9.1.5.Uniqlo (Thailand) Co Ltd

9.1.5.1. Business Description

9.1.5.2. Product Portfolio

9.1.5.3. Collaborations & Alliances

9.1.5.4. Recent Developments

9.1.5.5. Financial Details

9.1.5.6. Others

9.1.6.Thai Wacoal PCL

9.1.6.1. Business Description

9.1.6.2. Product Portfolio

9.1.6.3. Collaborations & Alliances

9.1.6.4. Recent Developments

9.1.6.5. Financial Details

9.1.6.6. Others

9.1.7.Jaspal Co Ltd

9.1.7.1. Business Description

9.1.7.2. Product Portfolio

9.1.7.3. Collaborations & Alliances

9.1.7.4. Recent Developments

9.1.7.5. Financial Details

9.1.7.6. Others

9.1.8.H&M Hennes & Mauritz AB

9.1.8.1. Business Description

9.1.8.2. Product Portfolio

9.1.8.3. Collaborations & Alliances

9.1.8.4. Recent Developments

9.1.8.5. Financial Details

9.1.8.6. Others

9.1.9.Nike Inc

9.1.9.1. Business Description

9.1.9.2. Product Portfolio

9.1.9.3. Collaborations & Alliances

9.1.9.4. Recent Developments

9.1.9.5. Financial Details

9.1.9.6. Others

9.1.10. LVMH Moët Hennessy Louis Vuitton SA

9.1.10.1. Business Description

9.1.10.2. Product Portfolio

9.1.10.3. Collaborations & Alliances

9.1.10.4. Recent Developments

9.1.10.5. Financial Details

9.1.10.6. Others

10. Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Product Type |

|

| By Age Group |

|

| By Price Category |

|

| By Sales Channel |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.