Sweden Childrenswear Market Report: Trends, Growth and Forecast (2026-2032)

Product Type (Apparel (Baby and Toddler Wear, Boys Apparel, Girls Apparel), Footwear (Boys Footwear, Girls Footwear), Accessories (Boys Accessories, Girls Accessories), Others), Age Group (Infant/Toddler (Below 2 years), Kids/Children (2 - 14 years)), Price Category (Mass, Premium), Sales Channel (Retail Offline, Retail Online) ... Read more

|

Major Players

|

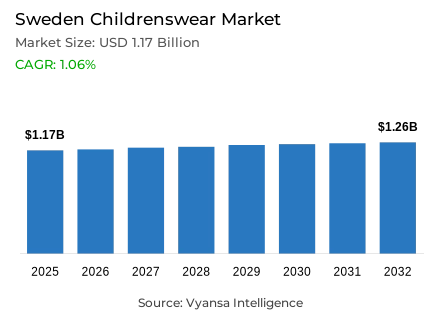

Sweden Childrenswear Market Statistics and Insights, 2026

- Market Size Statistics

- Childrenswear in Sweden is estimated at USD 1.17 billion.

- The market size is expected to grow to USD 1.26 billion by 2032.

- Market to register a cagr of around 1.06% during 2026-32.

- Product Type Shares

- Apparel grabbed market share of 80%.

- Competition

- More than 20 companies are actively engaged in producing childrenswear in Sweden.

- Top 5 companies acquired around 50% of the market share.

- Zara Sverige AB; Cubus AB; Nike Sweden AB; Lindex Sverige AB; H&M Hennes & Mauritz Sverige AB etc., are few of the top companies.

- Sales Channel

- Retail offline grabbed 70% of the market.

Sweden Childrenswear Market Outlook

The Sweden childrenswear market is valued at USD 1.17 billion in 2025, is set to reach USD 1.26 billion by 2032, expanding at a CAGR of around 1.06% during 2026-2032. Despite modest growth, the market faces challenges from the country’s declining population of children aged 0-14 years and the rising second-hand clothing trend, which continues to weigh on volume sales. However, steady demand for sustainable and high-quality apparel, which accounts for about 80% of total market share, underpins value growth. Swedish parents continue to invest in durable, functional, and eco-friendly childrenswear, particularly for outdoor activities, reflecting the nation’s strong environmental consciousness.

Sustainability continues to be the strong force shaping the market. Major brands including Polarn O Pyret, H&M, and KappAhl are increasing initiatives for recycling and second-hand purchases, such as PO.P Second-Hand and in-store garment collection schemes. Parents increasingly consider childrenswear as an investment, taking a quality over quantity approach to durable fabrics that can be used again, passed on, or resold. This is reflective of the wider Swedish attitude toward a circular economy, where buying second-hand clothing has become completely normalized. Sustainable collections are increasingly available through online channels such as Zalando and Babyshop.

The growth of retail e-commerce, supported by the strong digital infrastructure in the country, reshapes buying behavior. Even as retail offline accounts for around 70% of total sales, the online channel continues to grow rapidly due to convenience, wider product variety, and easy returns. Busy lifestyle parents of younger children are increasingly using online channels to shop, whereas older kids and teenagers take their fashion cues from social media platforms such as TikTok, Instagram, and YouTube, driving demand for trendy, value-for-money apparel.

Looking ahead, while low birth rates and the second-hand market will continue to constrain volume growth, value sales are expected to rise steadily due to premiumisation and sustainability-led consumption. Brands focusing on durability, transparency, and ethical production are likely to maintain a competitive advantage. Continued investment in online retailing, sustainability programs, and youth-oriented digital marketing will help players strengthen engagement and sustain moderate yet stable market growth.

Sweden Childrenswear Market Growth Driver

Government-Led Sustainability and end users Awareness Drive Market Growth

Sweden childrenswear market is growing rapidly, driven by the country's government sustainability policies and increased environmental awareness among parents. Swedish households have become much more environmentally aware regarding textile production and actively seek clothing made from organic, recycled, or responsibly sourced materials. This shift has encouraged leading brands such as Polarn O Pyret, H&M, and KappAhl to expand circular fashion initiatives, including take-back and resale programs that align with national environmental goals. The government's circular economy strategy continues to influence buying behavior, with eco-responsibility highlighted as a leading theme in the decision-making process when it comes to family clothing.

These efforts at the national level further reinforce sustainable consumption as a driver of long-term growth. According to Statistics Sweden, 90% of Swedish households sort waste for recycling, while the Swedish EPA reported textile recycling increased by 8% in 2024. Together, these policies and end users values have powered demand for durable, eco-friendly childrenswear, making Sweden one of Europe's most sustainability-oriented apparel markets.

Sweden Childrenswear Market Challenge

Falling Birth Rates Restrict Volume Growth Despite Value Expansion

The main factor that has affected Sweden's childrenswear market is the continuous decline in the child population. While retail value is supported by inflation and the premiumization trend, volume growth remains limited due to shrinking bases for children under 14 years of age. Families in Sweden focus on quality and functionality, especially in outdoor and durable clothes, but this reduces the age cohorts of younger children and diminishes further expansion possibilities. With a view to maintaining profitability, the industry will increasingly have to concentrate on higher-value rather than volume-driven growth.

This demographic contraction puts the onus on brands to innovate and differentiate via sustainability, design, and longevity of products. According to Statistics Sweden, the number of children within the 0-14 age bracket declined 2.3% in the year 2024, while the fertility rate fell to 1.52 babies per woman-the lowest figure in two decades. Eurostat projections suggest the downward trend will continue, entrenching the need for brands to adapt their strategies in a smaller but more discerning end users base.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Sweden Childrenswear Market Trend

Sustainability and Circular Fashion Redefine Swedish Childrenswear

Sustainability became the defining trend in Sweden's childrenswear market, with wide-scale adoption of circular fashion practices. Parents increasingly prefer durable, eco-friendly garments designed for reuse, resale, or to be handed down. This reflects deep-rooted Swedish culture for environmental responsibility. In response, brands are enhancing their sustainability credentials by initiating clothing return rewards and product longevity programs. Programs such as PO.P Second-Hand by Polarn O Pyret and garment recycling schemes by KappAhl are examples of companies integrating circularity into the core business model.

This market shift is in tune with European efforts to reduce textile waste and lower carbon emissions. According to the Swedish EPA, textiles account for 3% of Sweden's total carbon footprint, while the European Commission estimates that circular textile initiatives could reduce emissions by up to 40% by 2030. As sustainability becomes integral to family purchasing decisions, eco-conscious fashion is moving from a niche segment to a mainstream standard in Sweden's childrenswear landscape.

Sweden Childrenswear Market Opportunity

Second-Hand Clothes Are Driving Growth via Circular Consumption

The development of Sweden's second-hand clothing ecosystem is creating new avenues for sustainable growth in the childrenswear market. Parents are increasingly turning to second-hand clothing as an affordable and more sustainable option, with resale models going mainstream. From online resale sites to dedicated children's second-hand boutiques like Inimini and Glam Up Kids, online resale platforms are changing how kids' clothes are bought and sold. In addition, buy-back and resale programs are being launched by brands as a means of enhancing customer loyalty while reducing textile waste, in line with Sweden's goals of a circular economy.

The increasing connection between the importance of taking care of the environment and cost efficiency is redefining how value is created within the sector. According to Statistics Sweden, in 2024, 65% of Swedes bought or sold second-hand goods, while the European Environment Agency underlines that reused textiles produce 40% less GHG emissions compared with new clothing. With sustainable consumption gathering speed, the resale segment is all set to emerge as a strong avenue contributing to growth within Sweden's childrenswear market

Unlock Market Intelligence

Explore the market potential with our data-driven report

Sweden Childrenswear Market Segmentation Analysis

By Product Type

- Apparel

- Footwear

- Accessories

- Others

The segment with highest market share under By product type is apparel has a share of about 80% in the Sweden childrenswear market. Apparel leads the category due to the rising need among Swedish parents for durable, comfortable, and weather-friendly outfits for their children. The general outdoors culture and harsh climatic conditions in the country drive up demand for quality clothes serving all-year-round activities.

High-end and sustainable apparel brands, such as Polarn O Pyret and Mini Rodini, continue to attract parents who value eco-friendly and long-lasting materials that can be reused or resold. Moreover, with sustainability becoming central in purchasing decisions, the circular approach toward fashion is strengthening its position even further. Parents increasingly opt for high-end apparel with resale value, which reflects the growing eco-awareness of parents. The expanding retail e-commerce platforms that offer eco-conscious and second-hand apparel options also support this segment's ongoing dominance in Sweden's childrenswear market.

By Sales Channel

- Retail Offline

- Retail Online

The segment with highest market share under Sales Channel is Retail offline with around 70% of the Sweden childrenswear market share. Physical stores remain one of the most favorable aspects for parents, as they like to check the quality of the fabric, fitting, and comfort before making a purchase. Large chains such as H&M, Lindex, and KappAhl continue to anchor the offline landscape with extensive store networks and sustainable collections catering to families across the nation.

At the same time, physical stores are responding to changing attitudes by adding sustainability initiatives and second-hand programs, encouraging customers to recycle or trade in old clothes. These initiatives drive not only foot traffic into the stores but also tap into Sweden's strong sustainability mindset. While online shopping has grown rapidly, the offline channel will continue to dominate as it ensures trust, convenience, and a match with the trend of Swedish parents seeking high-quality, well-manufactured clothes.

List of Companies Covered in Sweden Childrenswear Market

The companies listed below are highly influential in the Sweden childrenswear market, with a significant market share and a strong impact on industry developments.

- Zara Sverige AB

- Cubus AB

- Nike Sweden AB

- Lindex Sverige AB

- H&M Hennes & Mauritz Sverige AB

- KappAhl Sverige AB (Publ)

- Polarn O Pyret AB

- adidas Sverige AB

- Gant Sweden AB

- Lager 157 AB

Frequently Asked Questions

Related Report

1. Market Segmentation

1.1. Research Scope

1.2. Research Methodology

1.3. Definitions and Assumptions

2. Executive Summary

3. Sweden Childrenswear Market Policies, Regulations, and Standards

4. Sweden Childrenswear Market Dynamics

4.1. Growth Factors

4.2. Challenges

4.3. Trends

4.4. Opportunities

5. Sweden Childrenswear Market Statistics, 2022-2032F

5.1. Market Size & Growth Outlook

5.1.1.By Revenues in USD Million

5.2. Market Segmentation & Growth Outlook

5.2.1.By Product Type

5.2.1.1. Apparel- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.1. Baby and Toddler Wear- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.2. Boys Apparel- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.3. Girls Apparel- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2. Footwear- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.1. Boys Footwear- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.2. Girls Footwear- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3. Accessories- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3.1. Boys Accessories- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3.2. Girls Accessories- Market Insights and Forecast 2022-2032, USD Million

5.2.1.4. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.2.By Age Group

5.2.2.1. Infant/Toddler (Below 2 years)- Market Insights and Forecast 2022-2032, USD Million

5.2.2.2. Kids/Children (2 - 14 years)- Market Insights and Forecast 2022-2032, USD Million

5.2.3.By Price Category

5.2.3.1. Mass- Market Insights and Forecast 2022-2032, USD Million

5.2.3.2. Premium- Market Insights and Forecast 2022-2032, USD Million

5.2.4.By Sales Channel

5.2.4.1. Retail Offline- Market Insights and Forecast 2022-2032, USD Million

5.2.4.2. Retail Online- Market Insights and Forecast 2022-2032, USD Million

5.2.5.By Competitors

5.2.5.1. Competition Characteristics

5.2.5.2. Market Share & Analysis

6. Sweden Apparel Childrenswear Market Statistics, 2022-2032

6.1. Market Size & Growth Outlook

6.1.1.By Revenues in USD Million

6.2. Market Segmentation & Growth Outlook

6.2.1.By Age Group- Market Insights and Forecast 2022-2032, USD Million

6.2.2.By Price Category- Market Insights and Forecast 2022-2032, USD Million

6.2.3.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

7. Sweden Footwear Childrenswear Market Statistics, 2022-2032

7.1. Market Size & Growth Outlook

7.1.1.By Revenues in USD Million

7.2. Market Segmentation & Growth Outlook

7.2.1.By Age Group- Market Insights and Forecast 2022-2032, USD Million

7.2.2.By Price Category- Market Insights and Forecast 2022-2032, USD Million

7.2.3.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

8. Sweden Accessories Childrenswear Market Statistics, 2022-2032

8.1. Market Size & Growth Outlook

8.1.1.By Revenues in USD Million

8.2. Market Segmentation & Growth Outlook

8.2.1.By Age Group- Market Insights and Forecast 2022-2032, USD Million

8.2.2.By Price Category- Market Insights and Forecast 2022-2032, USD Million

8.2.3.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

9. Competitive Outlook

9.1. Company Profiles

9.1.1.Lindex Sverige AB

9.1.1.1. Business Description

9.1.1.2. Product Portfolio

9.1.1.3. Collaborations & Alliances

9.1.1.4. Recent Developments

9.1.1.5. Financial Details

9.1.1.6. Others

9.1.2.H&M Hennes & Mauritz Sverige AB

9.1.2.1. Business Description

9.1.2.2. Product Portfolio

9.1.2.3. Collaborations & Alliances

9.1.2.4. Recent Developments

9.1.2.5. Financial Details

9.1.2.6. Others

9.1.3.KappAhl Sverige AB (Publ)

9.1.3.1. Business Description

9.1.3.2. Product Portfolio

9.1.3.3. Collaborations & Alliances

9.1.3.4. Recent Developments

9.1.3.5. Financial Details

9.1.3.6. Others

9.1.4.Polarn O Pyret AB

9.1.4.1. Business Description

9.1.4.2. Product Portfolio

9.1.4.3. Collaborations & Alliances

9.1.4.4. Recent Developments

9.1.4.5. Financial Details

9.1.4.6. Others

9.1.5.adidas Sverige AB

9.1.5.1. Business Description

9.1.5.2. Product Portfolio

9.1.5.3. Collaborations & Alliances

9.1.5.4. Recent Developments

9.1.5.5. Financial Details

9.1.5.6. Others

9.1.6.Zara Sverige AB

9.1.6.1. Business Description

9.1.6.2. Product Portfolio

9.1.6.3. Collaborations & Alliances

9.1.6.4. Recent Developments

9.1.6.5. Financial Details

9.1.6.6. Others

9.1.7.Cubus AB

9.1.7.1. Business Description

9.1.7.2. Product Portfolio

9.1.7.3. Collaborations & Alliances

9.1.7.4. Recent Developments

9.1.7.5. Financial Details

9.1.7.6. Others

9.1.8.Nike Sweden AB

9.1.8.1. Business Description

9.1.8.2. Product Portfolio

9.1.8.3. Collaborations & Alliances

9.1.8.4. Recent Developments

9.1.8.5. Financial Details

9.1.8.6. Others

9.1.9.Gant Sweden AB

9.1.9.1. Business Description

9.1.9.2. Product Portfolio

9.1.9.3. Collaborations & Alliances

9.1.9.4. Recent Developments

9.1.9.5. Financial Details

9.1.9.6. Others

9.1.10. Lager 157 AB

9.1.10.1. Business Description

9.1.10.2. Product Portfolio

9.1.10.3. Collaborations & Alliances

9.1.10.4. Recent Developments

9.1.10.5. Financial Details

9.1.10.6. Others

10. Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Product Type |

|

| By Age Group |

|

| By Price Category |

|

| By Sales Channel |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.