Thailand Bottled Water Market Report: Trends, Growth and Forecast (2026-2032)

By Type of Water (Carbonated Bottled Water, Flavoured Bottled Water, Functional Bottled Water, Still Bottled Water), By Sub Types (Purified (Desalinated, Atmospheric Generated, Others), Mineral, Other (Spring, Alkaline, Other)), By Packaging Material (Flexible Packaging (Aluminium, Pouches), Glass, Rigid Plastic (PET Bottles, Thin Wall Plastic Containers, Others)), By Price Category (Budget, Economy, Premium), By Pack Size (100 ml, 125 ml, 200 ml, 250 ml, 330 ml, 370 ml, 450 ml, 500 ml, 591 ml, 750 ml, 1,000 ml, 1,500 ml, 4,000 ml, 5,000 ml, Others), By Sales Channel (On Trade (Restaurants, Hotels, Cafes, Others), Off Trade (Grocery Retailers (Convenience Retail, Supermarkets, Hypermarkets, Small Local Grocer), Non-Grocery Retailers (General Merchandise Stores, Health and Beauty Specialists), Vending, E-commerce)) ... Read more

|

Major Players

|

Thailand Bottled Water Market Statistics and Insights, 2026

- Market Size Statistics

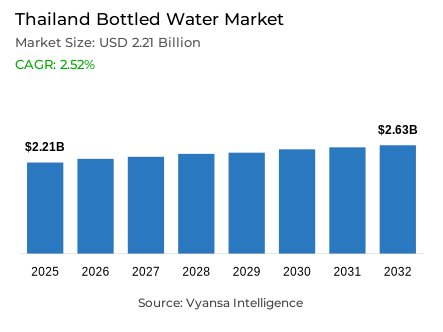

- Bottled water market size in Thailand was estimated at USD 2.21 billion in 2025.

- The market size is expected to grow to USD 2.63 billion by 2032.

- Market to register a CAGR of around 2.52% during 2026-32.

- Type of Water Shares

- Still bottled water grabbed market share of 75%.

- Competition

- More than 20 companies are actively engaged in producing bottled water in Thailand.

- Top 5 companies acquired around 50% of the market share.

- Tipco Foods (Thailand) PCL, General Beverage Co Ltd, ICC International PCL, Boon Rawd Brewery Co Ltd, Serm Suk PCL etc., are few of the top companies.

- Sales Channel

- Off trade grabbed 70% of the market.

Thailand Bottled Water Market Outlook

The market of Thailand bottled water is estimated at USD 2.21 billion in 2025 and is expected to reach approximately USD 2.63 billion by 2032, registering a moderate CAGR of around 2.52% during the 2026-2032 period.The market of Thailand bottled water remains influenced by the basic consumption trends and the views on the water safety. The major choice of families in Thailand is bottled water over direct tap water because of the fear of the quality of tap water, despite the fact that better drinking water sources exist throughout the country as shown by UNICEF/WHO statistics. In a 2023 study, 74.6% of households indicated that bottled water was their most frequently used source of drinking water, highlighting its extensive infiltration into everyday life.

However, the essence of this demand is bottled water, which is affordable and is used in daily hydration. The off-trade sales represent a considerable 70% of the bottling distribution, and hypermarkets and e-commerce offer extensive coverage of both urban and rural markets. This distribution reach helps in stable volume growth and habitual purchasing behaviour.

End users in urban areas are also trying out functional versions that have added health advantages, thus aiding brand differentiation in store shelves. This has prompted brands to go beyond simple hydration to attract wellness-conscious end users.

The bottled water is still a solid foundation to future growth since regional demand beyond the large cities is still a strong pillar since bottled water remains the most viable hydration choice where infrastructure limitations still exist. These varied demand forces form a strong market base as the bottled water sector in Thailand progresses to 2032.

Thailand Bottled Water Market Growth DriverClimate and Daily Hydration Needs Sustain Demand

The structural and lifestyle factors that have been entrenched in the daily consumption patterns are the main drivers of demand of bottled water in Thailand. Off-trade volume sales grew by 2% to 2025, which was facilitated by the hot and humid climate in Thailand and the lack of drinkable tap water. Bottled water remains a cheap, ubiquitous source of hydration in urban and rural regions, and it is a necessity in everyday life. Many workers, especially in service, retail, and outdoor jobs, have easy access to water dispensers in the workplace, which further strengthens the reliance on bottled water as a source of on-the-go hydration.

Still bottled water continues to dominate this demand with off-trade volumes expected to increase by 2-3% to 3,769,000 litres in 2025. Regular purchasing behaviour is still supported by its low cost and the ability to consume it on a regular basis, which ensures consistent volume growth regardless of income level.

Thailand Bottled Water Market ChallengeGradual Shift Toward Home Water Purification

One of the major issues that face the consumption of bottled water is the increasing use of home water purifiers by urban households. Although bottled water is still a necessity in terms of mobility and convenience, water filtration systems reduce the use of bottled water in the home. This is more evident in large cities where end users have more access to filtration technology and other hydration options.

Another challenge facing urban end users is the growing number of alternative beverage products such as functional beverages, RTD tea and sports drinks that compete with hydration events. Despite the fact that off-trade bottled water volume is still increasing in 2025, these substitutes are causing slower penetration growth in urban regions, which is putting pressure on bottled water brands to protect shelf space and consumption frequency in households that are increasingly relying on purified tap water as their daily consumption.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Thailand Bottled Water Market TrendCustomer Attraction Towards Premium and Functional Waters

Premiumisation is a conspicuous trend that determines the consumption pattern of bottled water. Even though still bottled water still reigns in the daily hydration, high-end urban end users are starting to see bottled water as a lifestyle and wellness product. Imported, mineral, and origin-specific waters have increased visibility in high-end retailing, with end users relating provenance, mineral content, and purity assertions to quality and wellbeing.

Health-conscious end users who want more than just hydration also like functional bottled water. Fortified products, such as those with vitamins, minerals, or electrolytes, are especially popular among urban workers, but they represent a smaller percentage of the total volumes. Still bottled water is still leading functional variants in terms of volume growth, and functional products are increasingly having an impact on brand differentiation and shelf strategies in competitive retail settings.

Thailand Bottled Water Market OpportunityExpansion Beyond Core Urban Centres

A significant opportunity is to increase the use of bottled water not only in large cities but also in peri-urban and remote areas. Bottled water is also the main hydration choice in most of these regions because of the lack of access to safe tap water or effective filtration systems. The familiarity with the brand and convenience support the position of bottled water as a reliable everyday need.

The small local grocer distribution ensures coverage of non-urban geographies, which maintains consistent demand even in times of limited consumer expenditure. With the maturity of urban markets, these under-served areas remain to support volume relevance of still bottled water, thus facilitating geographic diversification that maintains constant demand by fulfilling basic hydration requirements where infrastructure limitations still exist.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Thailand Bottled Water Market Segmentation Analysis

By Type of Water

- Carbonated Bottled Water

- Flavoured Bottled Water

- Functional Bottled Water

- Still Bottled Water

Under the category of type of water segment, still bottled water continues to dominate the market with the largest share of 75% of all bottled water. Its supremacy is a measure of affordability, mass supply, and applicability to daily hydration of all income brackets. Still bottled water is commonly bought to store at home and to carry around, which makes it highly integrated into everyday life.

In 2025,Still bottled water will be the most vibrant category in terms of volume , which will be backed by regular consumption occasions and bulk purchasing behaviour. Although functional and premium waters are gaining traction in urban markets, still bottled water remains the foundation of aggregate demand because of its necessity and wide availability.

By Sales Channel

- On Trade

- Restaurants

- Hotels

- Cafes

- Others

- Off Trade

- Grocery Retailers

- Convenience Retail

- Supermarkets

- Hypermarkets

- Small Local Grocer

- Non-Grocery Retailers

- General Merchandise Stores

- Health and Beauty Specialists

- Vending

- E-commerce

- Grocery Retailers

In the Sales Channel category, the off-trade segment has the largest share with 70% of the sales of bottled water. Hypermarkets are still the most popular off-trade channel due to bulk buying, and retail e-commerce has become the most vibrant channel in terms of stock-up behaviour among urban end users.

Although modern retail has expanded, small local grocers are still essential, especially in semi-urban and rural regions where modern penetration of trade is less. This mixed distribution system will make bottled water highly available in geographies, hence strengthening its position as a staple product in bottled water market of Thailand.

List of Companies Covered in Thailand Bottled Water Market

The companies listed below are highly influential in the Thailand bottled water market, with a significant market share and a strong impact on industry developments.

- Tipco Foods (Thailand) PCL

- General Beverage Co Ltd

- ICC International PCL

- Boon Rawd Brewery Co Ltd

- Serm Suk PCL

- Nestlé (Thai) Ltd

- Thai Pure Drinks Ltd

- Thai Beverage PCL

- TC Pharmaceutical Industry Co Ltd

- Pepsi-Cola (Thai) Trading Co Ltd

Competitive Landscape

Boon Rawd Brewery leads Thailand’s bottled water market in off-trade volume, thanks to a diverse portfolio that includes purified, mineral, and carbonated water. This variety allows the company to meet different end user needs and occasions. Strong brand recognition and trust, particularly in its flagship Singha brand, support its market leadership. Regular wins of “No. 1 Brand Thailand” awards reinforce its authority beyond alcoholic beverages and help leverage loyalty when entering new beverage segments.Tipco Foods (Thailand) PCL is a dynamic competitor, driven by its Aura brand. Aura highlights natural sourcing from rainfall filtered 250m underground and offers multiple pack sizes (1,500ml, 500ml, 330ml). Its focus on purity, mineral content, and health benefits appeals to wellness-conscious end users, positioning Aura as a premium alternative and challenging competitors to compete on brand story and end user trust, not just scale or price.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- Thailand Bottled Water Market Policies, Regulations, and Standards

- Thailand Bottled Water Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- Thailand Bottled Water Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Volume (Million Litres)

- Market Segmentation & Growth Outlook

- By Type of Water

- Carbonated Bottled Water- Market Insights and Forecast 2022-2032, USD Million

- Flavoured Bottled Water- Market Insights and Forecast 2022-2032, USD Million

- Functional Bottled Water- Market Insights and Forecast 2022-2032, USD Million

- Still Bottled Water- Market Insights and Forecast 2022-2032, USD Million

- By Sub Types

- Purified- Market Insights and Forecast 2022-2032, USD Million

- Desalinated- Market Insights and Forecast 2022-2032, USD Million

- Atmospheric Generated- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- Mineral- Market Insights and Forecast 2022-2032, USD Million

- Other (Spring, Alkaline, Other) - Market Insights and Forecast 2022-2032, USD Million

- Purified- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material

- Flexible Packaging- Market Insights and Forecast 2022-2032, USD Million

- Aluminium- Market Insights and Forecast 2022-2032, USD Million

- Pouches- Market Insights and Forecast 2022-2032, USD Million

- Glass- Market Insights and Forecast 2022-2032, USD Million

- Rigid Plastic- Market Insights and Forecast 2022-2032, USD Million

- PET Bottles- Market Insights and Forecast 2022-2032, USD Million

- Thin Wall Plastic Containers- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- Flexible Packaging- Market Insights and Forecast 2022-2032, USD Million

- By Price Category

- Budget- Market Insights and Forecast 2022-2032, USD Million

- Economy- Market Insights and Forecast 2022-2032, USD Million

- Premium- Market Insights and Forecast 2022-2032, USD Million

- By Pack Size

- 100 ml- Market Insights and Forecast 2022-2032, USD Million

- 125 ml- Market Insights and Forecast 2022-2032, USD Million

- 200 ml- Market Insights and Forecast 2022-2032, USD Million

- 250 ml- Market Insights and Forecast 2022-2032, USD Million

- 330 ml- Market Insights and Forecast 2022-2032, USD Million

- 370 ml- Market Insights and Forecast 2022-2032, USD Million

- 450 ml- Market Insights and Forecast 2022-2032, USD Million

- 500 ml- Market Insights and Forecast 2022-2032, USD Million

- 591 ml- Market Insights and Forecast 2022-2032, USD Million

- 750 ml- Market Insights and Forecast 2022-2032, USD Million

- 1,000 ml- Market Insights and Forecast 2022-2032, USD Million

- 1,500 ml- Market Insights and Forecast 2022-2032, USD Million

- 4,000 ml- Market Insights and Forecast 2022-2032, USD Million

- 5,000 ml- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel

- On Trade- Market Insights and Forecast 2022-2032, USD Million

- Restaurants- Market Insights and Forecast 2022-2032, USD Million

- Hotels- Market Insights and Forecast 2022-2032, USD Million

- Cafes- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- Off Trade- Market Insights and Forecast 2022-2032, USD Million

- Grocery Retailers- Market Insights and Forecast 2022-2032, USD Million

- Convenience Retail- Market Insights and Forecast 2022-2032, USD Million

- Supermarkets- Market Insights and Forecast 2022-2032, USD Million

- Hypermarkets- Market Insights and Forecast 2022-2032, USD Million

- Small Local Grocer- Market Insights and Forecast 2022-2032, USD Million

- Non-Grocery Retailers- Market Insights and Forecast 2022-2032, USD Million

- General Merchandise Stores- Market Insights and Forecast 2022-2032, USD Million

- Health and Beauty Specialists- Market Insights and Forecast 2022-2032, USD Million

- Vending- Market Insights and Forecast 2022-2032, USD Million

- E-commerce- Market Insights and Forecast 2022-2032, USD Million

- Grocery Retailers- Market Insights and Forecast 2022-2032, USD Million

- On Trade- Market Insights and Forecast 2022-2032, USD Million

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Type of Water

- Market Size & Growth Outlook

- Thailand Carbonated Bottled Water Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Volume (Million Litres)

- Market Segmentation & Growth Outlook

- By Sub Types- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Pack Size- Market Insights and Forecast 2022-2032, USD Million

- By Price Category- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Thailand Flavoured Bottled Water Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Volume (Million Litres)

- Market Segmentation & Growth Outlook

- By Sub Types- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Pack Size- Market Insights and Forecast 2022-2032, USD Million

- By Price Category- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Thailand Functional Bottled Water Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Volume (Million Litres)

- Market Segmentation & Growth Outlook

- By Sub Types- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Pack Size- Market Insights and Forecast 2022-2032, USD Million

- By Price Category- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Thailand Still Bottled Water Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Volume (Million Litres)

- Market Segmentation & Growth Outlook

- By Sub Types- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Pack Size- Market Insights and Forecast 2022-2032, USD Million

- By Price Category- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Boon Rawd Brewery Co Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Serm Suk PCL

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Nestlé (Thai) Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Thai Pure Drinks Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Thai Beverage PCL

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Tipco Foods (Thailand) PCL

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- General Beverage Co Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- ICC International PCL

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- TC Pharmaceutical Industry Co Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Pepsi-Cola (Thai) Trading Co Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Boon Rawd Brewery Co Ltd

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Type of Water |

|

| By Sub Types |

|

| By Packaging Material |

|

| By Price Category |

|

| By Pack Size |

|

| By Sales Channel |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.