Sweden Sports Nutrition Market Report: Trends, Growth and Forecast (2026-2032)

By Product Type (Sports Protein Products (Protein/Energy Bars, Sports Protein Powder, Sports Protein RTD), Sports Non-Protein Products), By Sales Channel (Retail Offline, Retail Online), By Ingredients (Vitamins and Minerals, Proteins and Amino Acids, Carbohydrates, Probiotics, Botanicals/Herbals, Others), By Functionality (Energy, Muscle growth, Hydration, Weight Management, Others), By End User (Bodybuilders, Athletes, Lifestyle Users) ... Read more

|

Major Players

|

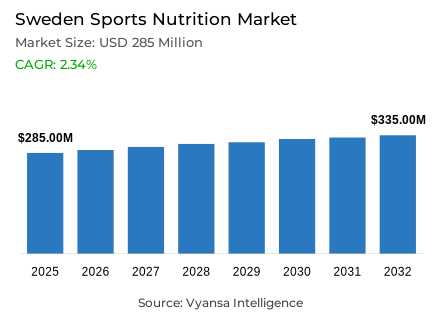

Sweden Sports Nutrition Market Statistics and Insights, 2026

- Market Size Statistics

- Sports nutrition market size in Sweden was estimated at USD 285 million in 2025.

- The market size is expected to grow to USD 335 million by 2032.

- Market to register a CAGR of around 2.34% during 2026-32.

- Product Type Shares

- Sports protein products grabbed market share of 70%.

- Competition

- More than 20 companies are actively engaged in producing sports nutrition in Sweden.

- Top 5 companies acquired around 50% of the market share.

- MM Sports AB, 13:e Protein Import AB, Nordic Sports Nutrition AB, Barebells Functional Foods AB, Orkla Care AB etc., are few of the top companies.

- Sales Channel

- Retail online grabbed 60% of the market.

Sweden Sports Nutrition Market Outlook

The Sweden sports nutrition market is estimated to have a long-term, moderate growth during the forecast period, increasing USD 285 million in 2025 to USD 335 million in 2032, thus, depicting a compound annual growth rate of about 2.34%. The strong gym going culture in Sweden, the growing focus on preventive healthcare, and the gradual mainstream acceptance of protein-rich nutrition will support market growth. Protein products, which now constitute approximately 70% of the total market value, will continue to be the foundation of the category, and protein powders, ready-to-drink beverages, and bars will still be demanded. Their wide accessibility on online platforms, fitness centres, and grocery stores will further support habitual consumption among all age groups.

The convenience-based consumption trends are likely to be at the center of the market development up to 2032. The already popular products like sports-protein RTDs and protein or energy bars are expected to experience increased adoption by time-starved end users seeking fast, nutritionally balanced products. At the same time, the increasing popularity of protein-enhanced foods will probably blur the category lines, prompting brands to experiment with flavors, textures, and delivery systems. This growing end-user base, between younger fitness-conscious and older adults who are more interested in muscle maintenance, will keep the market dynamic.

The sports nutrition of plant-based products will gain significant momentum in the outlook period. With a growing share of Swedish end users switching to vegan and vegetarian diets, the demand of clean-label, natural, and plant-based protein alternatives is expected to increase. Brands that diversify to offer vegan powders, bars, and RTDs will be in a good position to tap into this demand, especially as plant-based nutrition remains linked with healthier and more natural lifestyle decisions.

The retail online, which currently constitutes about 60% of the total market value, is likely to continue as the leading channel of distribution. Affordable prices, convenience in buying in large quantities, speedy delivery, and large product selections remain very appealing to sports nutrition end users in retail online. With the major brands becoming more aggressive with their digital approaches, online-only product releases and price wars are expected to rise. In general, long-term health-related practices, further development of convenient formats, and strong retail online dynamics will support the stable market growth until 2032.

Sweden Sports Nutrition Market Growth Driver

Strong national physical-activity levels and rising health awareness expand nutrition demand

Demand for sports nutrition products in Sweden continues to be shaped by the country’s high level of participation in physical and recreational activities. The 2024 World Health Organization country profile indicates that a significant percentage of adults in Sweden are active and fit to or beyond the recommended levels of physical activity, which is a deep-rooted culture of movement and fitness. Simultaneously, 2024 data on the adoption of digital technologies show that 98.1% of the population has access to the internet, which implies that it is highly exposed and open to health and wellness information, including messages that can encourage protein supplementation and functional nutrition.

Collectively, these elements justify the demand of protein powders, shakes, and fortified nutrition products across a wide range of final end users, such as gym-goers, recreational exercisers, and health-conscious adults. With nutrition becoming more of a part of holistic wellness practices, repeat and first-time buyers are driving volume growth among a variety of age groups.

Sweden Sports Nutrition Market Challenge

Overweight/obesity prevalence and population segments’ low exercise frequency limit recurring product uptake

Despite elevated levels of health awareness, a substantial share of Sweden’s adult population continues to experience weight-related health challenges. The statistics provided by the Public Health Agency of Sweden show that about 51% of adults are overweight or obese, which points to the lifestyle trends that can deter engagement in regular fitness routines. This restricts regular use of sports nutrition products by segments that would otherwise be beneficiaries.

Moreover, although physical activity is common, a significant segment of the population is inactive or exercises rarely. National surveys conducted over a long period of time indicate that approximately 13 to 15% of adults engage in sedentary leisure behaviour, which has not changed much in the last ten years. The continued lack of activity among these groups limits the transformation of general nutrition interest into regular and repeat product consumption beyond occasional trial.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Sweden Sports Nutrition Market Trend

Nutrition needs shift toward prevention, healthy ageing and mainstream dietary supplementation

Sweden, sports nutrition consumption is becoming less about younger, gym-oriented end users and more about older end users who are becoming more aware of the importance of protein in muscle maintenance and overall health. This population expansion justifies not only the performance-based nutrition but also the daily dietary supplementation in accordance with healthy ageing. The prevalence of overweight and obesity in the country of about 51% also shows that protein-enriched products are becoming a component of more comprehensive health-maintenance programs at all levels of fitness.

Simultaneously, the changing social health guidelines and eating habits are strengthening the balanced diet and sufficient protein consumption across the society. The digital access is high, with internet penetration standing at around 98.1%, which allows spreading nutritional science and wellness education quickly. As a result, sports nutrition products are still moving out of the niche fitness supplements into mainstream dietary supplements.

Sweden Sports Nutrition Market Opportunity

Expanding demand among general-health and ageing segments and rising overweight rates open new nutrition-market potential

The large percentage of adults that are overweight or obese, estimated at approximately 51%, indicates that there is a large base that can be addressed by nutrition products that are aimed at weight management, overall health and wellness, and healthy ageing as opposed to athletic performance. With the rise of preventive healthcare, brands with balanced, protein-rich formulations that are used in everyday health applications are in a good position to tap into new markets beyond the traditional sports users.

Moreover, the overall high level of physical activity in Sweden contributes to the fact that sports nutrition should be viewed as a lifestyle-oriented nutritional support and not as a purely performance-oriented supplementation. This, together with high health awareness and demographic ageing trends, provides a favourable environment to diversified product offerings to maintain muscle retention, vitality, and long-term wellbeing.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Sweden Sports Nutrition Market Segmentation Analysis

By Product Type

- Sports Protein Products

- Protein/Energy Bars

- Sports Protein Powder

- Sports Protein RTD

- Sports Non-Protein Products

The segment with highest market share under product type is Sports protein products, accounting for approximately 70% of the Sweden sports nutrition market. Protein powders, protein-based energy bars, and sports protein RTD beverages dominate consumption due to their established role in muscle recovery, performance support, and convenient snacking. Sweden’s strong gym culture and growing emphasis on preventive health further reinforce demand, supported by widespread availability across gyms, convenience stores, and grocery retailers.

Over the forecast period, protein-based products are expected to maintain their leading position as high-protein diets gain wider acceptance and end users increasingly prioritise convenience. Continued popularity of bars and RTD drinks as on-the-go meal alternatives, alongside expanding plant-based protein options aligned with vegan and natural nutrition preferences, will sustain the segment’s dominance.

By Sales Channel

- Retail Offline

- Retail Online

Retail online holds the largest share within the Sales Channel segmentation, accounting for approximately 60% of total market value. retail online dominance is driven by competitive pricing, broad product assortments, and strong appeal for bulk purchasing of protein powders and supplements. Leading brands continue to prioritise digital distribution, positioning online platforms as the primary purchasing channel for regular gym-goers and fitness-oriented end users.

Throughout the forecast period, online sales are expected to strengthen further as end users continue to value convenience, fast delivery, and transparent product comparison. While protein bars and RTD beverages maintain visibility through offline stores and fitness centres, the majority of category value is expected to flow through digital channels. The combined advantages of affordability, assortment breadth, and purchasing efficiency will ensure retail online remains the leading distribution channel in Sweden’s sports nutrition market.

List of Companies Covered in Sweden Sports Nutrition Market

The companies listed below are highly influential in the Sweden sports nutrition market, with a significant market share and a strong impact on industry developments.

- MM Sports AB

- 13:e Protein Import AB

- Nordic Sports Nutrition AB

- Barebells Functional Foods AB

- Orkla Care AB

- Midsona Sverige AB

- Better You AB

- Svenskt Kosttillskott AB

- Enervit Nutrition AB

- Mars Sverige AB

Competitive Landscape

Sweden sports nutrition market remains highly competitive, driven by strong gym culture, rising preventative-health awareness, and broad product availability across online and offline channels. The landscape is dominated by protein-focused brands, which collectively account for more than two-thirds of category value. Leading players with strong e-commerce strategies maintain a decisive advantage, as online retail represents around two-thirds of total value sales and offers competitive pricing, bulk options, and extensive assortments. Brands specialising in sports protein powder and non-protein supplements rely heavily on online distribution, while convenience channels favour bars and RTD products that appeal to on-the-go consumers. Growing competition is coming from protein-fortified packaged foods—ranging from yoghurts to snacks and bread—which attract mainstream health-focused consumers and indirectly pressure traditional sports nutrition brands. Meanwhile, the rise of plant-based and natural preferences pushes manufacturers to expand vegan portfolios, contributing to a more diverse and fragmented competitive environment.

Frequently Asked Questions

Related Report

1. Market Segmentation

1.1. Research Scope

1.2. Research Methodology

1.3. Definitions and Assumptions

2. Executive Summary

3. Sweden Sports Nutrition Market Policies, Regulations, and Standards

4. Sweden Sports Nutrition Market Dynamics

4.1. Growth Factors

4.2. Challenges

4.3. Trends

4.4. Opportunities

5. Sweden Sports Nutrition Market Statistics, 2022-2032F

5.1. Market Size & Growth Outlook

5.1.1.By Revenues in USD Million

5.2. Market Segmentation & Growth Outlook

5.2.1.By Product Type

5.2.1.1. Sports Protein Products- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.1. Protein/Energy Bars- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.2. Sports Protein Powder- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.3. Sports Protein RTD- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2. Sports Non-Protein Products- Market Insights and Forecast 2022-2032, USD Million

5.2.2.By Sales Channel

5.2.2.1. Retail Offline- Market Insights and Forecast 2022-2032, USD Million

5.2.2.2. Retail Online- Market Insights and Forecast 2022-2032, USD Million

5.2.3.By Ingredients

5.2.3.1. Vitamins and Minerals- Market Insights and Forecast 2022-2032, USD Million

5.2.3.2. Proteins and Amino Acids- Market Insights and Forecast 2022-2032, USD Million

5.2.3.3. Carbohydrates- Market Insights and Forecast 2022-2032, USD Million

5.2.3.4. Probiotics- Market Insights and Forecast 2022-2032, USD Million

5.2.3.5. Botanicals/Herbals- Market Insights and Forecast 2022-2032, USD Million

5.2.3.6. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.4.By Functionality

5.2.4.1. Energy- Market Insights and Forecast 2022-2032, USD Million

5.2.4.2. Muscle growth- Market Insights and Forecast 2022-2032, USD Million

5.2.4.3. Hydration- Market Insights and Forecast 2022-2032, USD Million

5.2.4.4. Weight Management- Market Insights and Forecast 2022-2032, USD Million

5.2.4.5. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.5.By End User

5.2.5.1. Bodybuilders- Market Insights and Forecast 2022-2032, USD Million

5.2.5.2. Athletes- Market Insights and Forecast 2022-2032, USD Million

5.2.5.3. Lifestyle Users- Market Insights and Forecast 2022-2032, USD Million

5.2.6.By Competitors

5.2.6.1. Competition Characteristics

5.2.6.2. Market Share & Analysis

6. Sweden Protein Products Sports Nutrition Market Statistics, 2022-2032F

6.1. Market Size & Growth Outlook

6.1.1.By Revenues in USD Million

6.2. Market Segmentation & Growth Outlook

6.2.1.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

6.2.2.By Ingredients- Market Insights and Forecast 2022-2032, USD Million

6.2.3.By Functionality- Market Insights and Forecast 2022-2032, USD Million

6.2.4.By End User- Market Insights and Forecast 2022-2032, USD Million

7. Sweden Non-Protein Products Sports Nutrition Market Statistics, 2022-2032F

7.1. Market Size & Growth Outlook

7.1.1.By Revenues in USD Million

7.2. Market Segmentation & Growth Outlook

7.2.1.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

7.2.2.By Ingredients- Market Insights and Forecast 2022-2032, USD Million

7.2.3.By Functionality- Market Insights and Forecast 2022-2032, USD Million

7.2.4.By End User- Market Insights and Forecast 2022-2032, USD Million

8. Competitive Outlook

8.1. Company Profiles

8.1.1.Barebells Functional Foods AB

8.1.1.1. Business Description

8.1.1.2. Product Portfolio

8.1.1.3. Collaborations & Alliances

8.1.1.4. Recent Developments

8.1.1.5. Financial Details

8.1.1.6. Others

8.1.2.Orkla Care AB

8.1.2.1. Business Description

8.1.2.2. Product Portfolio

8.1.2.3. Collaborations & Alliances

8.1.2.4. Recent Developments

8.1.2.5. Financial Details

8.1.2.6. Others

8.1.3.Midsona Sverige AB

8.1.3.1. Business Description

8.1.3.2. Product Portfolio

8.1.3.3. Collaborations & Alliances

8.1.3.4. Recent Developments

8.1.3.5. Financial Details

8.1.3.6. Others

8.1.4.Better You AB

8.1.4.1. Business Description

8.1.4.2. Product Portfolio

8.1.4.3. Collaborations & Alliances

8.1.4.4. Recent Developments

8.1.4.5. Financial Details

8.1.4.6. Others

8.1.5.Svenskt Kosttillskott AB

8.1.5.1. Business Description

8.1.5.2. Product Portfolio

8.1.5.3. Collaborations & Alliances

8.1.5.4. Recent Developments

8.1.5.5. Financial Details

8.1.5.6. Others

8.1.6.MM Sports AB

8.1.6.1. Business Description

8.1.6.2. Product Portfolio

8.1.6.3. Collaborations & Alliances

8.1.6.4. Recent Developments

8.1.6.5. Financial Details

8.1.6.6. Others

8.1.7.13:e Protein Import AB

8.1.7.1. Business Description

8.1.7.2. Product Portfolio

8.1.7.3. Collaborations & Alliances

8.1.7.4. Recent Developments

8.1.7.5. Financial Details

8.1.7.6. Others

8.1.8.Nordic Sports Nutrition AB

8.1.8.1. Business Description

8.1.8.2. Product Portfolio

8.1.8.3. Collaborations & Alliances

8.1.8.4. Recent Developments

8.1.8.5. Financial Details

8.1.8.6. Others

8.1.9.Enervit Nutrition AB

8.1.9.1. Business Description

8.1.9.2. Product Portfolio

8.1.9.3. Collaborations & Alliances

8.1.9.4. Recent Developments

8.1.9.5. Financial Details

8.1.9.6. Others

8.1.10. Mars Sverige AB

8.1.10.1. Business Description

8.1.10.2. Product Portfolio

8.1.10.3. Collaborations & Alliances

8.1.10.4. Recent Developments

8.1.10.5. Financial Details

8.1.10.6. Others

9. Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Product Type |

|

| By Sales Channel |

|

| By Ingredients |

|

| By Functionality |

|

| By End User |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.