Spain Sports Nutrition Market Report: Trends, Growth and Forecast (2026-2032)

By Product Type (Sports Protein Products (Protein/Energy Bars, Sports Protein Powder, Sports Protein RTD), Sports Non-Protein Products), By Sales Channel (Retail Offline, Retail Online), By Ingredients (Vitamins and Minerals, Proteins and Amino Acids, Carbohydrates, Probiotics, Botanicals/Herbals, Others), By Functionality (Energy, Muscle growth, Hydration, Weight Management, Others), By End User (Bodybuilders, Athletes, Lifestyle Users) ... Read more

|

Major Players

|

Spain Sports Nutrition Market Statistics and Insights, 2026

- Market Size Statistics

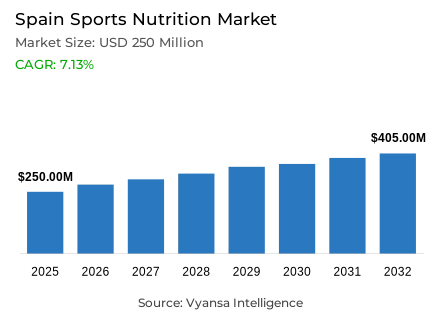

- Sports nutrition market size in Spain was estimated at USD 250 million in 2025.

- The market size is expected to grow to USD 405 million by 2032.

- Market to register a CAGR of around 7.13% during 2026-32.

- Product Type Shares

- Sports protein products grabbed market share of 65%.

- Competition

- More than 20 companies are actively engaged in producing sports nutrition in Spain.

- Top 5 companies acquired around 40% of the market share.

- Onsalesit SA, Laston Red SL, Herbalife International de España SA, The Hut.com Ltd, Nutrisport SA etc., are few of the top companies.

- Sales Channel

- Retail online grabbed 55% of the market.

Spain Sports Nutrition Market Outlook

The Spain sports nutrition market will grow steadily throughout the forecast period, increasing by USD 250 million in 2025 to USD 405 million in 2032, thus representing a compound annual growth rate of about 7.13%. This growth is largely supported by the fact that the number of health-conscious end users in Spain is on the rise, as sports nutrition products are gradually losing their image of being linked to athletes and gym-oriented people. As physical activity continues to become more and more widespread, with the number of people engaging in it remaining consistently high according to national surveys, sports nutrition is being viewed as a part of a healthy lifestyle. This development is likely to keep benefiting sports protein products, which already occupy 65% of the market share, and at the same time open up the prospects of newer formats and flavour innovations that are being launched by international and domestic brands.

It is expected that product innovation will be one of the key growth drivers during the forecast period. Following the success of products like NutrisportZero desserts and Foodspring flavoured whey product lines, manufacturers are likely to extend their diversification beyond traditional powder products. The growing popularity of protein-enriched products and crossover items will probably increase the intensity of competition, forcing brands to distinguish themselves by providing greater convenience and better taste profiles. The introduction of international players like Barebells, and the competitively priced local brands will add to the more dynamic and diversified competitive environment.

Future demand is also likely to be influenced by demographic growth, especially in women. With the increased visibility of women health and wellness in the Spanish media and online, more female-focused formulations related to nutrition, strength, and overall wellbeing are likely to be launched by the companies. The category is already being broadened in terms of demographic appeal through influencers like Helena Rodero and Marian Garcia Martinez who are already promoting more awareness about supplements and health education.

Retail online sales that are already 55% of the overall market value are likely to be the dominant sales channel as end users still value convenience, product variety, and price competitiveness. Concurrently, the availability will be improved by the allocation of more shelf space by grocery retailers. The Spain sports nutrition market is set to enter a strong and vibrant growth cycle by 2032, supported by a long-term history of product innovation, increasing health awareness, and a growing base of end-users.

Spain Sports Nutrition Market Growth Driver

Rising health engagement and wider exercise participation accelerate adoption of sports nutrition

The increasing interest in health, wellness, and regular exercise is further broadening the range of products that can be addressed by sports nutrition in Spain. The Centro de Investigaciones Sociologicas (CIS) reported that 37.7% of adults engage in regular physical activity in their leisure time, which is a significant proportion of the population that is increasingly adopting functional nutrition to supplement physical activities. This trend is consistent with the larger European trends, with the Eurobarometer Sport and Physical Activity Survey indicating that 38% of EU citizens exercise at least once a week. All these indicators reinforce the baseline demand of sports nutrition products.

With the growing integration of physical activity into everyday lifestyle practices, the use of protein powders, ready-to-drink shakes, and fortified bars is no longer limited to professional athletes but is also being adopted by the mainstream end user. Grocery retailers, in turn, have increased the shelf space of sports nutrition products, and online stores are gaining more and more loyal customers who want convenience and diversity. The correlation between the increased exercise attendance and the increased awareness of the wellness is the foundation of the long-term growth of the category.

Spain Sports Nutrition Market Challenge

High inactivity levels and rising overweight prevalence limit regular usage and slow market conversion

Market growth is limited by the uneven profile of physical activity participation in Spain despite the favourable growth dynamics. According to the CIS data, 52% of the population is not involved in any sport or exercise, which means that there is a large inactive group that restricts the repetitive use of performance-based nutrition products. This limited participation base slows the shift between infrequent trial to regular use, especially in demographics with infrequent fitness habits, leading to demand concentration among moderately to highly active people.

Market restrictions are also influenced by health and nutrition indicators. According to the Spanish Ministry of Health, 36% of the adult population is overweight, and 14% are obese, which is a result of dietary habits that cannot be overcome by sports nutrition products alone. These conditions can arouse interest in healthier lifestyles, but they also decrease the chances of long-term engagement in organized physical activity. Combined, the high levels of inactivity and high levels of overweight form a structural limitation to long-term penetration of categories.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Spain Sports Nutrition Market Trend

Protein fortification and innovative product formats broaden usage across mainstream consumer groups

The sports nutrition in Spain is increasingly being transformed by product diversification and fortification of proteins. On the European front, the Eurobarometer survey indicates that 44% of adults are taking at least 10 minutes of aerobic activity per week, which supports the need to have protein enrichment available in beverages, snacks, and dairy-alternative forms. At the same time, CIS data indicate that more than 52% of Spaniards are not physically active, which indicates that low-intensity and introductory functional nutrition products targeting lifestyle users, and not performance athletes, have a demand potential. Brand innovation strategies are being affected by this duality.

Manufacturers are reacting by increasing flavour profiles, plant-based protein formulations, and dessert-inspired products that attract end users who want to indulge and benefit their health. Packaged foods that are fortified with proteins, such as bars, yoghurts, and confectionery, still blur the traditional category lines. This differentiation serves the needs of performance-oriented end users and casual end users who want convenience in their functions, thus expanding the market base.

Spain Sports Nutrition Market Opportunity

Female-focused innovation and digital activation unlock new demographic and behavioural segments

Expanding participation of women in fitness and wellness activities is expected to create meaningful growth avenues for the sports nutrition market, as the category increasingly evolves away from its historically male-centric positioning and appeals to a more diverse end-user base. The CIS shows that 35.7% of women are physically active on a regular basis, as opposed to 39.7% of men, which means that there is a solid female base of participation with potential to expand. The trend is supported by the growing presence of women health and nutrition-related information on digital platforms, with influencers and qualified nutritionists actively influencing the awareness of supplements among all age groups. Specialized formulations such as collagen blends, lower-sugar versions, and hormone-supportive nutrients are in a good position to meet these requirements.

This opportunity is further enhanced by digital accessibility. The national ICT survey of Spain indicates that internet penetration among people aged 16–74 is over 96%, which allows conducting social commerce, influencer-based education, and omnichannel product releases. Through the convergence of female-oriented innovation with digital activation tactics and selective in-store interaction, brands will gain the ability to increase penetration among occasional exercisers and reinforce loyalty among current users.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Spain Sports Nutrition Market Segmentation Analysis

By Product Type

- Sports Protein Products

- Protein/Energy Bars

- Sports Protein Powder

- Sports Protein RTD

- Sports Non-Protein Products

The segment with highest market share under Product Type is Sports protein products, representing approximately 65% of the Spain sports nutrition market. This dominance reflects the country’s expanding health-focused population and growing interest in protein-rich diets among both active adults and lifestyle-oriented exercisers. According to the Spanish Ministry of Culture and Sports, more than 48% of Spaniards participated in weekly sports activity in 2023, signalling sustained growth in fitness engagement. This expanding active population continues to drive demand for protein powders, shakes, and bars that support muscle maintenance and recovery.

Over the forecast period, sports protein products are expected to retain their leading position as participation in physical activity continues to rise. Data from the Spanish National Health Survey (INE) indicate increasing adoption of daily exercise, supported by improved awareness around diet quality and protein intake among both men and women. Continued innovation in flavour profiles, convenient formats, and plant-based alternatives will further reinforce the segment’s role as the primary growth engine of the market.

By Sales Channel

- Retail Offline

- Retail Online

Retail online represents the largest share within the Sales Channel segmentation, accounting for approximately 55% of total market value. This leadership is driven by competitive pricing, extensive product assortments, and high levels of end user confidence in digital purchasing. The Spanish National Observatory of Telecommunications (ONTSI) reports that 77% of Spaniards made online purchases in 2023, reflecting one of the highest retail online penetration rates in Europe. This digital maturity particularly supports online sales of bulk products such as protein powders and multi-pack supplements.

Retail online is expected to continue expanding over the forecast period as end users increasingly rely on digital platforms for health and nutrition purchases. The European Commission’s Digital Economy and Society Index (DESI) highlights Spain’s strong digital infrastructure and rapid growth in online retail activity. Subscription models, influencer-led discovery, and direct-to-end user strategies are anticipated to further reinforce online channel dominance, ensuring retail online remains the primary distribution route for sports nutrition products.

List of Companies Covered in Spain Sports Nutrition Market

The companies listed below are highly influential in the Spain sports nutrition market, with a significant market share and a strong impact on industry developments.

- Onsalesit SA

- Laston Red SL

- Herbalife International de España SA

- The Hut.com Ltd

- Nutrisport SA

- Weider Nutrition SL

- Decathlon España SA

- Nutrition & Sante Iberia SL

- Enervit Nutrition SL

- LargeLife Ltd

Competitive Landscape

Spain sports nutrition market remains highly competitive and increasingly fragmented as both global and local players expand aggressively to capture a rapidly widening consumer base. Myprotein (The Hut.com Ltd) sustains a clear leadership position as the only brand with a double-digit share, supported by continual flavour innovations and strong online penetration. Nutrisport strengthens its position with new lines such as NutrisportZero, appealing to mainstream consumers through desserts and ready-to-drink formats. Sporting retailer Decathlon competes via its Aptonia line, though its share has slightly eroded amid intensifying rivalry. Brands such as Foodspring, Prozis, and emerging local names like Delinuts and Glorioso contribute to growing fragmentation, leveraging premium flavours, accessible pricing, and presence in major retailers like El Corte Inglés. Meanwhile, international entrants such as Barebells continue to gain traction with high-protein bars and shakes, pushing the competitive landscape toward more diverse formats, broader positioning, and stronger category innovation.

Frequently Asked Questions

Related Report

1. Market Segmentation

1.1. Research Scope

1.2. Research Methodology

1.3. Definitions and Assumptions

2. Executive Summary

3. Spain Sports Nutrition Market Policies, Regulations, and Standards

4. Spain Sports Nutrition Market Dynamics

4.1. Growth Factors

4.2. Challenges

4.3. Trends

4.4. Opportunities

5. Spain Sports Nutrition Market Statistics, 2022-2032F

5.1. Market Size & Growth Outlook

5.1.1.By Revenues in USD Million

5.2. Market Segmentation & Growth Outlook

5.2.1.By Product Type

5.2.1.1. Sports Protein Products- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.1. Protein/Energy Bars- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.2. Sports Protein Powder- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.3. Sports Protein RTD- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2. Sports Non-Protein Products- Market Insights and Forecast 2022-2032, USD Million

5.2.2.By Sales Channel

5.2.2.1. Retail Offline- Market Insights and Forecast 2022-2032, USD Million

5.2.2.2. Retail Online- Market Insights and Forecast 2022-2032, USD Million

5.2.3.By Ingredients

5.2.3.1. Vitamins and Minerals- Market Insights and Forecast 2022-2032, USD Million

5.2.3.2. Proteins and Amino Acids- Market Insights and Forecast 2022-2032, USD Million

5.2.3.3. Carbohydrates- Market Insights and Forecast 2022-2032, USD Million

5.2.3.4. Probiotics- Market Insights and Forecast 2022-2032, USD Million

5.2.3.5. Botanicals/Herbals- Market Insights and Forecast 2022-2032, USD Million

5.2.3.6. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.4.By Functionality

5.2.4.1. Energy- Market Insights and Forecast 2022-2032, USD Million

5.2.4.2. Muscle growth- Market Insights and Forecast 2022-2032, USD Million

5.2.4.3. Hydration- Market Insights and Forecast 2022-2032, USD Million

5.2.4.4. Weight Management- Market Insights and Forecast 2022-2032, USD Million

5.2.4.5. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.5.By End User

5.2.5.1. Bodybuilders- Market Insights and Forecast 2022-2032, USD Million

5.2.5.2. Athletes- Market Insights and Forecast 2022-2032, USD Million

5.2.5.3. Lifestyle Users- Market Insights and Forecast 2022-2032, USD Million

5.2.6.By Competitors

5.2.6.1. Competition Characteristics

5.2.6.2. Market Share & Analysis

6. Spain Protein Products Sports Nutrition Market Statistics, 2022-2032F

6.1. Market Size & Growth Outlook

6.1.1.By Revenues in USD Million

6.2. Market Segmentation & Growth Outlook

6.2.1.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

6.2.2.By Ingredients- Market Insights and Forecast 2022-2032, USD Million

6.2.3.By Functionality- Market Insights and Forecast 2022-2032, USD Million

6.2.4.By End User- Market Insights and Forecast 2022-2032, USD Million

7. Spain Non-Protein Products Sports Nutrition Market Statistics, 2022-2032F

7.1. Market Size & Growth Outlook

7.1.1.By Revenues in USD Million

7.2. Market Segmentation & Growth Outlook

7.2.1.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

7.2.2.By Ingredients- Market Insights and Forecast 2022-2032, USD Million

7.2.3.By Functionality- Market Insights and Forecast 2022-2032, USD Million

7.2.4.By End User- Market Insights and Forecast 2022-2032, USD Million

8. Competitive Outlook

8.1. Company Profiles

8.1.1.Hut.com Ltd, The

8.1.1.1. Business Description

8.1.1.2. Product Portfolio

8.1.1.3. Collaborations & Alliances

8.1.1.4. Recent Developments

8.1.1.5. Financial Details

8.1.1.6. Others

8.1.2.Nutrisport SA

8.1.2.1. Business Description

8.1.2.2. Product Portfolio

8.1.2.3. Collaborations & Alliances

8.1.2.4. Recent Developments

8.1.2.5. Financial Details

8.1.2.6. Others

8.1.3.Weider Nutrition SL

8.1.3.1. Business Description

8.1.3.2. Product Portfolio

8.1.3.3. Collaborations & Alliances

8.1.3.4. Recent Developments

8.1.3.5. Financial Details

8.1.3.6. Others

8.1.4.Decathlon España SA

8.1.4.1. Business Description

8.1.4.2. Product Portfolio

8.1.4.3. Collaborations & Alliances

8.1.4.4. Recent Developments

8.1.4.5. Financial Details

8.1.4.6. Others

8.1.5.Nutrition & Sante Iberia SL

8.1.5.1. Business Description

8.1.5.2. Product Portfolio

8.1.5.3. Collaborations & Alliances

8.1.5.4. Recent Developments

8.1.5.5. Financial Details

8.1.5.6. Others

8.1.6.Onsalesit SA

8.1.6.1. Business Description

8.1.6.2. Product Portfolio

8.1.6.3. Collaborations & Alliances

8.1.6.4. Recent Developments

8.1.6.5. Financial Details

8.1.6.6. Others

8.1.7.Laston Red SL

8.1.7.1. Business Description

8.1.7.2. Product Portfolio

8.1.7.3. Collaborations & Alliances

8.1.7.4. Recent Developments

8.1.7.5. Financial Details

8.1.7.6. Others

8.1.8.Herbalife International de España SA

8.1.8.1. Business Description

8.1.8.2. Product Portfolio

8.1.8.3. Collaborations & Alliances

8.1.8.4. Recent Developments

8.1.8.5. Financial Details

8.1.8.6. Others

8.1.9.Enervit Nutrition SL

8.1.9.1. Business Description

8.1.9.2. Product Portfolio

8.1.9.3. Collaborations & Alliances

8.1.9.4. Recent Developments

8.1.9.5. Financial Details

8.1.9.6. Others

8.1.10. LargeLife Ltd

8.1.10.1. Business Description

8.1.10.2. Product Portfolio

8.1.10.3. Collaborations & Alliances

8.1.10.4. Recent Developments

8.1.10.5. Financial Details

8.1.10.6. Others

9. Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Product Type |

|

| By Sales Channel |

|

| By Ingredients |

|

| By Functionality |

|

| By End User |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.