Spain Industrial Gases Market Report: Trends, Growth and Forecast (2026-2032)

By Gas Type (Nitrogen Gas, Oxygen Gas, Carbon Dioxide Gas, Argon Gas, Helium Gas, Hydrogen Gas, Other), By Supply Mode (Cylinders, Bulk, On-Site Production, Captive, Other), By Application (Combustion and Process Oxygen, Welding and Metal Fabrication, Inerting Blanketing and Heat Treating, Cryogenics and liquefaction, Chemical Synthesis and Hydrogenation, Purging and Purifications, Analytical and Calibration), By End User Industry (General Manufacturing, Food, Metallurgy, Chemicals, Healthcare, Electronics, Refining & Energy, Glass, Pulp & Paper, Others) ... Read more

|

Major Players

|

Spain Industrial Gases Market Statistics and Insights, 2026

- Market Size Statistics

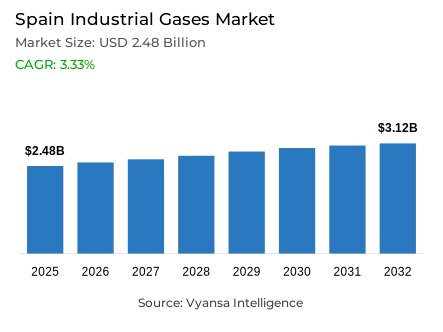

- Industrial gases in Spain is estimated at USD 2.48 billion in 2025.

- The market size is expected to grow to USD 3.12 billion by 2032.

- Market to register a cagr of around 3.33% during 2026-32.

- Gas Type Shares

- Oxygen gas grabbed market share of 40%.

- Competition

- More than 10 companies are actively engaged in producing industrial gases in Spain.

- Top 5 companies acquired around 75% of the market share.

- SOL España; Calvera Industrial Gases; Primagas Energía SA; Linde; Air Liquide etc., are few of the top companies.

- Supply Mode

- Cylinders grabbed 40% of the market.

Spain Industrial Gases Market Outlook

The Spain industrial gases market will grow from $2.48 billion in 2025 to $3.12 billion by 2032, at a CAGR of approximately 3.33% during the period 2026-2032. This steady growth is due to the robust demand for industrial and medical gases. Currently, the elderly population and prevalence of chronic respiratory diseases with over 3 million COPD patients have fueled the consumption of medical oxygen in the country. Many Spanish hospitals in regions like Catalonia, Andalusia, and Valencia have steadily adopted the oxygen-production process based on the Pressure Swing Adsorption technology on-site.

Industrial demand also contributes significantly, especially from the chemical and pharmaceutical industry, where consumption of gas stood at 61 GWh/d in May 2025. The automobile industry, employing more than 57,189 persons, is also gas-dependent, especially for its use in welding and precision fabrication. This demands a stable level of consumption throughout the period leading up to 2032. Oxygen gas leads the market, accounting for a dominating share of 40%. Nevertheless, it faces the challenge of pressures from the fast-track decarbonization strategy adopted by Spain in its updated PNIEC strategy.

The reduction of carbon emissions and the EU regulations imposed stringent spending for the manufacturing industry, especially when the chemicals industry requires an average of €3 billion investments until 2050 to update and modernize. The swift development in the green hydrogen segment enhances the future potential further. Plans in Spain target the installation of 12 GW of electrolyzers in the country by 2030, while the production target for green hydrogen is pegged at 2.5 Mtpa, receiving significant EU government subsidies.

Geographies including Catalonia, Tarragona, and the Andalusia region are emerging as prime locations for hydrogen, chemicals, and advanced industries. In the supply chain category, the cylinder segment presently leads the market, comprising 40%, due to its prevalence, albeit changing to larger or in-house solutions in the large industry space.

Spain Industrial Gases Market Growth DriverExpanding Healthcare Utilization and Manufacturing Demand

The country’s increasing healthcare needs and robust manufacturing sector form a supportive environment. The growing aged population in Spain and high incidence rates of chronic respiratory diseases, with over 3 million people suffering from COPD, continue to push huge volumes of medical oxygen consumption in hospitals and healthcare institutions. Advanced healthcare facilities in provinces such as Catalonia, Andalusia, and Valencia are increasingly turning to in situ PSA-based oxygen generators as independent sources in emergency situations.

Industrial demand is also equally strong, supported by the chemical and pharmaceutical industry in Spain, which registered 61 GWh of gas demand in May 2025. The automobile manufacturing industry, employing 57,189 workers and ranking second among European producers, also heavily depends on industrial gases. Thus, the overall dependence of the healthcare industry coupled with the automobile industry ensures robust market growth till 2032.

Spain Industrial Gases Market ChallengeIntensifying Regulatory Compliance and Decarbonization Pressures

The market is facing significant restraints as Spain is speeding up its nationwide de-carbonization plan due to Spain’s revised Integrated National Energy and Climate Plan (PNIEC). Spain is aiming to reduce greenhouse gas emissions by 32% by 2030 compared to 1990 levels, along with attaining climate neutrality by 2050, keeping a substantial compliance burden on the producers of industrial gases. The Industrial Pollution Prevention & Control (IPPC) Directive of the EU is adding pressing restrictions by strictly imposing limits on combustion process gases, such as nitrogen oxide (N2O) emissions.

The compliance with these regulations calls for heavy investments in capital, especially because the Spanish chemical industry requires around €3 billion per year from now until 2050 to adapt to the new scenario of modernization and decarbonization of the industry. Of this, €1.7 billion focuses on the construction of new plants, which presents a heavy burden for the industry as a whole, especially the suppliers of industrial gas who will now be forced to abandon the use of fossil fuels to produce hydrogen.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Spain Industrial Gases Market TrendRapid Expansion of Green Hydrogen and Energy Transition Pathways

Spain is going through a structural change because of the quick pace of green hydrogen technology development, thus changing demand structures in the Spain industrial gases market. Spain is poised to become Europe's hydrogen leader because of the government's approval of a 12GW electrolyzer capacity plan by 2030, a three-fold increase from the previous plan of 4GW. Spain, with 20% of Europe's announced electrolysis capacity, is also set to produce 25% of global green hydrogen by 2030.

Projections peg the expectation for Spanish green hydrogen production capacity at 2.5 Mtpa in the year 2030, with the first being utilized within the domestic industries and the remaining for export. The European Union has further supported this expected trajectory with an allocation of €794 million for seven large-scale projects with an aggregated capacity of 650 MW along with another allocation of €1.2 billion for the development of the hydrogen infrastructure.

Spain Industrial Gases Market OpportunityExpanding Potential in Decarbonizing Industrial and Petrochemical Hubs

Spain has highly industrialized areas that offer a focused market for the suppliers of those involved in the decarbonization plans and gas processes. Catalonia is responsible for the production of 41.4% of Spain’s chemical production, and Tarragona, which accounts for 25% of the total chemical production in Spain and 20 million metric tons per year of that national production, remains one of the biggest petrochemical sites in Southern Europe.

Further expansion comes from Andalusia, with a Green Hydrogen Roadmap to build out 3.7GW of electrolysis capacity, or 33% of Spain’s national plan. With more than 150 actors taking part in the Andalusian Hydrogen Alliance, a regional hub for decarbonization is taking shape. At the same time, Spain’s car industry employment base and its food and beverages industry cover a vast market for industrial gases used in processing, preservation, metalwork, and adaptation to emerging sustainability norms.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Spain Industrial Gases Market Segmentation Analysis

By Gas Type

- Nitrogen Gas

- Oxygen Gas

- Carbon Dioxide Gas

- Argon Gas

- Helium Gas

- Hydrogen Gas

- Other

Oxygen holds the highest market share in the Spain industrial gases market, accounting for approximately 40% of total demand, reflecting its indispensable role across medical, industrial, and chemical processes. Healthcare institutions depend heavily on medical oxygen due to Spain’s aging population and widespread chronic respiratory conditions, especially COPD affecting over 3 million individuals. Consistent therapeutic usage, increased preparedness after recent health crises, and expanded PSA-based on-site generation capabilities reinforce oxygen’s dominant position.

Industrial demand further strengthens oxygen’s leadership, particularly across metal fabrication, petrochemical refining, and pharmaceutical applications. Spain’s automotive industry—supported by 57,189 direct employees and an extensive network of manufacturing plants—relies on oxygen for precision cutting and welding operations. The pharmaceutical sector also utilizes oxygen extensively for sterilization and controlled-environment production cycles, contributing to stable, multisectoral demand that maintains oxygen as the leading gas type.

By Supply Mode

- Cylinders

- Bulk

- On-Site Production

- Captive

- Other

The cylinder supply mode commands the largest share of the Spain industrial gases market, accounting for 40% of total supply volume due to its accessibility, flexibility, and suitability for small and medium-sized enterprises. Spain’s industrial landscape, characterized by numerous SMEs in welding, fabrication, and maintenance services, benefits from portable cylinders that support non-continuous or mobile work environments. Healthcare centers in semi-urban and rural regions also depend on cylinder-based medical oxygen for emergency backup systems and portable care equipment.

The prevalence of cylinder distribution is closely tied to Spain’s decentralized manufacturing footprint, where businesses require cost-efficient solutions without investment in permanent infrastructure. While cylinder demand remains strong, larger petrochemical hubs in Tarragona and high-volume automotive facilities are increasingly shifting toward bulk liquid supply and on-site generation to improve cost efficiency and ensure uninterrupted availability. This parallel transition is creating a balanced and evolving supply landscape across the country.

List of Companies Covered in Spain Industrial Gases Market

The companies listed below are highly influential in the Spain industrial gases market, with a significant market share and a strong impact on industry developments.

- SOL España

- Calvera Industrial Gases

- Primagas Energía SA

- Linde

- Air Liquide

- Air Products

- Carburos Metálicos S.A.

- Messer Ibérica de Gases S.A.

- CMC Cerezuela

- Ibergass Technologies S.L.U.

Market News & Updates

- Air Liquide, 2025:

Air Liquide won a major five-year contract in September 2025 from the Community of Madrid to provide home-based respiratory care. The contract supports around 70,000 patients with COPD and sleep apnea. The company will supply medical oxygen, equipment, remote monitoring tools, patient education, and teleconsultation services. Its proposal was selected because it uses advanced digital tools such as predictive algorithms and artificial intelligence to improve patient outcomes and reduce healthcare system costs.

- Primagas Energía SA, 2025:

Primagas continues to expand the use of biopropane in Spain, an alternative fuel that can reduce carbon emissions by up to 80% compared with traditional propane. The company operates major storage facilities in Barcelona, Zaragoza, and Segovia, supporting households and industries across the country. Primagas is part of the global SHV Energy group, active in more than 20 countries. Its offerings include Autogas, LNG alternatives, and specialized gas equipment, helping Spain progress toward its clean-energy goals.

Frequently Asked Questions

Related Report

1. Market Segmentation

1.1. Research Scope

1.2. Research Methodology

1.3. Definitions and Assumptions

2. Executive Summary

3. Spain Industrial Gases Market Policies, Regulations, and Standards

4. Spain Industrial Gases Market Dynamics

4.1. Growth Factors

4.2. Challenges

4.3. Trends

4.4. Opportunities

5. Spain Industrial Gases Market Statistics, 2022-2032F

5.1. Market Size & Growth Outlook

5.1.1.By Revenues in USD Million

5.1.2.By Quantity Sold in Tons

5.2. Market Segmentation & Growth Outlook

5.2.1.By Gas Type

5.2.1.1. Nitrogen Gas- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

5.2.1.2. Oxygen Gas- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

5.2.1.3. Carbon Dioxide Gas- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

5.2.1.4. Argon Gas- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

5.2.1.5. Helium Gas- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

5.2.1.6. Hydrogen Gas- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

5.2.1.7. Other- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

5.2.2.By Supply Mode

5.2.2.1. Cylinders- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

5.2.2.2. Bulk- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

5.2.2.3. On-Site Production- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

5.2.2.4. Captive- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

5.2.2.5. Other- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

5.2.3.By Application

5.2.3.1. Combustion and Process Oxygen- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

5.2.3.2. Welding and Metal Fabrication- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

5.2.3.3. Inerting Blanketing and Heat Treating- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

5.2.3.4. Cryogenics and liquefaction- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

5.2.3.5. Chemical Synthesis and Hydrogenation- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

5.2.3.6. Purging and Purifications- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

5.2.3.7. Analytical and Calibration- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

5.2.4.By End User Industry

5.2.4.1. General Manufacturing- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

5.2.4.2. Food- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

5.2.4.3. Metallurgy- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

5.2.4.4. Chemicals- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

5.2.4.5. Healthcare- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

5.2.4.6. Electronics- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

5.2.4.7. Refining & Energy- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

5.2.4.8. Glass- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

5.2.4.9. Pulp & Paper- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

5.2.4.10. Others- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

5.2.5.By Competitors

5.2.5.1. Competition Characteristics

5.2.5.2. Market Share & Analysis

6. Spain Nitrogen Gas Market Statistics, 2022-2032

6.1. Market Size & Growth Outlook

6.1.1.By Revenues in USD Million

6.1.2.By Quantity Sold in Tons

6.2. Market Segmentation & Growth Outlook

6.2.1.By Supply Mode- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

6.2.2.By Application- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

6.2.3.By End User Industry- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

7. Spain Oxygen Gas Market Statistics, 2022-2032

7.1. Market Size & Growth Outlook

7.1.1.By Revenues in USD Million

7.1.2.By Quantity Sold in Tons

7.2. Market Segmentation & Growth Outlook

7.2.1.By Supply Mode- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

7.2.2.By Application- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

7.2.3.By End User Industry- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

8. Spain Carbon Dioxide Gas Market Statistics, 2022-2032

8.1. Market Size & Growth Outlook

8.1.1.By Revenues in USD Million

8.1.2.By Quantity Sold in Tons

8.2. Market Segmentation & Growth Outlook

8.2.1.By Supply Mode- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

8.2.2.By Application- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

8.2.3.By End User Industry- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

9. Spain Argon Gas Market Statistics, 2022-2032

9.1. Market Size & Growth Outlook

9.1.1.By Revenues in USD Million

9.1.2.By Quantity Sold in Tons

9.2. Market Segmentation & Growth Outlook

9.2.1.By Supply Mode- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

9.2.2.By Application- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

9.2.3.By End User Industry- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

10. Spain Helium Gas Market Statistics, 2022-2032

10.1. Market Size & Growth Outlook

10.1.1. By Revenues in USD Million

10.1.2. By Quantity Sold in Tons

10.2. Market Segmentation & Growth Outlook

10.2.1. By Supply Mode- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

10.2.2. By Application- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

10.2.3. By End User Industry- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

11. Spain Hydrogen Gas Market Statistics, 2022-2032

11.1. Market Size & Growth Outlook

11.1.1. By Revenues in USD Million

11.1.2. By Quantity Sold in Tons

11.2. Market Segmentation & Growth Outlook

11.2.1. By Supply Mode- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

11.2.2. By Application- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

11.2.3. By End User Industry- Market Insights and Forecast 2022-2032, USD Million & Quantity in Tons

12. Competitive Outlook

12.1. Company Profiles

12.1.1. Linde

12.1.1.1. Business Description

12.1.1.2. Product Portfolio

12.1.1.3. Collaborations & Alliances

12.1.1.4. Recent Developments

12.1.1.5. Financial Details

12.1.1.6. Others

12.1.2. Air Liquide

12.1.2.1. Business Description

12.1.2.2. Product Portfolio

12.1.2.3. Collaborations & Alliances

12.1.2.4. Recent Developments

12.1.2.5. Financial Details

12.1.2.6. Others

12.1.3. Air Products

12.1.3.1. Business Description

12.1.3.2. Product Portfolio

12.1.3.3. Collaborations & Alliances

12.1.3.4. Recent Developments

12.1.3.5. Financial Details

12.1.3.6. Others

12.1.4. Carburos Metálicos S.A.

12.1.4.1. Business Description

12.1.4.2. Product Portfolio

12.1.4.3. Collaborations & Alliances

12.1.4.4. Recent Developments

12.1.4.5. Financial Details

12.1.4.6. Others

12.1.5. Messer Ibérica de Gases S.A.

12.1.5.1. Business Description

12.1.5.2. Product Portfolio

12.1.5.3. Collaborations & Alliances

12.1.5.4. Recent Developments

12.1.5.5. Financial Details

12.1.5.6. Others

12.1.6. SOL España

12.1.6.1. Business Description

12.1.6.2. Product Portfolio

12.1.6.3. Collaborations & Alliances

12.1.6.4. Recent Developments

12.1.6.5. Financial Details

12.1.6.6. Others

12.1.7. Calvera Industrial Gases

12.1.7.1. Business Description

12.1.7.2. Product Portfolio

12.1.7.3. Collaborations & Alliances

12.1.7.4. Recent Developments

12.1.7.5. Financial Details

12.1.7.6. Others

12.1.8. Primagas Energía SA

12.1.8.1. Business Description

12.1.8.2. Product Portfolio

12.1.8.3. Collaborations & Alliances

12.1.8.4. Recent Developments

12.1.8.5. Financial Details

12.1.8.6. Others

12.1.9. CMC Cerezuela

12.1.9.1. Business Description

12.1.9.2. Product Portfolio

12.1.9.3. Collaborations & Alliances

12.1.9.4. Recent Developments

12.1.9.5. Financial Details

12.1.9.6. Others

12.1.10. Ibergass Technologies S.L.U.

12.1.10.1.Business Description

12.1.10.2.Product Portfolio

12.1.10.3.Collaborations & Alliances

12.1.10.4.Recent Developments

12.1.10.5.Financial Details

12.1.10.6.Others

13. Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Gas Type |

|

| By Supply Mode |

|

| By Application |

|

| By End User Industry |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.