Spain Bottled Water Market Report: Trends, Growth and Forecast (2026-2032)

By Type of Water (Carbonated Bottled Water, Flavoured Bottled Water, Functional Bottled Water, Still Bottled Water), By Sub Types (Purified (Desalinated, Atmospheric Generated, Others), Mineral, Other (Spring, Alkaline, Other)), By Packaging Material (Flexible Packaging (Aluminium, Pouches), Glass, Rigid Plastic (PET Bottles, Thin Wall Plastic Containers, Others)), By Price Category (Budget, Economy, Premium), By Pack Size (100 ml, 125 ml, 200 ml, 250 ml, 330 ml, 370 ml, 450 ml, 500 ml, 591 ml, 750 ml, 1,000 ml, 1,500 ml, 4,000 ml, 5,000 ml, Others), By Sales Channel (On Trade (Restaurants, Hotels, Cafes, Others), Off Trade (Grocery Retailers (Convenience Retail, Supermarkets, Hypermarkets, Small Local Grocer), Non-Grocery Retailers (General Merchandise Stores, Health and Beauty Specialists), Vending, E-commerce)) ... Read more

|

Major Players

|

Spain Bottled Water Market Statistics and Insights, 2026

- Market Size Statistics

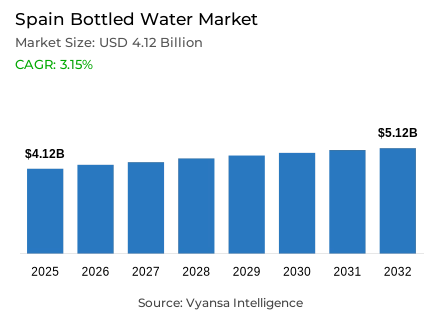

- Bottled water market size in Spain was estimated at USD 4.12 billion in 2025.

- The market size is expected to grow to USD 5.12 billion by 2032.

- Market to register a CAGR of around 3.15% during 2026-32.

- Type of Water Shares

- Still bottled water grabbed market share of 90%.

- Competition

- Bottled water in Spain is currently being catered to by more than 20 companies.

- Top 5 companies acquired around 35% of the market share.

- Nestlé Waters España SA, Balneario y Aguas de Solán de Cabras SA, Centros Comerciales Carrefour SA, Mercadona SA, Aguas Danone SA etc., are few of the top companies.

- Sales Channel

- Off trade grabbed 80% of the market.

Spain Bottled Water Market Outlook

In 2025, the bottled water market in Spain is valued at USD 4.12 billion and is projected to grow to USD 5.12 billion by 2032, with a CAGR of about 3.15%. Tourism, with 96.8 million international visitors in 2025, remains a source of regular impulse buying in cafés and transport stations. Furthermore, rising temperatures-2023 being the second warmest year, with an average of 15.2°C-keep hydration demand steady across both small formats and large packs.

The market is still dominated by bottled water, which holds a 90% market share due to its role in daily hydration and home consumption. However, increasing health awareness is shifting consumer preference toward sparkling and functional waters. With 15.2% of adults living with obesity, demand for low-sugar, better-for-you options continues to rise. Manufacturers are expanding portfolios with vitamin-enriched and low-calorie products that compete on functionality rather than simple hydration.

The primary distribution channel is off-trade, accounting for 80% of total market sales. Supermarkets continue to support bulk purchasing, while online shopping increasingly influences consumer behaviour. In 2025, 59.6% of residents make online purchases, creating opportunities for home delivery and subscription services focused on multi-packs. Digital platforms also allow brands to communicate sustainability initiatives and execute targeted promotions beyond traditional shelf displays.

Despite growth prospects, the category faces ongoing pressure linked to plastic waste. The 41.3% collection rate for single-use plastic bottles in 2023 heightens expectations on producers to improve recyclability and circularity. In a highly price-competitive market, these packaging-related costs can squeeze margins, forcing brands to carefully balance environmental compliance with efficient, economical logistics.

Spain Bottled Water Market Growth Driver

Tourism and Heat Reinforce Hydration Occasions

Spain’s strong visitor flows keep bottled water highly visible in travel and leisure settings, supporting frequent impulse purchases in cafés, restaurants, and convenience outlets. Official FRONTUR results show Spain receives 96.8 million international tourists in 2025, sustaining high footfall across hospitality and transport nodes where single‑serve water is a regular add‑on.

Warm conditions further lift hydration occasions. AEMET reports 2023 as Spain’s second warmest year on record, with an annual mean temperature of 15.2°C, which is 1.2°C above the 1991-2020 normal. Longer warm spells encourage consumers and visitors to carry bottled water for commuting and outdoor activity, supporting repeat purchases across both small formats and bulk take‑home packs. This strengthens baseline demand during peak travel months.

Spain Bottled Water Market Challenge

Recycling Performance Gaps Increase Packaging Pressure

Plastic waste scrutiny creates a structural challenge for bottled water players, as collection outcomes remain weak and raise the bar for compliance actions. Spain’s Ministry for the Ecological Transition estimates the separate collection rate for single‑use plastic beverage bottles at 41.3% in 2023, highlighting limited recovery performance for a high‑volume packaging format.

When collection performance is this low, producers face stronger expectations to redesign packs, improve recyclability, and finance recovery and sorting systems that strengthen circularity. For a category where price points are highly competitive and promotions are frequent, packaging‑driven costs can squeeze margins and limit room for wider product innovation, particularly in high‑rotation still water lines that depend on efficient, low‑cost logistics.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Spain Bottled Water Market Trend

Health-Led Premiumisation Expands Beyond Plain Water

Health and wellness priorities keep consumers focused on low‑sugar hydration, which supports faster interest in sparkling, flavoured, and functional bottled waters positioned as alternatives to carbonates. Spain’s 2023 European Health Survey shows 15.2% of adults (18+) live with obesity, reinforcing demand for everyday choices aligned with weight‑management and “better‑for‑you” routines. This shifts attention toward more differentiated water propositions.

In response, manufacturers widen portfolios with vitamin‑fortified and low‑calorie propositions, while carbonated water gains a more premium role as a meal companion rather than a basic refreshment. Packaging cues, smaller formats, and added‑benefit messaging become more important purchase triggers, as brands compete on taste, functionality, and perceived quality-not only on basic hydration across retail shelves.

Spain Bottled Water Market Opportunity

Rising Online Buying Supports Bulk and Subscription Models

Digital purchasing is a clear opportunity for bottled water, given the weight and frequency of bulk purchases and the need for convenient replenishment. INE’s 2025 ICT Household Survey shows 59.6% of people aged 16-74 make online purchases in the last three months, indicating a large addressable base for repeat ordering and scheduled delivery for households and workplaces alike.

This level of online adoption supports subscription packs, multi‑buy bundles, and retailer partnerships that reduce last‑mile friction and improve loyalty. Brands can also use digital channels to communicate sustainability actions (such as lighter bottles or recycled plastic content) and run targeted promotions without relying solely on shelf discounts, strengthening differentiation in a mature, price‑competitive category.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Spain Bottled Water Market Segmentation Analysis

By Type of Water

- Carbonated Bottled Water

- Flavoured Bottled Water

- Functional Bottled Water

- Still Bottled Water

The segment has the highest share around segment under the type of water is still bottled water, holding about 90% market share. This dominance reflects everyday hydration habits, where consumers prioritise familiarity, broad availability, and natural mineral positioning. Still water also fits bulk purchasing patterns, as multi‑litre packs are commonly selected for regular home consumption.

Carbonated bottled water remains smaller but is increasingly chosen as a soft‑drink substitute and a more “premium” table option in restaurants. Functional and flavoured waters further broaden choice for consumers seeking vitamins, low‑calorie taste, or targeted benefits. Even with faster momentum in these niches, still water retains the broadest consumption base and anchors most mainstream retail ranging and promotions.

By Sales Channel

- On Trade

- Restaurants

- Hotels

- Cafes

- Others

- Off Trade

- Grocery Retailers

- Convenience Retail

- Supermarkets

- Hypermarkets

- Small Local Grocer

- Non-Grocery Retailers

- General Merchandise Stores

- Health and Beauty Specialists

- Vending

- E-commerce

- Grocery Retailers

The segment has the highest share around segment under the sales channel is Off‑Trade, accounting for about 80% of the market. Bottled water is typically bought in bulk for home use, which supports supermarkets and other large retailers as the preferred purchase points due to price competitiveness and easier transport of multi‑packs.

On‑trade sales remain smaller but benefit from travel, tourism, and impulse consumption in hospitality venues, especially during warmer months. Spain’s 2025 international tourism volume reinforces this out‑of‑home purchase context. E‑commerce, while still within off‑trade, reshapes buying behaviour through door‑step delivery of heavy items and repeat multi‑buy ordering, helping brands capture incremental occasions beyond the main weekly shop.

List of Companies Covered in Spain Bottled Water Market

The companies listed below are highly influential in the Spain bottled water market, with a significant market share and a strong impact on industry developments.

- Nestlé Waters España SA

- Balneario y Aguas de Solán de Cabras SA

- Centros Comerciales Carrefour SA

- Mercadona SA

- Aguas Danone SA

- Calidad Pascual SAU

- Agua Mineral San Benedetto SA

- Vichy Catalán (Grupo) SA

- Cía Servicios de Bebidas Refrescantes SL

- Gestion Fuente Liviana SL

Competitive Landscape

Spain’s bottled water market is increasingly shaped by affordability and shifting consumption preferences. Mercadona leads the category, while Aguas Danone holds a notably smaller share, highlighting a clear polarisation between value-driven consumers and those maintaining brand loyalty and quality preferences. The ongoing cost-of-living crisis continues to strengthen private label bottled water, as many households prioritise lower prices over branded offerings. At the same time, sparkling bottled water is gaining traction, particularly during the summer months, reflecting changing consumer tastes traditionally seen in neighbouring markets. Brands are responding by broadening portfolios, as illustrated by Nestlé expanding its presence through the Maison Perrier range, positioning carbonated water as a growth avenue within an increasingly competitive landscape.

Frequently Asked Questions

Related Report

1. Market Segmentation

1.1. Research Scope

1.2. Research Methodology

1.3. Definitions and Assumptions

2. Executive Summary

3. Spain Bottled Water Market Policies, Regulations, and Standards

4. Spain Bottled Water Market Dynamics

4.1. Growth Factors

4.2. Challenges

4.3. Trends

4.4. Opportunities

5. Spain Bottled Water Market Statistics, 2022-2032F

5.1. Market Size & Growth Outlook

5.1.1.By Revenues in USD Million

5.1.2.By Volume (Million Litres)

5.2. Market Segmentation & Growth Outlook

5.2.1.By Type of Water

5.2.1.1. Carbonated Bottled Water- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2. Flavoured Bottled Water- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3. Functional Bottled Water- Market Insights and Forecast 2022-2032, USD Million

5.2.1.4. Still Bottled Water- Market Insights and Forecast 2022-2032, USD Million

5.2.2.By Sub Types

5.2.2.1. Purified- Market Insights and Forecast 2022-2032, USD Million

5.2.2.1.1. Desalinated- Market Insights and Forecast 2022-2032, USD Million

5.2.2.1.2. Atmospheric Generated- Market Insights and Forecast 2022-2032, USD Million

5.2.2.1.3. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.2.2. Mineral- Market Insights and Forecast 2022-2032, USD Million

5.2.2.3. Other (Spring, Alkaline, Other) - Market Insights and Forecast 2022-2032, USD Million

5.2.3.By Packaging Material

5.2.3.1. Flexible Packaging- Market Insights and Forecast 2022-2032, USD Million

5.2.3.1.1. Aluminium- Market Insights and Forecast 2022-2032, USD Million

5.2.3.1.2. Pouches- Market Insights and Forecast 2022-2032, USD Million

5.2.3.2. Glass- Market Insights and Forecast 2022-2032, USD Million

5.2.3.3. Rigid Plastic- Market Insights and Forecast 2022-2032, USD Million

5.2.3.3.1. PET Bottles- Market Insights and Forecast 2022-2032, USD Million

5.2.3.3.2. Thin Wall Plastic Containers- Market Insights and Forecast 2022-2032, USD Million

5.2.3.3.3. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.4.By Price Category

5.2.4.1. Budget- Market Insights and Forecast 2022-2032, USD Million

5.2.4.2. Economy- Market Insights and Forecast 2022-2032, USD Million

5.2.4.3. Premium- Market Insights and Forecast 2022-2032, USD Million

5.2.5.By Pack Size

5.2.5.1. 100 ml- Market Insights and Forecast 2022-2032, USD Million

5.2.5.2. 125 ml- Market Insights and Forecast 2022-2032, USD Million

5.2.5.3. 200 ml- Market Insights and Forecast 2022-2032, USD Million

5.2.5.4. 250 ml- Market Insights and Forecast 2022-2032, USD Million

5.2.5.5. 330 ml- Market Insights and Forecast 2022-2032, USD Million

5.2.5.6. 370 ml- Market Insights and Forecast 2022-2032, USD Million

5.2.5.7. 450 ml- Market Insights and Forecast 2022-2032, USD Million

5.2.5.8. 500 ml- Market Insights and Forecast 2022-2032, USD Million

5.2.5.9. 591 ml- Market Insights and Forecast 2022-2032, USD Million

5.2.5.10. 750 ml- Market Insights and Forecast 2022-2032, USD Million

5.2.5.11. 1,000 ml- Market Insights and Forecast 2022-2032, USD Million

5.2.5.12. 1,500 ml- Market Insights and Forecast 2022-2032, USD Million

5.2.5.13. 4,000 ml- Market Insights and Forecast 2022-2032, USD Million

5.2.5.14. 5,000 ml- Market Insights and Forecast 2022-2032, USD Million

5.2.5.15. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.6.By Sales Channel

5.2.6.1. On Trade- Market Insights and Forecast 2022-2032, USD Million

5.2.6.1.1. Restaurants- Market Insights and Forecast 2022-2032, USD Million

5.2.6.1.2. Hotels- Market Insights and Forecast 2022-2032, USD Million

5.2.6.1.3. Cafes- Market Insights and Forecast 2022-2032, USD Million

5.2.6.1.4. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.6.2. Off Trade- Market Insights and Forecast 2022-2032, USD Million

5.2.6.2.1. Grocery Retailers- Market Insights and Forecast 2022-2032, USD Million

5.2.6.2.1.1. Convenience Retail- Market Insights and Forecast 2022-2032, USD Million

5.2.6.2.1.2. Supermarkets- Market Insights and Forecast 2022-2032, USD Million

5.2.6.2.1.3. Hypermarkets- Market Insights and Forecast 2022-2032, USD Million

5.2.6.2.1.4. Small Local Grocer- Market Insights and Forecast 2022-2032, USD Million

5.2.6.2.2. Non-Grocery Retailers- Market Insights and Forecast 2022-2032, USD Million

5.2.6.2.2.1. General Merchandise Stores- Market Insights and Forecast 2022-2032, USD Million

5.2.6.2.2.2. Health and Beauty Specialists- Market Insights and Forecast 2022-2032, USD Million

5.2.6.2.3. Vending- Market Insights and Forecast 2022-2032, USD Million

5.2.6.2.4. E-commerce- Market Insights and Forecast 2022-2032, USD Million

5.2.7.By Competitors

5.2.7.1. Competition Characteristics

5.2.7.2. Market Share & Analysis

6. Spain Carbonated Bottled Water Market Statistics, 2022-2032

6.1. Market Size & Growth Outlook

6.1.1.By Revenues in USD Million

6.1.2.By Volume (Million Litres)

6.2. Market Segmentation & Growth Outlook

6.2.1.By Sub Types- Market Insights and Forecast 2022-2032, USD Million

6.2.2.By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

6.2.3.By Pack Size- Market Insights and Forecast 2022-2032, USD Million

6.2.4.By Price Category- Market Insights and Forecast 2022-2032, USD Million

6.2.5.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

7. Spain Flavoured Bottled Water Market Statistics, 2022-2032

7.1. Market Size & Growth Outlook

7.1.1.By Revenues in USD Million

7.1.2.By Volume (Million Litres)

7.2. Market Segmentation & Growth Outlook

7.2.1.By Sub Types- Market Insights and Forecast 2022-2032, USD Million

7.2.2.By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

7.2.3.By Pack Size- Market Insights and Forecast 2022-2032, USD Million

7.2.4.By Price Category- Market Insights and Forecast 2022-2032, USD Million

7.2.5.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

8. Spain Functional Bottled Water Market Statistics, 2022-2032

8.1. Market Size & Growth Outlook

8.1.1.By Revenues in USD Million

8.1.2.By Volume (Million Litres)

8.2. Market Segmentation & Growth Outlook

8.2.1.By Sub Types- Market Insights and Forecast 2022-2032, USD Million

8.2.2.By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

8.2.3.By Pack Size- Market Insights and Forecast 2022-2032, USD Million

8.2.4.By Price Category- Market Insights and Forecast 2022-2032, USD Million

8.2.5.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

9. Spain Still Bottled Water Market Statistics, 2022-2032

9.1. Market Size & Growth Outlook

9.1.1.By Revenues in USD Million

9.1.2.By Volume (Million Litres)

9.2. Market Segmentation & Growth Outlook

9.2.1.By Sub Types- Market Insights and Forecast 2022-2032, USD Million

9.2.2.By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

9.2.3.By Pack Size- Market Insights and Forecast 2022-2032, USD Million

9.2.4.By Price Category- Market Insights and Forecast 2022-2032, USD Million

9.2.5.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

10. Competitive Outlook

10.1. Company Profiles

10.1.1. Mercadona SA

10.1.1.1. Business Description

10.1.1.2. Product Portfolio

10.1.1.3. Collaborations & Alliances

10.1.1.4. Recent Developments

10.1.1.5. Financial Details

10.1.1.6. Others

10.1.2. Aguas Danone SA

10.1.2.1. Business Description

10.1.2.2. Product Portfolio

10.1.2.3. Collaborations & Alliances

10.1.2.4. Recent Developments

10.1.2.5. Financial Details

10.1.2.6. Others

10.1.3. Calidad Pascual SAU

10.1.3.1. Business Description

10.1.3.2. Product Portfolio

10.1.3.3. Collaborations & Alliances

10.1.3.4. Recent Developments

10.1.3.5. Financial Details

10.1.3.6. Others

10.1.4. Agua Mineral San Benedetto SA

10.1.4.1. Business Description

10.1.4.2. Product Portfolio

10.1.4.3. Collaborations & Alliances

10.1.4.4. Recent Developments

10.1.4.5. Financial Details

10.1.4.6. Others

10.1.5. Vichy Catalán (Grupo) SA

10.1.5.1. Business Description

10.1.5.2. Product Portfolio

10.1.5.3. Collaborations & Alliances

10.1.5.4. Recent Developments

10.1.5.5. Financial Details

10.1.5.6. Others

10.1.6. Nestlé Waters España SA

10.1.6.1. Business Description

10.1.6.2. Product Portfolio

10.1.6.3. Collaborations & Alliances

10.1.6.4. Recent Developments

10.1.6.5. Financial Details

10.1.6.6. Others

10.1.7. Balneario y Aguas de Solán de Cabras SA

10.1.7.1. Business Description

10.1.7.2. Product Portfolio

10.1.7.3. Collaborations & Alliances

10.1.7.4. Recent Developments

10.1.7.5. Financial Details

10.1.7.6. Others

10.1.8. Centros Comerciales Carrefour SA

10.1.8.1. Business Description

10.1.8.2. Product Portfolio

10.1.8.3. Collaborations & Alliances

10.1.8.4. Recent Developments

10.1.8.5. Financial Details

10.1.8.6. Others

10.1.9. Cía Servicios de Bebidas Refrescantes SL

10.1.9.1. Business Description

10.1.9.2. Product Portfolio

10.1.9.3. Collaborations & Alliances

10.1.9.4. Recent Developments

10.1.9.5. Financial Details

10.1.9.6. Others

10.1.10. Gestion Fuente Liviana SL

10.1.10.1.Business Description

10.1.10.2.Product Portfolio

10.1.10.3.Collaborations & Alliances

10.1.10.4.Recent Developments

10.1.10.5.Financial Details

10.1.10.6.Others

11. Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Type of Water |

|

| By Sub Types |

|

| By Packaging Material |

|

| By Price Category |

|

| By Pack Size |

|

| By Sales Channel |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.