Southeast Asia Forestry Machinery Market Report: Trends, Growth and Forecast (2026-2032)

By Equipment Type (Felling Equipment (Chainsaw, Harvester, Feller Buncher), Extracting Equipment (Forwarder, Skidder), On-Site Processing Equipment (Chipper, Delimber), Other Forestry Equipment (Loader, Mulcher)), By Power Source (Diesel, Hybrid, Battery-Electric), By Automation Level (Manual, Semi-Autonomous, Fully Autonomous), By End User (Contract Logging Firms, Forest Ownership Groups, Pulp and Paper Companies), By Country (Malaysia, Indonesia, Singapore, Cambodia, Vietnam, Thailand, Philippines, Rest of Southeast Asia) ... Read more

|

Major Players

|

Southeast Asia Forestry Machinery Market Statistics and Insights, 2026

- Market Size Statistics

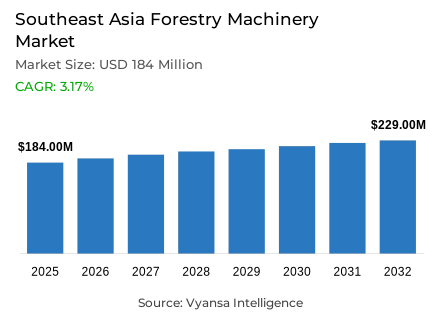

- Forestry machinery market size in Southeast Asia was valued at USD 184 million in 2025 and is estimated at USD 195 million in 2026.

- The market size is expected to grow to USD 229 million by 2032.

- Market to register a CAGR of around 3.17% during 2026-32.

- Equipment Type Shares

- Felling equipment grabbed market share of 40%.

- Competition

- More than 10 companies are actively engaged in producing forestry machinery in Southeast Asia.

- Top 5 companies acquired around 45% of the market share.

- Kubota Corporation, Doosan Bobcat, Mitsubishi Heavy Industries, Caterpillar Inc., Komatsu Ltd. etc., are few of the top companies.

- Power Source

- Diesel grabbed 85% of the market.

- Country

- Indonesia leads with a 30% share of the Southeast Asia market.

Southeast Asia Forestry Machinery Market Outlook

The Southeast Asia forestry machinery market was valued at USD 184 million in 2025 and is projected to advance from USD 195 million in 2026 to USD 229 million by 2032, registering a CAGR of approximately 3.17% during the forecast period. This growth trajectory is anchored in the region's expanding industrial plantation forestry sector, where rising timber harvesting activities across Indonesia, Vietnam, and Thailand are generating sustained and measurable demand for mechanized harvesting and extraction equipment. The convergence of growing wood processing requirements, pulp production expansion, and increasing government investment in forest restoration programmes is progressively encouraging forestry operators across the region to modernize equipment fleets and reduce dependency on manual labor across large-scale commercial forestry operations.

Felling Equipment commands approximately 40% share within the equipment type category, reflecting the foundational role that harvesters, chainsaws, and feller bunchers occupy in enabling timber extraction across dense tropical forest zones and industrial plantation areas throughout Southeast Asia. Commercial logging and plantation harvesting activities across Indonesia, Vietnam, and Thailand continue to generate consistent procurement demand for advanced felling systems, as mechanized cutting equipment improves productivity, minimises operational delays, and supports efficient large-scale timber collection across the region's commercially active forestry zones.

Diesel-powered machinery accounts for nearly 85% share within the power source category, a dominance sustained by the high torque output, operational durability, and continuous performance reliability that diesel configurations deliver across rugged tropical terrain conditions and remote forestry locations where electric charging infrastructure remains largely absent. Harvesters, skidders, loaders, and forwarders across Southeast Asia's plantation and logging operations rely on diesel engines as the most practically viable power source for uninterrupted heavy-duty timber extraction and transportation activity.

Indonesia leads the Southeast Asia forestry machinery market with approximately 30% share, supported by extensive forest resources and large-scale industrial plantation activities that generate substantial demand for harvesting, transportation, and plantation maintenance equipment. As per data published by the Food and Agriculture Organization, Indonesia produced more than 64.84 million cubic meters of industrial roundwood in 2024, reinforcing the structural depth of mechanized forestry equipment demand that underpins the country's regional market leadership through the forecast period.

Southeast Asia Forestry Machinery Market Growth Driver

Expanding Timber Production and Plantation Forestry Strengthening Machinery Deployment

The primary commercial driver within the Southeast Asia forestry machinery market is the region's expanding industrial forestry activity, where rising timber production volumes and the growth of commercial plantation operations are generating consistent and operationally critical demand for mechanized harvesting, extraction, and transportation equipment across Indonesia, Vietnam, and Thailand. According to statistics released by the Food and Agriculture Organization, Indonesia alone accounts for nearly 5% of global industrial roundwood consumption in 2024, a share that reflects the region's substantial timber processing capacity and the scale of harvesting infrastructure required to sustain it. This production volume places significant operational pressure on forestry equipment fleets, where mechanized logging solutions are increasingly preferred over labor-intensive manual methods to improve harvesting speed and reduce operational costs across large plantation forestry systems.

Government investment in forest-based rural economies and sustainable forestry practices is further reinforcing this demand base across the region. As indicated by authoritative sources at the World Bank, sustainable forest management supports employment generation and rural development across emerging economies, creating a policy environment that encourages forestry companies to invest in modernized equipment fleets capable of improving both productivity and environmental compliance. Rising investments in forest restoration, plantation management, and wood-product value chains across Southeast Asia are collectively expanding the addressable demand base for the Southeast Asia forestry machinery market, with forestry mechanization Southeast Asia-wide becoming an increasingly central component of national agricultural and land management strategies through the forecast period.

Southeast Asia Forestry Machinery Market Challenge

Infrastructure Deficits and High Ownership Costs Constraining Mechanization Penetration

The most structurally persistent challenge facing the Southeast Asia forestry machinery market is the combination of weak transport infrastructure across remote forest regions and the high capital burden associated with advanced forestry equipment ownership, two constraints that together suppress mechanization penetration among the small and medium forestry contractors that form a significant portion of the region's active forestry sector. Poor road connectivity, uneven terrain, and inadequate servicing facilities across many logging and plantation areas increase operational downtime and transportation inefficiencies during timber extraction activities, reducing the effective utilisation rates of deployed machinery and weakening the financial case for equipment investment among smaller operators. Evidence drawn from public data released by the OECD confirms that logistics costs in some ASEAN member states account for up to 20% of the price of finished goods, a figure that reflects the persistent transport and supply-chain inefficiencies that also elevate the operational costs of heavy forestry machinery deployment across the region.

High acquisition and maintenance costs for advanced harvesters, forwarders, and feller bunchers compound this infrastructure constraint significantly, as these equipment categories require substantial upfront capital investment alongside continuous servicing and spare-part replacement expenditure across their operational lifecycles. Based on data from the International Trade Administration, Southeast Asian countries continue to rely heavily on imported industrial machinery and equipment, increasing both procurement costs and long-term maintenance dependency for heavy forestry machinery across the regional sector. This import dependency limits the ability of smaller forestry contractors to achieve cost-effective machinery ownership, reinforcing the concentration of advanced equipment among larger commercial operators and constraining the broader penetration of mechanized forestry operations Southeast Asia-wide.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Southeast Asia Forestry Machinery Market Trend

Digital Monitoring and Precision Forestry Technologies Gaining Commercial Traction

A structurally significant operational shift is underway across Southeast Asia's commercial forestry sector, where the adoption of digital monitoring systems, GPS-enabled forestry machinery, and telematics platforms is progressively transforming how plantation and logging operations are managed across large-scale forest environments in Indonesia, Vietnam, and Thailand. Forestry operators are integrating fuel-monitoring systems, telematics-enabled equipment tracking, and data-driven forestry management tools into their operational frameworks to optimise timber extraction efficiency, reduce waste, and improve compliance with sustainable harvesting standards that are increasingly demanded by downstream buyers in pulp, paper, and construction supply chains. This technological transition is creating measurable demand for smart forestry equipment configurations that deliver both operational intelligence and environmental performance data within a single integrated platform.

Environmental pressure is accelerating the pace of this trend with particular urgency. In line with findings from Reuters, forest loss in Indonesia surged by 66% in 2025, reaching its highest level in eight years as a consequence of weakened environmental protections and expanding food and energy self-sufficiency programmes, a development that has intensified regulatory and commercial scrutiny of forestry operations across the region. Rising conservation pressure is compelling forestry operators to demonstrate measurable sustainability outcomes through precision forestry systems, land monitoring technologies, and efficient machinery deployment practices that reduce ecological disruption during timber extraction. The Southeast Asia forestry machinery market is responding to this demand with a growing range of advanced forestry harvesting technologies that combine operational efficiency with the environmental accountability that sustainable forest management frameworks now require.

Southeast Asia Forestry Machinery Market Opportunity

Reforestation Programmes and Plantation Expansion Creating Long-Cycle Equipment Demand

Large-scale reforestation initiatives and the continued expansion of commercial plantation forestry across Southeast Asia represent the most structurally durable opportunity available within the Southeast Asia forestry machinery market, providing a policy-supported and long-cycle demand base for mechanized land preparation, biomass clearing, and plantation maintenance equipment across multiple national forestry programmes. Data compiled from internationally recognised public authorities at the Food and Agriculture Organization confirms that Asia holds nearly 146 million hectares of planted forests, accounting for approximately 23% of the region's total forest area and significantly exceeding the global average of 8%, a coverage base that requires continuous mechanized management across its full plantation lifecycle. This planted forest area generates recurring procurement demand for mulchers, loaders, excavators, and land-clearing equipment that is structurally distinct from natural forest harvesting cycles and less exposed to the conservation restrictions that increasingly govern primary forest operations.

Government-led mangrove rehabilitation, degraded land restoration, and commercial plantation development programmes across Indonesia, Vietnam, and Thailand are materially expanding the equipment deployment opportunities available to forestry machinery manufacturers and contractors operating across the region. The Food and Agriculture Organization further highlights that while East and South Asia record strong plantation gains through large-scale tree-planting initiatives, Southeast Asia continues facing forest losses that increase the urgency of efficient forest restoration and land management solutions. For operators within the Southeast Asia forestry machinery market, these reforestation and plantation programmes represent a commercially compelling long-term demand segment, supported by committed public investment in forest carbon sequestration, biodiversity restoration, and rural employment generation objectives across the region's major forestry economies.

Southeast Asia Forestry Machinery Market Country Analysis

By Country

- Malaysia

- Indonesia

- Singapore

- Cambodia

- Vietnam

- Thailand

- Philippines

- Rest of Southeast Asia

Indonesia leads the Southeast Asia forestry machinery market with approximately 30% share, supported by the country's position as one of the Asia-Pacific region's largest forestry-producing economies, where extensive forest resources, large-scale industrial plantation operations, and active pulp and paper production collectively generate substantial and diversified demand for harvesting, transportation, and plantation maintenance machinery. As per official figures from the Food and Agriculture Organization, Indonesia produced more than 64.84 million cubic meters of industrial roundwood in 2024, a production volume that anchors consistent procurement activity for harvesters, skidders, loaders, and mulchers across the country's commercially active forestry sector. Government-supported forest rehabilitation programmes and social forestry initiatives implemented by Indonesia's Ministry of Environment and Forestry further reinforce machinery demand by expanding the scope of mechanized land preparation, biomass clearing, and plantation maintenance activities across degraded forest areas undergoing active restoration.

Vietnam and Thailand represent the region's second and third most commercially significant forestry machinery markets, each supported by expanding acacia and eucalyptus plantation sectors that generate consistent demand for mechanized timber extraction and plantation management equipment. Industry findings suggest that forestry equipment modernization trends across Vietnam are accelerating as pulp and paper export volumes grow and downstream buyers impose more stringent operational and sustainability standards on timber supply chains. Myanmar, Cambodia, and Laos contribute at smaller scale but represent structurally emerging demand zones as plantation forestry activities expand and government investment in forest restoration progressively increases mechanized equipment deployment across the region's less commercially developed forestry economies.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Southeast Asia Forestry Machinery Market Segmentation Analysis

By Equipment Type

- Felling Equipment

- Chainsaw

- Harvester

- Feller Buncher

- Extracting Equipment

- Forwarder

- Skidder

- On-Site Processing Equipment

- Chipper

- Delimber

- Other Forestry Equipment

- Loader

- Mulcher

Felling Equipment accounts for approximately 40% share within the equipment type category across the Southeast Asia forestry machinery market, a dominance that reflects the irreplaceable operational role that harvesters, chainsaws, and feller bunchers occupy as the primary machinery enabling timber extraction across both dense natural forest zones and large industrial plantation areas throughout the region. Commercial logging and plantation harvesting activities across Indonesia, Vietnam, and Thailand consistently generate procurement demand for advanced felling systems, as mechanized cutting equipment reduces the labor intensity of primary harvesting operations, improves cutting precision, and supports efficient large-volume timber collection during active harvesting cycles. Statistics show that growing timber demand from pulp, paper, and construction industries is reinforcing the deployment of technologically advanced felling systems across Southeast Asia's commercially active forestry zones.

The commercial strength of felling equipment within the Southeast Asia forestry machinery market is further sustained by the breadth of plantation types across which these systems are deployed, encompassing eucalyptus, acacia, and mixed timber plantations across Indonesia and Vietnam where mechanized timber extraction equipment is increasingly replacing manual and semi-mechanized harvesting methods. As industrial forestry activities continue expanding and plantation areas under active harvesting grow across the region, demand for modern felling machinery incorporating GPS-enabled guidance systems and forestry telematics is expected to strengthen progressively through the forecast period. Forestry operators prioritising productivity improvement and operational efficiency are projected to direct a sustained proportion of equipment investment toward advanced felling configurations, reinforcing the segment's structural leadership within the equipment type category through 2032.

By Power Source

- Diesel

- Hybrid

- Battery-Electric

Diesel-powered configurations account for approximately 85% share within the power source category across the Southeast Asia forestry machinery market, a position grounded in the fundamental operational realities of tropical plantation and logging environments where remote location, absence of reliable electrical grid infrastructure, and demands for sustained heavy-duty performance make diesel machinery the only commercially practical power source for continuous large-scale timber harvesting and extraction operations. Harvesters, skidders, loaders, and forwarders deployed across Indonesia, Vietnam, and Thailand's commercial forestry operations rely on diesel engines for their high torque output, long operating hours, and operational durability across the rugged and varied terrain conditions that characterise active forest environments throughout the region. Official records confirm that remote forestry locations across Southeast Asia continue to lack the power network reliability required to support electric or hybrid machinery adoption at commercially meaningful scale.

The sustained dominance of diesel systems within the Southeast Asia forestry machinery market reflects not only current infrastructure constraints but also the well-established serviceability of diesel equipment across the region's forestry contractor networks, where maintenance expertise, spare-part availability, and fuelling logistics are structured around combustion-based machinery. While low-emission forestry equipment and hybrid forestry machinery are generating increasing manufacturer attention, the infrastructure preconditions for meaningful alternative power adoption in active Southeast Asian forest environments remain absent across the majority of operational zones. Diesel configurations are therefore projected to retain their dominant power source share throughout the forecast period, with gradual incremental adoption of fuel-efficient engine technologies progressively improving the environmental performance of diesel machinery without displacing its operational primacy across the region's commercial forestry sector.

Various Market Players in Southeast Asia Forestry Machinery Market

The companies mentioned below are highly active in the Southeast Asia forestry machinery market, occupying a considerable portion of the market and shaping industry progress.

- Kubota Corporation

- Doosan Bobcat

- Mitsubishi Heavy Industries

- Caterpillar Inc.

- Komatsu Ltd.

- Hitachi Construction Machinery

- Volvo Construction Equipment

- CNH Industrial N.V.

- Sumitomo Heavy Industries

- Ponsse

- Tigercat Industries

- John Deere

Market News & Updates

- Ponsse, 2026:

Ponsse launched the next-generation Opti 5G information system for track-based forestry machines in 2026 alongside the OptiFellingAssist solution aimed at improving harvesting precision, operational safety, and machine productivity. The upgraded digital platform supports advanced machine connectivity and real-time forestry operations management, aligning with increasing demand for intelligent and automated forestry solutions in mechanized timber harvesting markets, including Southeast Asia.

- Komatsu Ltd., 2025:

Komatsu introduced the new TimberPro TN230D log loader in 2025, designed for demanding forestry operations with upgraded hydraulic performance, dual service platforms, enhanced operator visibility, and improved maintenance access. The machine incorporates higher swing torque and Power Max technology to support heavy timber handling applications, strengthening Komatsu’s forestry equipment portfolio used across logging and timber processing operations globally, including Southeast Asia.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- Southeast Asia Forestry Machinery Market Policies, Regulations, and Standards

- Southeast Asia Forestry Machinery Production (Thousand Ton) Trend 2022-2032

- Southeast Asia Forestry Machinery Production (Thousand Ton) Trend By Equipment Type

- Felling Equipment

- Extracting Equipment

- On-Site Processing Equipment

- Other Forestry Equipment

- Company Wise Production Plants and Statistics

- Installed Production Capacity

- Actual Production

- Planned Production Target

- Southeast Asia Forestry Machinery Production (Thousand Ton) Trend By Equipment Type

- Southeast Asia Forestry Machinery Pricing Analysis 2022-2032

- Southeast Asia Forestry Machinery Pricing Trend (Units) 2022-2032

- Southeast Asia Forestry Machinery Pricing Trend (Units) By Regions 2022-2032

- Malaysia

- Indonesia

- Singapore

- Cambodia

- Vietnam

- Thailand

- Philippines

- Southeast Asia Forestry Machinery Pricing Trend (Units) By Equipment Type 2022-2032

- Felling Equipment

- Extracting Equipment

- On-Site Processing Equipment

- Other Forestry Equipment

- Southeast Asia Forestry Machinery Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- Southeast Asia Forestry Machinery Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold (Thousand Units)

- Market Segmentation & Growth Outlook

- By Equipment Type

- Felling Equipment- Market Insights and Forecast 2022-2032, USD Million

- Chainsaw- Market Insights and Forecast 2022-2032, USD Million

- Harvester- Market Insights and Forecast 2022-2032, USD Million

- Feller Buncher- Market Insights and Forecast 2022-2032, USD Million

- Extracting Equipment- Market Insights and Forecast 2022-2032, USD Million

- Forwarder- Market Insights and Forecast 2022-2032, USD Million

- Skidder- Market Insights and Forecast 2022-2032, USD Million

- On-Site Processing Equipment- Market Insights and Forecast 2022-2032, USD Million

- Chipper- Market Insights and Forecast 2022-2032, USD Million

- Delimber- Market Insights and Forecast 2022-2032, USD Million

- Other Forestry Equipment- Market Insights and Forecast 2022-2032, USD Million

- Loader- Market Insights and Forecast 2022-2032, USD Million

- Mulcher- Market Insights and Forecast 2022-2032, USD Million

- Felling Equipment- Market Insights and Forecast 2022-2032, USD Million

- By Power Source

- Diesel- Market Insights and Forecast 2022-2032, USD Million

- Hybrid- Market Insights and Forecast 2022-2032, USD Million

- Battery-Electric- Market Insights and Forecast 2022-2032, USD Million

- By Automation Level

- Manual- Market Insights and Forecast 2022-2032, USD Million

- Semi-Autonomous- Market Insights and Forecast 2022-2032, USD Million

- Fully Autonomous- Market Insights and Forecast 2022-2032, USD Million

- By End User

- Contract Logging Firms- Market Insights and Forecast 2022-2032, USD Million

- Forest Ownership Groups- Market Insights and Forecast 2022-2032, USD Million

- Pulp and Paper Companies- Market Insights and Forecast 2022-2032, USD Million

- By Country

- Malaysia

- Indonesia

- Singapore

- Cambodia

- Vietnam

- Thailand

- Philippines

- Rest of Southeast Asia

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Equipment Type

- Market Size & Growth Outlook

- Malaysia Forestry Machinery Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold (Thousand Units)

- Market Segmentation & Growth Outlook

- By Equipment Type- Market Insights and Forecast 2022-2032, USD Million

- By Power Source- Market Insights and Forecast 2022-2032, USD Million

- By Automation Level- Market Insights and Forecast 2022-2032, USD Million

- By Sales Type- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Indonesia Forestry Machinery Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold (Thousand Units)

- Market Segmentation & Growth Outlook

- By Equipment Type- Market Insights and Forecast 2022-2032, USD Million

- By Power Source- Market Insights and Forecast 2022-2032, USD Million

- By Automation Level- Market Insights and Forecast 2022-2032, USD Million

- By Sales Type- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Singapore Forestry Machinery Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold (Thousand Units)

- Market Segmentation & Growth Outlook

- By Equipment Type- Market Insights and Forecast 2022-2032, USD Million

- By Power Source- Market Insights and Forecast 2022-2032, USD Million

- By Automation Level- Market Insights and Forecast 2022-2032, USD Million

- By Sales Type- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Cambodia Forestry Machinery Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold (Thousand Units)

- Market Segmentation & Growth Outlook

- By Equipment Type- Market Insights and Forecast 2022-2032, USD Million

- By Power Source- Market Insights and Forecast 2022-2032, USD Million

- By Automation Level- Market Insights and Forecast 2022-2032, USD Million

- By Sales Type- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Vietnam Forestry Machinery Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold (Thousand Units)

- Market Segmentation & Growth Outlook

- By Equipment Type- Market Insights and Forecast 2022-2032, USD Million

- By Power Source- Market Insights and Forecast 2022-2032, USD Million

- By Automation Level- Market Insights and Forecast 2022-2032, USD Million

- By Sales Type- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Thailand Forestry Machinery Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold (Thousand Units)

- Market Segmentation & Growth Outlook

- By Equipment Type- Market Insights and Forecast 2022-2032, USD Million

- By Power Source- Market Insights and Forecast 2022-2032, USD Million

- By Automation Level- Market Insights and Forecast 2022-2032, USD Million

- By Sales Type- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Philippines Forestry Machinery Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold (Thousand Units)

- Market Segmentation & Growth Outlook

- By Equipment Type- Market Insights and Forecast 2022-2032, USD Million

- By Power Source- Market Insights and Forecast 2022-2032, USD Million

- By Automation Level- Market Insights and Forecast 2022-2032, USD Million

- By Sales Type- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Caterpillar Inc.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Komatsu Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Hitachi Construction Machinery

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Volvo Construction Equipment

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- CNH Industrial N.V.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Kubota Corporation

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Doosan Bobcat

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Mitsubishi Heavy Industries

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Sumitomo Heavy Industries

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Ponsse

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Tigercat Industries

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- John Deere

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Caterpillar Inc.

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Equipment Type |

|

| By Power Source |

|

| By Automation Level |

|

| By End User |

|

| By Country |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.