Brazil Combine Harvester Market Report: Trends, Growth and Forecast (2026-2032)

By Type (Self-propelled, Tractor-pulled Combine, PTO-powered Combine), By Mechanism (Hydraulic, Hybrid), By Power (Below 150 HP, 150-300 HP, 300-450 HP, 450-550 HP, Above 550 HP), By Class (Class 1-2, Class 3-4, Class 5-6, Class 7 & Above), By Grain Tank Size (< 250 bu, 250-350 bu, > 350 bu), By Region (North, Center-West, Northeast, Southeast, South) ... Read more

|

Major Players

|

Brazil Combine Harvester Market Statistics and Insights, 2026

- Market Size Statistics

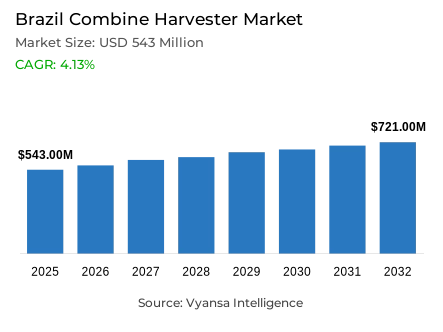

- Combine harvester market size in Brazil was valued at USD 543 million in 2025 and is estimated at USD 562 million in 2026.

- The market size is expected to grow to USD 721 million by 2032.

- Market to register a CAGR of around 4.13% during 2026-32.

- Type Shares

- Self-propelled grabbed market share of 80%.

- Competition

- More than 10 companies are actively engaged in producing combine harvester in Brazil.

- Top 5 companies acquired around 70% of the market share.

- Valtra Brasil, SLC Maquinas, CLAAS America Latina, John Deere Brasil, AGCO do Brasil etc., are few of the top companies.

- Mechanism

- Hydraulic grabbed 65% of the market.

Brazil Combine Harvester Market Outlook

The Brazil combine harvester market was valued at USD 543 million in 2025 and is projected to advance from USD 562 million in 2026 to USD 721 million by 2032, registering a CAGR of 4.13% during the forecast period. Brazil's position as the world's largest soybean exporter and one of the most commercially intensive grain-producing nations globally creates a structural and self-reinforcing demand base for mechanized harvesting equipment, where the scale of cultivated area and the narrowness of viable harvest windows together make combine harvester deployment operationally non-negotiable across large commercial farming systems.

Self-propelled combine harvesters command approximately 80% share within the type category, reflecting the operational requirements of Brazil's expansive grain farming sector, where the consolidation of cutting, threshing, and grain collection into a single continuous process is essential for managing large cultivation areas within acceptable harvesting timeframes. These systems are the preferred configuration across the soybean belt regions of Mato Grosso, Paraná, and Goiás, where uninterrupted field coverage and high throughput are the primary measures of operational performance for commercial farming operators.

Hydraulic systems account for approximately 65% share within the mechanism category, sustained by their operational superiority in delivering smooth machine control, responsive field adaptation, and reduced downtime across Brazil's intensive harvesting cycles. The demanding conditions of peak grain harvesting seasons, where equipment must perform continuously over extended periods across vast cultivation areas, make hydraulic configurations the most commercially reliable mechanism choice for large-scale farming operations.

Brazil's agricultural land scale reinforces the depth of this market across all forecast years. As per data published by FAO FAOSTAT, Brazil harvested more than 95 million hectares of agricultural crops in recent datasets, a figure that anchors sustained demand for advanced harvesting equipment and positions the Brazil combine harvester market for consistent expansion through 2032.

Brazil Combine Harvester Market Growth Driver

Soybean and Corn Production Scale Generating Sustained Harvesting Equipment Demand

The primary commercial driver within the Brazil combine harvester market is the country's exceptional grain production volume, which creates recurring and operationally critical demand for high-capacity harvesting machinery across the nation's most commercially active agricultural regions. According to statistics released by the USDA Foreign Agricultural Service, Brazil's soybean production reached 180 million metric tonnes in MY 2025/26 while corn production reached 130 million metric tonnes in the same marketing year, a combined output that places Brazil among the most demanding environments globally for harvesting equipment performance and fleet capacity. These production volumes require combine harvesters capable of operating at sustained throughput levels across cultivation areas that span millions of hectares during harvest windows that allow minimal operational delay.

Evidence drawn from public data released by FAO FAOSTAT confirms that Brazil harvested approximately 47.3 to 47.6 million hectares of soybean area in recent datasets, a land coverage figure that illustrates the structural depth of mechanized harvesting demand across the country's grain farming systems. Expanding soybean cultivation Brazil-wide and rising corn production Brazil-wide are not short-cycle phenomena but are sustained by long-term export commitments and domestic food processing demand that continuously reinforce the case for advanced harvesting machinery investment. Brazil agricultural mechanization has therefore become less a discretionary capital decision and more a prerequisite for commercial viability in a grain farming sector where harvest speed, grain recovery rates, and equipment reliability directly determine export competitiveness and farm-level profitability.

Brazil Combine Harvester Market Challenge

Equipment Affordability and Farm Fragmentation Constraining Mechanization Reach

High combine harvester costs represent the most structurally entrenched challenge facing broader market penetration in Brazil, where a large proportion of agricultural establishments operate at scales that make full machinery ownership financially inaccessible without reliable and appropriately structured financing support. As per official figures from the Brazilian Institute of Geography and Statistics, family farming establishments account for nearly 77% of all agricultural establishments in Brazil, a distribution that reveals the fundamental tension between the country's globally significant grain output and the fragmented smallholder farming systems that coexist alongside its commercial agribusiness operations. Agricultural equipment financing challenges are most acute in these smallholder segments, where income volatility tied to commodity price fluctuations limits the predictability needed to service large machinery loan commitments.

The Brazil combine harvester market therefore faces a persistent structural divide between the commercially intensive large-farm segment, which drives the majority of equipment demand, and the smallholder segment, which remains largely dependent on contract harvesting services or outdated equipment configurations. Based on data from the World Bank, agriculture contributes approximately 6.5% of GDP across Latin America and the Caribbean, reflecting income patterns that remain sensitive to commodity cycles and weather disruptions. Agricultural credit access limitations compound this dynamic, as credit terms in rural Brazil do not consistently align with the seasonal cash flow patterns of smaller producers. Small farm mechanization barriers are unlikely to resolve rapidly, and the combine harvester industry in Brazil must continue developing rental, leasing, and cooperative ownership structures to extend market reach beyond its current large-farm concentration.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Brazil Combine Harvester Market Trend

Digital Agriculture Integration Transforming the Operational Profile of Harvesting Equipment

Precision farming technologies are progressively redefining what commercial operators in Brazil expect from combine harvesting equipment, shifting the purchasing decision from one centred on mechanical capacity alone to one that encompasses digital integration, real-time data generation, and connectivity with broader farm management systems. Insights sourced from official databases at the OECD Agricultural Policy Monitoring and Evaluation 2024 report confirm that Brazil has institutionalised precision farming adoption through the National Policy for Incentives on Precision Agriculture and Livestock under Law No. 14,475, with rural credit lines across the country formally structured to finance precision farming equipment acquisition, creating a direct policy-to-market pathway for advanced harvesting technology uptake.

GPS-guided harvesting equipment, automated steering systems, and yield monitoring systems are now standard specifications rather than premium additions across large commercial harvesting fleets in Mato Grosso and Rio Grande do Sul. The Brazil combine harvester market is responding to this demand evolution with a growing range of connected farm machinery configurations that integrate sensor-based harvesting systems, telematics for agricultural equipment, and data-driven farming equipment analytics into operational platforms. These technologies enable farm operators to monitor grain loss rates in real time, adjust harvesting parameters dynamically, and generate field-level performance data that informs the next season's cultivation and equipment planning decisions. As agricultural automation in Brazil's farming sector continues deepening, precision-enabled harvesters are expected to become the dominant equipment standard across the commercial grain belt through the forecast period.

Brazil Combine Harvester Market Opportunity

Export Growth and Post-Harvest Loss Reduction Expanding the Investment Case for Mechanization

Brazil's status as the world's most commercially significant soybean exporter creates a structurally compelling opportunity environment for combine harvester deployment, where the financial consequences of harvesting inefficiency are magnified by the volume and value of grain moving through international trade channels each season. Data compiled from internationally recognised public authorities at the Food and Agriculture Organization confirms that grain post-harvest losses globally range between 10% and 20%, a loss band that carries exceptional commercial weight in a country where soybean harvesting machinery demand is tied directly to export contract fulfilment and grain quality standards imposed by international buyers. Reducing harvest losses through advanced combine harvesters is therefore not only a productivity objective but an export competitiveness imperative for Brazil's commercial farming sector.

The opportunity for expanded combine harvester adoption is further strengthened by the geographic extension of grain farming into frontier agricultural regions of Brazil's central-west interior, where new cultivation areas are being brought under commercial production and require fresh investment in harvesting infrastructure. As indicated by authoritative sources at the United States Department of Agriculture (USDA), Brazil remains the world's largest soybean exporter in recent agricultural trade datasets, a position that is sustained only through continuous improvement in harvesting speed, grain recovery efficiency, and operational reliability across an expanding agricultural footprint. Autonomous harvesting technology and AI-powered combine harvesters represent the next generation of this investment cycle, with Brazil's large commercial farming operations providing the scale and financial capacity to pilot and adopt these technologies ahead of most other agricultural markets in the Latin American region.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Brazil Combine Harvester Market Segmentation Analysis

By Type

- Self-propelled

- Tractor-pulled Combine

- PTO-powered Combine

Self-propelled combine harvesters command approximately 80% share within the Type category in the Brazil combine harvester market, a dominance that is structurally grounded in the operational logic of large-scale soybean and corn farming, where the ability to complete cutting, threshing, separation, and grain collection in a single uninterrupted field pass is the most commercially efficient configuration available to farm operators managing thousands of hectares under time-sensitive harvest conditions. In line with findings from FAO FAOSTAT, Brazil harvested more than 95 million hectares of agricultural crop area in recent datasets, a scale that demands harvesting systems capable of sustained high-throughput performance without the coordination dependencies associated with tractor-mounted or PTO-powered alternative configurations.

Commercial farming operators across Mato Grosso, Paraná, and Goiás consistently select self-propelled platforms because they reduce total harvesting cycle time, support integration with GPS-guided harvesting equipment and precision harvesting solutions, and deliver the operational independence required across remote and expansive grain-producing zones where equipment downtime carries disproportionate financial consequence. As Brazil agricultural mechanization continues advancing and cultivation areas expand into the central-west frontier, self-propelled combine harvesters are expected to retain their dominant share position throughout the forecast period, supported by the growing availability of AI-integrated harvesting equipment and telematics-enabled combine harvesters that extend the operational intelligence of these platforms beyond basic mechanical harvesting functions.

By Mechanism

- Hydraulic

- Hybrid

Hydraulic combine harvesters account for approximately 65% share within the Mechanism category across the Brazil combine harvester market, a position that reflects the functional advantages hydraulic systems deliver in one of the world's most demanding large-scale grain harvesting environments. Hydraulic mechanisms provide the responsive machine control, directional flexibility, and operational consistency that Brazil's intensive commercial farming cycles require, particularly across the extended harvesting periods in Mato Grosso and Rio Grande do Sul where equipment must sustain peak performance across large land areas without significant interruption. Validated reports from the USDA Economic Research Service confirm that precision-enabled agricultural machinery adoption continues to increase across large-scale farming systems, reinforcing demand for mechanism configurations that support both high operational accuracy and low downtime during critical harvesting periods.

The sustained commercial preference for hydraulic systems within Brazil's harvesting equipment fleet is also reinforced by their compatibility with the precision farming technologies increasingly integrated into commercial combine platforms. Hydraulic harvesting systems support the smooth and controllable machine movements required for accurate GPS-guided field coverage and consistent header performance across varying crop densities and field terrain conditions. As the Brazil combine harvester market continues expanding and the operational expectations placed on harvesting equipment become more technologically sophisticated, hydraulic configurations are projected to maintain their dominant mechanism share through 2032, supported by their established reliability record and their structural compatibility with next-generation combine harvesters being deployed across Brazil's commercial grain belt.

List of Companies Covered in Brazil Combine Harvester Market

The companies listed below are highly influential in the Brazil combine harvester market, with a significant market share and a strong impact on industry developments.

- Valtra Brasil

- SLC Maquinas

- CLAAS America Latina

- John Deere Brasil

- AGCO do Brasil

- New Holland Agriculture Brasil

- Case IH Brasil

- Massey Ferguson Brasil

- Fendt Brasil

- Komatsu Forest Brasil

Market News & Updates

- John Deere Brasil, 2026:

John Deere introduced expanded agricultural automation technologies during Casa John Deere 2026 in Brazil, including upgrades across precision agriculture equipment and integrated digital solutions designed to improve operational efficiency and harvesting productivity. The launch strengthened the company’s advanced harvesting and connected farming portfolio for large-scale Brazilian agricultural operations.

- AGCO do Brasil, 2025:

AGCO expanded its harvesting and smart farming technology portfolio through new automation and intelligent machinery developments showcased for its Massey Ferguson, Fendt, and Valtra brands. The update included advanced harvesting technologies, mixed-fleet management capabilities, and AI-enabled agricultural solutions intended to improve harvesting efficiency and digital farm operations, supporting AGCO’s combine harvester positioning in Brazil and South America.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- Brazil Combine Harvester Market Policies, Regulations, and Standards

- Brazil Combine Harvester Production (Thousand Ton) Trend 2022-2032

- Brazil Combine Harvester Production (Thousand Ton) Trend By Type

- Self-propelled

- Tractor-pulled Combine

- PTO-powered Combine

- Company Wise Production Plants and Statistics

- Installed Production Capacity

- Actual Production

- Planned Production Target

- Brazil Combine Harvester Production (Thousand Ton) Trend By Type

- Brazil Combine Harvester Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- Brazil Combine Harvester Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold (Thousand Units)

- Market Segmentation & Growth Outlook

- By Type

- Self-propelled- Market Insights and Forecast 2022-2032, USD Million

- Tractor-pulled Combine- Market Insights and Forecast 2022-2032, USD Million

- PTO-powered Combine- Market Insights and Forecast 2022-2032, USD Million

- By Mechanism

- Hydraulic- Market Insights and Forecast 2022-2032, USD Million

- Hybrid- Market Insights and Forecast 2022-2032, USD Million

- By Power

- Below 150 HP- Market Insights and Forecast 2022-2032, USD Million

- 150-300 HP- Market Insights and Forecast 2022-2032, USD Million

- 300-450 HP- Market Insights and Forecast 2022-2032, USD Million

- 450-550 HP- Market Insights and Forecast 2022-2032, USD Million

- Above 550 HP- Market Insights and Forecast 2022-2032, USD Million

- By Class

- Class 1-2- Market Insights and Forecast 2022-2032, USD Million

- Class 3-4- Market Insights and Forecast 2022-2032, USD Million

- Class 5-6- Market Insights and Forecast 2022-2032, USD Million

- Class 7 & Above- Market Insights and Forecast 2022-2032, USD Million

- By Grain Tank Size

- < 250 bu- Market Insights and Forecast 2022-2032, USD Million

- 250-350 bu- Market Insights and Forecast 2022-2032, USD Million

- > 350 bu- Market Insights and Forecast 2022-2032, USD Million

- By Region

- North- Market Insights and Forecast 2022-2032, USD Million

- Center-West- Market Insights and Forecast 2022-2032, USD Million

- Northeast- Market Insights and Forecast 2022-2032, USD Million

- Southeast- Market Insights and Forecast 2022-2032, USD Million

- South- Market Insights and Forecast 2022-2032, USD Million

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Type

- Market Size & Growth Outlook

- Brazil Self-propelled Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold (Thousand Units)

- Market Segmentation & Growth Outlook

- By Mechanism- Market Insights and Forecast 2022-2032, USD Million

- By Power- Market Insights and Forecast 2022-2032, USD Million

- By Class- Market Insights and Forecast 2022-2032, USD Million

- By Grain Tank Size- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Brazil Tractor-pulled Combine Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold (Thousand Units)

- Market Segmentation & Growth Outlook

- By Mechanism- Market Insights and Forecast 2022-2032, USD Million

- By Power- Market Insights and Forecast 2022-2032, USD Million

- By Class- Market Insights and Forecast 2022-2032, USD Million

- By Grain Tank Size- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Brazil PTO-powered Combine Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold (Thousand Units)

- Market Segmentation & Growth Outlook

- By Mechanism- Market Insights and Forecast 2022-2032, USD Million

- By Power- Market Insights and Forecast 2022-2032, USD Million

- By Class- Market Insights and Forecast 2022-2032, USD Million

- By Grain Tank Size- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- John Deere Brasil

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- AGCO do Brasil

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- New Holland Agriculture Brasil

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Case IH Brasil

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Massey Ferguson Brasil

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Valtra Brasil

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- SLC Maquinas

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- CLAAS America Latina

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Fendt Brasil

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Komatsu Forest Brasil

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- John Deere Brasil

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Type |

|

| By Mechanism |

|

| By Power |

|

| By Class |

|

| By Grain Tank Size |

|

| By Region |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.