Brazil Forestry Machinery Market Report: Trends, Growth and Forecast (2026-2032)

By Equipment Type (Felling Equipment (Chainsaw, Harvester, Feller Buncher), Extracting Equipment (Forwarder, Skidder), On-Site Processing Equipment (Chipper, Delimber), Other Forestry Equipment (Loader, Mulcher)), By Power Source (Diesel, Hybrid, Battery-Electric), By Automation Level (Manual, Semi-Autonomous, Fully Autonomous), By End User (Contract Logging Firms, Forest Ownership Groups, Pulp and Paper Companies), By Region (North, Center-West, Northeast, Southeast, South) ... Read more

|

Major Players

|

Brazil Forestry Machinery Market Statistics and Insights, 2026

- Market Size Statistics

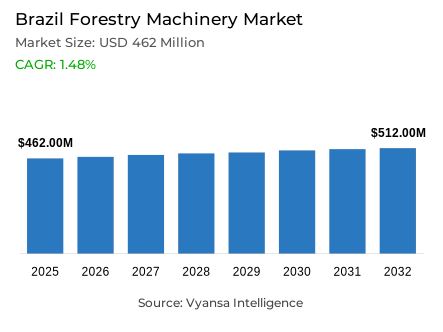

- Forestry machinery market size in Brazil was valued at USD 462 million in 2025 and is estimated at USD 473 million in 2026.

- The market size is expected to grow to USD 512 million by 2032.

- Market to register a CAGR of around 1.48% during 2026-32.

- Equipment Type Shares

- Felling equipment grabbed market share of 45%.

- Competition

- More than 10 companies are actively engaged in producing forestry machinery in Brazil.

- Top 5 companies acquired around 55% of the market share.

- Husqvarna, Caterpillar, Valmet, John Deere, Komatsu Forest etc., are few of the top companies.

- Power Source

- Diesel grabbed 80% of the market.

Brazil Forestry Machinery Market Outlook

The Brazil forestry machinery market was valued at USD 462 million in 2025 and is projected to advance from USD 473 million in 2026 to USD 512 million by 2032, registering a CAGR of 1.48% during the forecast period. This steady growth trajectory reflects the structural continuity of Brazil's planted forest economy, where eucalyptus and pine plantation operations across pulpwood, timber, charcoal, and industrial wood supply chains generate recurring and operationally consistent demand for mechanized felling, skidding, forwarding, loading, debarking, and chipping equipment. Growth remains moderate as fleet buyers prioritise reliability and adopt machinery where productivity gains demonstrably justify capital expenditure, creating a demand environment shaped by careful replacement cycles rather than aggressive expansion.

Felling Equipment commands approximately 45% share within the equipment type category, a position anchored by the foundational role that harvesters, feller bunchers, cutting heads, and chainsaw systems occupy as the primary machinery enabling tree cutting across Brazil's commercial plantation forestry sector. The dominance of this segment reflects the operational logic of eucalyptus and pine harvesting, where fast, safe, and consistent cutting at the first stage of the forestry value chain directly determines downstream productivity across forwarding, loading, and transport operations.

Diesel-powered configurations hold approximately 80% share within the power source category, sustained by the heavy-load demands, long operating shift requirements, and remote plantation site conditions that make diesel machinery the most practically reliable configuration for feller bunchers, skidders, loaders, forwarders, and harvesters deployed across Brazil's large-scale silviculture operations. Charging infrastructure limitations and the operational durability requirements of commercial forestry environments ensure diesel configurations retain their dominant share position through the forecast period.

Brazil's silviculture sector provides the structural demand foundation that sustains the Brazil forestry machinery market across all forecast years. As per data published by the Brazilian Institute of Geography and Statistics, Brazil's forestry production value reached a record BRL 44.3 billion in 2024, representing a 16.7% increase compared to 2023, with silviculture accounting for 84.1% of the total at BRL 37.2 billion, a figure that reinforces the scale and commercial depth of planted forest activity driving mechanized equipment demand through 2032.

Brazil Forestry Machinery Market Growth Driver

Silviculture Expansion and Record Forestry Output Anchoring Mechanized Equipment Demand

The primary commercial driver within the Brazil forestry machinery market is the country's expanding silviculture economy, where record forestry production values and the continued growth of industrial planted forest operations are generating sustained and measurable demand for mechanized harvesting, loading, forwarding, and transport equipment across eucalyptus and pine plantation systems. According to statistics released by the Brazilian Institute of Geography and Statistics in late 2025, Brazil's forest production reached a record high of BRL 44.3 billion in 2024, a 16.7% increase compared to 2023, while silviculture represented 84.1% of total forestry production value at BRL 37.2 billion, a concentration that confirms planted forest activity as the dominant and most commercially consequential demand source for forestry machinery across the country. This output scale places continuous operational pressure on harvesting infrastructure, where mechanized equipment is the only viable means of achieving the cutting speed, wood recovery rates, and operator safety standards required across large commercial plantation operations.

Plantation forestry and industrial wood supply chains represent the strongest and most structurally reliable demand segments within this driver context, as pulp and paper operators, charcoal producers, and timber processors collectively require reliable felling machines, loaders, forwarders, skidders, and chippers that minimise downtime, improve cutting accuracy, and support continuous wood flow across active harvesting cycles. Brazil forestry mechanization has progressed to the point where large plantation owners and contractors measure competitiveness in terms of harvesting precision and uptime rather than labor cost alone, reinforcing investment in advanced mechanized logging solutions as a commercial necessity rather than a discretionary upgrade across the country's most productive silviculture regions.

Brazil Forestry Machinery Market Challenge

Environmental Compliance Obligations Elevating Operational Risk Across Forestry Activities

Environmental compliance represents the most structurally consequential challenge currently facing machinery buyers and forestry contractors operating within the Brazil forestry machinery market, as strengthening deforestation monitoring frameworks are progressively increasing documentation, traceability, and land-use verification burdens across timber harvesting and transport operations throughout the country. Evidence drawn from public data released by Brazil's federal government confirms that official deforestation in the Legal Amazon fell 11.08% in 2025 to 5,796 square kilometres, while Cerrado deforestation fell 11.49% to 7,235.27 square kilometres, figures that reflect an increasingly active regulatory environment in which forestry operators must demonstrate continuous compliance with authorized land-use boundaries and legal timber sourcing requirements. While reduced deforestation reflects positive conservation outcomes, the intensified monitoring infrastructure that produces these results simultaneously increases the compliance obligations placed on every stage of commercial forestry operations.

The practical consequence for the Brazil forestry machinery market is that felling equipment, skidders, loaders, and transport machinery must now be demonstrably deployed within authorized planted forests or legally permitted timber operations, with documentation requirements extending across harvesting permits, transport authorisations, and contractor compliance records. Any operational link with illegal wood movement exposes buyers and contractors to fines, equipment seizure risk, project delays, and reputational damage that can materially affect commercial relationships with downstream pulp, paper, and timber buyers. This compliance burden increases the administrative complexity and operational risk profile of machinery deployment, particularly for smaller contractors whose documentation management capacity may be limited, and represents a persistent structural constraint on the pace and breadth of mechanized forestry expansion across Brazil's environmentally sensitive forest regions.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Brazil Forestry Machinery Market Trend

Diesel Fleet Modernization Defining Brazil's Forestry Energy Transition Pathway

The dominant operational trend within the Brazil forestry machinery market is the progressive modernization of diesel-powered forestry equipment rather than a rapid transition toward full electrification, a trajectory shaped by the practical realities of remote plantation environments where charging infrastructure remains limited and where operational reliability across heavy-load, long-shift harvesting cycles remains the primary purchasing criterion for fleet buyers. Diesel systems retain approximately 80% power source share because forestry sites across Brazil's eucalyptus and pine plantation zones require sustained high torque output, extended operating range, and field-service familiarity that current electric and hybrid alternatives cannot consistently deliver at commercial scale across demanding tropical terrain conditions. Fleet modernization is therefore proceeding through incremental improvements in diesel engine efficiency, emissions performance, and machine intelligence rather than through wholesale power source transition.

Brazil's national energy policy is shaping this modernization trend through biodiesel blending rather than electrification mandates, creating a cleaner combustion pathway for heavy forestry fleets without requiring infrastructure investment that remote plantation environments cannot yet support. Based on data from Brazil's federal government, the National Biodiesel Program has produced 77 billion liters of biodiesel over 20 years, avoided 240 million tonnes of CO₂ emissions, and generated USD 38 billion in import savings, a policy achievement that positions biodiesel-blended diesel as the most commercially practical near-term sustainability solution for Brazil's forestry machinery sector. As GPS-enabled forestry machinery, telematics integration, and predictive maintenance systems become more widely adopted across commercial plantation fleets, the modernization trend is expected to combine incremental environmental improvement with measurable productivity and uptime gains through the forecast period.

Brazil Forestry Machinery Market Opportunity

Pulpwood Expansion and Fleet Replacement Cycles Creating Targeted Equipment Demand

The most commercially immediate opportunity within the Brazil forestry machinery market is concentrated in mechanized harvesting for pulpwood and high-volume industrial wood operations, where the structural dominance of silviculture within Brazil's forestry economy creates a large and commercially defined addressable base for equipment suppliers offering feller bunchers, harvesters, cutting heads, skidders, forwarders, loaders, debarkers, and chippers that deliver measurable improvements in productivity, fuel efficiency, and operational uptime. As indicated by authoritative sources at the Brazilian Institute of Geography and Statistics, silviculture represented 84.1% of Brazil's total forestry production value in 2024, a concentration that confirms the pulpwood and planted forest segment as the primary commercial arena within which equipment replacement and modernization investment decisions are made. Pulp and paper operators in particular require machinery that reduces downtime, improves cutting accuracy, and supports continuous wood flow across high-volume harvesting cycles, creating a demand profile that favours technically advanced and reliability-proven equipment configurations.

Replacement demand represents the most structurally accessible component of this opportunity, driven by ageing fleet inventories across commercial plantation operations where older equipment configurations can no longer meet the productivity, fuel efficiency, safety, or uptime standards required by competitive industrial wood supply chains. Forestry fleet modernization trends across Brazil's most productive silviculture regions in Mato Grosso, Paraná, and Minas Gerais are progressively creating procurement opportunities for equipment manufacturers and distributors whose product portfolios address both the operational performance requirements of large-scale plantation harvesting and the environmental compliance expectations of downstream buyers in pulp, paper, and timber export markets.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Brazil Forestry Machinery Market Segmentation Analysis

By Equipment Type

- Felling Equipment

- Chainsaw

- Harvester

- Feller Buncher

- Extracting Equipment

- Forwarder

- Skidder

- On-Site Processing Equipment

- Chipper

- Delimber

- Other Forestry Equipment

- Loader

- Mulcher

Felling Equipment accounts for approximately 45% share within the equipment type category across the Brazil forestry machinery market, a dominance grounded in the operational primacy of tree cutting as the first and most critical stage of mechanized forestry value chains, where the speed, precision, and safety of felling activity directly determines the productivity of every downstream operation from forwarding through to processing and transport. Harvesters, feller bunchers, cutting heads, and chainsaw-based systems collectively form the core machinery through which Brazil's commercial eucalyptus and pine plantation operators convert standing timber into extractable log volumes, and the commercial logic of plantation forestry where fast cutting cycles, lower manual risk, and high wood recovery are the primary operational measures reinforces consistent and sustained procurement demand for this equipment category. Industry findings suggest that plantation owners and contractors across Brazil's major silviculture regions consistently direct the largest share of machinery investment toward felling configurations because improvements at the cutting stage generate compounding productivity benefits across the entire harvesting chain.

Within the Brazil forestry machinery market, the commercial strength of felling equipment is further reinforced by the growth of pulpwood operations across eucalyptus plantations in Minas Gerais and Mato Grosso, where high-rotation harvesting cycles create recurring replacement demand for cutting heads, chainsaw systems, and harvester attachments that wear under intensive use. As Brazil's silviculture economy continues expanding and industrial wood supply chains place greater emphasis on harvesting precision, operator safety compliance, and cutting efficiency, felling equipment is projected to retain its dominant share position throughout the forecast period, supported by ongoing investment in mechanized logging solutions and the progressive adoption of GPS-enabled and telematics-integrated harvesting configurations across commercial plantation fleets.

By Power Source

- Diesel

- Hybrid

- Battery-Electric

Diesel-powered configurations account for approximately 80% share within the power source category across the Brazil forestry machinery market, a position that reflects the non-negotiable operational requirements of large-scale plantation forestry, where heavy loads, uneven terrain, extended operating shifts, and remote site conditions make diesel machinery the only commercially viable power source for continuous, high-productivity harvesting and extraction activity. Feller bunchers, skidders, loaders, forwarders, and harvesters deployed across Brazil's eucalyptus and pine plantation zones rely on diesel engines for their high torque output, long operating range, and established field-service support networks that enable rapid maintenance and minimise downtime during active harvesting cycles. Validated reports from Brazil's federal government confirm that the National Biodiesel Program has produced 77 billion liters of biodiesel over 20 years, supporting cleaner diesel-blend utilisation across heavy forestry fleets while combustion-based configurations remain operationally dominant.

The sustained preference for diesel systems within the Brazil forestry machinery market is reinforced by the service infrastructure that has developed around combustion-based equipment across the country's major forestry regions, where spare-part availability, maintenance expertise, and fuelling logistics are comprehensively structured around diesel machinery. While hybrid forestry equipment and low-emission forestry machinery are receiving increasing manufacturer attention, the remote plantation conditions that characterise active forestry operations across Mato Grosso, Paraná, and southern Brazil present infrastructure preconditions for alternative power adoption that remain unmet across the majority of commercially active sites. Diesel configurations are therefore projected to maintain their dominant power source share well through 2032, with fleet modernization proceeding through fuel-efficient engine upgrades and biodiesel-blend adoption rather than structural power source transition.

List of Companies Covered in Brazil Forestry Machinery Market

The companies listed below are highly influential in the Brazil forestry machinery market, with a significant market share and a strong impact on industry developments.

- Husqvarna

- Caterpillar

- Valmet

- John Deere

- Komatsu Forest

- Ponsse

- Tigercat

- STIHL

- FAE

- Sotreq

Market News & Updates

- John Deere, 2025:

John Deere launched its new H Series forestry machines, including the 1270H and 1470H harvesters and the 2010H and 2510H forwarders. The updated range features enhanced hydraulics, advanced automation systems, redesigned booms, and fuel-efficiency improvements aimed at increasing operational productivity in mechanized forestry applications. The launch expands John Deere’s portfolio for large-scale forestry operations, including plantation forestry environments relevant to Brazil.

- Komatsu Forest, 2025:

Komatsu Forest introduced the new Komatsu 898 forwarder, developed for plantation forestry operations in South America, including Brazil. The machine includes a higher load capacity of 25 tonnes, upgraded transmission, larger load space, and configurable wheel options designed for high-volume timber extraction. The product expansion supports large-scale plantation harvesting operations and improves efficiency in demanding forestry environments.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- Brazil Forestry Machinery Market Policies, Regulations, and Standards

- Brazil Forestry Machinery Production (Thousand Ton) Trend 2022-2032

- Brazil Forestry Machinery Production (Thousand Ton) Trend By Equipment Type

- Felling Equipment

- Extracting Equipment

- On-Site Processing Equipment

- Other Forestry Equipment

- Company Wise Production Plants and Statistics

- Installed Production Capacity

- Actual Production

- Planned Production Target

- Brazil Forestry Machinery Production (Thousand Ton) Trend By Equipment Type

- Brazil Forestry Machinery Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- Brazil Forestry Machinery Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold (Thousand Units)

- Market Segmentation & Growth Outlook

- By Equipment Type

- Felling Equipment- Market Insights and Forecast 2022-2032, USD Million

- Chainsaw- Market Insights and Forecast 2022-2032, USD Million

- Harvester- Market Insights and Forecast 2022-2032, USD Million

- Feller Buncher- Market Insights and Forecast 2022-2032, USD Million

- Extracting Equipment- Market Insights and Forecast 2022-2032, USD Million

- Forwarder- Market Insights and Forecast 2022-2032, USD Million

- Skidder- Market Insights and Forecast 2022-2032, USD Million

- On-Site Processing Equipment- Market Insights and Forecast 2022-2032, USD Million

- Chipper- Market Insights and Forecast 2022-2032, USD Million

- Delimber- Market Insights and Forecast 2022-2032, USD Million

- Other Forestry Equipment- Market Insights and Forecast 2022-2032, USD Million

- Loader- Market Insights and Forecast 2022-2032, USD Million

- Mulcher- Market Insights and Forecast 2022-2032, USD Million

- Felling Equipment- Market Insights and Forecast 2022-2032, USD Million

- By Power Source

- Diesel- Market Insights and Forecast 2022-2032, USD Million

- Hybrid- Market Insights and Forecast 2022-2032, USD Million

- Battery-Electric- Market Insights and Forecast 2022-2032, USD Million

- By Automation Level

- Manual- Market Insights and Forecast 2022-2032, USD Million

- Semi-Autonomous- Market Insights and Forecast 2022-2032, USD Million

- Fully Autonomous- Market Insights and Forecast 2022-2032, USD Million

- By End User

- Contract Logging Firms- Market Insights and Forecast 2022-2032, USD Million

- Forest Ownership Groups- Market Insights and Forecast 2022-2032, USD Million

- Pulp and Paper Companies- Market Insights and Forecast 2022-2032, USD Million

- By Region

- North- Market Insights and Forecast 2022-2032, USD Million

- Center-West- Market Insights and Forecast 2022-2032, USD Million

- Northeast- Market Insights and Forecast 2022-2032, USD Million

- Southeast- Market Insights and Forecast 2022-2032, USD Million

- South- Market Insights and Forecast 2022-2032, USD Million

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Equipment Type

- Market Size & Growth Outlook

- Brazil Felling Equipment Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold (Thousand Units)

- Market Segmentation & Growth Outlook

- By Power Source- Market Insights and Forecast 2022-2032, USD Million

- By Automation Level- Market Insights and Forecast 2022-2032, USD Million

- By Sales Type- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Brazil Extracting Equipment Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold (Thousand Units)

- Market Segmentation & Growth Outlook

- By Power Source- Market Insights and Forecast 2022-2032, USD Million

- By Automation Level- Market Insights and Forecast 2022-2032, USD Million

- By Sales Type- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Brazil On-Site Processing Equipment Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold (Thousand Units)

- Market Segmentation & Growth Outlook

- By Power Source- Market Insights and Forecast 2022-2032, USD Million

- By Automation Level- Market Insights and Forecast 2022-2032, USD Million

- By Sales Type- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Brazil Other Forestry Equipment Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold (Thousand Units)

- Market Segmentation & Growth Outlook

- By Power Source- Market Insights and Forecast 2022-2032, USD Million

- By Automation Level- Market Insights and Forecast 2022-2032, USD Million

- By Sales Type- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- John Deere

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Komatsu Forest

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Ponsse

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Tigercat

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- STIHL

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Husqvarna

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Caterpillar

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Valmet

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- FAE

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Sotreq

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- John Deere

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Equipment Type |

|

| By Power Source |

|

| By Automation Level |

|

| By End User |

|

| By Region |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.