South America Combine Harvester Market Report: Trends, Growth and Forecast (2026-2032)

By Type (Self-propelled, Tractor-pulled Combine, PTO-powered Combine), By Mechanism (Hydraulic, Hybrid), By Power (Below 150 HP, 150-300 HP, 300-450 HP, 450-550 HP, Above 550 HP), By Class (Class 1-2, Class 3-4, Class 5-6, Class 7 & Above), By Grain Tank Size (< 250 bu, 250-350 bu, > 350 bu), By Country (Brazil, Argentina, Chile, Peru, Ecuador, Colombia, Rest of South America) ... Read more

|

Major Players

|

South America Combine Harvester Market Statistics and Insights, 2026

- Market Size Statistics

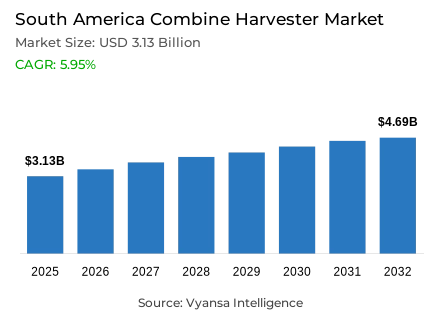

- Combine harvester market size in South America was valued at USD 3.13 billion in 2025 and is estimated at USD 3.22 billion in 2026.

- The market size is expected to grow to USD 4.69 billion by 2032.

- Market to register a CAGR of around 5.95% during 2026-32.

- Type Shares

- Self-propelled grabbed market share of 80%.

- Competition

- More than 10 companies are actively engaged in producing combine harvester in South America.

- Top 5 companies acquired around 70% of the market share.

- Case IH, New Holland Agriculture, CLAAS KGaA mbH, John Deere, AGCO Corporation etc., are few of the top companies.

- Mechanism

- Hydraulic grabbed 65% of the market.

- Country

- Brazil leads with a 50% share of the South America market.

South America Combine Harvester Market Outlook

The South America combine harvester market was valued at USD 3.13 billion in 2025 and is projected to advance from USD 3.22 billion in 2026 to USD 4.69 billion by 2032, registering a CAGR of 5.95% during the forecast period. This trajectory is anchored in the region's position as one of the world's most commercially significant grain-producing zones, where expanding cultivation of soybean, corn, and wheat continues to generate sustained and measurable demand for mechanized harvesting systems capable of managing vast cultivation areas within narrowing harvest windows.

Self-propelled combine harvesters account for approximately 80% of equipment deployed across South America's grain farming operations, reflecting the operational imperative of completing cutting, threshing, and grain collection within a single continuous pass. Large-scale commercial farms across Brazil and Argentina consistently favour these systems because they reduce total harvesting time, limit dependency on coordinated equipment fleets, and support efficient grain recovery across extensive cultivation areas during periods of peak agricultural activity.

Hydraulic mechanisms represent the dominant configuration within the mechanism category, commanding approximately 65% share across active harvesting fleets in the region. Their prevalence is driven by the superior operational control, machine handling flexibility, and field adaptability that hydraulic systems deliver across South America's diverse agricultural terrain, ranging from the expansive flatlands of Brazil's Cerrado to the Pampas of Argentina.

Brazil leads the regional market with approximately 52% share, supported by highly commercialised grain infrastructure and an intensive focus on export-oriented agricultural output. As per data published by the Food and Agriculture Organization, Brazil harvested more than 95 million hectares of agricultural crops in recent FAOSTAT datasets, reinforcing the structural depth of mechanized harvesting demand that continues to underpin South America's combine harvester industry across the forecast period.

South America Combine Harvester Market Growth Driver

Expanding Grain Production Volumes Drive Sustained Machinery Demand

The primary commercial driver within the South America combine harvester market is the region's sustained and large-scale grain production activity, which generates recurring and operationally critical demand for high-capacity harvesting machinery across Brazil and Argentina's expansive agricultural systems. According to statistics released by the World Bank, Brazil produced approximately 138.98 million tonnes of cereals in 2024, while the United States Department of Agriculture (USDA) Foreign Agricultural Service's Oilseeds: World Markets and Trade report confirmed that Brazil's soybean production reached 180 million metric tonnes in its most recent projections. These volumes place extraordinary operational pressure on harvesting infrastructure, where timely mechanized crop collection becomes non-negotiable to protect yield quality and reduce grain loss during critical post-maturity windows.

Expanding soybean cultivation and increasing corn production across the region further deepen this demand base, as agricultural mechanization South America-wide has become less a strategic investment and more a structural necessity for commercial viability. The dependence on high-capacity harvesting machinery is particularly acute because harvesting windows in South American grain farming are narrow, leaving inadequate time for manual or semi-mechanised collection across large cultivation areas. Rising farm equipment investments are being directed toward systems capable of sustained throughput under these conditions, and self-propelled combine harvesters with precision harvesting machinery capabilities are increasingly central to how large-scale operators manage their productivity obligations across the forecast period.

South America Combine Harvester Market Challenge

Financing Barriers and Farm Fragmentation Constrain Equipment Penetration

High acquisition costs represent the most structurally persistent challenge facing broader combine harvester adoption across South America, particularly among small and medium-scale farming operations that form the backbone of the region's agricultural holdings. According to official figures from the Inter-American Development Bank's report Family Farming in Latin America and the Caribbean, family farms account for nearly 81% of agricultural holdings across the region, a distribution that fundamentally limits mechanization penetration because fragmented landholding patterns reduce machinery utilization efficiency and weaken the financial case for individual equipment ownership.

Farm equipment financing challenges compound this constraint significantly. Based on data from the World Bank national accounts, agriculture contributes approximately 6.5% of GDP across Latin America and the Caribbean, yet rural financing access remains structurally uneven, with credit terms frequently misaligned with the seasonal and cyclical income patterns of smallholder producers. The South America combine harvester market therefore faces a sustained tension between the operational imperative for mechanized harvesting and the financial inaccessibility that keeps a significant portion of the farming population reliant on older, lower-capacity equipment or contract harvesting arrangements. Operational costs in mechanized harvesting remain elevated by fuel price volatility and machinery maintenance obligations, reinforcing the barriers that continue to suppress penetration in sub-commercial farming segments across the region.

Unlock Market Intelligence

Explore the market potential with our data-driven report

South America Combine Harvester Market Trend

Precision Agriculture Technologies Reshaping Harvesting Equipment Capabilities

A structurally consequential transformation is underway across South America's commercial farming sector, where precision agriculture integration is progressively redefining the functional expectations placed on combine harvesting equipment. GPS-guided harvesting systems, automated steering controls, and yield monitoring systems are no longer features associated exclusively with premium equipment tiers but are becoming baseline operational requirements across large-scale grain farms in Brazil and Argentina. Evidence drawn from public data released by the OECD Agricultural Policy Monitoring and Evaluation 2024 report confirms that Brazil has formally institutionalised precision farming adoption through the National Policy for Incentives on Precision Agriculture and Livestock under Law No. 14,475, with the majority of rural credit lines in the country now financing precision farming equipment acquisition.

This policy environment has materially accelerated the pace at which AI-enabled combine harvesters and sensor-based agricultural machinery are being introduced into active commercial fleets. IoT-enabled combine harvesters equipped with real-time farm monitoring capabilities are increasingly deployed across Brazil's soybean and corn belts, where data-driven farming equipment allows operators to dynamically adjust harvesting parameters, reduce grain loss, and improve throughput efficiency across large continuous cultivation areas. The South America combine harvester market is responding to this demand shift with a growing portfolio of connected agricultural machinery systems, positioning the region's commercial farming sector at the intersection of agricultural scale and digital operational sophistication through the forecast period.

South America Combine Harvester Market Opportunity

Post-Harvest Loss Reduction Programmes Opening Mechanization Investment Pathways

Reducing post-harvest grain losses represents one of the most commercially significant and policy-supported opportunities currently available within the South America combine harvester market, providing a clear and quantifiable rationale for expanded mechanized harvesting investment across the region's grain production systems. As indicated by authoritative sources at the Food and Agriculture Organization, global grain post-harvest losses range between 10% and 20%, a loss band that translates into substantial economic and food security consequences for a region whose agricultural export revenues are structurally dependent on grain volume and quality at point of delivery. This figure creates a measurable commercial justification for upgrading harvesting infrastructure beyond what productivity arguments alone might support.

Expanding export-oriented farming across Brazil and Argentina further strengthens this opportunity, as international grain buyers increasingly apply quality and traceability standards that are difficult to meet through mechanically unreliable or operationally outdated harvesting systems. Data compiled from internationally recognised public authorities at the Economic Commission for Latin America and the Caribbean confirms that agriculture remains one of the region's primary export-generating sectors, and that sustained investment in mechanized agricultural infrastructure is directly tied to South America's long-term competitiveness in global grain markets. Agricultural automation technologies that reduce harvesting losses, improve grain separation quality, and accelerate field-to-storage cycles represent the most commercially immediate pathway for equipment manufacturers and operators seeking to align with this expanding export demand structure.

South America Combine Harvester Market Country Analysis

By Country

- Brazil

- Argentina

- Chile

- Peru

- Ecuador

- Colombia

- Rest of South America

Brazil leads the South America combine harvester market with approximately 52% share, a position supported by the country's unmatched combination of agricultural land scale, commercialised grain farming infrastructure, and sustained export-oriented production volumes. As per official figures from FAO FAOSTAT, Brazil harvested more than 95 million hectares of agricultural crops in recent datasets, while the USDA Grain and Feed Annual report highlights continued expansion in Brazil's grain production systems through 2024 and 2025. Strong precision farming adoption, favourable rural credit policy, and a large installed base of commercial farming operations continue to reinforce Brazil's structural leadership in regional combine harvester deployment and fleet modernisation.

Argentina represents the region's second most commercially significant market, anchored by its intensive soybean and corn production systems across the Pampas agricultural zone, where large-scale operations generate consistent demand for high-horsepower harvesting machinery. Industry findings suggest that mechanized corn harvesting in Argentina and Paraguay's grain harvesting machinery sector are both expanding as export-oriented grain farming extends beyond Brazil's immediate agricultural footprint. Uruguay and Chile contribute at a smaller scale, with agricultural modernization in Latin America creating gradual mechanisation momentum across both economies. Collectively, the structural growth of South America's grain export sector, combined with increasing adoption of connected agricultural machinery systems and government support for farm mechanization, positions the regional market for sustained combine harvester demand expansion through 2032.

Unlock Market Intelligence

Explore the market potential with our data-driven report

South America Combine Harvester Market Segmentation Analysis

By Type

- Self-propelled

- Tractor-pulled Combine

- PTO-powered Combine

Self-propelled combine harvesters account for approximately 80% of equipment deployed within the Type category across South America's grain farming sector, a dominance that reflects the operational logic of large-scale commercial agriculture where harvesting efficiency is measured in hectares per hour rather than equipment unit cost. These machines consolidate cutting, threshing, separation, and grain collection into a single continuous operation, removing the coordination complexity associated with tractor-mounted or PTO-powered configurations and enabling uninterrupted field coverage across the extensive cultivation areas that characterise Brazil and Argentina's primary grain-producing zones. In line with findings from FAOSTAT, Brazil's soybean crop area exceeded 48.5 million hectares in recent datasets, a figure that illustrates the scale of harvesting demand that self-propelled systems are uniquely positioned to address.

Within the South America combine harvester market, the commercial preference for self-propelled systems is further reinforced by their compatibility with precision harvesting machinery technologies including GPS-guided harvesting, automated steering, and real-time yield monitoring, which are most effectively integrated into purpose-built self-propelled platforms. As grain farming operations across the region continue expanding their cultivated areas and intensifying their focus on reducing harvesting losses and improving throughput speed, self-propelled combine harvesters are expected to consolidate their share position throughout the forecast period, supported by ongoing investment in connected agricultural machinery and high-capacity harvesting equipment across Brazil and Argentina's commercial farming systems.

By Mechanism

- Hydraulic

- Hybrid

Hydraulic combine harvesters account for approximately 65% of active equipment configurations within the Mechanism category across the South America combine harvester market, a share position grounded in the measurable operational advantages that hydraulic systems deliver across the diverse and demanding field conditions prevalent in South American grain farming. Hydraulic mechanisms provide superior machine handling, smoother directional control, and responsive adjustment capability across varying terrain, making them highly effective for continuous harvesting operations across both the flat expanses of Brazil's agricultural interior and the variable topography encountered in other major grain-producing regions of the continent. Validated reports from the USDA Economic Research Service confirm that precision-enabled agricultural machinery adoption continues to increase across large-scale farming operations, reinforcing demand for mechanism configurations that support higher operational accuracy and reduced downtime.

The operational resilience of hydraulic systems also contributes to their sustained commercial preference in an environment where machinery downtime in farming carries significant financial consequence during narrow harvesting windows. Hydraulic configurations enable faster field adaptation and more consistent equipment performance under the intensive utilisation cycles that characterise peak harvest periods across South America's commercial grain sector. As agricultural mechanization South America-wide continues advancing, and as grain farming operations expand both in scale and in the operational complexity of their harvesting requirements, hydraulic systems are projected to retain their dominant configuration position throughout the forecast period, supported by their compatibility with high-capacity harvesting equipment and advanced grain separation systems.

Various Market Players in South America Combine Harvester Market

The companies mentioned below are highly active in the South America combine harvester market, occupying a considerable portion of the market and shaping industry progress.

- Case IH

- New Holland Agriculture

- CLAAS KGaA mbH

- John Deere

- AGCO Corporation

- Massey Ferguson

- Valtra

- CNH Industrial N.V.

- SDF Group (Deutz-Fahr)

- Kubota Corporation

- Yanmar Holdings Co. Ltd.

- Metalfor S.A.

Market News & Updates

- John Deere, 2025:

John Deere expanded availability and field deployment of its S7 Series combines across major grain-producing markets, including South America, with upgraded predictive harvesting automation, enhanced grain-loss sensing, and improved fuel-efficiency systems. The combines introduced predictive ground speed automation and integrated precision harvesting technologies designed to improve soybean and corn harvesting efficiency under varying crop conditions common across Brazil and Argentina.

- Case IH, 2025:

Case IH advanced its Axial-Flow AF Series combine platform with the AF9 and AF10 models featuring higher horsepower, larger grain tanks, upgraded rotor systems, and enhanced Harvest Command automation technology. The combines were developed for high-capacity grain harvesting operations and support large-scale soybean, corn, and wheat harvesting applications relevant to commercial farming operations across South America.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- South America Combine Harvester Market Policies, Regulations, and Standards

- South America Combine Harvester Production (Thousand Ton) Trend 2022-2032

- South America Combine Harvester Production (Thousand Ton) Trend By Type

- Self-propelled

- Tractor-pulled Combine

- PTO-powered Combine

- Company Wise Production Plants and Statistics

- Installed Production Capacity

- Actual Production

- Planned Production Target

- South America Combine Harvester Production (Thousand Ton) Trend By Type

- South America Combine Harvester Pricing Analysis 2022-2032

- South America Combine Harvester Pricing Trend (Units) 2022-2032

- South America Combine Harvester Pricing Trend (Units) By Regions 2022-2032

- Brazil

- Argentina

- Chile

- Peru

- Ecuador

- Colombia

- South America Combine Harvester Pricing Trend (Units) By Type 2022-2032

- Self-propelled

- Tractor-pulled Combine

- PTO-powered Combine

- South America Combine Harvester Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- South America Combine Harvester Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold (Thousand Units)

- Market Segmentation & Growth Outlook

- By Type

- Self-propelled- Market Insights and Forecast 2022-2032, USD Million

- Tractor-pulled Combine- Market Insights and Forecast 2022-2032, USD Million

- PTO-powered Combine- Market Insights and Forecast 2022-2032, USD Million

- By Mechanism

- Hydraulic- Market Insights and Forecast 2022-2032, USD Million

- Hybrid- Market Insights and Forecast 2022-2032, USD Million

- By Power

- Below 150 HP- Market Insights and Forecast 2022-2032, USD Million

- 150-300 HP- Market Insights and Forecast 2022-2032, USD Million

- 300-450 HP- Market Insights and Forecast 2022-2032, USD Million

- 450-550 HP- Market Insights and Forecast 2022-2032, USD Million

- Above 550 HP- Market Insights and Forecast 2022-2032, USD Million

- By Class

- Class 1-2- Market Insights and Forecast 2022-2032, USD Million

- Class 3-4- Market Insights and Forecast 2022-2032, USD Million

- Class 5-6- Market Insights and Forecast 2022-2032, USD Million

- Class 7 & Above- Market Insights and Forecast 2022-2032, USD Million

- By Grain Tank Size

- < 250 bu- Market Insights and Forecast 2022-2032, USD Million

- 250-350 bu- Market Insights and Forecast 2022-2032, USD Million

- > 350 bu- Market Insights and Forecast 2022-2032, USD Million

- By Country

- Brazil

- Argentina

- Chile

- Peru

- Ecuador

- Colombia

- Rest of South America

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Type

- Market Size & Growth Outlook

- Brazil Combine Harvester Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold (Thousand Units)

- Market Segmentation & Growth Outlook

- By Type- Market Insights and Forecast 2022-2032, USD Million

- By Mechanism- Market Insights and Forecast 2022-2032, USD Million

- By Power- Market Insights and Forecast 2022-2032, USD Million

- By Class- Market Insights and Forecast 2022-2032, USD Million

- By Grain Tank Size- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Argentina Combine Harvester Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold (Thousand Units)

- Market Segmentation & Growth Outlook

- By Type- Market Insights and Forecast 2022-2032, USD Million

- By Mechanism- Market Insights and Forecast 2022-2032, USD Million

- By Power- Market Insights and Forecast 2022-2032, USD Million

- By Class- Market Insights and Forecast 2022-2032, USD Million

- By Grain Tank Size- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Chile Combine Harvester Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold (Thousand Units)

- Market Segmentation & Growth Outlook

- By Type- Market Insights and Forecast 2022-2032, USD Million

- By Mechanism- Market Insights and Forecast 2022-2032, USD Million

- By Power- Market Insights and Forecast 2022-2032, USD Million

- By Class- Market Insights and Forecast 2022-2032, USD Million

- By Grain Tank Size- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Peru Combine Harvester Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold (Thousand Units)

- Market Segmentation & Growth Outlook

- By Type- Market Insights and Forecast 2022-2032, USD Million

- By Mechanism- Market Insights and Forecast 2022-2032, USD Million

- By Power- Market Insights and Forecast 2022-2032, USD Million

- By Class- Market Insights and Forecast 2022-2032, USD Million

- By Grain Tank Size- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Ecuador Combine Harvester Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold (Thousand Units)

- Market Segmentation & Growth Outlook

- By Type- Market Insights and Forecast 2022-2032, USD Million

- By Mechanism- Market Insights and Forecast 2022-2032, USD Million

- By Power- Market Insights and Forecast 2022-2032, USD Million

- By Class- Market Insights and Forecast 2022-2032, USD Million

- By Grain Tank Size- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Colombia Combine Harvester Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Units Sold (Thousand Units)

- Market Segmentation & Growth Outlook

- By Type- Market Insights and Forecast 2022-2032, USD Million

- By Mechanism- Market Insights and Forecast 2022-2032, USD Million

- By Power- Market Insights and Forecast 2022-2032, USD Million

- By Class- Market Insights and Forecast 2022-2032, USD Million

- By Grain Tank Size- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- John Deere

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- AGCO Corporation

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Massey Ferguson

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Valtra

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- CNH Industrial N.V.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Case IH

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- New Holland Agriculture

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- CLAAS KGaA mbH

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- SDF Group (Deutz-Fahr)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Kubota Corporation

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Yanmar Holdings Co. Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Metalfor S.A.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- John Deere

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Type |

|

| By Mechanism |

|

| By Power |

|

| By Class |

|

| By Grain Tank Size |

|

| By Country |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.