Southeast Asia Agricultural Machinery Market Report: Trends, Growth and Forecast (2026-2032)

By Type (Tractors (Horsepower (Less than 40 HP, 40 HP–99 HP, Greater than 100 HP), Tractor Type (Compact Utility Tractors, Utility Tractors, Row-Crop Tractors)), Plowing and Cultivating Machinery (Plows, Harrows, Cultivators and Tillers, Others), Planting Machinery (Seed Drills, Planters, Spreaders, Others), Harvesting Machinery (Combine Harvesters-Threshers, Forage Harvesters, Others), Haying and Forage Machinery (Mower-conditioners, Balers, Others), Irrigation Machinery (Sprinkler Irrigation, Drip Irrigation, Others), Others), By Application (Land Development & Seed Bed Preparation, Sowing & Planting, Weed Cultivation, Plant Protection, Harvesting & Threshing, Post-harvest & Agro Processing), By Automation (Automatic, Semi-automatic, Manual), By Country (Malaysia, Indonesia, Singapore, Cambodia, Vietnam, Thailand, Philippines, Rest of Southeast Asia) ... Read more

|

Major Players

|

Southeast Asia Agricultural Machinery Market Statistics and Insights, 2026

- Market Size Statistics

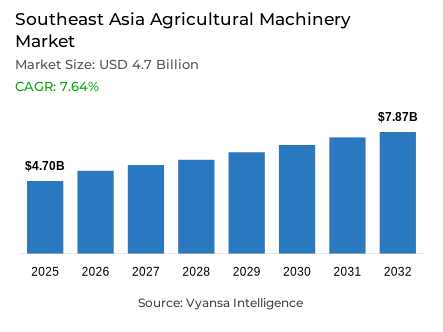

- Agricultural machinery market size in Southeast Asia was valued at USD 4.7 billion in 2025 and is estimated at USD 5.22 billion in 2026.

- The market size is expected to grow to USD 7.87 billion by 2032.

- Market to register a CAGR of around 7.64% during 2026-32.

- Type Shares

- Tractors grabbed market share of 35%.

- Competition

- More than 10 companies are actively engaged in producing agricultural machinery in Southeast Asia.

- Top 5 companies acquired around 70% of the market share.

- Yanmar Holdings Co. Ltd., CLAAS KGaA mbH, SDF Group, John Deere, Kubota Corporation etc., are few of the top companies.

- Automation

- Semi-automatic grabbed 55% of the market.

- Country

- Thailand leads with a 30% share of the Southeast Asia market.

Southeast Asia Agricultural Machinery Market Outlook

The Southeast Asia Agricultural Machinery Market was valued at USD 4.7 billion in 2025 and is projected to advance from USD 5.22 billion in 2026 to USD 7.87 billion by 2032, registering a CAGR of 7.64% during the forecast period. This expansion is structurally grounded in the region's deep agricultural dependency, where farming systems form the economic foundation of multiple national economies and where the gap between current mechanization levels and operational productivity requirements continues to widen under the pressure of rising food security needs and labor efficiency imperatives. Based on data from the World Bank, agriculture accounts for more than 30% of employment in several regional economies and contributes approximately 11% of GDP across developing East Asia and the Pacific, a structural weight that makes mechanization investment a national economic priority rather than a sectoral preference.

Tractors command approximately 35% share within the equipment category, a position anchored by their operational versatility across plowing, tilling, planting, and transport activities in rice, palm oil, and vegetable farming systems that collectively define the agricultural landscape across the Southeast Asia Agricultural Machinery Market. Their deployment spans both smallholder and commercial farm configurations, sustaining consistent procurement demand across labor-intensive cultivation cycles where tractor-based mechanization remains the most accessible and operationally practical entry point into farm modernization.

Semi-automatic systems hold nearly 55% share within the automation segment, reflecting the commercial logic of a region where fragmented landholdings and cost-sensitive farming conditions make full automation economically inaccessible for the majority of active farm operators. Semi-automatic tractors, harvesters, and irrigation systems reduce manual labor dependency while maintaining cost structures that remain manageable across small and medium-scale rice and plantation agriculture operations throughout the region.

Thailand leads the Southeast Asia Agricultural Machinery Market with approximately 30% share, supported by its large rice production base, export-oriented agricultural sector, and comparatively advanced mechanization infrastructure relative to other regional economies. As per data published by the Food and Agriculture Organization, sustained labor shortages and rising agricultural productivity pressures across Thailand and its neighboring economies continue reinforcing long-term machinery demand through 2032.

Southeast Asia Agricultural Machinery Market Growth Driver

Agricultural Productivity Focus and Labor Reduction Requirements

Rising agricultural productivity needs and labor reduction imperatives establish sustained demand for farm equipment throughout Southeast Asia. Statistics from World Bank confirm agriculture contributes approximately 11% of GDP across developing East Asia & Pacific while accounting for more than 30% employment in several Southeast Asian economies. This employment concentration directly translates into heightened relevance for mechanized solutions supporting labor efficiency. Growing productivity pressure ensures persistent equipment demand supporting improved farming outcomes throughout extended forecast period.

Rice production dominance and commercial farming expansion strengthen commercial foundation for agricultural machinery deployment. Published evidence from FAO indicates Southeast Asia produces approximately 194 million tonnes rice annually while region accounts for nearly 90% global rice production and consumption. This production scale creates opportunity for equipment suppliers developing solutions supporting large-scale cultivation. Food security imperatives ensure sustained machinery demand supporting enhanced regional food production across farming communities.

Southeast Asia Agricultural Machinery Market Challenge

High Equipment Costs and Rural Infrastructure Limitations

Southeast Asia agricultural machinery sector faces substantial challenge from high purchasing and maintenance costs restricting smallholder farmer adoption. Official records from FAO indicate small farms account for nearly 87% of Asian farmland, often defined as less than 2 hectares, establishing widespread capital constraints. This farm-size concentration creates operational barriers limiting equipment acquisition. Service providers must develop affordable solutions addressing capital investment barriers for smallholder systems.

Rural infrastructure deficit and financing limitation intensity adoption barriers for farm equipment. Evidence from regional analysis reveals many farming areas continue experiencing restricted access to machinery servicing, spare parts, farm credit, and fuel infrastructure affecting equipment viability. This infrastructure absence creates difficult operating environment affecting farmer confidence and equipment utilization. Manufacturers must develop solutions supporting feasible service and maintenance pathways throughout Southeast Asia agricultural sector.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Southeast Asia Agricultural Machinery Market Trend

Smart Farming and Precision Agriculture Technology Integration

Southeast Asia agricultural machinery sector demonstrates pronounced shift toward smart and precision farming technologies enabling productivity optimization. Market data from FAO indicates digital agriculture technologies expanding globally to improve productivity and resource management while Organisation for Economic Co-operation and Development (OECD)-FAO Agricultural Outlook notes South and Southeast Asia account for 39% global population yet only 12% agricultural land, establishing productivity imperative. This technology momentum directly supports expansion for GPS-enabled tractors and automated systems. Published evidence establishes agricultural productivity growth in Southeast Asia accounting for more than 60% output growth between 2001-2013.

Fuel-efficient equipment and technology-integrated machinery adoption strengthen industry-wide adoption of advanced farming solutions. Published data establishes manufacturers increasingly focusing on fuel-efficient technology-integrated equipment suitable for rice cultivation and plantation farming. This innovation focus supports expansion for smart irrigation systems, drones, and automated harvesting across Southeast Asia. Service providers developing technology-enabled and fuel-efficient solutions position themselves advantageously capturing growth opportunities throughout regional agricultural sector.

Southeast Asia Agricultural Machinery Market Opportunity

Mechanized Rice Cultivation and Post-Harvest Management System Expansion

Strong opportunities emerge in mechanized rice cultivation supporting large-scale production requirements. Official records from FAO reveal Southeast Asia produces approximately 194 million tonnes rice annually establishing substantial equipment demand for mechanization. This production scale creates commercial opportunity for equipment suppliers developing combine harvesters, rice transplanters, and threshers supporting large-scale operations. Rice production expansion directly enables accelerated machinery adoption across regional farming communities.

Government mechanization support and agribusiness investment strengthen commercial foundation for farm equipment deployment. Evidence indicates governments and agribusiness companies increasingly focusing on productivity improvement through mechanized farming practices with agriculture accounting for more than 30% employment across several Southeast Asian economies. This policy momentum creates sustained opportunity for machinery providers developing solutions supporting farming efficiency. Growing labor shortages and commercial agriculture activities ensure sustained equipment demand throughout extended forecast period.

Southeast Asia Agricultural Machinery Market Country Analysis

By Country

- Malaysia

- Indonesia

- Singapore

- Cambodia

- Vietnam

- Thailand

- Philippines

- Rest of Southeast Asia

Thailand emerges as leading regional market with 30% share within Southeast Asia agricultural machinery sector, reflecting strong rice cultivation sector and export-oriented agricultural economy. Official records from FAO reveal Thailand's rice production typically ranges between 32-34 million tonnes annually establishing substantial production base supporting equipment demand. This agricultural scale directly supports heightened machinery relevance throughout country. Thailand's rice sector prominence ensures continued regional leadership.

Agricultural export focus and mechanization adoption strengthen commercial foundation for Thailand agricultural machinery dominance. Published evidence from World Bank establishes agriculture contributes approximately 8% to Thailand's GDP while country remains major agricultural exporter with increasing tractor and harvester adoption supported by commercial farming activities. This export momentum creates sustained opportunity for equipment suppliers serving established farming channels and modernizing agricultural systems. Service providers developing Thailand-focused solutions addressing rice production requirements position themselves advantageously capturing regional leadership throughout Southeast Asia agricultural sector.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Southeast Asia Agricultural Machinery Market Segmentation Analysis

By Type

- Tractors

- Horsepower

- Less than 40 HP

- 40 HP–99 HP

- Greater than 100 HP

- Tractor Type

- Compact Utility Tractors

- Utility Tractors

- Row-Crop Tractors

- Horsepower

- Plowing and Cultivating Machinery

- Plows

- Harrows

- Cultivators and Tillers

- Others

- Planting Machinery

- Seed Drills

- Planters

- Spreaders

- Others

- Harvesting Machinery

- Combine Harvesters-Threshers

- Forage Harvesters

- Others

- Haying and Forage Machinery

- Mower-conditioners

- Balers

- Others

- Irrigation Machinery

- Sprinkler Irrigation

- Drip Irrigation

- Others

- Others

Tractors commands market leadership at 35% share within Southeast Asia agricultural machinery sector, establishing dominant equipment positioning through broad applicability supporting plowing, tilling, planting, and hauling across rice, sugarcane, palm oil, and vegetable operations. This segment maintains leading position due to tractor suitability for multiple farming applications improving operational efficiency, generating sustained demand for versatile solutions. Tractor delivery accessible positioning supporting routine farming applications while enabling productivity enhancement, establishing broad appeal across smallholder and commercial farmers globally.

This market leadership position reflects farming community's continued selection of tractors supporting essential work throughout agricultural lifecycles. Tractors remain important because agricultural mechanization continues increasing across Asia to improve labor productivity and cultivation efficiency while supporting multiple applications. The 35% share indicates this segment continues shaping equipment demand, manufacturer innovation focus, and operational structure throughout Southeast Asia agricultural sector. Manufacturers maintaining tractor leadership develop competitive advantages enabling broader market penetration and sustained revenue growth supporting diverse farming applications.

By Automation

- Automatic

- Semi-automatic

- Manual

The segment has the highest share around semi-automatic systems under the Automation category, accounting for 55% share. Semi-automatic agricultural machinery dominates across Southeast Asia because it provides a balance between operational efficiency and affordability for farmers managing medium-scale agricultural activities.

These systems are widely preferred as they reduce manual labor requirements while remaining more cost-effective than fully automated machinery. Semi-automatic equipment also suits the fragmented farming structures common across several Southeast Asian countries, where farmers require flexible and easy-to-operate machinery solutions. Growing adoption of mechanized farming practices across rice, palm oil, and plantation agriculture further supports demand for semi-automatic agricultural machinery throughout the region.

Various Market Players in Southeast Asia Agricultural Machinery Market

The companies mentioned below are highly active in the Southeast Asia agricultural machinery market, occupying a considerable portion of the market and shaping industry progress.

- Yanmar Holdings Co. Ltd.

- CLAAS KGaA mbH

- SDF Group

- John Deere

- Kubota Corporation

- CNH Industrial N.V.

- AGCO Corporation

- Mahindra & Mahindra Ltd.

- Iseki & Co. Ltd.

- Lovol Heavy Industry

- YTO Group Corporation

- Daedong Corporation

Market News & Updates

- Kubota Corporation, 2025:

Kubota continued expanding its agricultural machinery portfolio across Southeast Asia through its Thailand-based subsidiary Siam Kubota, highlighting upgraded combine harvester solutions for ASEAN rice farming operations. The company emphasized wider deployment of high-durability combine harvesters designed for rice cultivation conditions in Thailand, Myanmar, Indonesia, and the Philippines, supporting ongoing mechanization demand across Southeast Asian agricultural markets.

- Yanmar Holdings Co. Ltd, 2025:

Yanmar strengthened its smart agriculture activities in Southeast Asia through the launch of the “Chia Tai Experience” smart farming center in Thailand. The initiative introduced advanced agricultural technologies including Yanmar’s YR Series rice transplanter and smart farming solutions aimed at improving operational efficiency and sustainable rice cultivation practices. The development supports broader adoption of precision agriculture technologies within ASEAN farming markets.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- Southeast Asia Agricultural Machinery Market Policies, Regulations, and Standards

- Southeast Asia Agricultural Machinery Production (Thousand Unit) Trend 2022-2032

- Southeast Asia Agricultural Machinery Production (Thousand Unit) Trend By Type

- Tractors

- Plowing and Cultivating Machinery

- Planting Machinery

- Harvesting Machinery

- Haying and Forage Machinery

- Irrigation Machinery

- Company Wise Production Plants and Statistics

- Installed Production Capacity

- Actual Production

- Planned Production Target

- Southeast Asia Agricultural Machinery Production (Thousand Unit) Trend By Type

- Southeast Asia Agricultural Machinery Pricing Analysis 2022-2032

- Southeast Asia Agricultural Machinery Pricing Trend (USD/Unit) 2022-2032

- Southeast Asia Agricultural Machinery Pricing Trend (USD/Unit) By Countries 2022-2032

- Malaysia

- Indonesia

- Singapore

- Cambodia

- Vietnam

- Thailand

- Philippines

- Rest of Southeast Asia

- Southeast Asia Agricultural Machinery Pricing Trend (USD/Unit) By Countries 2022-2032

- Agricultural Machinery Pricing Trend (USD/Unit) By Type 2022-2032

- Tractors

- Plowing and Cultivating Machinery

- Planting Machinery

- Harvesting Machinery

- Haying and Forage Machinery

- Irrigation Machinery

- Southeast Asia Agricultural Machinery Pricing Trend (USD/Unit) 2022-2032

- Southeast Asia Agricultural Machinery Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- Southeast Asia Agricultural Machinery Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Type

- Tractors- Market Insights and Forecast 2022-2032, USD Million

- Horsepower- Market Insights and Forecast 2022-2032, USD Million

- Less than 40 HP- Market Insights and Forecast 2022-2032, USD Million

- 40 HP–99 HP- Market Insights and Forecast 2022-2032, USD Million

- Greater than 100 HP- Market Insights and Forecast 2022-2032, USD Million

- Tractor Type- Market Insights and Forecast 2022-2032, USD Million

- Compact Utility Tractors- Market Insights and Forecast 2022-2032, USD Million

- Utility Tractors- Market Insights and Forecast 2022-2032, USD Million

- Row-Crop Tractors- Market Insights and Forecast 2022-2032, USD Million

- Horsepower- Market Insights and Forecast 2022-2032, USD Million

- Plowing and Cultivating Machinery- Market Insights and Forecast 2022-2032, USD Million

- Plows- Market Insights and Forecast 2022-2032, USD Million

- Harrows- Market Insights and Forecast 2022-2032, USD Million

- Cultivators and Tillers- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- Planting Machinery- Market Insights and Forecast 2022-2032, USD Million

- Seed Drills- Market Insights and Forecast 2022-2032, USD Million

- Planters- Market Insights and Forecast 2022-2032, USD Million

- Spreaders- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- Harvesting Machinery- Market Insights and Forecast 2022-2032, USD Million

- Combine Harvesters-Threshers- Market Insights and Forecast 2022-2032, USD Million

- Forage Harvesters- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- Haying and Forage Machinery- Market Insights and Forecast 2022-2032, USD Million

- Mower-conditioners- Market Insights and Forecast 2022-2032, USD Million

- Balers- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- Irrigation Machinery- Market Insights and Forecast 2022-2032, USD Million

- Sprinkler Irrigation- Market Insights and Forecast 2022-2032, USD Million

- Drip Irrigation- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- Tractors- Market Insights and Forecast 2022-2032, USD Million

- By Application

- Land Development & Seed Bed Preparation- Market Insights and Forecast 2022-2032, USD Million

- Sowing & Planting- Market Insights and Forecast 2022-2032, USD Million

- Weed Cultivation- Market Insights and Forecast 2022-2032, USD Million

- Plant Protection- Market Insights and Forecast 2022-2032, USD Million

- Harvesting & Threshing- Market Insights and Forecast 2022-2032, USD Million

- Post-harvest & Agro Processing- Market Insights and Forecast 2022-2032, USD Million

- By Automation

- Automatic- Market Insights and Forecast 2022-2032, USD Million

- Semi-automatic- Market Insights and Forecast 2022-2032, USD Million

- Manual- Market Insights and Forecast 2022-2032, USD Million

- By Country

- Malaysia

- Indonesia

- Singapore

- Cambodia

- Vietnam

- Thailand

- Philippines

- Rest of Southeast Asia

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Type

- Market Size & Growth Outlook

- Malaysia Agricultural Machinery Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Type- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Automation- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Indonesia Agricultural Machinery Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Type- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Automation- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Singapore Agricultural Machinery Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Type- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Automation- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Cambodia Agricultural Machinery Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Type- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Automation- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Vietnam Agricultural Machinery Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Type- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Automation- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Thailand Agricultural Machinery Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Type- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Automation- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Philippines Agricultural Machinery Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Type- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Automation- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- John Deere

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Kubota Corporation

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- CNH Industrial N.V.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- AGCO Corporation

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Mahindra & Mahindra Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Yanmar Holdings Co. Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- CLAAS KGaA mbH

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- SDF Group

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Iseki & Co. Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Lovol Heavy Industry

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- YTO Group Corporation

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Daedong Corporation

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- John Deere

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Type |

|

| By Application |

|

| By Automation |

|

| By Country |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.