China Combine Harvester Market Report: Trends, Growth and Forecast (2026-2032)

By Type (Self-propelled, Tractor-pulled Combine, PTO-powered Combine), By Mechanism (Hydraulic, Hybrid), By Power (Below 150 HP, 150-300 HP, 300-450 HP, 450-550 HP, Above 550 HP), By Class (Class 1-2, Class 3-4, Class 5-6, Class 7 & Above), By Grain Tank Size (< 250 bu, 250-350 bu, > 350 bu), By Region (North, East, Southwest, Northwest, North East, South) ... Read more

|

Major Players

|

China Combine Harvester Market Statistics and Insights, 2026

- Market Size Statistics

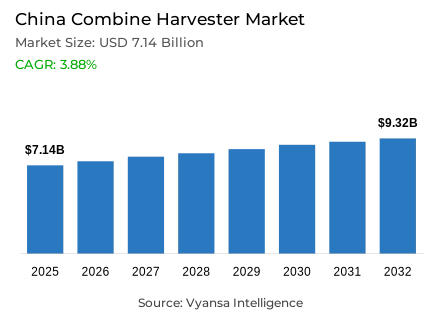

- Combine harvester market size in China was valued at USD 7.14 billion in 2025 and is estimated at USD 7.43 billion in 2026.

- The market size is expected to grow to USD 9.32 billion by 2032.

- Market to register a CAGR of around 3.88% during 2026-32.

- Type Shares

- Self-propelled grabbed market share of 80%.

- Competition

- More than 10 companies are actively engaged in producing combine harvester in China.

- Top 5 companies acquired around 55% of the market share.

- Shandong Shifeng Group Co. Ltd., Xingguang Agricultural Machinery Co. Ltd., Jiangsu Changfa Agricultural Equipment Co. Ltd., Weichai Lovol Intelligent Agricultural Technology, Zoomlion Heavy Industry Science & Technology Co. Ltd. etc., are few of the top companies.

- Mechanism

- Hydraulic grabbed 65% of the market.

China Combine Harvester Market Outlook

The China Combine Harvester Market was valued at USD 7.14 billion in 2025 and is projected to advance from USD 7.43 billion in 2026 to USD 9.32 billion by 2032, registering a compound annual growth rate of approximately 3.88% across the forecast period. This sustained expansion reflects the structural convergence of three reinforcing conditions that define China's agricultural machinery procurement environment: record-level grain production volumes that generate recurring harvesting equipment demand, a national mechanization agenda embedded within formal agricultural modernization policy, and accelerating rural labor shortages that are converting harvesting efficiency from a competitive advantage into an operational requirement across major grain-producing provinces. The market's commercial momentum is therefore anchored not in cyclical investment patterns but in durable structural pressures that are deepening across China's agricultural production base.

Self-propelled combine harvesters command the leading position within the product type category at approximately 80% of total market share, a dominance that reflects both the operational superiority of this configuration and its alignment with the scale requirements of China's large grain-producing regions. By integrating reaping, threshing, and cleaning functions within a single autonomous platform, self-propelled machines eliminate the operational dependencies and logistical inefficiencies associated with tractor-mounted configurations, making them the machinery of choice across commercial wheat, rice, and corn cultivation belts in Heilongjiang, Inner Mongolia, and North China's agricultural heartlands.

Within the mechanism segmentation, hydraulic systems hold approximately 65% of total market share, a position sustained by the measurable operational advantages these systems deliver across the full spectrum of combine harvesting functions. Hydraulic mechanisms govern steering precision, header lifting, threshing intensity, and unloading operations, and their ability to improve machine adaptability across varying crop conditions and field terrain has made them the functional standard across China's commercial harvesting equipment fleet. Smoother operation, reduced operator fatigue, and compatibility with high-capacity harvesting activities reinforce hydraulic system adoption as the dominant mechanism preference within the market.

China's combine harvester demand is geographically concentrated across the country's northern and northeastern grain belts, where large-scale cultivation of wheat, corn, and soybean generates the highest machinery utilization rates and the most commercially significant procurement volumes. As per data published by the National Bureau of Statistics of China, the country's grain production reached a record 714.88 million tonnes in 2025, a production volume that demands harvesting infrastructure of considerable scale and technological sophistication to process efficiently within narrow seasonal windows. This production scale positions China as one of the most commercially significant harvesting equipment markets globally.

China Combine Harvester Market Growth Driver

Record Grain Output and National Mechanization Policy Sustain Harvesting Equipment Demand

The primary commercial driver within the China Combine Harvester Market is the country's sustained achievement of record grain production volumes combined with a formally institutionalised national commitment to mechanized harvesting that has progressively raised the operational standard across major agricultural provinces. According to statistics released by the National Bureau of Statistics of China, grain output reached approximately 706.5 million tonnes in 2024, reflecting the scale of cultivation activity across wheat, rice, corn, and soybean farming regions that generates consistent and commercially substantial demand for high-capacity harvesting equipment. Harvesting operations at this production scale cannot be sustained through manual or partially mechanized methods, making combine harvester deployment not a productivity enhancement but an operational prerequisite for meeting China's food production targets within the time constraints imposed by seasonal harvesting windows.

Government mechanization policy has reinforced and accelerated this demand trajectory by embedding combine harvester adoption within China's broader agricultural modernization agenda. Evidence drawn from public data released by the Ministry of Agriculture and Rural Affairs of China confirms that the comprehensive mechanization rate of crop cultivation and harvesting reached approximately 76.7% in recent reporting periods, a figure that reflects the institutional progress of China's agricultural modernization initiatives and simultaneously identifies the remaining mechanization gap that continues to generate procurement demand. Rising rural labor shortages across agricultural provinces are intensifying the commercial urgency of this policy push within China's agricultural mechanization market, as farming communities that once supplemented machinery with seasonal labor are increasingly unable to mobilise adequate workforce capacity during peak harvesting periods, making grain harvesting automation the operationally critical investment across an expanding portion of China's grain production base.

China Combine Harvester Market Challenge

Fragmented Landholdings and High Equipment Costs Create Structural Adoption Barriers

A commercially significant challenge facing the China Combine Harvester Market is the persistent mismatch between the scale requirements of efficient combine harvester utilization and the fragmented landholding conditions that characterize a substantial portion of China's rural farming landscape. Based on data from the Organisation for Economic Co-operation and Development, the average farm size in China remains below one hectare, a scale at which the capital cost of large combine harvesters cannot be recovered through productivity gains within commercially viable operating timeframes. This fragmentation problem is further documented by research published in Frontiers, which confirms that the average cultivated land area of China's rural households remains below 7.5 mu and is distributed across approximately 5.5 separate plots, creating operational inefficiencies that reduce machinery utilization rates and increase per-hectare harvesting costs across smallholder farming communities.

The high investment threshold for advanced harvesting systems creates an additional layer of commercial pressure for small and medium-scale operators who are simultaneously confronting rising maintenance costs, seasonal machinery demand patterns, and limited access to agricultural equipment financing. These cost pressures are not uniformly distributed across the market; large-scale commercial farming operations in Heilongjiang and Inner Mongolia can absorb high-capacity combine harvester investments across sufficient cultivated area to generate acceptable returns, while smaller operators across central and southern provinces face a structurally different economic calculus. This bifurcation creates a market environment where demand for autonomous harvesting machines is concentrated among a commercially significant but geographically limited segment, while the majority of farming operations continue to rely on shared machinery services, rental platforms, and government-subsidised procurement schemes to access harvesting equipment within the China grain harvester market.

Unlock Market Intelligence

Explore the market potential with our data-driven report

China Combine Harvester Market Trend

Smart and Autonomous Harvesting Technologies Are Redefining Operational Standards Across Grain Production

A well-defined and commercially consequential structural trend within the China Combine Harvester Market is the accelerating integration of GPS-enabled combine harvesters, AI-driven harvesting systems, and precision agriculture machinery into operational farming practice across China's major grain production belts. In line with findings from the Food and Agriculture Organization of the United Nations, digital agriculture technologies are expanding globally to deliver improvements in crop productivity, resource efficiency, and climate resilience, and China is advancing this transition at a pace that reflects both the scale of its grain production obligations and the depth of its domestic agri-technology manufacturing capability. Beidou navigation harvesting systems, real-time yield analytics platforms, intelligent threshing control mechanisms, and IoT-enabled agricultural machinery are transitioning from premium configurations into standard procurement considerations across commercially active farming regions.

The scale of China's investment in smart agricultural technologies provides a structural foundation for this trend that extends well beyond the combine harvester category in isolation. As per official figures from the Civil Aviation Administration of China, more than 251,000 agricultural drones were operational across China's farming sector in 2024, a deployment figure that illustrates the institutional and commercial readiness of China's agricultural ecosystem to absorb and operationalize advanced precision farming technologies at scale. This broader digital agriculture transformation in China is creating an operational environment in which combine harvesters that cannot interface with farm management software, satellite-assisted farming systems, or telematics solutions are increasingly regarded as functionally insufficient for modern commercial grain farming, accelerating the market transition toward connected farming equipment and raising the technology baseline across the China combine harvester industry.

China Combine Harvester Market Opportunity

Large-Scale Grain Farming Modernization Creates a Sustained High-Technology Equipment Demand Pipeline

The most commercially substantial opportunity within the China Combine Harvester Market is concentrated at the intersection of record grain production ambition and the national investment program directed at upgrading harvesting infrastructure across major agricultural provinces. Data compiled from internationally recognised public authorities at the National Bureau of Statistics of China confirms that the country's grain production reached 714.88 million tonnes in 2025, a record figure that simultaneously reflects the productive capacity of China's farming system and the harvesting equipment intensity required to process this output volume efficiently across time-constrained seasonal windows. Continued expansion of high-standard farmland development programs, which are reshaping previously fragmented plots into contiguous cultivation zones suitable for large-scale machinery deployment, is directly expanding the addressable market for advanced combine harvesters, high-capacity harvesting headers, and autonomous field operation systems across China's grain belt provinces.

Government initiatives supporting rural revitalization, agricultural modernization, and food security provide a policy scaffolding that is translating this structural opportunity into measurable and near-term procurement activity across the China smart harvesting market. Validated reports from the Ministry of Agriculture and Rural Affairs of China confirm that mechanized farming continues expanding across major grain-producing regions with the explicit objective of improving productivity and reducing labor dependency, creating a demand environment in which advanced harvesting systems are actively supported through subsidy mechanisms, equipment procurement programs, and public investment in agricultural infrastructure. Rising commercial farming consolidation across northeastern provinces, combined with growing focus on reducing post-harvest losses through precision harvesting technologies, is further extending the commercial depth of this opportunity across multiple crop types and geographic regions within the China combine harvester industry.

Unlock Market Intelligence

Explore the market potential with our data-driven report

China Combine Harvester Market Segmentation Analysis

By Type

- Self-propelled

- Tractor-pulled Combine

- PTO-powered Combine

Self-propelled combine harvesters command the highest share within the product type category of the China Combine Harvester Market at approximately 80%, a position that reflects the decisive operational advantages this configuration delivers across the large-scale wheat, rice, corn, and soybean cultivation systems that define China's commercially significant farming regions. Unlike tractor-mounted alternatives that introduce dependency on separate power units and reduce field mobility across varying terrain conditions, self-propelled machines integrate all harvesting functions within a single autonomous platform, delivering the speed, capacity, and operational flexibility that large-scale grain farming activities require across narrow seasonal harvesting windows. This functional self-sufficiency has made the self-propelled configuration the institutional standard for commercial harvesting operations across China's most productive agricultural provinces.

The commercial entrenchment of self-propelled harvesters within the China agricultural machinery market is further reinforced by the alignment between this equipment category and the mechanization objectives embedded within China's national agricultural policy framework. As indicated by authoritative sources at the Ministry of Agriculture and Rural Affairs of China, mechanized harvesting levels continue to advance across major agricultural provinces as government policy actively supports the transition away from labor-intensive harvesting methods. Rising adoption of GPS-enabled combine harvesters, machine vision agriculture systems, and autonomous field operation capabilities across commercially active grain farming regions is further strengthening the commercial position of self-propelled configurations, which provide the mechanical platform most compatible with the precision agriculture equipment integrations that are redefining operational standards across China's grain harvester market.

By Mechanism

- Hydraulic

- Hybrid

Hydraulic systems hold the most commercially significant position within the mechanism segmentation of the China Combine Harvester Market, accounting for approximately 65% of total market share. This dominance is driven by the functional comprehensiveness of hydraulic mechanisms across the full operational cycle of combine harvesting, where steering responsiveness, header height adjustment, threshing intensity modulation, and grain unloading coordination are all governed by hydraulic control systems that deliver precision and reliability across varying crop densities, field gradients, and moisture conditions. No alternative mechanism category within China's harvesting equipment landscape matches the operational versatility that hydraulic systems provide across the diverse agronomic conditions encountered across rice paddies in southern provinces, wheat fields in northern plains, and corn cultivation zones across northeastern China.

The commercial primacy of hydraulic systems within the China combine harvester industry is reinforced by their compatibility with the smart harvesting technology integrations that are becoming progressively standard across commercially active harvesting fleets. Hydraulic precision enables the consistent machine control required for yield monitoring systems, intelligent threshing control algorithms, and real-time harvesting efficiency optimization platforms to function reliably across changing field conditions. As indicated by authoritative sources at the Ministry of Agriculture and Rural Affairs of China, harvesting mechanization is advancing across major grain-producing regions, and this advancement is being delivered predominantly through hydraulic-mechanism harvesters that combine operational sophistication with the mechanical durability required for high-intensity seasonal deployment. Sustained investment in large-scale grain farming equipment and rising focus on harvesting efficiency optimization are expected to maintain hydraulic mechanism dominance across the China Combine Harvester Market throughout the forecast period.

List of Companies Covered in China Combine Harvester Market

The companies listed below are highly influential in the China combine harvester market, with a significant market share and a strong impact on industry developments.

- Shandong Shifeng Group Co. Ltd.

- Xingguang Agricultural Machinery Co. Ltd.

- Jiangsu Changfa Agricultural Equipment Co. Ltd.

- Weichai Lovol Intelligent Agricultural Technology

- Zoomlion Heavy Industry Science & Technology Co. Ltd.

- YTO Group Corporation

- Jiangsu World Agricultural Machinery Co. Ltd.

- Luoyang Zhongshou Machinery Equipment Co. Ltd.

- Wuzheng Agricultural Equipment Co. Ltd.

- Dongfeng Agricultural Machinery Group Co. Ltd.

Market News & Updates

- Weichai Lovol Intelligent Agricultural Technology, 2025:

Weichai Lovol announced that its 600,000th combine harvester rolled off the production line in January 2025, highlighting continued expansion of its harvesting equipment portfolio in China. The milestone unit was the upgraded GM5125 combine harvester, featuring improvements in reliability, harvesting efficiency, and adaptability for large-scale grain harvesting operations. The company also expanded its combine harvester lineup across tangential flow, single axial flow, and dual axial flow technologies.

- Zoomlion Heavy Industry Science & Technology Co. Ltd, 2025:

Zoomlion introduced the TF220 combine harvester during the 2024 China International Agricultural Machinery Exhibition, with commercialization continuing across the Chinese market in 2025. The model was launched with higher feeding capacity, larger grain tank configuration, and a compound threshing and cleaning system designed to reduce grain loss below 0.6%. The launch strengthened Zoomlion’s high-end intelligent harvesting machinery portfolio for wheat, soybean, and corn harvesting applications.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- China Combine Harvester Market Policies, Regulations, and Standards

- China Combine Harvester Production (Thousand Unit) Trend 2022-2032

- China Combine Harvester Production (Thousand Unit) Trend By Type

- Self-propelled

- Tractor-pulled Combine

- PTO-powered Combine

- Company Wise Production Plants and Statistics

- Installed Production Capacity

- Actual Production

- Planned Production Target

- China Combine Harvester Production (Thousand Unit) Trend By Type

- China Combine Harvester Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- China Combine Harvester Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Type

- Self-propelled- Market Insights and Forecast 2022-2032, USD Million

- Tractor-pulled Combine- Market Insights and Forecast 2022-2032, USD Million

- PTO-powered Combine- Market Insights and Forecast 2022-2032, USD Million

- By Mechanism

- Hydraulic- Market Insights and Forecast 2022-2032, USD Million

- Hybrid- Market Insights and Forecast 2022-2032, USD Million

- By Power

- Below 150 HP- Market Insights and Forecast 2022-2032, USD Million

- 150-300 HP- Market Insights and Forecast 2022-2032, USD Million

- 300-450 HP- Market Insights and Forecast 2022-2032, USD Million

- 450-550 HP- Market Insights and Forecast 2022-2032, USD Million

- Above 550 HP- Market Insights and Forecast 2022-2032, USD Million

- By Class

- Class 1-2- Market Insights and Forecast 2022-2032, USD Million

- Class 3-4- Market Insights and Forecast 2022-2032, USD Million

- Class 5-6- Market Insights and Forecast 2022-2032, USD Million

- Class 7 & Above- Market Insights and Forecast 2022-2032, USD Million

- By Grain Tank Size

- < 250 bu- Market Insights and Forecast 2022-2032, USD Million

- 250-350 bu- Market Insights and Forecast 2022-2032, USD Million

- > 350 bu- Market Insights and Forecast 2022-2032, USD Million

- By Region

- North- Market Insights and Forecast 2022-2032, USD Million

- East- Market Insights and Forecast 2022-2032, USD Million

- Southwest- Market Insights and Forecast 2022-2032, USD Million

- Northwest- Market Insights and Forecast 2022-2032, USD Million

- North East- Market Insights and Forecast 2022-2032, USD Million

- South- Market Insights and Forecast 2022-2032, USD Million

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Type

- Market Size & Growth Outlook

- China Self-propelled Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Mechanism- Market Insights and Forecast 2022-2032, USD Million

- By Power- Market Insights and Forecast 2022-2032, USD Million

- By Class- Market Insights and Forecast 2022-2032, USD Million

- By Grain Tank Size- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- China Tractor-pulled Combine Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Mechanism- Market Insights and Forecast 2022-2032, USD Million

- By Power- Market Insights and Forecast 2022-2032, USD Million

- By Class- Market Insights and Forecast 2022-2032, USD Million

- By Grain Tank Size- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- China PTO-powered Combine Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Mechanism- Market Insights and Forecast 2022-2032, USD Million

- By Power- Market Insights and Forecast 2022-2032, USD Million

- By Class- Market Insights and Forecast 2022-2032, USD Million

- By Grain Tank Size- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Weichai Lovol Intelligent Agricultural Technology

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Zoomlion Heavy Industry Science & Technology Co. Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- YTO Group Corporation

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Jiangsu World Agricultural Machinery Co. Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Luoyang Zhongshou Machinery Equipment Co. Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Shandong Shifeng Group Co. Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Xingguang Agricultural Machinery Co. Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Jiangsu Changfa Agricultural Equipment Co. Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Wuzheng Agricultural Equipment Co. Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Dongfeng Agricultural Machinery Group Co. Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Weichai Lovol Intelligent Agricultural Technology

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Type |

|

| By Mechanism |

|

| By Power |

|

| By Class |

|

| By Grain Tank Size |

|

| By Region |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.