Japan Agricultural Machinery Market Report: Trends, Growth and Forecast (2026-2032)

By Type (Tractors (Horsepower (Less than 40 HP, 40 HP–99 HP, Greater than 100 HP), Tractor Type (Compact Utility Tractors, Utility Tractors, Row-Crop Tractors)), Plowing and Cultivating Machinery (Plows, Harrows, Cultivators and Tillers, Others), Planting Machinery (Seed Drills, Planters, Spreaders, Others), Harvesting Machinery (Combine Harvesters-Threshers, Forage Harvesters, Others), Haying and Forage Machinery (Mower-conditioners, Balers, Others), Irrigation Machinery (Sprinkler Irrigation, Drip Irrigation, Others), Others), By Application (Land Development & Seed Bed Preparation, Sowing & Planting, Weed Cultivation, Plant Protection, Harvesting & Threshing, Post-harvest & Agro Processing), By Automation (Automatic, Semi-automatic, Manual) ... Read more

|

Major Players

|

Japan Agricultural Machinery Market Statistics and Insights, 2026

- Market Size Statistics

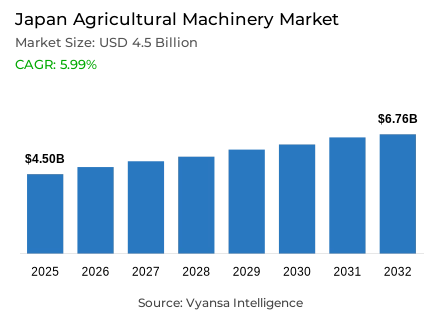

- Agricultural machinery market size in Japan was valued at USD 4.5 billion in 2025 and is estimated at USD 4.88 billion in 2026.

- The market size is expected to grow to USD 6.76 billion by 2032.

- Market to register a CAGR of around 5.99% during 2026-32.

- Type Shares

- Tractors grabbed market share of 40%.

- Competition

- More than 10 companies are actively engaged in producing agricultural machinery in Japan.

- Top 5 companies acquired around 85% of the market share.

- Honda Motor Co. Ltd., Shibaura Machine Co. Ltd., Kioritz Corporation, Kubota Corporation, Yanmar Holdings Co. Ltd. etc., are few of the top companies.

- Automation

- Automatic grabbed 40% of the market.

Japan Agricultural Machinery Market Outlook

The Japan Agricultural Machinery Market was valued at USD 4.5 billion in 2025 and is projected to advance from USD 4.88 billion in 2026 to USD 6.76 billion by 2032, registering a CAGR of 5.99% during the forecast period. The structural driver underpinning this trajectory is demographically anchored rather than cyclical, as Japan's agricultural workforce faces an aging crisis that is progressively converting mechanization from a productivity enhancement into an operational prerequisite across rice paddies, horticulture farms, and mixed cultivation systems. As per data published by Japan's Ministry of Agriculture, Forestry and Fisheries, the average age of core farm workers in Japan exceeds 68 years, a demographic imbalance that leaves no commercially viable path forward for sustained agricultural output without accelerated equipment adoption.

Tractors command approximately 40% share within the equipment category, sustained by their multi-functional utility across soil preparation, planting support, and transport activities that make them indispensable across Japan's fragmented and small-scale farm structure. Compact tractor configurations are particularly significant within the Japan Agricultural Machinery Market, as they are engineered to operate effectively within the narrow and dispersed plot layouts that characterise the majority of active agricultural holdings across the country, enabling mechanized field operations where standard equipment dimensions would be impractical.

Automatic systems account for nearly 40% share within the automation segment, reflecting the accelerating pace at which farmers are deploying automatic transplanters, harvesting systems, and precision-guided tractors to offset chronic labor shortages and maintain operational continuity across rice and crop production systems. According to statistics released by the Ministry of Agriculture, Forestry and Fisheries, smart agriculture initiatives actively promote robotics and automation technologies across Japan's farming sector, creating a direct policy-to-market pathway for advanced equipment adoption.

Japan's limited arable land base intensifies the productivity imperative that sustains equipment demand across all forecast years. Validated reports from the Food and Agriculture Organization confirm that Japan's agricultural output per hectare requirements remain among the highest in Asia, reinforcing continuous investment in precision and automated machinery as the primary mechanism through which the Japan Agricultural Machinery Market sustains long-term agricultural productivity against a structurally shrinking rural workforce.

Japan Agricultural Machinery Market Growth Driver

Aging Agricultural Workforce Converts Labor-Saving Equipment Into Structural Necessity

The primary commercial driver within the Japan agricultural machinery market is the country's deeply entrenched agricultural labor shortage, which has been intensifying across decades and now compels farming operations at every scale to substitute machinery for human labor across core cultivation activities. According to statistics released by Japan's Ministry of Agriculture, Forestry and Fisheries, the average age of core agricultural workers in Japan currently exceeds 68 years, a figure that reflects not only an aging workforce but an accelerating attrition of skilled agricultural labor that cannot be replaced through conventional recruitment. Farm mechanization in Japan is no longer a productivity enhancement strategy; it has become the primary operational response to a workforce that is simultaneously shrinking in numbers and advancing in age across rural communities.

This demographic trajectory is compounding the commercial urgency of agricultural mechanization in Japan across every major crop segment. Paddy field machinery, robotic farming systems, and automated transplanting and harvesting equipment are being adopted not primarily for competitive gain but because many farming operations are no longer able to sustain cultivation schedules without them. As indicated by authoritative sources at the World Bank, arable land accounts for only approximately 11.1% of Japan's total land area, which means productivity per hectare must remain high even as available labor per hectare continues to decline. This convergence of shrinking workforce supply and constrained land availability creates a durable and structurally embedded demand environment for advanced agricultural equipment across the Japan agricultural machinery market.

Japan Agricultural Machinery Market Challenge

High Capital Costs and Fragmented Landholdings Constrain Full Mechanization Potential

A structurally significant challenge facing the Japan agricultural machinery market is the mismatch between the cost profile of advanced farming equipment and the economic capacity of Japan's predominantly small-scale farming operations. Autonomous tractors, smart combine harvesters, GPS guidance systems, and robotic harvesting equipment carry high acquisition and maintenance costs that are difficult to absorb for operators managing plots well below the thresholds at which large machinery investments generate commercially viable returns. Based on data from Japan's Ministry of Agriculture, Forestry and Fisheries, Japan's total cultivated land area remains below 4.3 million hectares, and the fragmented distribution of this land across small individual holdings means that the per-hectare economics of machinery investment remain challenging across a significant portion of the farming base.

Rural depopulation intensifies this challenge by reducing both the available labor supply and the local knowledge base required to operate and maintain increasingly sophisticated farming equipment. As per official figures from Japan's Statistics Bureau, individuals aged 65 and above account for more than 29.4% of Japan's total population, and in rural agricultural prefectures this proportion is substantially higher. The high adoption cost of smart farming technologies creates an additional layer of financial pressure for ageing farm operators who may lack both the capital and the technical familiarity to transition to digital agriculture transformation platforms. These overlapping pressures create a commercial environment where machinery demand is structurally strong but conversion rates are constrained by affordability and operational complexity across the smaller farming segment.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Japan Agricultural Machinery Market Trend

Autonomous and AI-Enabled Equipment Is Redefining Operational Standards Across Japanese Farming

A well-defined and commercially consequential structural trend within the Japan agricultural machinery market is the accelerating adoption of autonomous and AI-powered agricultural equipment across paddy cultivation, horticulture, and precision crop management operations. Evidence drawn from public data released by Japan's Ministry of Agriculture, Forestry and Fisheries confirms that more than 70% of agricultural communities across Japan are currently experiencing labor shortages severe enough to impair normal farming operations, a condition that is converting interest in smart agriculture technologies into active procurement decisions across multiple machinery categories. GPS-enabled tractors, agricultural drones, automated rice transplanters, and sensor-based irrigation systems are transitioning from demonstration technologies into standard operational investments across an expanding range of farming enterprises.

Japan's deep institutional capability in robotics and precision engineering is providing a structurally advantageous foundation for this technology transition within its domestic agriculture sector. Validated reports from the International Federation of Robotics confirm that Japan remains the world's largest industrial robot manufacturer and accounted for approximately 46% of global robot production output in recent measurement periods. This manufacturing depth is enabling domestic agricultural equipment producers to integrate advanced robotics, telematics systems, and machine learning capabilities into farming machinery at a pace that aligns with the urgency of the labor shortage challenge. The result is a market environment where agricultural machinery used in paddy farming is being redesigned around automation rather than operator assistance, accelerating the pace of modernization across Japan's agricultural equipment sector.

Japan Agricultural Machinery Market Opportunity

Precision Agriculture Expansion Unlocks Demand for High-Technology Machinery Across Constrained Farmland

Demand for precision farming equipment in Japan is expanding within a commercially compelling structural context where land limitations and labor constraints simultaneously increase the economic premium on per-hectare productivity. In line with findings from the World Bank, arable land represents approximately 12% of Japan's total land area, a constraint that places intensive and technology-supported farming systems at the centre of Japan's long-term agricultural productivity strategy. This land scarcity dynamic creates demand for AI and IoT in agriculture applications, smart irrigation adoption, precision seeding equipment, and robotic harvesting systems that generate measurable yield improvements within a fixed and largely non-expandable agricultural footprint.

Institutional support for this transition is reinforcing commercial momentum across the Japan agricultural machinery market. Data compiled from internationally recognised public authorities at the OECD-FAO Agricultural Outlook 2024-2033 confirms that Japan continues to advance agricultural productivity improvement and resource-efficient farming practices as formal national policy priorities, driven by both labor shortages and land limitations. Rising public and private investment in precision agriculture systems, autonomous navigation equipment, and farm management software is expanding the addressable market for high-technology agricultural machinery across Japan, with opportunity concentrated in segments where automation directly substitutes for declining human labor and where data-driven crop management can deliver productivity gains across compact, intensively managed farmland.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Japan Agricultural Machinery Market Segmentation Analysis

By Type

- Tractors

- Horsepower

- Less than 40 HP

- 40 HP–99 HP

- Greater than 100 HP

- Tractor Type

- Compact Utility Tractors

- Utility Tractors

- Row-Crop Tractors

- Horsepower

- Plowing and Cultivating Machinery

- Plows

- Harrows

- Cultivators and Tillers

- Others

- Planting Machinery

- Seed Drills

- Planters

- Spreaders

- Others

- Harvesting Machinery

- Combine Harvesters-Threshers

- Forage Harvesters

- Others

- Haying and Forage Machinery

- Mower-conditioners

- Balers

- Others

- Irrigation Machinery

- Sprinkler Irrigation

- Drip Irrigation

- Others

- Others

Tractors command the highest share within the machinery type category of the Japan agricultural machinery market at approximately 40%, a position that reflects the operational indispensability of this equipment class across Japan's diverse cropping systems. Unlike single-function harvesting or transplanting machinery, tractors serve a broad range of field operations including soil preparation, cultivation, planting support, and intra-farm transportation, making them the most commercially versatile category within the equipment landscape. Compact utility tractors, in particular, have established a commercially dominant position because their dimensional specifications align closely with the narrow plot widths, paddy field layouts, and terraced farming structures that characterize productive agricultural land across many of Japan's rural prefectures.

The commercial rationale behind tractor leadership within the Japan agricultural mechanization market is reinforced by the segment's alignment with the country's labor substitution imperative. As per data published by Japan's Ministry of Agriculture, Forestry and Fisheries, mechanization remains the formally recognized pathway to sustaining agricultural labor productivity as the farming workforce contracts and ages. Compact tractors operating with enhanced maneuverability, fuel-efficient engine configurations, and compatibility with precision farming attachments represent the machinery category best positioned to absorb the largest share of ongoing equipment investment across both rice cultivation and horticulture operations. Sustained demand from smallholder farmers replacing manual field work with mechanized systems is expected to maintain tractor demand as the volume and value anchor of the Japan farm equipment sector across the forecast period.

By Automation

- Automatic

- Semi-automatic

- Manual

The segment has the highest share around Automatic under the Automation segment, accounting for nearly 40% market share in the Japan Agricultural Machinery Market. Automatic agricultural machinery witnesses strong demand due to Japan’s aging farming population, shrinking agricultural workforce, and increasing focus on improving farm productivity through mechanization. Farmers increasingly adopt automatic tractors, rice transplanters, harvesters, and spraying systems to reduce manual labor dependency and improve operational efficiency across agricultural activities.

Japan continues to promote smart agriculture and precision farming technologies to strengthen food production efficiency. According to Japan’s Ministry of Agriculture, Forestry and Fisheries (MAFF), the country continues expanding the use of robotic and automated farming equipment under its smart agriculture initiatives. Automatic machinery helps improve accuracy, reduce operational time, and optimize fuel and resource usage across farming operations. These advantages continue supporting higher adoption of automatic agricultural equipment across commercial farming activities in Japan.

List of Companies Covered in Japan Agricultural Machinery Market

The companies listed below are highly influential in the Japan agricultural machinery market, with a significant market share and a strong impact on industry developments.

- Honda Motor Co. Ltd.

- Shibaura Machine Co. Ltd.

- Kioritz Corporation

- Kubota Corporation

- Yanmar Holdings Co. Ltd.

- Iseki & Co. Ltd.

- Mitsubishi Mahindra Agricultural Machinery Co. Ltd.

- Takakita Co. Ltd.

- Ohashi Inc.

- Hinomoto Agricultural Machinery

Market News & Updates

- Kubota Corporation, 2026:

Kubota announced the launch of three new agricultural machinery models for the Japanese market, including the KRH450 standard combine harvester, the EDC1101 edamame combine, and the TS552N/752N Unemaster Pro tiller series. The new lineup expands Kubota’s harvesting and field management equipment portfolio for Japanese farms, with phased commercial launches scheduled from January to June 2026.

- Yanmar Holdings Co. Ltd., 2025:

Yanmar Agri introduced the YH2A/3A combine harvester series for small and medium-scale farms in Japan’s mountainous and semi-mountainous agricultural regions. The updated machines feature enhanced operational safety, improved harvesting performance, and usability upgrades designed for difficult terrain and labor-constrained farming environments. Commercial sales began in January 2026 across Japan.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- Japan Agricultural Machinery Market Policies, Regulations, and Standards

- Japan Agricultural Machinery Production (Thousand Unit) Trend 2022-2032

- Japan Agricultural Machinery Production (Thousand Unit) Trend By Type

- Tractors

- Plowing and Cultivating Machinery

- Planting Machinery

- Harvesting Machinery

- Haying and Forage Machinery

- Irrigation Machinery

- Company Wise Production Plants and Statistics

- Installed Production Capacity

- Actual Production

- Planned Production Target

- Japan Agricultural Machinery Production (Thousand Unit) Trend By Type

- Japan Agricultural Machinery Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- Japan Agricultural Machinery Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Type

- Tractors- Market Insights and Forecast 2022-2032, USD Million

- Horsepower- Market Insights and Forecast 2022-2032, USD Million

- Less than 40 HP- Market Insights and Forecast 2022-2032, USD Million

- 40 HP–99 HP- Market Insights and Forecast 2022-2032, USD Million

- Greater than 100 HP- Market Insights and Forecast 2022-2032, USD Million

- Tractor Type- Market Insights and Forecast 2022-2032, USD Million

- Compact Utility Tractors- Market Insights and Forecast 2022-2032, USD Million

- Utility Tractors- Market Insights and Forecast 2022-2032, USD Million

- Row-Crop Tractors- Market Insights and Forecast 2022-2032, USD Million

- Horsepower- Market Insights and Forecast 2022-2032, USD Million

- Plowing and Cultivating Machinery- Market Insights and Forecast 2022-2032, USD Million

- Plows- Market Insights and Forecast 2022-2032, USD Million

- Harrows- Market Insights and Forecast 2022-2032, USD Million

- Cultivators and Tillers- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- Planting Machinery- Market Insights and Forecast 2022-2032, USD Million

- Seed Drills- Market Insights and Forecast 2022-2032, USD Million

- Planters- Market Insights and Forecast 2022-2032, USD Million

- Spreaders- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- Harvesting Machinery- Market Insights and Forecast 2022-2032, USD Million

- Combine Harvesters-Threshers- Market Insights and Forecast 2022-2032, USD Million

- Forage Harvesters- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- Haying and Forage Machinery- Market Insights and Forecast 2022-2032, USD Million

- Mower-conditioners- Market Insights and Forecast 2022-2032, USD Million

- Balers- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- Irrigation Machinery- Market Insights and Forecast 2022-2032, USD Million

- Sprinkler Irrigation- Market Insights and Forecast 2022-2032, USD Million

- Drip Irrigation- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- Tractors- Market Insights and Forecast 2022-2032, USD Million

- By Application

- Land Development & Seed Bed Preparation- Market Insights and Forecast 2022-2032, USD Million

- Sowing & Planting- Market Insights and Forecast 2022-2032, USD Million

- Weed Cultivation- Market Insights and Forecast 2022-2032, USD Million

- Plant Protection- Market Insights and Forecast 2022-2032, USD Million

- Harvesting & Threshing- Market Insights and Forecast 2022-2032, USD Million

- Post-harvest & Agro Processing- Market Insights and Forecast 2022-2032, USD Million

- By Automation

- Automatic- Market Insights and Forecast 2022-2032, USD Million

- Semi-automatic- Market Insights and Forecast 2022-2032, USD Million

- Manual- Market Insights and Forecast 2022-2032, USD Million

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Type

- Market Size & Growth Outlook

- Japan Tractors Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Automation- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Japan Plowing and Cultivating Machinery Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Automation- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Japan Planting Machinery Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Automation- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Japan Harvesting Machinery Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Automation- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Japan Haying and Forage Machinery Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Automation- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Japan Irrigation Machinery Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Automation- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Kubota Corporation

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Yanmar Holdings Co. Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Iseki & Co. Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Mitsubishi Mahindra Agricultural Machinery Co. Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Takakita Co. Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Honda Motor Co. Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Shibaura Machine Co. Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Kioritz Corporation

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Ohashi Inc.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Hinomoto Agricultural Machinery

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Kubota Corporation

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Type |

|

| By Application |

|

| By Automation |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.