South Korea Sports Nutrition Market Report: Trends, Growth and Forecast (2026-2032)

By Product Type (Sports Protein Products (Protein/Energy Bars, Sports Protein Powder, Sports Protein RTD), Sports Non-Protein Products), By Sales Channel (Retail Offline, Retail Online), By Ingredients (Vitamins and Minerals, Proteins and Amino Acids, Carbohydrates, Probiotics, Botanicals/Herbals, Others), By Functionality (Energy, Muscle growth, Hydration, Weight Management, Others), By End User (Bodybuilders, Athletes, Lifestyle Users) ... Read more

|

Major Players

|

South Korea Sports Nutrition Market Statistics and Insights, 2026

- Market Size Statistics

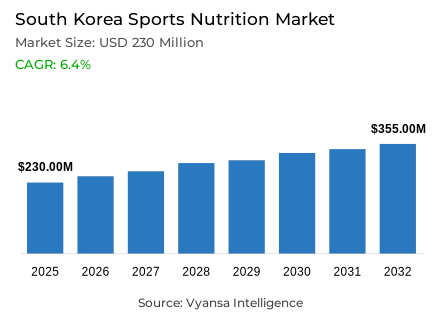

- Sports nutrition market size in South Korea was estimated at USD 230 million in 2025.

- The market size is expected to grow to USD 355 million by 2032.

- Market to register a CAGR of around 6.4% during 2026-32.

- Product Type Shares

- Sports protein products grabbed market share of 95%.

- Competition

- More than 15 companies are actively engaged in producing sports nutrition in South Korea.

- Top 5 companies acquired around 40% of the market share.

- Dongwon F&B Co Ltd, Nong Shim Kellogg Co, Lotte Wellfood Co Ltd, Maeil Dairies Co Ltd, Orion Corp etc., are few of the top companies.

- Sales Channel

- Retail offline grabbed 80% of the market.

South Korea Sports Nutrition Market Outlook

The South Korea sports nutrition market is set to experience a significant upward trend as the market expands to include a wider age bracket. The market is estimated to be USD 230 million in 2025 and is expected to increase to USD 355 million in 2032 with a compound annual growth rate of about 6.4%. The growth will be supported by increased interest in muscle health among the aging population and the ongoing culture of self-improvement among younger adults. With the emergence of protein as a daily food item, sports nutrition is no longer a niche product in the fitness market, but a mainstream lifestyle product.

The core driver of growth will be sports protein products that have already secured a dominant 95% market share. The fast emergence of sports protein RTD products in the past few years has widened the overall end user base due to their convenience and good brand name by the market players like Hi-Mune and Selex. Although the growth in RTD products will stabilise, their wide penetration will keep on aiding market growth. Nevertheless, the growth of protein powder will be limited by the competition with general-use protein supplements and RTD forms.

Sports non-protein products will become prominent throughout the forecast period. With the growing awareness of energy support, endurance, and body protection during and after exercises, more end users will consider non-protein formats. This change will open up the market players to offer diversification other than protein and meet the changing lifestyle and wellness needs. Trends in weight-management will also support this change, as RTD protein drinks are becoming more popular as meal replacements.

Distribution wise, retail offline channels are the leading ones with 80% market share, which is backed by high availability in convenience stores, pharmacies, and supermarkets. Although the retail offline will continue to be the main sales channel, online purchasing will probably grow as end users compare prices and find new product innovations. All in all, the increasing health awareness, aging population, and constant innovation of product forms will guarantee a healthy market growth up to 2032

South Korea Sports Nutrition Market Growth Driver

Ageing Population and Increased Protein Consumption Among Older Adults

South Korea rapidly aging population remains a fundamental driver supporting the expansion of the sports nutrition market. According to Statistics Korea, in 2024, 18.4% of the population will be aged 65 years and above, and it is estimated that South Korea will become a super-aged country by 2026. As muscle loss with age is increasing, the Korea Disease Control and Prevention Agency has established that one out of every three adults aged 60 years and above is at risk of sarcopenia, which further supports the need of protein products to maintain muscle. Sports protein powders and ready-to-drink products are becoming more popular as convenient sources of protein and functional health products as older adults pursue convenient nutrition and health benefits.

At the same time, the category is being reinforced by health-based consumption among younger adults. According to the Ministry of Health and Welfare, 67% of adults aged 20s and 30s work out at least once a week, which makes protein a stable part of their diet. This generational demographic change significantly increases the end user base of the category and supports long-term growth.

South Korea Sports Nutrition Market Challenge

Low Per Capita Consumption of Sports Protein Powder

The consumption of sports protein powder per capita is still a major challenge in Korea despite the increasing interest in proteins. According to OECD dietary intake data, the average daily protein intake in Korea is 88g per capita, compared to 92g in Japan and 113g in the United States, which represents a less protein-based dietary structure. This reduces the need of traditional protein powder formats. In addition, KOSIS indicates that 65% of supplement users buy vitamins and minerals, and only 17% buy protein supplements, which demonstrates the prevalence of non-protein supplements.

The use of powder formats is further limited by the substantial competition of vitamin-based protein supplements and protein RTD products. Domestic brands like Hi-Mune and Selex have placed RTD products and general-purpose protein supplements as more convenient and accessible products, which has constrained the growth of traditional powder consumption despite the increasing overall protein interest.

Unlock Market Intelligence

Explore the market potential with our data-driven report

South Korea Sports Nutrition Market Trend

Strong Momentum for Sports Non-Protein Products

The growing adoption of sports non-protein products is emerging as a prominent market trend, as end users become increasingly informed about their role in supporting hydration, energy metabolism, and post-exercise recovery. KDCA states that 41% of adults experience fatigue-related symptoms every week, which explains the popularity of products that support energy production and body protection. This is in line with the growing use of pre-workout and post-workout non-protein formulations. Moreover, the Ministry of Health and Welfare statistics show that 32% of adults complain of poor micronutrient consumption, which justifies the need to use fortified non-protein workout supplements.

The adoption of protein RTD products between 2020 and 2023 created a large pool of daily protein end users, which opened the way to diversified product forms. With the growth of lifestyle-based sports nutrition, non-protein products, such as hydration beverages, amino acid blends, and energy-support formulas, are poised to grow significantly in the future, as lifestyle needs extend beyond muscle-building goals.

South Korea Sports Nutrition Market Opportunity

Convergence of Weight Management and Protein-Based Meal Alternatives

The intersection of sports nutrition and weight management is a significant market growth opportunity. The OECD Obesity Update indicates that 36.6% of adults in Korea are overweight, and weight-control behaviours are on the increase, especially among younger end users. To supplement this trend, according to Statistics Korea, 53% of adults aged 2039 years miss breakfast at least two times per week, creating a significant opportunity in the market of convenient meal-replacement-style protein RTD products. These trends justify the placement of RTD protein drinks as low-calorie, balanced drinks that satisfy daily protein needs.

This change broadens sports nutrition consumption beyond gymnasium-based consumption into everyday wellness practices. Meal-replacement brands are also providing low-calorie, nutrient-balanced products, which have increased the interest in products that provide a combination of protein and energy and immune support. With end users becoming more concerned with convenience, balanced nutrition, and weight management, meal-replacement-style sports protein products are a high-potential growth opportunity.

Unlock Market Intelligence

Explore the market potential with our data-driven report

South Korea Sports Nutrition Market Segmentation Analysis

By Product Type

- Sports Protein Products

- Protein/Energy Bars

- Sports Protein Powder

- Sports Protein RTD

- Sports Non-Protein Products

The segment with highest market share under product type is Sports protein products, capturing around 95% of the South Korea sports nutrition market. This dominance is driven by the widespread adoption of sports protein RTD formats, which have become the primary entry point into the category for numerous end users due to their convenience and strong presence across retail channels. Local brands such as Hi-Mune Active and Selex have fulfilled a major role in shaping demand, offering RTD products and daily-use protein supplements that appeal to both younger fitness focused end users and older adults seeking muscle maintenance.

Throughout the forecast period, sports protein products are expected to retain their leadership position, supported by continued product innovation, expanding use cases such as meal replacement, and rising interest in general wellness. As the market becomes more specialised, protein products will remain at the centre of growth, notwithstanding the gradual traction gained by non-protein sports nutrition among end users seeking energy, endurance, and recovery-focused solutions.

By Sales Channel

- Retail Offline

- Retail Online

Retail offline represents the segment with the highest share within the sales channel, capturing 80% of the South Korea sports nutrition market. Supermarkets, health stores, and pharmacies continue to dominate due to their comprehensive product assortments and strong visibility of leading RTD and supplement brands. Offline channels additionally benefit from impulse purchases, frequent promotional activities, and end user trust—particularly important in a market where numerous buyers prefer reassurance regarding product quality and safety.

During the forecast period, retail offline is expected to maintain its dominant position as the expanding product range encourages shoppers to explore new formats in person. While online platforms are gaining traction for bulk purchases and convenience, offline stores remain central for product discovery, comparison, and first-time purchases. The strong integration of sports nutrition with everyday grocery and pharmacy shopping will continue supporting the leadership of the offline channel over the forecast period.

List of Companies Covered in South Korea Sports Nutrition Market

The companies listed below are highly influential in the South Korea sports nutrition market, with a significant market share and a strong impact on industry developments.

- Dongwon F&B Co Ltd

- Nong Shim Kellogg Co

- Lotte Wellfood Co Ltd

- Maeil Dairies Co Ltd

- Orion Corp

- Herbalife Korea Co Ltd

- Il Dong Foodis Co Ltd

- Ignis Inc

- Kun6man Inc

- Boryung Pharmaceutical Co Ltd

Competitive Landscape

Local brands such as Hi-Mune Active and Selex continued to shape the competitive landscape of South Korea’s sports nutrition market in 2024, driving growth through their strong focus on convenient sports protein RTD formats. These brands built early leadership by catering to lifestyle-oriented consumers, and their dominance has limited the expansion of traditional sports protein powders. As RTDs matured, competition intensified with more brands introducing specialised formulations targeting muscle health, ageing consumers, and general daily nutrition. Meanwhile, the rise of protein supplements within vitamins and dietary supplements further broadened competitive pressures, as many consumers opted for general-use protein products instead of sports-specific powders. With the market evolving toward greater segmentation, emerging players and established brands alike are increasingly investing in new formats and expanding beyond protein into emerging non-protein sports nutrition solutions.

Frequently Asked Questions

Related Report

1. Market Segmentation

1.1. Research Scope

1.2. Research Methodology

1.3. Definitions and Assumptions

2. Executive Summary

3. South Korea Sports Nutrition Market Policies, Regulations, and Standards

4. South Korea Sports Nutrition Market Dynamics

4.1. Growth Factors

4.2. Challenges

4.3. Trends

4.4. Opportunities

5. South Korea Sports Nutrition Market Statistics, 2022-2032F

5.1. Market Size & Growth Outlook

5.1.1.By Revenues in USD Million

5.2. Market Segmentation & Growth Outlook

5.2.1.By Product Type

5.2.1.1. Sports Protein Products- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.1. Protein/Energy Bars- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.2. Sports Protein Powder- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.3. Sports Protein RTD- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2. Sports Non-Protein Products- Market Insights and Forecast 2022-2032, USD Million

5.2.2.By Sales Channel

5.2.2.1. Retail Offline- Market Insights and Forecast 2022-2032, USD Million

5.2.2.2. Retail Online- Market Insights and Forecast 2022-2032, USD Million

5.2.3.By Ingredients

5.2.3.1. Vitamins and Minerals- Market Insights and Forecast 2022-2032, USD Million

5.2.3.2. Proteins and Amino Acids- Market Insights and Forecast 2022-2032, USD Million

5.2.3.3. Carbohydrates- Market Insights and Forecast 2022-2032, USD Million

5.2.3.4. Probiotics- Market Insights and Forecast 2022-2032, USD Million

5.2.3.5. Botanicals/Herbals- Market Insights and Forecast 2022-2032, USD Million

5.2.3.6. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.4.By Functionality

5.2.4.1. Energy- Market Insights and Forecast 2022-2032, USD Million

5.2.4.2. Muscle growth- Market Insights and Forecast 2022-2032, USD Million

5.2.4.3. Hydration- Market Insights and Forecast 2022-2032, USD Million

5.2.4.4. Weight Management- Market Insights and Forecast 2022-2032, USD Million

5.2.4.5. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.5.By End User

5.2.5.1. Bodybuilders- Market Insights and Forecast 2022-2032, USD Million

5.2.5.2. Athletes- Market Insights and Forecast 2022-2032, USD Million

5.2.5.3. Lifestyle Users- Market Insights and Forecast 2022-2032, USD Million

5.2.6.By Competitors

5.2.6.1. Competition Characteristics

5.2.6.2. Market Share & Analysis

6. South Korea Protein Products Sports Nutrition Market Statistics, 2022-2032F

6.1. Market Size & Growth Outlook

6.1.1.By Revenues in USD Million

6.2. Market Segmentation & Growth Outlook

6.2.1.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

6.2.2.By Ingredients- Market Insights and Forecast 2022-2032, USD Million

6.2.3.By Functionality- Market Insights and Forecast 2022-2032, USD Million

6.2.4.By End User- Market Insights and Forecast 2022-2032, USD Million

7. South Korea Non-Protein Products Sports Nutrition Market Statistics, 2022-2032F

7.1. Market Size & Growth Outlook

7.1.1.By Revenues in USD Million

7.2. Market Segmentation & Growth Outlook

7.2.1.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

7.2.2.By Ingredients- Market Insights and Forecast 2022-2032, USD Million

7.2.3.By Functionality- Market Insights and Forecast 2022-2032, USD Million

7.2.4.By End User- Market Insights and Forecast 2022-2032, USD Million

8. Competitive Outlook

8.1. Company Profiles

8.1.1.Maeil Dairies Co Ltd

8.1.1.1. Business Description

8.1.1.2. Product Portfolio

8.1.1.3. Collaborations & Alliances

8.1.1.4. Recent Developments

8.1.1.5. Financial Details

8.1.1.6. Others

8.1.2.Orion Corp

8.1.2.1. Business Description

8.1.2.2. Product Portfolio

8.1.2.3. Collaborations & Alliances

8.1.2.4. Recent Developments

8.1.2.5. Financial Details

8.1.2.6. Others

8.1.3.Herbalife Korea Co Ltd

8.1.3.1. Business Description

8.1.3.2. Product Portfolio

8.1.3.3. Collaborations & Alliances

8.1.3.4. Recent Developments

8.1.3.5. Financial Details

8.1.3.6. Others

8.1.4.Il Dong Foodis Co Ltd

8.1.4.1. Business Description

8.1.4.2. Product Portfolio

8.1.4.3. Collaborations & Alliances

8.1.4.4. Recent Developments

8.1.4.5. Financial Details

8.1.4.6. Others

8.1.5.Ignis Inc

8.1.5.1. Business Description

8.1.5.2. Product Portfolio

8.1.5.3. Collaborations & Alliances

8.1.5.4. Recent Developments

8.1.5.5. Financial Details

8.1.5.6. Others

8.1.6.Dongwon F&B Co Ltd

8.1.6.1. Business Description

8.1.6.2. Product Portfolio

8.1.6.3. Collaborations & Alliances

8.1.6.4. Recent Developments

8.1.6.5. Financial Details

8.1.6.6. Others

8.1.7.Nong Shim Kellogg Co

8.1.7.1. Business Description

8.1.7.2. Product Portfolio

8.1.7.3. Collaborations & Alliances

8.1.7.4. Recent Developments

8.1.7.5. Financial Details

8.1.7.6. Others

8.1.8.Lotte Wellfood Co Ltd

8.1.8.1. Business Description

8.1.8.2. Product Portfolio

8.1.8.3. Collaborations & Alliances

8.1.8.4. Recent Developments

8.1.8.5. Financial Details

8.1.8.6. Others

8.1.9.Kun6man Inc

8.1.9.1. Business Description

8.1.9.2. Product Portfolio

8.1.9.3. Collaborations & Alliances

8.1.9.4. Recent Developments

8.1.9.5. Financial Details

8.1.9.6. Others

8.1.10. Boryung Pharmaceutical Co Ltd

8.1.10.1. Business Description

8.1.10.2. Product Portfolio

8.1.10.3. Collaborations & Alliances

8.1.10.4. Recent Developments

8.1.10.5. Financial Details

8.1.10.6. Others

9. Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Product Type |

|

| By Sales Channel |

|

| By Ingredients |

|

| By Functionality |

|

| By End User |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.