South Africa Construction Equipment Rental Market Report: Trends, Growth and Forecast (2026-2032)

By Equipment Type (Earthmoving Equipment, Material Handling Equipment, Other Construction Equipment), By Propulsion (Diesel, Gas, CNG, LPG, Electric), By Application (Power & Utilities, Mining, Hospitality, Residential, Healthcare & Educational, Roads & Highway, Manufacturing Units, Others), By Engine Capacity (< 5L, 5–10L, 10L), By Power Output (< 100 HP, 101–200 HP, 201–400 HP, 400 HP) ... Read more

|

Major Players

|

South Africa Construction Equipment Rental Market Statistics and Insights, 2026

- Market Size Statistics

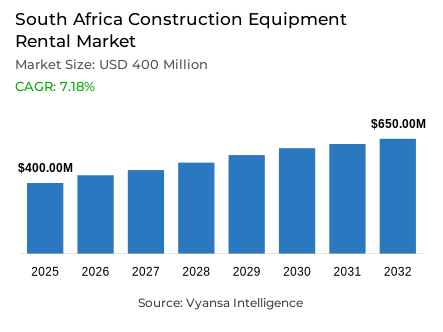

- Construction equipment rental market size in South Africa was valued at USD 400 million in 2025 and is estimated at USD 462 million in 2026.

- The market size is expected to grow to USD 650 million by 2032.

- Market to register a CAGR of around 7.18% during 2026-32.

- Equipment Type Shares

- Earthmoving equipment grabbed market share of 45%.

- Competition

- More than 10 companies are actively engaged in producing construction equipment rental in South Africa.

- Top 5 companies acquired around 45% of the market share.

- Goscor Earthmoving, Hiretech, Stampede, Caterpillar Inc., Babcock International Group etc., are few of the top companies.

- Application

- Roads & highway grabbed 30% of the market.

South Africa Construction Equipment Rental Market Outlook

The South Africa construction equipment rental market was valued at USD 400 million in 2025 and is projected to advance from USD 462 million in 2026 to USD 650 million by 2032, registering a CAGR of 7.18% across the forecast period. This sustained expansion reflects a structural shift within South Africa's construction and infrastructure sector toward fleet flexibility, where contractors increasingly prefer construction machinery rental South Africa arrangements over capital-intensive ownership to reduce balance-sheet exposure, eliminate idle-machine risk, and align equipment availability precisely with the phased requirements of roadworks, utility upgrades, mining support, and public infrastructure programmes. Growth is anchored not in private building activity but in the recurring machinery demand generated by a nationally funded infrastructure investment programme of exceptional scale.

The country's public expenditure pipeline provides the South Africa construction equipment rental market with a structurally dependable demand foundation. As per data published by the Government of South Africa, public infrastructure spending over the three-year medium-term expenditure framework is projected to exceed R1 trillion, with R402 billion directed toward transport and logistics, R219.2 billion toward energy infrastructure, and R156.3 billion toward water and sanitation, each sector generating sustained demand for excavators, loaders, bulldozers, graders, cranes, rollers, tippers, forklifts, and diesel generators across overlapping project phases.

Road infrastructure represents the most commercially reliable and equipment-intensive component of this demand base. According to statistics released by the National Treasury of South Africa, R93.1 billion is allocated to SANRAL for active maintenance and rehabilitation of the 24,000-kilometre national road network, while R53.1 billion supports provincial road maintenance and refurbishment, creating continuous machinery requirements for earthworks, grading, compaction, drainage, material handling, and pavement preparation that align naturally with equipment rental for road construction rather than fleet ownership.

The broader construction environment remains mixed, which reinforces rather than undermines the rental model's commercial relevance. Evidence drawn from public data released by Statistics South Africa confirms that real GDP grew only 0.1% in Q1 2025 before strengthening to 0.8% in Q2 2025, while construction recorded its third consecutive quarterly decline in Q2 due to weakness in residential and non-residential building activity. This uneven output environment encourages contractors to avoid heavy ownership commitments and favour flexible plant hire South Africa arrangements that convert capital expenditure into project-linked operating cost.

South Africa Construction Equipment Rental Market Growth Driver

Infrastructure Spending Scale and Multi-Sector Project Execution Are Generating Sustained Fleet Demand

The primary commercial driver within the South Africa construction equipment rental market is the nationally funded infrastructure spending programme that creates recurring and multi-sector machinery demand across transport, energy, water, and logistics projects that require equipment-intensive execution at every phase. As per data published by the Government of South Africa, the 2025 Budget directs R402 billion toward transport and logistics, R219.2 billion toward energy, and R156.3 billion toward water and sanitation, with each sector requiring different machine combinations across clearing, trenching, foundation preparation, drainage, compaction, material handling, and site power that rental providers can service more efficiently than individual contractor-owned fleets.

Economic and multilateral support reinforces this driver with institutional depth and medium-term investment credibility. Validated reports from the IMF confirm that South Africa's economic growth is estimated at 1.3% in 2025 and projected to accelerate to 1.4% in 2026, with investment driven by structural reforms supporting medium-term improvement, while the World Bank approved a USD 1.5 billion operation in June 2025 specifically to support energy security, transmission investment, freight transport efficiency, and Transnet unbundling reforms that can generate substantial downstream civil works, logistics upgrades, and utility infrastructure projects creating sustained earthmoving equipment rental South Africa demand.

South Africa Construction Equipment Rental Market Challenge

Weak Construction Output and Project Execution Delays Are Compressing Fleet Utilization Returns

The most commercially consequential structural challenge within the South Africa heavy equipment rental market is the persistent weakness and uneven distribution of construction output that reduces fleet utilization, pressures pricing discipline, and constrains asset returns across rental providers dependent on consistent equipment deployment. Based on data from Statistics South Africa, the construction industry contracted by 3.8% in Q1 2025, contributing a negative 0.1 percentage point to GDP growth, with weakness concentrated in residential and non-residential buildings, while Q2 2025 saw construction record its third consecutive decline despite broader GDP strengthening to 0.8%, confirming that private building activity remains structurally insufficient to compensate for infrastructure-led demand pockets.

Public-sector execution risk compounds this challenge by creating a disconnect between large budget allocations and immediate equipment demand. Infrastructure budgets must pass through planning, procurement, environmental approval, tender award, contractor mobilisation, and payment cycles before generating actual rental demand, and delays at any stage compress rental windows, intensify competition around peak project periods, and create utilization volatility that smaller providers with limited branch networks and fewer long-term contracts are least equipped to absorb. Macroeconomic pressures including public debt reaching 77% of GDP at end-March 2025, as confirmed by the IMF, further constrain project pacing and affect contractor working capital availability.

Unlock Market Intelligence

Explore the market potential with our data-driven report

South Africa Construction Equipment Rental Market Trend

Maintenance-Led Road Rehabilitation Is Repositioning Rental as a Recurring Operational Tool

A well-defined and commercially significant structural trend is reshaping equipment demand composition within the South Africa construction equipment rental market, as the national infrastructure agenda shifts emphasis from large greenfield development toward active maintenance and rehabilitation of existing road and utility assets, a mode of spending that is highly compatible with flexible rental models and generates more recurring, location-specific, and phase-variable equipment requirements than single large-project ownership justifies. As per data published by the Government of South Africa, the 2025 Budget specifically emphasises maintaining and repairing existing infrastructure alongside building new infrastructure, a dual mandate that diversifies the demand base for road rehabilitation equipment rental across resurfacing, drainage repair, shoulder widening, pavement rehabilitation, and bridge maintenance activities.

SANRAL's 2024/25 operational data reinforces the structural basis of this trend. Evidence drawn from public data released by SANRAL confirms that the 27,478-kilometre national road network is valued at R780 billion and recorded an Overall Condition Index of 64.45 against an annual target of at least 70, signalling a persistent and commercially significant maintenance gap that supports ongoing demand for motor graders, compactors, excavators, loaders, dump trucks, and diesel generators across active rehabilitation programmes running simultaneously across Gauteng, KwaZulu-Natal, Western Cape, Eastern Cape, Limpopo, and Mpumalanga project corridors.

South Africa Construction Equipment Rental Market Opportunity

Energy, Freight, and PPP Reform Are Creating Multi-Category Equipment Rental Demand Beyond Road Construction

The most commercially compelling growth opportunity within the plant hire market South Africa lies in the energy, freight transport, and logistics modernisation agenda that is generating a new and structurally distinct layer of equipment rental demand beyond the established road construction base. As per official figures from the World Bank, the USD 1.5 billion operation approved in June 2025 supports energy security, grid access, municipal distribution, freight transport efficiency, and Transnet unbundling reforms that are expected to generate downstream civil works across transmission corridors, port access roads, intermodal facilities, logistics nodes, and rail maintenance sites, all requiring crane rental South Africa, excavator deployment, forklift operations, compaction equipment, and diesel generator support across early-works and infrastructure upgrading phases.

Public-private partnership reform is expanding the commercial depth of this opportunity by improving project conversion from policy commitment to awarded contract. According to statistics released by the Government of South Africa, new PPP regulations gazetted in 2025 are designed to reduce procedural complexity, increase deal flow, and fast-track infrastructure provision, while the Department of Transport and Transnet's private-sector participation unit has issued requests for information and qualification on ore, chrome, coal, and manganese rail lines and an independent rolling stock leasing company. The African Development Bank's USD 474.6 million loan approved in 2025 supporting infrastructure governance, renewable energy, and climate resilience further strengthens the opportunity outlook for rental providers with multi-category fleets, fast mobilisation capability, and maintenance-backed contract offerings.

Unlock Market Intelligence

Explore the market potential with our data-driven report

South Africa Construction Equipment Rental Market Segmentation Analysis

By Equipment Type

- Earthmoving Equipment

- Material Handling Equipment

- Other Construction Equipment

Earthmoving Equipment commands the highest share within the equipment type category at 45%, reflecting the fundamental and operationally non-negotiable role of excavation, grading, trenching, loading, and hauling machinery at the earliest and most capital-intensive phases of every major construction, infrastructure, road, utility, energy, and mining-support project within the South Africa construction equipment rental market. Contractors consistently prioritise earthmoving equipment rental because machines including excavators, bulldozers, loaders, motor graders, crawler loaders, trenchers, and dump trucks carry high purchase costs, fuel consumption, operator requirements, maintenance schedules, and depreciation risk that are difficult to justify under the uneven project cycles and cautious ownership sentiment that characterise South Africa's current construction environment, where Statistics South Africa confirmed construction's third consecutive quarterly decline in Q2 2025 despite broader GDP growth.

Its dominant share is structurally reinforced by the land- and civil-works intensity of South Africa's infrastructure spending composition, where transport, energy, and water projects all commence with site clearing, trenching, foundation preparation, drainage installation, and access-road construction that require earthmoving machines before any other equipment category becomes relevant. SANRAL's R93.1 billion road maintenance allocation, the R219.2 billion energy infrastructure programme, and the R156.3 billion water and sanitation budget collectively confirm that the sectors driving rental demand are precisely those requiring sustained earthmoving fleet deployment, making this segment's 45% share both commercially durable and structurally supported throughout the forecast period.

By Application

- Power & Utilities

- Mining

- Hospitality

- Residential

- Healthcare & Educational

- Roads & Highway

- Manufacturing Units

- Others

Roads and Highway commands the highest share within the application category at 30%, establishing transport infrastructure construction and rehabilitation as the most commercially significant and equipment-intensive end-use context within the South Africa construction equipment rental market. Contractors executing road projects consistently generate demand across multiple machine categories simultaneously, requiring excavators for drainage and earthworks, motor graders for surface leveling and base preparation, rollers for compaction, loaders for aggregate handling, tippers for haulage, and diesel generator rental South Africa for remote site power, creating a breadth of rental requirements per project that no other single application category currently matches. Its segment leadership reflects the high equipment intensity, phased machinery rotation, and continuous maintenance cycle characteristics that make road projects structurally well-suited to rental rather than ownership models.

The public funding depth behind this segment provides commercial durability that distinguishes it from private building-dependent applications. Based on data from the National Treasury, R402 billion is allocated to transport and logistics over the medium-term expenditure framework, with R93.1 billion directed specifically to SANRAL for national road maintenance and R53.1 billion for provincial road refurbishment, while SANRAL's own reporting confirms a nationally managed road asset base of 27,478 kilometres valued at R780 billion with a condition index gap that necessitates continuous rehabilitation. Flagship projects including the R28 billion N2 Wild Coast Road and R11.5 billion Moloto Road upgrade further confirm that Roads and Highway will remain the most reliable and volume-generating application segment within the South Africa construction equipment rental market through the forecast period.

List of Companies Covered in South Africa Construction Equipment Rental Market

The companies listed below are highly influential in the South Africa construction equipment rental market, with a significant market share and a strong impact on industry developments.

- Goscor Earthmoving

- Hiretech

- Stampede

- Caterpillar Inc.

- Babcock International Group

- John Deere Africa Middle East

- Coastal Hire

- Talisman Hire

- Liebherr Group

- Byrne Equipment Rental

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- South Africa Construction Equipment Rental Market Policies, Regulations, and Standards

- South Africa Construction Equipment Rental Cost Trends, 2022-2032

- Earthmoving Equipment

- Excavators

- Loaders

- Bulldozers

- Skid Steer Loaders

- Motor Graders

- Crawler Loaders

- Trenchers

- Dump Trucks

- Others

- Material Handling Equipment

- Cranes

- Forklifts

- Tippers

- Others

- Other Construction Equipment

- Road Rollers

- Diesel Generators

- Others

- Earthmoving Equipment

- South Africa Construction Equipment Rental Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- South Africa Construction Equipment Rental Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Equipment Type

- Earthmoving Equipment- Market Insights and Forecast 2022-2032, USD Million

- Excavators- Market Insights and Forecast 2022-2032, USD Million

- Loaders- Market Insights and Forecast 2022-2032, USD Million

- Bulldozers- Market Insights and Forecast 2022-2032, USD Million

- Skid Steer Loaders- Market Insights and Forecast 2022-2032, USD Million

- Motor Graders- Market Insights and Forecast 2022-2032, USD Million

- Crawler Loaders- Market Insights and Forecast 2022-2032, USD Million

- Trenchers- Market Insights and Forecast 2022-2032, USD Million

- Dump Trucks- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- Material Handling Equipment- Market Insights and Forecast 2022-2032, USD Million

- Cranes- Market Insights and Forecast 2022-2032, USD Million

- Forklifts- Market Insights and Forecast 2022-2032, USD Million

- Tippers- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- Other Construction Equipment- Market Insights and Forecast 2022-2032, USD Million

- Road Rollers- Market Insights and Forecast 2022-2032, USD Million

- Diesel Generators- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- Earthmoving Equipment- Market Insights and Forecast 2022-2032, USD Million

- By Propulsion

- Diesel- Market Insights and Forecast 2022-2032, USD Million

- Gas- Market Insights and Forecast 2022-2032, USD Million

- CNG- Market Insights and Forecast 2022-2032, USD Million

- LPG- Market Insights and Forecast 2022-2032, USD Million

- Electric- Market Insights and Forecast 2022-2032, USD Million

- By Application

- Power & Utilities- Market Insights and Forecast 2022-2032, USD Million

- Mining- Market Insights and Forecast 2022-2032, USD Million

- Hospitality- Market Insights and Forecast 2022-2032, USD Million

- Residential- Market Insights and Forecast 2022-2032, USD Million

- Healthcare & Educational- Market Insights and Forecast 2022-2032, USD Million

- Roads & Highway- Market Insights and Forecast 2022-2032, USD Million

- Manufacturing Units- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Engine Capacity

- < 5L- Market Insights and Forecast 2022-2032, USD Million

- 5–10L- Market Insights and Forecast 2022-2032, USD Million

- 10L- Market Insights and Forecast 2022-2032, USD Million

- By Power Output

- < 100 HP- Market Insights and Forecast 2022-2032, USD Million

- 101–200 HP- Market Insights and Forecast 2022-2032, USD Million

- 201–400 HP- Market Insights and Forecast 2022-2032, USD Million

- 400 HP- Market Insights and Forecast 2022-2032, USD Million

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Equipment Type

- Market Size & Growth Outlook

- South Africa Earthmoving Equipment Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Propulsion- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Engine Capacity- Market Insights and Forecast 2022-2032, USD Million

- By Power Output- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- South Africa Material Handling Equipment Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Propulsion- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Engine Capacity- Market Insights and Forecast 2022-2032, USD Million

- By Power Output- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- South Africa Other Construction Equipment Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Propulsion- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Engine Capacity- Market Insights and Forecast 2022-2032, USD Million

- By Power Output- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Caterpillar Inc.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Babcock International Group

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- John Deere Africa Middle East

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Coastal Hire

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Talisman Hire

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Goscor Earthmoving

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Hiretech

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Stampede

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Liebherr Group

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Byrne Equipment Rental

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Caterpillar Inc.

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Equipment Type |

|

| By Propulsion |

|

| By Application |

|

| By Engine Capacity |

|

| By Power Output |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.