China Ultrafiltration Market Report: Trends, Growth and Forecast (2026-2032)

By Membrane Material (Polymeric Membranes (Polyvinylidene Fluoride, Polyethersulfone, Polysulfone, Polyacrylonitrile, Polyvinyl Chloride, Others), Ceramic Membranes), By Module Type (Hollow Fiber, Tubular, Plate & Frame, Spiral Wound, Others), By System Type (Pressurized Ultrafiltration Systems, Submerged Ultrafiltration Systems), By Application (Municipal Water Treatment, Municipal Wastewater Treatment, Industrial Process Water Treatment, Wastewater Reuse & Recycling, Desalination Pre treatment, Food & Beverage Processing, Biopharmaceutical & Pharmaceutical Processing, Chemical & Petrochemical Processing, Others), By End Use Industry (Municipal, Food & Beverage, Pharmaceutical & Biotechnology, Chemical & Petrochemical, Power Generation, Oil & Gas, Electronics & Semiconductor, Pulp & Paper, Textile, Others), By Region (North, East, Southwest, Northwest, North East, South) ... Read more

|

Major Players

|

China Ultrafiltration Market Statistics and Insights, 2026

- Market Size Statistics

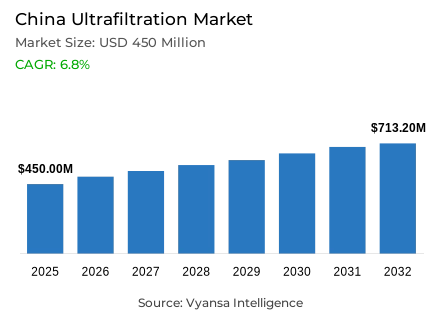

- Ultrafiltration market size in China was valued at USD 450 million in 2025 and is estimated at USD 480.6 million in 2026.

- The market size is expected to grow to USD 713.2 million by 2032.

- Market to register a CAGR of around 6.8% during 2026-32.

- Membrane Material Shares

- Polymeric membranes grabbed market share of 80%.

- Competition

- More than 10 companies are actively engaged in producing ultrafiltration in China.

- Top 5 companies acquired around 15% of the market share.

- Veolia Water Technologies, Pall Corporation, Toray, Beijing OriginWater, Tianjin MOTIMO etc., are few of the top companies.

- Module Type

- Hollow fiber grabbed 54% of the market.

China Ultrafiltration Market Outlook

Valued at USD 450 million in 2025, China ultrafiltration market is advancing from USD 480.6 million in 2026 toward USD 713.2 million by 2032, representing 6.8% compound annual growth rate throughout the forecast window. This steady expansion trajectory reflects rising treatment needs across municipal and industrial applications, strengthened focus on water quality, and growing role of membrane-based systems in modern filtration operations. Market momentum remains underpinned by industrial upgrading toward high-tech production requiring cleaner process water, policy-driven wastewater treatment improvements, and expanding unconventional water reuse creating demand for reliable membrane filtration infrastructure.

Industrial upgrading and high-tech manufacturing expansion establish foundational market driver sustaining consistent demand for ultrafiltration systems throughout China's production sectors. Evidence from National Bureau of Statistics reveals high-tech manufacturing value added rises 8.9% in 2024, with integrated circuit output growing 22.2% in 2024, establishing pronounced industrial technology advancement. This industrial expansion directly translates into heightened market relevance for ultrafiltration systems supporting pre-treatment, polishing, and stable water-quality management across advanced operations. High-tech factories require ultrafiltration supporting reliable removal of suspended solids, colloids, and micro-organisms before downstream processing, enabling better consistency and tighter quality control throughout sophisticated manufacturing environments.

Water treatment standards advancement and green wastewater treatment initiatives reshape China ultrafiltration market toward efficient, environmentally conscious system deployment. Published data from National Development and Reform Commission and Ministry of Housing and Urban-Rural Development indicates first batch of 45 green and low-carbon benchmark sewage treatment plants announced in January 2025, establishing focus on pollution removal alongside energy efficiency and resource recovery. Analysis from Ministry of Housing and Urban-Rural Development reveals cities encouraged building professional plant-network integrated operation systems with centralized urban domestic sewage collection reaching above 73% by 2027, creating demand for ultrafiltration supporting efficient integrated treatment operations. This treatment infrastructure modernization creates market opportunity for membrane-based systems enabling smarter, more connected operations.

Market segmentation demonstrates pronounced demand concentration within polymeric membrane materials and hollow fiber module designs supporting mainstream treatment applications. Polymeric membranes commands 80% market share through broad applicability across municipal and industrial applications supporting practical installation and scalable deployment, while hollow fiber accounts for 54% of module demand reflecting mainstream treatment alignment and efficient system design. This China ultrafiltration market structure indicates end-users increasingly prioritize reliable membrane materials and proven module formats supporting long-term operational stability and large-scale treatment requirements.

China Ultrafiltration Market Growth Driver

Advanced Manufacturing Keeps Filtration Demand Rising

Rapid industrial upgrading and high-tech manufacturing expansion establish sustained demand for ultrafiltration systems supporting cleaner process water and stronger wastewater control. Statistics from National Bureau of Statistics confirm high-tech manufacturing value added rises 8.9% in 2024, with integrated circuit output growing 22.2% in 2024, establishing pronounced industrial technology momentum. This manufacturing expansion directly translates into heightened market relevance for ultrafiltration systems emphasizing reliable removal of suspended solids, colloids, and microorganisms supporting product quality consistency. Advanced industrial operations require ultrafiltration supporting process water stability and efficient reuse of treated water enabling operational efficiency improvements.

Process water quality requirements and manufacturing consistency demands strengthen commercial foundation for comprehensive ultrafiltration system deployment. Published evidence indicates ultrafiltration fits sectors where product quality and process stability matter throughout daily operations, with water treatment systems supporting reliable pre-treatment and polishing functions. High-tech factories expanding production require ultrafiltration systems enabling better consistency, tighter quality control, and more efficient re-use of treated process water. Manufacturing sector growth ensures sustained demand for professional ultrafiltration infrastructure supporting advanced industrial operations throughout extended forecast period.

China Ultrafiltration Market Challenge

Complex Water Quality Keeps Operating Burden High

Ultrafiltration market faces substantial challenge from complexity of pollution loads entering treatment systems affecting membrane performance management. Official records from Ministry of Ecology and Environment indicate groundwater points in Classes I to IV account for 77.9% in 2024, meaning notable share falls outside that range, establishing uneven baseline water quality. This variable feedwater quality profile makes membrane performance harder to manage across different locations and operating conditions. Service providers must develop adaptive ultrafiltration protocols addressing diverse pollution load variations throughout China's treatment environments.

Expanding new-pollutant control initiatives and broadening contaminant scope intensify operating complexity for ultrafiltration systems. Evidence from Ministry of Ecology and Environment reveals China launches two batches of 23 pilot projects in 17 provinces for new-pollutant control covering PFAS, antibiotics, dyeing, and coatings, establishing expanded treatment requirements. This broadening contaminant scope raises pretreatment needs, increases fouling risks, and demands more rigorous operating requirements in complex municipal and industrial treatment environments. Ultrafiltration suppliers must develop enhanced systems addressing emerging pollutants while maintaining reliable performance across conventional contamination profiles.

Unlock Market Intelligence

Explore the market potential with our data-driven report

China Ultrafiltration Market Trend

Green Plant Upgrades Are Shaping Technology Choices

China ultrafiltration market demonstrates pronounced shift toward greener and more efficient wastewater treatment plant operations emphasizing energy efficiency and resource recovery. Market data from National Development and Reform Commission and Ministry of Housing and Urban-Rural Development indicates first batch of 45 green and low-carbon benchmark sewage treatment plants announced in January 2025, establishing industry focus extending beyond pollution removal to environmental performance. This treatment modernization trend supports ultrafiltration deployment within environmentally conscious system frameworks. Green treatment standards create competitive advantages for ultrafiltration providers developing energy-efficient membrane systems and resource recovery capabilities.

Integrated network operations and centralized treatment system coordination strengthen industry-wide adoption of connected ultrafiltration infrastructure. Published data from Ministry of Housing and Urban-Rural Development and four other departments reveals cities encouraged building professional plant-network integrated operation systems, with centralized urban domestic sewage collection reaching above 73% by 2027. This network-level integration supports market expansion for ultrafiltration systems incorporating digital monitoring, predictive maintenance, and smart operational controls. Connected treatment infrastructure enables service providers developing integrated ultrafiltration solutions to establish competitive advantages supporting sustained market growth.

China Ultrafiltration Market Opportunity

Reuse Expansion Opens the Broadest Growth White Space

Strong opportunities emerge in reclaimed water and unconventional water reuse supporting industrial recycling and municipal water sustainability initiatives. Official records from State Council indicate China's unconventional water utilization exceeds 25 billion cubic meters in 2025, with water use per unit of GDP and per unit of industrial value added falling more than 20% and 25% respectively from 2020 levels. This substantial unconventional water deployment directly supports ultrafiltration market expansion through demand for reliable membrane-based treatment enabling safe water reuse. Reclaimed water projects represent growth opportunity for ultrafiltration providers developing specialized systems optimized for reuse applications.

Policy-driven water resource efficiency and tax incentives strengthen commercial foundation for unconventional water ultrafiltration deployment. Evidence from National Development and Reform Commission reveals 2024 water resource tax reform exempts reclaimed water and other unconventional water from water resource tax, helping lower usage costs. This favorable policy environment creates better commercial room for ultrafiltration in industrial recycling, municipal reuse, and regional reclaimed-water projects requiring dependable membrane-based treatment. Tax exemptions and policy support directly improve project economics supporting accelerated ultrafiltration adoption across water reuse applications throughout China.

Unlock Market Intelligence

Explore the market potential with our data-driven report

China Ultrafiltration Market Segmentation Analysis

By Membrane Material

- Polymeric Membranes

- Polyvinylidene Fluoride

- Polyethersulfone

- Polysulfone

- Polyacrylonitrile

- Polyvinyl Chloride

- Others

- Ceramic Membranes

Polymeric membranes commands market leadership at 80% share within China ultrafiltration market, establishing dominant membrane-material positioning through broad applicability across municipal and industrial applications. This market segment maintains leading position due to industry preference for materials easier to use across diverse treatment requirements, supporting practical installation and scalable deployment. Polymeric membrane solutions deliver accessible positioning supporting routine operational use while maintaining adequate filtration performance across varied feedwater conditions, establishing broad appeal across municipal and industrial operators seeking reliable ultrafiltration solutions.

This market leadership position reflects buyers' continued selection of membrane materials supporting practical installation and commercial familiarity. Polymeric membranes remain important because they provide established option for different treatment setups while supporting broad deployment across expanding water treatment requirements. The 80% market share indicates this segment continues shaping material demand, supplier focus, and broader direction of ultrafiltration adoption throughout China market. Manufacturers maintaining polymeric membrane leadership develop competitive advantages enabling broader market penetration and sustained revenue growth supporting category expansion.

By Module Type

- Hollow Fiber

- Tubular

- Plate & Frame

- Spiral Wound

- Others

Hollow fiber commands market leadership at 54% share within China ultrafiltration market, establishing dominant module-type positioning through alignment with mainstream water and wastewater treatment needs across municipal and industrial installations. This market segment maintains leading position due to end-user preference for module designs fitting large-scale treatment requirements and supporting efficient system design, enabling broad application suitability. Hollow fiber solutions deliver accessible positioning supporting routine operational deployment while maintaining adequate filtration performance across industrial and municipal environments, establishing broad appeal across operators seeking scalable ultrafiltration systems.

This market leadership position reflects end-users' continued selection of module types supporting efficient system design and operational scalability. Hollow fiber remains important because it aligns well with large-scale treatment requirements and ongoing system expansion across different end-use sectors. The 54% market share indicates this segment continues influencing module selection, project design, and broader technology structure throughout China ultrafiltration industry. Manufacturers maintaining hollow fiber module leadership develop competitive advantages enabling customer retention and sustained market growth supporting category expansion throughout extended forecast period.

List of Companies Covered in China Ultrafiltration Market

The companies listed below are highly influential in the China ultrafiltration market, with a significant market share and a strong impact on industry developments.

- Veolia Water Technologies

- Pall Corporation

- Toray

- Beijing OriginWater

- Tianjin MOTIMO

- Litree

- Scinor

- DuPont Water Solutions

- Asahi Kasei Microza

- Pentair X-Flow

Market News & Updates

- DuPont Water Solutions, 2026:

DuPont launched Inge™ ultrafiltration modules with integrated pre-filter in April 2026. The product combines pre-filtration and ultrafiltration inside one module housing. This design reduces plant footprint, standalone pre-filtration needs, and related operating costs. It supports drinking water, seawater, expansion, and containerized treatment applications. DuPont’s China website confirms its portfolio includes ultrafiltration membranes and advanced separation technologies. This launch is important for China’s ultrafiltration market because compact UF systems suit dense municipal, industrial, and desalination projects. The product also strengthens UF-RO pretreatment adoption across water reuse applications. It supports operators seeking smaller plants, simpler design, and reliable feedwater quality.

- Toray, 2026:

Toray announced a lower-biofouling ultrafiltration membrane module launch in April 2026. The module features a 0.005-micrometer nominal pore size for advanced UF separation. This development directly supports China’s demand for higher-quality wastewater reuse and industrial water recovery. Toray’s China Water Treatment Research Laboratories develop advanced water supply, wastewater reuse, industrial discharge reuse, and desalination technologies. They also provide technical support for Toray membrane products in China. The launch improves Toray’s positioning in high-performance UF systems for Chinese water projects. It can reduce downstream RO fouling risks and improve long-term system stability. The update strengthens China’s transition toward efficient UF-based reuse infrastructure.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- China Ultrafiltration Market Policies, Regulations, and Standards

- China Ultrafiltration Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- China Ultrafiltration Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Membrane Material

- Polymeric Membranes- Market Insights and Forecast 2022-2032, USD Million

- Polyvinylidene Fluoride- Market Insights and Forecast 2022-2032, USD Million

- Polyethersulfone- Market Insights and Forecast 2022-2032, USD Million

- Polysulfone- Market Insights and Forecast 2022-2032, USD Million

- Polyacrylonitrile- Market Insights and Forecast 2022-2032, USD Million

- Polyvinyl Chloride- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- Ceramic Membranes- Market Insights and Forecast 2022-2032, USD Million

- Polymeric Membranes- Market Insights and Forecast 2022-2032, USD Million

- By Module Type

- Hollow Fiber- Market Insights and Forecast 2022-2032, USD Million

- Tubular- Market Insights and Forecast 2022-2032, USD Million

- Plate & Frame- Market Insights and Forecast 2022-2032, USD Million

- Spiral Wound- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By System Type

- Pressurized Ultrafiltration Systems- Market Insights and Forecast 2022-2032, USD Million

- Submerged Ultrafiltration Systems- Market Insights and Forecast 2022-2032, USD Million

- By Application

- Municipal Water Treatment- Market Insights and Forecast 2022-2032, USD Million

- Municipal Wastewater Treatment- Market Insights and Forecast 2022-2032, USD Million

- Industrial Process Water Treatment- Market Insights and Forecast 2022-2032, USD Million

- Wastewater Reuse & Recycling- Market Insights and Forecast 2022-2032, USD Million

- Desalination Pre treatment- Market Insights and Forecast 2022-2032, USD Million

- Food & Beverage Processing- Market Insights and Forecast 2022-2032, USD Million

- Biopharmaceutical & Pharmaceutical Processing- Market Insights and Forecast 2022-2032, USD Million

- Chemical & Petrochemical Processing- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By End Use Industry

- Municipal- Market Insights and Forecast 2022-2032, USD Million

- Food & Beverage- Market Insights and Forecast 2022-2032, USD Million

- Pharmaceutical & Biotechnology- Market Insights and Forecast 2022-2032, USD Million

- Chemical & Petrochemical- Market Insights and Forecast 2022-2032, USD Million

- Power Generation- Market Insights and Forecast 2022-2032, USD Million

- Oil & Gas- Market Insights and Forecast 2022-2032, USD Million

- Electronics & Semiconductor- Market Insights and Forecast 2022-2032, USD Million

- Pulp & Paper- Market Insights and Forecast 2022-2032, USD Million

- Textile- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Region

- North- Market Insights and Forecast 2022-2032, USD Million

- East- Market Insights and Forecast 2022-2032, USD Million

- Southwest- Market Insights and Forecast 2022-2032, USD Million

- Northwest- Market Insights and Forecast 2022-2032, USD Million

- North East- Market Insights and Forecast 2022-2032, USD Million

- South- Market Insights and Forecast 2022-2032, USD Million

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Membrane Material

- Market Size & Growth Outlook

- China Polymeric Membranes Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Module Type- Market Insights and Forecast 2022-2032, USD Million

- By System Type- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By End Use Industry- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- China Ceramic Membranes Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Module Type- Market Insights and Forecast 2022-2032, USD Million

- By System Type- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By End Use Industry- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Beijing OriginWater

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Tianjin MOTIMO

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Litree

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Scinor

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- DuPont Water Solutions

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Veolia Water Technologies

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Pall Corporation

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Toray

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Asahi Kasei Microza

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Pentair X Flow

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Beijing OriginWater

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Membrane Material |

|

| By Module Type |

|

| By System Type |

|

| By Application |

|

| By End Use Industry |

|

| By Region |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.