South Africa Childrenswear Market Report: Trends, Growth and Forecast (2026-2032)

Product Type (Apparel (Baby and Toddler Wear, Boys Apparel, Girls Apparel), Footwear (Boys Footwear, Girls Footwear), Accessories (Boys Accessories, Girls Accessories), Others), Age Group (Infant/Toddler (Below 2 years), Kids/Children (2 - 14 years)), Price Category (Mass, Premium), Sales Channel (Retail Offline, Retail Online) ... Read more

|

Major Players

|

South Africa Childrenswear Market Statistics and Insights, 2026

- Market Size Statistics

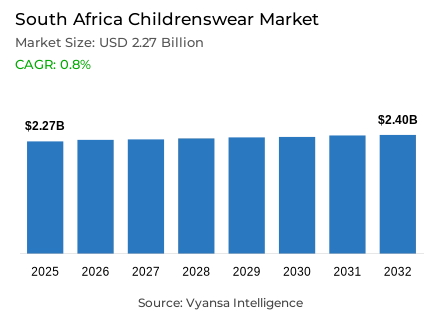

- Childrenswear in South Africa is estimated at USD 2.27 billion.

- The market size is expected to grow to USD 2.4 billion by 2032.

- Market to register a cagr of around 0.8% during 2026-32.

- Product Type Shares

- Apparel grabbed market share of 75%.

- Competition

- More than 10 companies are actively engaged in producing childrenswear in South Africa.

- Top 5 companies acquired around 30% of the market share.

- Pick 'n' Pay Retailers (Pty) Ltd; Retailability Group; Nike South Africa Pty Ltd; Mr Price Group Ltd; Foschini Group Ltd etc., are few of the top companies.

- Sales Channel

- Retail offline grabbed 90% of the market.

South Africa Childrenswear Market Outlook

The South Africa childrenswear market was valued at USD 2.27 billion in 2025 and is set to touch USD 2.4 billion by 2032, growing at a CAGR of around 0.8% during 2026–2032. Changing family structures and increasing disposable incomes, particularly among dual-income households, propel growth. With smaller families, parents have more to spend on discretionary items such as clothes, while social media remains a key driver of style preferences for both parents and their children. The apparel segment leads the market with 75% owing to the demand for fashionable and licensed products based on children's shows and online content.

Competition for the market, however, is increasing with the emergence of international online platforms like Shein and Temu, which offer trendy, low-cost options to local brands. Imports remain popular at present but may soon become less affordable if subject to import taxes, and demand may shift towards domestic players. The strategy of local childrenswear brands has been to focus on target niche markets with personalized and handmade designs. Rupert & Rosie and Myang, among other brands, have taken advantage of the "Made in South Africa" identity and social media storytelling as avenues to capture high-end end userss who look for specialty pieces.

International brands like Forever New and Zara will further solidify this market with new launches, targeting upper-income parents who seek quality, durability, and eco-friendliness. These collections cater to aspirational end userss seeking exclusivity and timelessness in design. Meanwhile, social media remains a key driver in shaping brand discovery and fashion choices, ranging from parents to child influencers who participate actively in new trends and product lines.

Meanwhile, affordability pressures and sustainability awareness are fostering the rise of second-hand childrenswear. Retailers such as Yaga, whose outlets sell imported branded items, alongside online players, are on the rise as parents seek more affordable, environmentally friendly options. Traditional stores remain core to the market, with 90% of sales coming from retail offline, but this is supplemented by an increasingly dynamic online and social commerce environment that offers support for brick-and-mortar retail.

South Africa Childrenswear Market Growth DriverIncomes on the Rise, Shifting Family Structures Boost Market Growth

Strong momentum in household income increases and changes in family structure have acted as main drivers in the childrenswear market of South Africa. Increased female workforce participation has meant dual-income households can allocate higher portions of their budgets towards discretionary spending, including children's apparel and accessories. In other words, this economic stability permitted parents to spend on high-quality, fashionable, and comfortable clothes for their children. According to Stats SA, female labour force participation stood at 47.5% in 2024, which is higher compared to previous years.

Urbanisation is speeding up the adoption of fashion and is also a factor in the choice of clothing preferred by families. The World Bank estimates that 68% of South Africa's population is currently living in urban areas, thus exposing them to international fashion trends and the use of social media. Urban parents are becoming more interested in fashionable, long-lasting, aspirational designs reflective of social standing and lifestyle. All these socioeconomic and cultural changes continue to create a solid foundation for further sustained market growth.

South Africa Childrenswear Market TrendSocial Media and Local Brand Influence on Children’s Fashion

Social media has become a key driver in South Africa into the fashion trends in children, hence reimagining how families interact with brands and style. It acts as an essential place of discovery where trends create, launch, or establish themselves, thanks to platforms like Instagram, TikTok, and Facebook. Influencer marketing, including campaigns involving child influencers, has raised consciousness around fashionable clothing and driven more parents toward digital retail. According to We Are Social, 82% of South Africans aged 16–64 are active social media users, among the highest engagement rates on the continent.

This digital transformation has also given rise to strong local brands, such as Myang and Rupert & Rosie, realizing the importance of exclusively made, superior-quality children's wear. Their emphasis on craftsmanship, sustainability, and personalization resonates with high-end, urban parents who identify themselves through authenticity and community-focused values. The growing visibility of these local labels is very much representative of a wider cultural shift in support of homegrown design and the small business in South Africa's evolving fashion landscape.

Unlock Market Intelligence

Explore the market potential with our data-driven report

South Africa Childrenswear Market OpportunityGrowing Popularity of Second-Hand and Sustainable Fashion

A higher acceptance of second-hand apparel presents a significant growth opportunity for the childrenswear market in South Africa. With growing inflation and increased environmental awareness, parents are more willing to embrace circular fashion through resale platforms and community-based exchanges. According to the DFFE, it is estimated that textile waste comprises nearly 5% of total landfill volume. This suggests the need to adopt sustainable consumption patterns. Furthermore, the South African Reserve Bank estimates that end users prices surged 5.5% year-on-year in 2024, hence, affordability has become a major driver of purchase decisions.

Platforms for the secondhand marketplace, like Yaga, along with branded thrift boutiques, are on the rise; these offer high-quality used clothes at more reasonably priced levels. Beyond economic practicality, this model also resonates with eco-conscious end users values that emphasize waste reduction and resource efficiency. As sustainable fashion becomes increasingly mainstreamed, the resale and recycling ecosystem is set to become a key driver in shaping future growth within South Africa's childrenswear industry.

Unlock Market Intelligence

Explore the market potential with our data-driven report

South Africa Childrenswear Market Segmentation Analysis

By Product Type

- Apparel

- Footwear

- Accessories

- Others

The segment with highest market share under Product Type is Apparel holding approximately 75% of the market share in the South Africa childrenswear market. This growth is credited to increasing exposure to social media among parents and children alike, increasing awareness and demand for international fashion and licensed apparel. With declining family size and growing numbers of dual-income families, parents are spending more on quality and fashionable clothing that expresses individuality and comfort.

Affluent families emerge with a strong demand for high-end and fashionable clothing, where material quality, craftsmanship, and design take precedence. Meanwhile, apparel enjoys wide appeal across income groups. As high-income end userss continue to favour premium local and international brands, middle- and low-income households are increasingly meeting their needs with either low-cost imports or second-hand apparel. This mix of aspirational fashion and value will keep apparel at the top of South Africa's childrenswear market well into the forecast period.

By Sales Channel

- Retail Offline

- Retail Online

The segment with highest market share under Sales Channel is retail offline captures around 90% of the market share in the South Africa childrenswear market. Physical retail remains the preferred shopping channel for parents, who value the ability to check product quality, fit, and material before buying. Dominated by established retailers, department stores, and branded outlets, this space caters to a wide range of price points — from premium boutiques to mass-market chains. Shopping in stores also aligns with South Africa’s social culture, where families often prefer in-person browsing and purchasing experiences.

Although developing, the online channels like Shein and Temu have limited coverage compared to offline brick-and-mortar stores because of the challenge of logistics and delivery costs. Offline retail channels can still build end users trust through personalized services, brand familiarity, and convenient accessibility. With an increasing number of local designers and premium brands expanding their store presence, retail offline is very likely to maintain its strong dominance in the South Africa childrenswear market.

List of Companies Covered in South Africa Childrenswear Market

The companies listed below are highly influential in the South Africa childrenswear market, with a significant market share and a strong impact on industry developments.

- Pick 'n' Pay Retailers (Pty) Ltd

- Retailability Group

- Nike South Africa Pty Ltd

- Mr Price Group Ltd

- Foschini Group Ltd

- Pepkor Holdings Ltd

- Woolworths Holdings Ltd (South Africa)

- Truworths Group Pty Ltd

- Roadget Business Pte Ltd

- Cotton On Clothing Pty Ltd

Frequently Asked Questions

Related Report

1. Market Segmentation

1.1. Research Scope

1.2. Research Methodology

1.3. Definitions and Assumptions

2. Executive Summary

3. South Africa Childrenswear Market Policies, Regulations, and Standards

4. South Africa Childrenswear Market Dynamics

4.1. Growth Factors

4.2. Challenges

4.3. Trends

4.4. Opportunities

5. South Africa Childrenswear Market Statistics, 2022-2032F

5.1. Market Size & Growth Outlook

5.1.1.By Revenues in USD Million

5.2. Market Segmentation & Growth Outlook

5.2.1.By Product Type

5.2.1.1. Apparel- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.1. Baby and Toddler Wear- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.2. Boys Apparel- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.3. Girls Apparel- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2. Footwear- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.1. Boys Footwear- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.2. Girls Footwear- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3. Accessories- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3.1. Boys Accessories- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3.2. Girls Accessories- Market Insights and Forecast 2022-2032, USD Million

5.2.1.4. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.2.By Age Group

5.2.2.1. Infant/Toddler (Below 2 years)- Market Insights and Forecast 2022-2032, USD Million

5.2.2.2. Kids/Children (2 - 14 years)- Market Insights and Forecast 2022-2032, USD Million

5.2.3.By Price Category

5.2.3.1. Mass- Market Insights and Forecast 2022-2032, USD Million

5.2.3.2. Premium- Market Insights and Forecast 2022-2032, USD Million

5.2.4.By Sales Channel

5.2.4.1. Retail Offline- Market Insights and Forecast 2022-2032, USD Million

5.2.4.2. Retail Online- Market Insights and Forecast 2022-2032, USD Million

5.2.5.By Competitors

5.2.5.1. Competition Characteristics

5.2.5.2. Market Share & Analysis

6. South Africa Apparel Childrenswear Market Statistics, 2022-2032

6.1. Market Size & Growth Outlook

6.1.1.By Revenues in USD Million

6.2. Market Segmentation & Growth Outlook

6.2.1.By Age Group- Market Insights and Forecast 2022-2032, USD Million

6.2.2.By Price Category- Market Insights and Forecast 2022-2032, USD Million

6.2.3.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

7. South Africa Footwear Childrenswear Market Statistics, 2022-2032

7.1. Market Size & Growth Outlook

7.1.1.By Revenues in USD Million

7.2. Market Segmentation & Growth Outlook

7.2.1.By Age Group- Market Insights and Forecast 2022-2032, USD Million

7.2.2.By Price Category- Market Insights and Forecast 2022-2032, USD Million

7.2.3.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

8. South Africa Accessories Childrenswear Market Statistics, 2022-2032

8.1. Market Size & Growth Outlook

8.1.1.By Revenues in USD Million

8.2. Market Segmentation & Growth Outlook

8.2.1.By Age Group- Market Insights and Forecast 2022-2032, USD Million

8.2.2.By Price Category- Market Insights and Forecast 2022-2032, USD Million

8.2.3.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

9. Competitive Outlook

9.1. Company Profiles

9.1.1.Mr Price Group Ltd

9.1.1.1. Business Description

9.1.1.2. Product Portfolio

9.1.1.3. Collaborations & Alliances

9.1.1.4. Recent Developments

9.1.1.5. Financial Details

9.1.1.6. Others

9.1.2.Foschini Group Ltd, The

9.1.2.1. Business Description

9.1.2.2. Product Portfolio

9.1.2.3. Collaborations & Alliances

9.1.2.4. Recent Developments

9.1.2.5. Financial Details

9.1.2.6. Others

9.1.3.Pepkor Holdings Ltd

9.1.3.1. Business Description

9.1.3.2. Product Portfolio

9.1.3.3. Collaborations & Alliances

9.1.3.4. Recent Developments

9.1.3.5. Financial Details

9.1.3.6. Others

9.1.4.Woolworths Holdings Ltd (South Africa)

9.1.4.1. Business Description

9.1.4.2. Product Portfolio

9.1.4.3. Collaborations & Alliances

9.1.4.4. Recent Developments

9.1.4.5. Financial Details

9.1.4.6. Others

9.1.5.Truworths Group Pty Ltd

9.1.5.1. Business Description

9.1.5.2. Product Portfolio

9.1.5.3. Collaborations & Alliances

9.1.5.4. Recent Developments

9.1.5.5. Financial Details

9.1.5.6. Others

9.1.6.Pick 'n' Pay Retailers (Pty) Ltd

9.1.6.1. Business Description

9.1.6.2. Product Portfolio

9.1.6.3. Collaborations & Alliances

9.1.6.4. Recent Developments

9.1.6.5. Financial Details

9.1.6.6. Others

9.1.7.Retailability Group

9.1.7.1. Business Description

9.1.7.2. Product Portfolio

9.1.7.3. Collaborations & Alliances

9.1.7.4. Recent Developments

9.1.7.5. Financial Details

9.1.7.6. Others

9.1.8.Nike South Africa Pty Ltd

9.1.8.1. Business Description

9.1.8.2. Product Portfolio

9.1.8.3. Collaborations & Alliances

9.1.8.4. Recent Developments

9.1.8.5. Financial Details

9.1.8.6. Others

9.1.9.Roadget Business Pte Ltd

9.1.9.1. Business Description

9.1.9.2. Product Portfolio

9.1.9.3. Collaborations & Alliances

9.1.9.4. Recent Developments

9.1.9.5. Financial Details

9.1.9.6. Others

9.1.10. Cotton On Clothing Pty Ltd

9.1.10.1. Business Description

9.1.10.2. Product Portfolio

9.1.10.3. Collaborations & Alliances

9.1.10.4. Recent Developments

9.1.10.5. Financial Details

9.1.10.6. Others

10. Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Product Type |

|

| By Age Group |

|

| By Price Category |

|

| By Sales Channel |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.