South Africa Bottled Water Market Report: Trends, Growth and Forecast (2026-2032)

By Type of Water (Carbonated Bottled Water, Flavoured Bottled Water, Functional Bottled Water, Still Bottled Water), By Sub Types (Purified (Desalinated, Atmospheric Generated, Others), Mineral, Other (Spring, Alkaline, Other)), By Packaging Material (Flexible Packaging (Aluminium, Pouches), Glass, Rigid Plastic (PET Bottles, Thin Wall Plastic Containers, Others)), By Price Category (Budget, Economy, Premium), By Pack Size (100 ml, 125 ml, 200 ml, 250 ml, 330 ml, 370 ml, 450 ml, 500 ml, 591 ml, 750 ml, 1,000 ml, 1,500 ml, 4,000 ml, 5,000 ml, Others), By Sales Channel (On Trade (Restaurants, Hotels, Cafes, Others), Off Trade (Grocery Retailers (Convenience Retail, Supermarkets, Hypermarkets, Small Local Grocer), Non-Grocery Retailers (General Merchandise Stores), Vending, E-commerce)), By Region (Gauteng, Western Cape, Eastern Cape, North West, Others) ... Read more

|

Major Players

|

South Africa Bottled Water Market Statistics and Insights, 2026

- Market Size Statistics

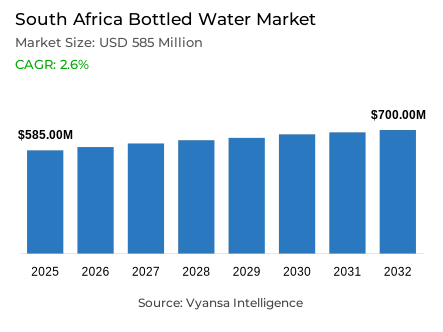

- Bottled water market size in South Africa was estimated at USD 585 million in 2025.

- The market size is expected to grow to USD 700 million by 2032.

- Market to register a CAGR of around 2.6% during 2026-32.

- Type of Water Shares

- Still bottled water grabbed market share of 45%.

- Competition

- Bottled water in South Africa is currently being catered to by more than 15 companies.

- Top 5 companies acquired around 70% of the market share.

- Chill Beverages International (Pty) Ltd, Tsitsikamma Crystal Spring Water CC, Shoprite Checkers (Pty) Ltd, Coca-Cola South Africa (Pty) Ltd, Ekhamanzi Springs (Pty) Ltd etc., are few of the top companies.

- Sales Channel

- Off trade grabbed 85% of the market.

South Africa Bottled Water Market Outlook

The South Africa bottled water market is estimated at around USD 585 million in 2025 and projected to reach about USD 700 million in 2032 with a CAGR of about 2.6% between 2026 and 2032. This small but consistent growth shows that bottled water is no longer a luxury item but a necessity of most households. The ongoing shortages in the municipal water infrastructure have created a stable demand floor that is less prone to economic changes and is rather directly linked to the basic accessibility and safety needs.

Continued breakdowns in water infrastructure perpetuate this trend. More than half of potable water systems fail or barely meet quality standards, and certified high-performance systems are very rare. The leakage has been pronounced, the billing deficit has increased, and the municipal debt has been growing, which has reduced the maintenance capacity, increasing the occurrence of supply disruptions. As a result, bottled water is being relied on more and more during outages, drought warnings, and threats of contamination. The retailers have reacted by increasing supply in times of emergency thus strengthening the role of bottled water as a domestic protection and not just an emergency.

The market is also affected by the increasing awareness about microplastics and PFAS pollution. The environmental and public-health concerns about single-use plastic packaging have increased regulatory compliance requirements and operational costs to manufacturers. Despite the fact that PET is still the most common due to its affordability, an increasing number of health-conscious consumers are increasingly shifting towards glass and aluminium. Tighter adherence to WHO-consistent quality standards has increased the demands on testing, transparency, and packaging decisions, which puts pressure on the margins, but at the same time, it strengthens consumer trust in products that meet quality standards.

However, still bottled water has a 45% market share, supported by its low price, wide format range, and the ongoing year-round need of daily hydration. Off-trade sales channel constitute 85% of the share and the main distribution structure is supermarkets. Their wide geographic reach, bulk-buying capabilities, and timely access during supply interruptions assure their further relevance in market volume forecasts up to 2032.

South Africa Bottled Water Market Growth Driver

Infrastructure Failure Reinforces Bottled Water as a Daily Necessity

The constant failures in municipal water systems are one of the basic drivers of demand in the South Africa bottled water market. National tests show that 52% of drinking water systems are not functioning or barely to the quality standards, and only 26 out of 958 systems, or 3%, have received Blue Drop certification. These shortcomings are most acute in large cities, where water wastage is beyond sustainable levels. In eThekwini alone, 56% of treated water is wasted in leaks and billing inefficiencies, which directly affect the reliability of supply and require rotational limitations. The problem is aggravated by financial distress, with municipal debt to water boards amounting to R22.36 billion, an increase of 151% in five years and a crippling constraint on maintenance and reinvestment.

These systemic failures have repositioned bottled water as a luxury item into a utility item among millions of end users. Bottled water is becoming a primary source of safe drinking water and not a secondary source during declared outages, drought conditions, and contamination risks. Retailers have reacted by increasing the supply of bottled water in times of supply crises, as it is an important part of household resilience. As South Africa is estimated to experience a 17% national water deficit by 2030, the structural reliance on bottled water by end-users is entrenched, supporting the perpetuated baseline demand as municipal instability continues.

South Africa Bottled Water Market Challenge

Health and Packaging Concerns Intensify Market Constraints

The increasing awareness of microplastics and PFAS pollution is becoming a material limitation to the South Africa bottled water market, especially in terms of packaging options and long-term health attitudes. In 2024, the world produced 220 million tonnes of plastic waste, 69.5 million tonnes of which was improperly handled and discharged into the natural environment. Single-use PET bottles are at the centre of environmental and health discussions because they contribute to 40% of all plastic waste. The scientific evidence of synergistic toxicity of combined exposure to PFAS and microplastics has increased the level of scrutiny beyond the individual contamination issues.

PFAS persistence is also a more difficult issue, because the substances are bioaccumulative and have already been associated with thyroid dysfunction, increased cholesterol, liver damage, and a compromised immune system. Although PET packaging is still the most popular because of its affordability and scalability, health-conscious and more affluent end users are moving to glass and aluminium packaging that is seen as safer. The South African National Bottled Water Association has responded by increasing the implementation of water quality standards in line with the WHO guidelines. This heightened compliance expense and operational scrutiny puts margin pressure and at the same time heightens expectations regarding transparency, testing and packaging innovation.

Unlock Market Intelligence

Explore the market potential with our data-driven report

South Africa Bottled Water Market Trend

Digital Grocery Platforms Reshape Purchasing Behaviour

E-commerce has become the most rapidly expanding distribution channel in the South Africa bottled water market, and it has radically transformed the way end users obtain the essential hydration. Online retail grew at an annualised rate of 38% up to 2025, far surpassing the growth of physical retail by 1.6%. By 2025, total e-commerce turnover will be over R130 billion, which is about 10% of total retail sales. The key to this change is grocery-led platforms, with Checkers Sixty60 registering 47% growth in the first half of 2025 and generating R19 billion in sales and Pick n Pay on-demand delivery growing by 60% in its last financial year.

The Woolies Dash by Woolworths also registered almost 50% increase in online grocery sales, which supports the importance of the rapid-delivery platforms in daily shopping. These services have been especially useful in times of municipal water shortages, when physical access is limited, and rapid replenishment is required. Bulk online purchases of bottled water have become normalised through mobile adoption, logistics efficiency, and secure digital payments. End-user behaviour is being transformed by subscription models, personalised recommendations and bundled pricing, making e-commerce a structurally embedded growth channel, not a temporary convenience.

South Africa Bottled Water Market Opportunity

Refill Infrastructure Unlocks Cost and Sustainability Upside

The refill water stations are a major opportunity in the South Africa bottled water market as they directly solve the affordability and plastic waste issues. Refill models enable end users to get purified water at significantly lower prices and reuse containers, eliminating the reliance on single-use packaging. This strategy has proven to be environmentally effective as evidenced by international experience with over 80 refill stations installed by the West Basin Municipal Water District and an estimated 110,000 plastic water bottles being taken out of the waste stream each year. These results underscore refill infrastructure as a scalable waste reduction solution and the increase in access to safe drinking water.

The bottled water industry in South Africa is in a position to facilitate this model through advanced production standards. The members of SANBWA have closed-loop water recycling systems and high-precision filling technologies, with a maximum water-use ratio of 1.6 to 1 litre of product, versus 2.5 to 4 litres in other food and beverage operations. Other forms of sterilisation such as ultraviolet and ozone treatments also save more water and still ensure safety. With the increased regulatory control over refill operations, the compliance with the packaged water standards will become a key to the mainstream adoption.

Unlock Market Intelligence

Explore the market potential with our data-driven report

South Africa Bottled Water Market Segmentation Analysis

By Type of Water

- Carbonated Bottled Water

- Flavoured Bottled Water

- Functional Bottled Water

- Still Bottled Water

Still water holds a 45% market share in the South Africa bottled water market, making it the largest and most stable product category. Its dominance is rooted in affordability and broad format availability, ranging from single-serve PET bottles to multi-packs and bulk options that serve diverse income segments. Still water benefits from consistent, year-round demand, as it is primarily consumed for daily hydration rather than discretionary refreshment. Municipal water disruptions further reinforce its role as a functional necessity, particularly during supply interruptions when households prioritise safe, neutral drinking water.

Intense competition within the still water segment has driven frequent promotions and aggressive pricing strategies across retail channels. Private label offerings from major supermarkets have expanded rapidly, strengthening shelf presence and improving affordability for price-sensitive end users. Unlike sparkling or flavoured alternatives, still water aligns directly with health-oriented behaviour and sugar-reduction priorities, supporting stable volume growth. The combination of price accessibility, crisis relevance, and routine consumption ensures still water remains the core volume driver underpinning the broader market.

By Sales Channel

- On Trade

- Restaurants

- Hotels

- Cafes

- Others

- Off Trade

- Grocery Retailers

- Convenience Retail

- Supermarkets

- Hypermarkets

- Small Local Grocer

- Non-Grocery Retailers

- General Merchandise Stores

- Vending

- E-commerce

- Grocery Retailers

Off-trade retail channels account for 85% of bottled water sales in South Africa, establishing supermarkets as the dominant route to market. Large grocery chains leverage extensive national footprints, competitive pricing structures, and high inventory turnover to meet both routine and emergency demand. These outlets serve multiple end-user segments simultaneously, offering low-cost private labels alongside premium brands, ensuring bottled water remains accessible across income groups. Physical retail also plays a critical role during water outages, providing immediate availability when supply security becomes a priority.

While e-commerce is the fastest-growing channel at 38% annualised growth, it remains secondary in absolute share terms. Supermarkets continue to benefit from accessibility across formal and informal areas, established trust, and the ability to facilitate bulk purchases without delivery delays. Shelf expansion for eco-friendly packaging and functional water formats reflects evolving preferences without eroding core volume. The 85% off-trade share underscores the continued importance of brick-and-mortar retail as the primary distribution backbone of the South Africa bottled water market.

List of Companies Covered in South Africa Bottled Water Market

The companies listed below are highly influential in the South Africa bottled water market, with a significant market share and a strong impact on industry developments.

- Chill Beverages International (Pty) Ltd

- Tsitsikamma Crystal Spring Water CC

- Shoprite Checkers (Pty) Ltd

- Coca-Cola South Africa (Pty) Ltd

- Ekhamanzi Springs (Pty) Ltd

- Clover Waters SA (Pty) Ltd

- Ceres Fruit Juices (Pty) Ltd

- Woolworths (Pty) Ltd

- DGB (Pty) Ltd

- Spar South Africa (Pty) Ltd

Competitive Landscape

South Africa’s bottled water market in 2025 remains led by Coca-Cola South Africa, which maintains overall category leadership through a strong multi-brand strategy. Ekhamanzi Springs’ AQuelle continues to head the market in brand terms, supported by affordable pricing, nationwide distribution, and a wide range spanning still, sparkling, and flavoured variants, alongside sustainability-led innovations such as tethered caps. Coca-Cola’s Valpre strengthens the premium segment, leveraging low-sodium spring water positioning, eco-friendly bottling, and strong visibility in hospitality and corporate channels. At the same time, private label bottled water from major retailers such as Pick n Pay and Checkers is gaining momentum, driven by competitive pricing, bulk pack formats, and shelf dominance, intensifying competition across value-focused segments.

Frequently Asked Questions

Related Report

1. Market Segmentation

1.1. Research Scope

1.2. Research Methodology

1.3. Definitions and Assumptions

2. Executive Summary

3. South Africa Bottled Water Market Policies, Regulations, and Standards

4. South Africa Bottled Water Market Dynamics

4.1. Growth Factors

4.2. Challenges

4.3. Trends

4.4. Opportunities

5. South Africa Bottled Water Market Statistics, 2022-2032F

5.1. Market Size & Growth Outlook

5.1.1.By Revenues in USD Million

5.1.2.By Volume (Million Litres)

5.2. Market Segmentation & Growth Outlook

5.2.1.By Type of Water

5.2.1.1. Carbonated Bottled Water- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2. Flavoured Bottled Water- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3. Functional Bottled Water- Market Insights and Forecast 2022-2032, USD Million

5.2.1.4. Still Bottled Water- Market Insights and Forecast 2022-2032, USD Million

5.2.2.By Sub Types

5.2.2.1. Purified- Market Insights and Forecast 2022-2032, USD Million

5.2.2.1.1. Desalinated- Market Insights and Forecast 2022-2032, USD Million

5.2.2.1.2. Atmospheric Generated- Market Insights and Forecast 2022-2032, USD Million

5.2.2.1.3. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.2.2. Mineral- Market Insights and Forecast 2022-2032, USD Million

5.2.2.3. Other (Spring, Alkaline, Other) - Market Insights and Forecast 2022-2032, USD Million

5.2.3.By Packaging Material

5.2.3.1. Flexible Packaging- Market Insights and Forecast 2022-2032, USD Million

5.2.3.1.1. Aluminium- Market Insights and Forecast 2022-2032, USD Million

5.2.3.1.2. Pouches- Market Insights and Forecast 2022-2032, USD Million

5.2.3.2. Glass- Market Insights and Forecast 2022-2032, USD Million

5.2.3.3. Rigid Plastic- Market Insights and Forecast 2022-2032, USD Million

5.2.3.3.1. PET Bottles- Market Insights and Forecast 2022-2032, USD Million

5.2.3.3.2. Thin Wall Plastic Containers- Market Insights and Forecast 2022-2032, USD Million

5.2.3.3.3. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.4.By Price Category

5.2.4.1. Budget- Market Insights and Forecast 2022-2032, USD Million

5.2.4.2. Economy- Market Insights and Forecast 2022-2032, USD Million

5.2.4.3. Premium- Market Insights and Forecast 2022-2032, USD Million

5.2.5.By Pack Size

5.2.5.1. 100 ml- Market Insights and Forecast 2022-2032, USD Million

5.2.5.2. 125 ml- Market Insights and Forecast 2022-2032, USD Million

5.2.5.3. 200 ml- Market Insights and Forecast 2022-2032, USD Million

5.2.5.4. 250 ml- Market Insights and Forecast 2022-2032, USD Million

5.2.5.5. 330 ml- Market Insights and Forecast 2022-2032, USD Million

5.2.5.6. 370 ml- Market Insights and Forecast 2022-2032, USD Million

5.2.5.7. 450 ml- Market Insights and Forecast 2022-2032, USD Million

5.2.5.8. 500 ml- Market Insights and Forecast 2022-2032, USD Million

5.2.5.9. 591 ml- Market Insights and Forecast 2022-2032, USD Million

5.2.5.10. 750 ml- Market Insights and Forecast 2022-2032, USD Million

5.2.5.11. 1,000 ml- Market Insights and Forecast 2022-2032, USD Million

5.2.5.12. 1,500 ml- Market Insights and Forecast 2022-2032, USD Million

5.2.5.13. 4,000 ml- Market Insights and Forecast 2022-2032, USD Million

5.2.5.14. 5,000 ml- Market Insights and Forecast 2022-2032, USD Million

5.2.5.15. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.6.By Sales Channel

5.2.6.1. On Trade- Market Insights and Forecast 2022-2032, USD Million

5.2.6.1.1. Restaurants- Market Insights and Forecast 2022-2032, USD Million

5.2.6.1.2. Hotels- Market Insights and Forecast 2022-2032, USD Million

5.2.6.1.3. Cafes- Market Insights and Forecast 2022-2032, USD Million

5.2.6.1.4. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.6.2. Off Trade- Market Insights and Forecast 2022-2032, USD Million

5.2.6.2.1. Grocery Retailers- Market Insights and Forecast 2022-2032, USD Million

5.2.6.2.1.1. Convenience Retail- Market Insights and Forecast 2022-2032, USD Million

5.2.6.2.1.2. Supermarkets- Market Insights and Forecast 2022-2032, USD Million

5.2.6.2.1.3. Hypermarkets- Market Insights and Forecast 2022-2032, USD Million

5.2.6.2.1.4. Small Local Grocer- Market Insights and Forecast 2022-2032, USD Million

5.2.6.2.2. Non-Grocery Retailers- Market Insights and Forecast 2022-2032, USD Million

5.2.6.2.2.1. General Merchandise Stores- Market Insights and Forecast 2022-2032, USD Million

5.2.6.2.3. Vending- Market Insights and Forecast 2022-2032, USD Million

5.2.6.2.4. E-commerce- Market Insights and Forecast 2022-2032, USD Million

5.2.7.By Region

5.2.7.1. Gauteng

5.2.7.2. Western Cape

5.2.7.3. Eastern Cape

5.2.7.4. North West

5.2.7.5. Others

5.2.8.By Competitors

5.2.8.1. Competition Characteristics

5.2.8.2. Market Share & Analysis

6. South Africa Carbonated Bottled Water Market Statistics, 2022-2032

6.1. Market Size & Growth Outlook

6.1.1.By Revenues in USD Million

6.1.2.By Volume (Million Litres)

6.2. Market Segmentation & Growth Outlook

6.2.1.By Sub Types- Market Insights and Forecast 2022-2032, USD Million

6.2.2.By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

6.2.3.By Pack Size- Market Insights and Forecast 2022-2032, USD Million

6.2.4.By Price Category- Market Insights and Forecast 2022-2032, USD Million

6.2.5.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

6.2.6.By Region- Market Insights and Forecast 2022-2032, USD Million

7. South Africa Flavoured Bottled Water Market Statistics, 2022-2032

7.1. Market Size & Growth Outlook

7.1.1.By Revenues in USD Million

7.1.2.By Volume (Million Litres)

7.2. Market Segmentation & Growth Outlook

7.2.1.By Sub Types- Market Insights and Forecast 2022-2032, USD Million

7.2.2.By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

7.2.3.By Pack Size- Market Insights and Forecast 2022-2032, USD Million

7.2.4.By Price Category- Market Insights and Forecast 2022-2032, USD Million

7.2.5.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

7.2.6.By Region- Market Insights and Forecast 2022-2032, USD Million

8. South Africa Functional Bottled Water Market Statistics, 2022-2032

8.1. Market Size & Growth Outlook

8.1.1.By Revenues in USD Million

8.1.2.By Volume (Million Litres)

8.2. Market Segmentation & Growth Outlook

8.2.1.By Sub Types- Market Insights and Forecast 2022-2032, USD Million

8.2.2.By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

8.2.3.By Pack Size- Market Insights and Forecast 2022-2032, USD Million

8.2.4.By Price Category- Market Insights and Forecast 2022-2032, USD Million

8.2.5.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

8.2.6.By Region- Market Insights and Forecast 2022-2032, USD Million

9. South Africa Still Bottled Water Market Statistics, 2022-2032

9.1. Market Size & Growth Outlook

9.1.1.By Revenues in USD Million

9.1.2.By Volume (Million Litres)

9.2. Market Segmentation & Growth Outlook

9.2.1.By Sub Types- Market Insights and Forecast 2022-2032, USD Million

9.2.2.By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

9.2.3.By Pack Size- Market Insights and Forecast 2022-2032, USD Million

9.2.4.By Price Category- Market Insights and Forecast 2022-2032, USD Million

9.2.5.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

9.2.6.By Region- Market Insights and Forecast 2022-2032, USD Million

10. Competitive Outlook

10.1. Company Profiles

10.1.1. Coca-Cola South Africa (Pty) Ltd

10.1.1.1. Business Description

10.1.1.2. Product Portfolio

10.1.1.3. Collaborations & Alliances

10.1.1.4. Recent Developments

10.1.1.5. Financial Details

10.1.1.6. Others

10.1.2. Ekhamanzi Springs (Pty) Ltd

10.1.2.1. Business Description

10.1.2.2. Product Portfolio

10.1.2.3. Collaborations & Alliances

10.1.2.4. Recent Developments

10.1.2.5. Financial Details

10.1.2.6. Others

10.1.3. Clover Waters SA (Pty) Ltd

10.1.3.1. Business Description

10.1.3.2. Product Portfolio

10.1.3.3. Collaborations & Alliances

10.1.3.4. Recent Developments

10.1.3.5. Financial Details

10.1.3.6. Others

10.1.4. Ceres Fruit Juices (Pty) Ltd

10.1.4.1. Business Description

10.1.4.2. Product Portfolio

10.1.4.3. Collaborations & Alliances

10.1.4.4. Recent Developments

10.1.4.5. Financial Details

10.1.4.6. Others

10.1.5. Woolworths (Pty) Ltd

10.1.5.1. Business Description

10.1.5.2. Product Portfolio

10.1.5.3. Collaborations & Alliances

10.1.5.4. Recent Developments

10.1.5.5. Financial Details

10.1.5.6. Others

10.1.6. Chill Beverages International (Pty) Ltd

10.1.6.1. Business Description

10.1.6.2. Product Portfolio

10.1.6.3. Collaborations & Alliances

10.1.6.4. Recent Developments

10.1.6.5. Financial Details

10.1.6.6. Others

10.1.7. Tsitsikamma Crystal Spring Water CC

10.1.7.1. Business Description

10.1.7.2. Product Portfolio

10.1.7.3. Collaborations & Alliances

10.1.7.4. Recent Developments

10.1.7.5. Financial Details

10.1.7.6. Others

10.1.8. Shoprite Checkers (Pty) Ltd

10.1.8.1. Business Description

10.1.8.2. Product Portfolio

10.1.8.3. Collaborations & Alliances

10.1.8.4. Recent Developments

10.1.8.5. Financial Details

10.1.8.6. Others

10.1.9. DGB (Pty) Ltd

10.1.9.1. Business Description

10.1.9.2. Product Portfolio

10.1.9.3. Collaborations & Alliances

10.1.9.4. Recent Developments

10.1.9.5. Financial Details

10.1.9.6. Others

10.1.10. Spar South Africa (Pty) Ltd

10.1.10.1.Business Description

10.1.10.2.Product Portfolio

10.1.10.3.Collaborations & Alliances

10.1.10.4.Recent Developments

10.1.10.5.Financial Details

10.1.10.6.Others

11. Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Type of Water |

|

| By Sub Types |

|

| By Packaging Material |

|

| By Price Category |

|

| By Pack Size |

|

| By Sales Channel |

|

| By Region |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.