Singapore Bottled Water Market Report: Trends, Growth and Forecast (2026-2032)

By Type of Water (Carbonated Bottled Water, Flavoured Bottled Water, Functional Bottled Water, Still Bottled Water), By Sub Types (Purified (Desalinated, Atmospheric Generated, Others), Mineral, Other (Spring, Alkaline, Other)), By Packaging Material (Flexible Packaging (Aluminium, Pouches), Glass, Rigid Plastic (PET Bottles, Thin Wall Plastic Containers, Others)), By Price Category (Budget, Economy, Premium), By Pack Size (100 ml, 125 ml, 200 ml, 250 ml, 330 ml, 370 ml, 450 ml, 500 ml, 591 ml, 750 ml, 1,000 ml, 1,500 ml, 4,000 ml, 5,000 ml, Others), By Sales Channel (On Trade (Restaurants, Hotels, Cafes, Others), Off Trade (Grocery Retailers (Convenience Retail, Supermarkets, Hypermarkets, Small Local Grocer), Non-Grocery Retailers (General Merchandise Stores), Vending, E-commerce)) ... Read more

|

Major Players

|

Singapore Bottled Water Market Statistics and Insights, 2026

- Market Size Statistics

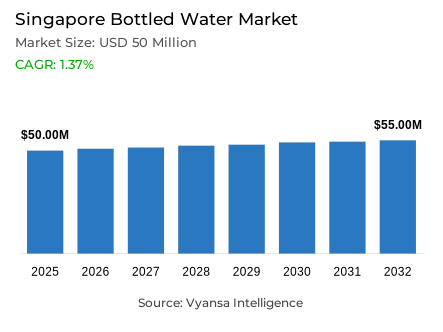

- Bottled water in Singapore is estimated at USD 50 million in 2025.

- The market size is expected to grow to USD 55 million by 2032.

- Market to register a cagr of around 1.37% during 2026-32.

- Type of Water Shares

- Still bottled water grabbed market share of 80%.

- Competition

- Bottled water in Singapore is currently being catered to by more than 5 companies.

- Top 5 companies acquired around 85% of the market share.

- Yee Lee Oils & Foodstuffs (S) Pte Ltd, Otsuka Pharmaceutical Pte Ltd, NTUC FairPrice Co-operative Pte Ltd, Danone Asia Holdings Pte Ltd, F&N Foods (S) Pte Ltd etc., are few of the top companies.

- Sales Channel

- Off trade grabbed 70% of the market.

Singapore Bottled Water Market Outlook

The Singapore bottled water market is estimated to be USD 50 million in 2025 and is projected to increase to almost USD 55 million in 2032, with a relatively low compound annual growth rate of about 1.37% in the 2026-2032 period. The market is characterized by a stable growth, which is a sign of its mature and well-developed position. Bottled water has become a daily routine aspect of daily consumption, supported by increased health awareness and an apparent shift in the consumption of sugar-sweetened drinks to the consumption of calorie-free water. To a significant segment of the end users, bottled water has become the foundation of long-term wellness goals and not just a drink to take occasionally.

Health factors still form the basis of demand in the daily consumption events. Increased attention to non-communicable diseases and sugar intake has strengthened the role of bottled water as a simple and preventive source of hydration in the urban lifestyle. Portability, high quality and easy supply are promoted in a high-density and busy environment of Singapore, which promotes frequent use among office workers, students and commuters. These factors help to sustain the volume demand, despite the fact that the overall market growth is moderate.

The market perspective is increasingly being determined by environmental regulation. The policies of sustainability, especially the upcoming Beverage Container Return Scheme, are placing extra compliance demands on packaging, labeling, and logistics. Although these steps are progressing national recycling and waste-reduction goals, they also increase the cost of operation and limit the flexibility of prices of bottled-water manufacturers, particularly those that use single-use PET packages. Therefore, the margin pressure will be a relevant feature during the forecast period.

The patterns of structural demand remain clearly defined in terms of product categories and channels of distribution. The market is dominated by still bottled water, with a market share of 80% and this indicates its broad applicability in day to day hydration.The off-trade channels contribute to about 70% of the sales, which highlights the importance of supermarkets, hypermarkets, and convenience stores in making daily purchases at home and workplace. Together, these dynamics suggest a stable, health-oriented market that will see a gradual increase in value up to 2032.

Singapore Bottled Water Market Growth Driver

Health-Oriented Hydration Reinforcing Daily Urban Consumption

The increase in health awareness remains a structural factor that promotes the demand of bottled water in the Singapore bottled water market, as the end users are moving towards calorie-free hydration and abandoning the sugar-sweetened drinks. Bottled water is no longer considered a luxury drink but a daily part of healthy living, which is consistent with the long-term health management objectives. This change in behaviour reflects the wider societal health truths, with non-communicable diseases causing at least 43 million deaths worldwide in 2021, which is approximately 75% of non-pandemic-related deaths. These results have solidified the policy focus on healthier food options, which indirectly supports the positioning of bottled water as a safe and preventive hydration source in the urban lifestyle.

In Singapore, the health-led orientation is entrenched, with non-communicable diseases contributing to about 75% of all deaths in 2019, highlighting the structural significance of sugar reduction. The convenience of bottled water, its uniform quality and ready accessibility also contribute to the habitual use of the product by office workers, students, and commuters. These qualities strengthen the repetitive, repeat buying in a high-density, high-paced urban setting, where anchoring consistent volume demand is found in daily consumption events.

Singapore Bottled Water Market Challenge

Environmental Compliance Raising Cost and Operational Pressure

Environmental control is one of the structural limitations of bottled water manufacturers in Singapore because sustainability requirements are becoming more and more important in packaging and logistics. With the Beverage Container Return Scheme to be introduced in April 2026, a refundable deposit on eligible beverage containers is to be introduced to support national recycling goals. Although consistent with long-term waste reduction objectives, the scheme introduces compliance layers in the packaging design, labelling standards, reverse logistics, and deposit administration, making the operations of market participants more complex.

In the case of bottled water brands, especially those that use single-use PET packages, these requirements come at the cost of increased cost structures and decreased pricing flexibility. The deposits, packaging to fit regulatory requirements and returns infrastructure management puts pressure on margins in a market where end users are still price sensitive despite increasing sustainability awareness. Consequently, regulatory compliance serves as a constraining element to short-term profitability and heightens competition in the mass and mid-priced bottled water products.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Singapore Bottled Water Market Trend

Circular Economy Focus Reshaping Packaging and Brand Strategy

Sustainable practices in the Singapore bottled water sector have gained momentum, largely due to government intervention and alterations in social culture. The Zero Waste Masterplan and the Beverage Container Return Scheme exemplify the strong commitment from the government towards establishing a framework for long-term investment through recycling, reuse, and circular resource management. The favourable response to these initiatives has led to various changes in the way bottled water is positioned, fabricated, and delivered; companies are embracing sustainability as a cornerstone of their strategic brand positioning versus merely an adjunct characteristic of bottled water products.

As a result, bottled water manufacturers are re-evaluating their packaging choices and begin to consider alternative options such as higher recyclability, reusable forms of packaging, or using less plastic. Because of the regulatory scheme, the direction that bottled water manufacturers are likely to invest in, and the nature of products under development will be driven by significant incentives to align closely with the national goal of reducing waste. Therefore, the development of innovative packaging, development of brand positioning relative to sustainability, and adopting principles of a circular economy will fundamentally shift how bottled water manufacturers define their long-term sustainability and create competitive advantages that are not limited to price or providing hydration.

Singapore Bottled Water Market Opportunity

Premiumisation and Functional Positioning Supporting Value Expansion

The good economic fundamentals in Singapore provide favourable environment to higher-value bottled water propositions, especially in the premium and functional segments. In 2024, GDP per capita was estimated at USD 90,674, which indicates a high level of purchasing power and a proven willingness of end users to pay a premium to perceive quality, wellness benefits, and sustainability certifications. This economic context underpins bottled water products that are marketed on the basis of mineral content, functional hydration advantages, taste differentiation, and polished brand stories.

Premium bottled water formats help producers to go beyond simple hydration and earn more money by positioning based on lifestyle. The health-conscious and wealthy end users are attracted to functional claims, unique sourcing narratives, and packaging that is environmentally friendly. Simultaneously, service-based models like subscriptions and curated delivery programmes enhance the interaction and promote repeat buying. With the growing trend of bottled water being linked to wellness, quality, and identity, premiumisation is an apparent value addition avenue in a saturated urban market.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Singapore Bottled Water Market Segmentation Analysis

By Type of Water

- Carbonated Bottled Water

- Flavoured Bottled Water

- Functional Bottled Water

- Still Bottled Water

Under the Type of Water segmentation, still bottled water holds the dominant position, accounting for around 80% of the Singapore bottled water market. Its leadership is anchored in its universal suitability for everyday hydration, neutral taste profile, and strong alignment with health-focused consumption habits. Purified and spring water formats continue to meet core hydration needs across households, workplaces, and foodservice settings, reinforcing still bottled water as the default choice for regular use across demographic groups.

While flavoured, carbonated, and functional water variants are gaining visibility and supporting incremental value growth, they remain supplementary rather than substitutive. These formats address specific occasions or preferences but do not displace still bottled water’s central role in daily consumption. As a result, still bottled water continues to underpin volume stability, acting as the structural backbone of the category and ensuring consistent baseline demand across retail and institutional purchasing channels.

By Sales Channel

- On Trade

- Restaurants

- Hotels

- Cafes

- Others

- Off Trade

- Grocery Retailers

- Convenience Retail

- Supermarkets

- Hypermarkets

- Small Local Grocer

- Non-Grocery Retailers

- General Merchandise Stores

- Vending

- E-commerce

- Grocery Retailers

Within the Sales Channel segmentation, off-trade distribution accounts for approximately 70% of bottled water sales, reflecting its deep integration into everyday household and workplace purchasing patterns. Supermarkets and hypermarkets dominate this channel due to their broad assortments, frequent promotions, and ability to support bulk purchasing by families and offices. These formats facilitate high-volume sales of multipacks and larger bottle sizes while also accommodating premium and functional bottled water alongside mass-market offerings.

Convenience stores play a complementary role, catering primarily to on-the-go hydration needs among commuters and office workers. Smaller pack sizes and impulse purchases drive turnover, though limited shelf space and price sensitivity restrict premium expansion. At the same time, direct-to-consumer and subscription-based models are emerging as niche but strategically important avenues, particularly for premium and sustainable bottled water concepts, supporting gradual diversification within the off-trade landscape.

List of Companies Covered in Singapore Bottled Water Market

The companies listed below are highly influential in the Singapore bottled water market, with a significant market share and a strong impact on industry developments.

- Yee Lee Oils & Foodstuffs (S) Pte Ltd

- Otsuka Pharmaceutical Pte Ltd

- NTUC FairPrice Co-operative Pte Ltd

- Danone Asia Holdings Pte Ltd

- F&N Foods (S) Pte Ltd

- Coca-Cola Singapore Beverages Pte Ltd

- Nestlé Singapore Pte Ltd

- Yeo Hiap Seng Ltd

Competitive Landscape

Singapore’s bottled water market in 2025 is highly competitive, driven by innovation, sustainability, and differentiated brand positioning. Major players such as Danone Asia, F&N Foods, and Coca-Cola Singapore dominate the landscape. Danone leads the premium segment through Evian and Volvic, supported by sustainability initiatives such as recycled PET and reusable packaging trials. F&N focuses on mass-market appeal with affordable natural and purified bottled water, alongside functional carbonated variants enhanced with vitamins and electrolytes. Coca-Cola competes through Dasani and Smartwater, leveraging advanced filtration, flavour innovation, and strong lifestyle-led marketing. New entrants such as BE WTR and Jääde are intensifying competition in the premium space by emphasising reusable packaging, circular models, and eco-conscious branding, raising sustainability expectations across the category.

Frequently Asked Questions

Related Report

1. Market Segmentation

1.1. Research Scope

1.2. Research Methodology

1.3. Definitions and Assumptions

2. Executive Summary

3. Singapore Bottled Water Market Policies, Regulations, and Standards

4. Singapore Bottled Water Market Dynamics

4.1. Growth Factors

4.2. Challenges

4.3. Trends

4.4. Opportunities

5. Singapore Bottled Water Market Statistics, 2022-2032F

5.1. Market Size & Growth Outlook

5.1.1.By Revenues in USD Million

5.1.2.By Volume (Million Litres)

5.2. Market Segmentation & Growth Outlook

5.2.1.By Type of Water

5.2.1.1. Carbonated Bottled Water- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2. Flavoured Bottled Water- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3. Functional Bottled Water- Market Insights and Forecast 2022-2032, USD Million

5.2.1.4. Still Bottled Water- Market Insights and Forecast 2022-2032, USD Million

5.2.2.By Sub Types

5.2.2.1. Purified- Market Insights and Forecast 2022-2032, USD Million

5.2.2.1.1. Desalinated- Market Insights and Forecast 2022-2032, USD Million

5.2.2.1.2. Atmospheric Generated- Market Insights and Forecast 2022-2032, USD Million

5.2.2.1.3. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.2.2. Mineral- Market Insights and Forecast 2022-2032, USD Million

5.2.2.3. Other (Spring, Alkaline, Other) - Market Insights and Forecast 2022-2032, USD Million

5.2.3.By Packaging Material

5.2.3.1. Flexible Packaging- Market Insights and Forecast 2022-2032, USD Million

5.2.3.1.1. Aluminium- Market Insights and Forecast 2022-2032, USD Million

5.2.3.1.2. Pouches- Market Insights and Forecast 2022-2032, USD Million

5.2.3.2. Glass- Market Insights and Forecast 2022-2032, USD Million

5.2.3.3. Rigid Plastic- Market Insights and Forecast 2022-2032, USD Million

5.2.3.3.1. PET Bottles- Market Insights and Forecast 2022-2032, USD Million

5.2.3.3.2. Thin Wall Plastic Containers- Market Insights and Forecast 2022-2032, USD Million

5.2.3.3.3. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.4.By Price Category

5.2.4.1. Budget- Market Insights and Forecast 2022-2032, USD Million

5.2.4.2. Economy- Market Insights and Forecast 2022-2032, USD Million

5.2.4.3. Premium- Market Insights and Forecast 2022-2032, USD Million

5.2.5.By Pack Size

5.2.5.1. 100 ml- Market Insights and Forecast 2022-2032, USD Million

5.2.5.2. 125 ml- Market Insights and Forecast 2022-2032, USD Million

5.2.5.3. 200 ml- Market Insights and Forecast 2022-2032, USD Million

5.2.5.4. 250 ml- Market Insights and Forecast 2022-2032, USD Million

5.2.5.5. 330 ml- Market Insights and Forecast 2022-2032, USD Million

5.2.5.6. 370 ml- Market Insights and Forecast 2022-2032, USD Million

5.2.5.7. 450 ml- Market Insights and Forecast 2022-2032, USD Million

5.2.5.8. 500 ml- Market Insights and Forecast 2022-2032, USD Million

5.2.5.9. 591 ml- Market Insights and Forecast 2022-2032, USD Million

5.2.5.10. 750 ml- Market Insights and Forecast 2022-2032, USD Million

5.2.5.11. 1,000 ml- Market Insights and Forecast 2022-2032, USD Million

5.2.5.12. 1,500 ml- Market Insights and Forecast 2022-2032, USD Million

5.2.5.13. 4,000 ml- Market Insights and Forecast 2022-2032, USD Million

5.2.5.14. 5,000 ml- Market Insights and Forecast 2022-2032, USD Million

5.2.5.15. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.6.By Sales Channel

5.2.6.1. On Trade- Market Insights and Forecast 2022-2032, USD Million

5.2.6.1.1. Restaurants- Market Insights and Forecast 2022-2032, USD Million

5.2.6.1.2. Hotels- Market Insights and Forecast 2022-2032, USD Million

5.2.6.1.3. Cafes- Market Insights and Forecast 2022-2032, USD Million

5.2.6.1.4. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.6.2. Off Trade- Market Insights and Forecast 2022-2032, USD Million

5.2.6.2.1. Grocery Retailers- Market Insights and Forecast 2022-2032, USD Million

5.2.6.2.1.1. Convenience Retail- Market Insights and Forecast 2022-2032, USD Million

5.2.6.2.1.2. Supermarkets- Market Insights and Forecast 2022-2032, USD Million

5.2.6.2.1.3. Hypermarkets- Market Insights and Forecast 2022-2032, USD Million

5.2.6.2.1.4. Small Local Grocer- Market Insights and Forecast 2022-2032, USD Million

5.2.6.2.2. Non-Grocery Retailers- Market Insights and Forecast 2022-2032, USD Million

5.2.6.2.2.1. General Merchandise Stores- Market Insights and Forecast 2022-2032, USD Million

5.2.6.2.3. Vending- Market Insights and Forecast 2022-2032, USD Million

5.2.6.2.4. E-commerce- Market Insights and Forecast 2022-2032, USD Million

5.2.7.By Competitors

5.2.7.1. Competition Characteristics

5.2.7.2. Market Share & Analysis

6. Singapore Carbonated Bottled Water Market Statistics, 2022-2032

6.1. Market Size & Growth Outlook

6.1.1.By Revenues in USD Million

6.1.2.By Volume (Million Litres)

6.2. Market Segmentation & Growth Outlook

6.2.1.By Sub Types- Market Insights and Forecast 2022-2032, USD Million

6.2.2.By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

6.2.3.By Pack Size- Market Insights and Forecast 2022-2032, USD Million

6.2.4.By Price Category- Market Insights and Forecast 2022-2032, USD Million

6.2.5.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

7. Singapore Flavoured Bottled Water Market Statistics, 2022-2032

7.1. Market Size & Growth Outlook

7.1.1.By Revenues in USD Million

7.1.2.By Volume (Million Litres)

7.2. Market Segmentation & Growth Outlook

7.2.1.By Sub Types- Market Insights and Forecast 2022-2032, USD Million

7.2.2.By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

7.2.3.By Pack Size- Market Insights and Forecast 2022-2032, USD Million

7.2.4.By Price Category- Market Insights and Forecast 2022-2032, USD Million

7.2.5.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

8. Singapore Functional Bottled Water Market Statistics, 2022-2032

8.1. Market Size & Growth Outlook

8.1.1.By Revenues in USD Million

8.1.2.By Volume (Million Litres)

8.2. Market Segmentation & Growth Outlook

8.2.1.By Sub Types- Market Insights and Forecast 2022-2032, USD Million

8.2.2.By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

8.2.3.By Pack Size- Market Insights and Forecast 2022-2032, USD Million

8.2.4.By Price Category- Market Insights and Forecast 2022-2032, USD Million

8.2.5.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

9. Singapore Still Bottled Water Market Statistics, 2022-2032

9.1. Market Size & Growth Outlook

9.1.1.By Revenues in USD Million

9.1.2.By Volume (Million Litres)

9.2. Market Segmentation & Growth Outlook

9.2.1.By Sub Types- Market Insights and Forecast 2022-2032, USD Million

9.2.2.By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

9.2.3.By Pack Size- Market Insights and Forecast 2022-2032, USD Million

9.2.4.By Price Category- Market Insights and Forecast 2022-2032, USD Million

9.2.5.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

10. Competitive Outlook

10.1. Company Profiles

10.1.1. Danone Asia Holdings Pte Ltd

10.1.1.1. Business Description

10.1.1.2. Product Portfolio

10.1.1.3. Collaborations & Alliances

10.1.1.4. Recent Developments

10.1.1.5. Financial Details

10.1.1.6. Others

10.1.2. F&N Foods (S) Pte Ltd

10.1.2.1. Business Description

10.1.2.2. Product Portfolio

10.1.2.3. Collaborations & Alliances

10.1.2.4. Recent Developments

10.1.2.5. Financial Details

10.1.2.6. Others

10.1.3. Coca-Cola Singapore Beverages Pte Ltd

10.1.3.1. Business Description

10.1.3.2. Product Portfolio

10.1.3.3. Collaborations & Alliances

10.1.3.4. Recent Developments

10.1.3.5. Financial Details

10.1.3.6. Others

10.1.4. Nestlé Singapore Pte Ltd

10.1.4.1. Business Description

10.1.4.2. Product Portfolio

10.1.4.3. Collaborations & Alliances

10.1.4.4. Recent Developments

10.1.4.5. Financial Details

10.1.4.6. Others

10.1.5. Yeo Hiap Seng Ltd

10.1.5.1. Business Description

10.1.5.2. Product Portfolio

10.1.5.3. Collaborations & Alliances

10.1.5.4. Recent Developments

10.1.5.5. Financial Details

10.1.5.6. Others

10.1.6. Yee Lee Oils & Foodstuffs (S) Pte Ltd

10.1.6.1. Business Description

10.1.6.2. Product Portfolio

10.1.6.3. Collaborations & Alliances

10.1.6.4. Recent Developments

10.1.6.5. Financial Details

10.1.6.6. Others

10.1.7. Otsuka Pharmaceutical Pte Ltd

10.1.7.1. Business Description

10.1.7.2. Product Portfolio

10.1.7.3. Collaborations & Alliances

10.1.7.4. Recent Developments

10.1.7.5. Financial Details

10.1.7.6. Others

10.1.8. NTUC FairPrice Co-operative Pte Ltd

10.1.8.1. Business Description

10.1.8.2. Product Portfolio

10.1.8.3. Collaborations & Alliances

10.1.8.4. Recent Developments

10.1.8.5. Financial Details

10.1.8.6. Others

11. Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Type of Water |

|

| By Sub Types |

|

| By Packaging Material |

|

| By Price Category |

|

| By Pack Size |

|

| By Sales Channel |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.