Philippines Menstrual Care Market Report: Trends, Growth and Forecast (2026-2032)

Product Type (Pantyliners, Tampons (Applicator Tampons, Digital Tampons), Towels (Standard Towels (Standard Towels with Wings, Standard Towels Without Wings), Slim/Thin/Ultra-Thin Towels (Slim/Thin/Ultra-Thin Towels with Wings, Slim/Thin/Ultra-Thin Towels Without Wings)), Intimate Wipes, Menstrual Cups, Period Underwear), Nature (Disposable, Reusable), Age Group (Up to 18 Years, 19-30 Years, 31-40 Years, 40 Years and Above), Sales Channel (Retail Offline, Retail Online) ... Read more

|

Major Players

|

Philippines Menstrual Care Market Statistics and Insights, 2026

- Market Size Statistics

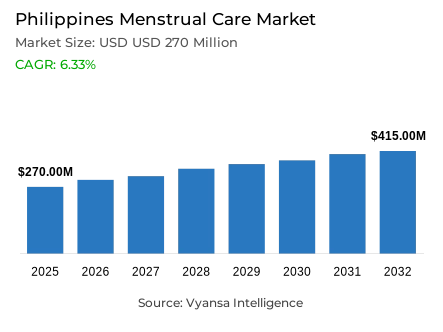

- Menstrual care in Philippines is estimated at USD 270 million in 2025.

- The market size is expected to grow to USD 415 million by 2032.

- Market to register a cagr of around 6.33% during 2026-32.

- Product Type Shares

- Towels grabbed market share of 80%.

- Competition

- More than 5 companies are actively engaged in producing menstrual care in Philippines.

- Top 5 companies acquired around 85% of the market share.

- JS Unitrade Merchandise Inc; Mega Soft Hygienic Products Inc; Kimberly-Clark Philippines Inc; Johnson & Johnson (Philippines) Inc; Procter & Gamble Philippines Inc etc., are few of the top companies.

- Sales Channel

- Retail offline grabbed 90% of the market.

Philippines Menstrual Care Market Outlook

The Philippines menstrual care market is expected to show a strong growth with a market valuation of USD 270 million in 2025 to about USD 415 million in 2032; this is a high compound annual growth rate of about 6.33% in the forecast period of 2026-2032.Towels, which control about 80% of the market share, will continue to be the biggest and most vibrant type of product, driven by their popularity, low cost, and ease of operation. The further increase in growth rates will be supported by the further reentry of women into physical working conditions and the rise in social-activity engagement, which will stimulate more frequent replenishment of menstrual product stocks.

The positioning of pantyliners is to ensure a consistent growth over the forecast period, which is driven by the increasing use of pantyliners by younger female groups and the aging population in need of light incontinence products. Their versatility makes them more relevant than the conventional use of these products in menstrual contexts, and social-media platforms and education campaigns keep raising awareness about the importance of proper menstrual-hygiene practices. In the meantime, new menstrual products, such as period underwear, menstrual cups, and disc designs, will find a market presence, especially in the segments of the market that are environmentally aware and urban end user, thus providing a chance to innovate and expand into a niche market.

The distribution-infrastructure environment is dominated by retail offline channels, which contribute almost 90% of the sales volume. The main points of purchase are still supermarket formats, drugstore establishments, and smaller local grocery operations, which are backed by convenience attributes, product variety, and competitive pricing structures. retail online platforms, with a smaller market-share percentage, are also growing steadily as online platforms, such as Shopee and Lazada, offer bundle promotional deals, flash-sale deals, and subscriptions, which are attractive to price-sensitive and time-conscious end user groups, especially when it comes to bulk-buying transactions.

The innovation projects during the forecast period will focus on comfort optimisation, quality improvement, and integration of sustainability. Brand entities are anticipated to increase product-line collections, employing soft, breathable fabric structures, seamless design frameworks, and biodegradable material structures to fulfill local end user preference trends. Educational programs and marketing campaigns will remain playing critical roles in creating awareness, enhancing the acceptance of modern menstrual products, and promoting the use of sustainable solutions. This changing market environment will enhance the competitive forces, product differentiation and long-term growth of the Philippine menstrual-care market.

Philippines Menstrual Care Market Growth Driver

Returning Workforce and Awareness Programs Boost Demand

Rising female workforce participation and stronger menstrual hygiene education initiatives are driving sustained growth in menstrual care demand in the Philippines. According to recent statistics provided by the Philippine Statistics Authority (PSA) and the International Labour Organization (ILO), the female labour-force participation is estimated to be 49.8 to 50.2% in 2024, which implies that there is a significant number of economically active women who buy menstrual care products on a regular basis. The Department of Education and UNICEF are still incorporating Comprehensive Sexuality Education (CSE) into school curriculum systems, thus enhancing the level of knowledge among adolescent girls on puberty, reproductive health, and menstrual hygiene management. These governmental efforts are supplemented by educational campaigns conducted by brand organizations, such as Kotex and Johnson & Johnson, which strengthen the awareness creation and product-acceptance curves.

retail online websites like Shopee and Lazada are significant in providing convenient procurement avenues to a wide range of menstrual care product portfolios. Their convenient online shopping services cater to the urban and rural end user segments, increase product availability, and maintain continuity in demand. All these efforts drive the development of the market by normalizing menstrual care discourse and encouraging healthy hygiene practices in the country.

Philippines Menstrual Care Market Challenge

Cultural Norms and Limited Adoption of Modern Products

The use of tampons and reusable menstrual product options is still limited by cultural taboos and lack of information. According to UNICEF research results, a significant number of adolescent groups learn about menstruation informally; about 30% of the population still does not have full menstrual health education, which restricts the acceptance of new product offerings. The health issues that are related to the use of tampons, especially the fear of toxic shock syndrome as reported by the World Health Organization in the developing economies of Asia, are some of the factors that have led to a consistent inclination towards disposable pad products.

These behavioural barriers are compounded by economic factors. Hygiene-related items inflation was at about 6.7% in 2024, as per the Bangko Sentral ng Pilipinas data, which decreased end user purchasing power and limited access to higher-level or reusable menstrual products. Such socio-economic and cultural issues hinder the portfolio diversification and long-term market-growth prospects, especially in rural and lower-income demographic groups.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Philippines Menstrual Care Market Trend

Growing Preference for Sustainable and Comfort-Focused Products

The end user favour of premium and sustainable menstrual care products is on the rise, especially in the middle- and higher-income end user segments in urban geographic regions. According to the Department of Environment and Natural Resources (DENR), there is growing interest in biodegradable formulations, organic cotton compositions, and reusable product alternatives. The social media sites play critical roles in encouraging the adoption of eco-friendly lifestyles. Innovations, such as antimicrobial and moisture-wicking period underwear, improve comfort and hygiene features, thus creating a new niche market segment based on wellness optimisation.

The shift to sustainability is also observed in the increasing demand of end user to purchase products that have minimal environmental impact without affecting the quality performance. The retail online platforms and direct-to-end user distribution models will help to provide wider access to these innovative product offerings, particularly to younger demographic groups that appreciate the comfort features and environmental sustainability.

Philippines Menstrual Care Market Opportunity

Modern Menstrual Products to Gain Traction

Low penetration of tampons, menstrual cups, and period underwear indicates substantial scope for future expansion within the Philippines feminine hygiene market.. Legislative efforts suggest the improvement of comprehensive sexuality education systems, which would cover about 27 million school-going children, thus creating a better understanding and acceptance of modern menstrual products, as per the 2023 Philippine Statistics Authority data. Corporate-based educational campaigns such as Johnson 2012 and Kimberly-Clark Philippines are designed to increase product-profile awareness and adoption of usage.

Product-customisation approaches, including different tampon size options and convenient applicator designs at affordable prices, will be essential elements of entering different demographic groups. Together with digital marketing campaigns and social outreach programmes, these strategic plans provide a strong base of future development in this large and dynamic market environment.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Philippines Menstrual Care Market Segmentation Analysis

By Product Type

- Pantyliners

- Tampons

- Towels

- Intimate Wipes

- Menstrual Cups

- Period Underwear

Towels constitute the dominant segment within the product type categorization, commanding approximately 80% of the Philippines menstrual care market share. Towels maintain their position as the most extensively utilized product attributable to their convenience, reliability, and broad appeal across diverse age demographic groups. Their dominance is reinforced through strong brand recognition equity, including established market participants such as Kotex and Johnson & Johnson's Carefree, alongside private label alternatives delivering affordable and accessible product options. Slim, thin, and ultra-thin towel variant configurations are experiencing increasing popularity, offering comfort attributes, discreteness characteristics, and improved absorbency performance, aligning with daily requirements and lifestyle preferences of local end-user populations.

Despite the emergence of modern menstrual products including menstrual cups, period underwear, and tampons, disposable towels continue to sustain their leadership positioning. Their convenience attributes, comprehensive availability, and continued end user trust ensure robust volume and value sales performance. Manufacturers are additionally pursuing innovation trajectories incorporating sustainable materials and premium design architectures to appeal to environmentally conscious and quality-focused end user segments, supporting the segment's ongoing growth momentum.

By Sales Channel

- Retail Offline

- Retail Online

Retail offline channels maintain dominant positioning within the sales channel segmentation, representing approximately 90% of the Philippines menstrual care market. Supermarket formats, drugstore establishments, and health and beauty retail outlets dominate this distribution channel, offering comprehensive product range portfolios, promotional pricing initiatives, and immediate product availability, which remain critical determinants for Filipino end user demographics. retail offline infrastructure continues to benefit from high visibility of established brand entities including Kotex and Carefree, attracting end-user populations who demonstrate preference for physical product comparison capabilities and access to trusted product alternatives.

While retail online channels are experiencing expansion trajectories, particularly for modern menstrual product categories, retail offline distribution continues to function as the preferred procurement channel attributable to its accessibility, convenience, and cost-effectiveness attributes. Supermarket and drugstore formats have strengthened their competitive positioning through offering bundle pack configurations, discount pricing structures, and private label options, catering to price-sensitive household demographics. These strategic initiatives reinforce the dominance of offline distribution channels, ensuring that retail infrastructure remains the primary distribution methodology for menstrual care products throughout the forecast period.

List of Companies Covered in Philippines Menstrual Care Market

The companies listed below are highly influential in the Philippines menstrual care market, with a significant market share and a strong impact on industry developments.

- JS Unitrade Merchandise Inc

- Mega Soft Hygienic Products Inc

- Kimberly-Clark Philippines Inc

- Johnson & Johnson (Philippines) Inc

- Procter & Gamble Philippines Inc

- Winalite International Inc

Competitive Landscape

Established players such as Johnson & Johnson (Carefree) and Kimberly-Clark Philippines (Kotex) maintained strong positions through brand recognition, marketing initiatives, and educational campaigns on menstrual health. Kotex leveraged events like #FlexYourMood and campus outreach to strengthen consumer engagement, while Johnson & Johnson focused on product trust and consistent quality. Emerging brands, particularly in period underwear, tapped niche segments through online direct-to-consumer models, appealing to younger and environmentally conscious consumers. E-commerce platforms such as Shopee and Lazada further intensified competition by offering promotions, bundle deals, and convenient delivery, challenging traditional retail channels and reshaping the market’s competitive dynamics.

Frequently Asked Questions

Related Report

1. Market Segmentation

1.1. Research Scope

1.2. Research Methodology

1.3. Definitions and Assumptions

2. Executive Summary

3. Philippines Menstrual Care Market Policies, Regulations, and Standards

4. Philippines Menstrual Care Market Dynamics

4.1. Growth Factors

4.2. Challenges

4.3. Trends

4.4. Opportunities

5. Philippines Menstrual Care Market Statistics, 2022-2032F

5.1. Market Size & Growth Outlook

5.1.1.By Revenues in USD Million

5.2. Market Segmentation & Growth Outlook

5.2.1.By Product Type

5.2.1.1. Pantyliners- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2. Tampons- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.1. Applicator Tampons- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.2. Digital Tampons- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3. Towels- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3.1. Standard Towels- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3.1.1. Standard Towels with Wings- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3.1.2. Standard Towels Without Wings- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3.2. Slim/Thin/Ultra-Thin Towels- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3.2.1. Slim/Thin/Ultra-Thin Towels with Wings- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3.2.2. Slim/Thin/Ultra-Thin Towels Without Wings- Market Insights and Forecast 2022-2032, USD Million

5.2.1.4. Intimate Wipes- Market Insights and Forecast 2022-2032, USD Million

5.2.1.5. Menstrual Cups- Market Insights and Forecast 2022-2032, USD Million

5.2.1.6. Period Underwear- Market Insights and Forecast 2022-2032, USD Million

5.2.2.By Nature

5.2.2.1. Disposable- Market Insights and Forecast 2022-2032, USD Million

5.2.2.2. Reusable- Market Insights and Forecast 2022-2032, USD Million

5.2.3.By Age Group

5.2.3.1. Up to 18 Years- Market Insights and Forecast 2022-2032, USD Million

5.2.3.2. 19-30 Years- Market Insights and Forecast 2022-2032, USD Million

5.2.3.3. 31-40 Years- Market Insights and Forecast 2022-2032, USD Million

5.2.3.4. 40 Years and Above- Market Insights and Forecast 2022-2032, USD Million

5.2.4.By Sales Channel

5.2.4.1. Retail Offline- Market Insights and Forecast 2022-2032, USD Million

5.2.4.2. Retail Online- Market Insights and Forecast 2022-2032, USD Million

5.2.5.By Competitors

5.2.5.1. Competition Characteristics

5.2.5.2. Market Share & Analysis

6. Philippines Pantyliners Menstrual Care Market Statistics, 2022-2032

6.1. Market Size & Growth Outlook

6.1.1.By Revenues in USD Million

6.2. Market Segmentation & Growth Outlook

6.2.1.By Nature- Market Insights and Forecast 2022-2032, USD Million

6.2.2.By Age Group- Market Insights and Forecast 2022-2032, USD Million

6.2.3.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

7. Philippines Tampons Menstrual Care Market Statistics, 2022-2032

7.1. Market Size & Growth Outlook

7.1.1.By Revenues in USD Million

7.2. Market Segmentation & Growth Outlook

7.2.1.By Product Type- Market Insights and Forecast 2022-2032, USD Million

7.2.2.By Nature- Market Insights and Forecast 2022-2032, USD Million

7.2.3.By Age Group- Market Insights and Forecast 2022-2032, USD Million

7.2.4.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

8. Philippines Towels Menstrual Care Market Statistics, 2022-2032

8.1. Market Size & Growth Outlook

8.1.1.By Revenues in USD Million

8.2. Market Segmentation & Growth Outlook

8.2.1.By Product Type- Market Insights and Forecast 2022-2032, USD Million

8.2.2.By Nature- Market Insights and Forecast 2022-2032, USD Million

8.2.3.By Age Group- Market Insights and Forecast 2022-2032, USD Million

8.2.4.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

9. Philippines Intimate Wipes Market Statistics, 2022-2032

9.1. Market Size & Growth Outlook

9.1.1.By Revenues in USD Million

9.2. Market Segmentation & Growth Outlook

9.2.1.By Nature- Market Insights and Forecast 2022-2032, USD Million

9.2.2.By Age Group- Market Insights and Forecast 2022-2032, USD Million

9.2.3.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

10. Philippines Menstrual Cups Menstrual Care Market Statistics, 2022-2032

10.1. Market Size & Growth Outlook

10.1.1. By Revenues in USD Million

10.2. Market Segmentation & Growth Outlook

10.2.1. By Nature- Market Insights and Forecast 2022-2032, USD Million

10.2.2. By Age Group- Market Insights and Forecast 2022-2032, USD Million

10.2.3. By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

11. Philippines Period Underwear Menstrual Care Market Statistics, 2022-2032

11.1. Market Size & Growth Outlook

11.1.1. By Revenues in USD Million

11.2. Market Segmentation & Growth Outlook

11.2.1. By Nature- Market Insights and Forecast 2022-2032, USD Million

11.2.2. By Age Group- Market Insights and Forecast 2022-2032, USD Million

11.2.3. By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

12. Competitive Outlook

12.1. Company Profiles

12.1.1. Johnson & Johnson (Philippines) Inc

12.1.1.1. Business Description

12.1.1.2. Product Portfolio

12.1.1.3. Collaborations & Alliances

12.1.1.4. Recent Developments

12.1.1.5. Financial Details

12.1.1.6. Others

12.1.2. Procter & Gamble Philippines Inc

12.1.2.1. Business Description

12.1.2.2. Product Portfolio

12.1.2.3. Collaborations & Alliances

12.1.2.4. Recent Developments

12.1.2.5. Financial Details

12.1.2.6. Others

12.1.3. JS Unitrade Merchandise Inc

12.1.3.1. Business Description

12.1.3.2. Product Portfolio

12.1.3.3. Collaborations & Alliances

12.1.3.4. Recent Developments

12.1.3.5. Financial Details

12.1.3.6. Others

12.1.4. Mega Soft Hygienic Products Inc

12.1.4.1. Business Description

12.1.4.2. Product Portfolio

12.1.4.3. Collaborations & Alliances

12.1.4.4. Recent Developments

12.1.4.5. Financial Details

12.1.4.6. Others

12.1.5. Kimberly-Clark Philippines Inc

12.1.5.1. Business Description

12.1.5.2. Product Portfolio

12.1.5.3. Collaborations & Alliances

12.1.5.4. Recent Developments

12.1.5.5. Financial Details

12.1.5.6. Others

12.1.6. Winalite International Inc

12.1.6.1. Business Description

12.1.6.2. Product Portfolio

12.1.6.3. Collaborations & Alliances

12.1.6.4. Recent Developments

12.1.6.5. Financial Details

12.1.6.6. Others

13. Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Product Type |

|

| By Nature |

|

| By Age Group |

|

| By Sales Channel |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.