North America Industrial Water & Wastewater Pump Market Report: Trends, Growth and Forecast (2026-2032)

By Pump Type (Centrifugal Pumps (End Suction, Split Case, Vertical (Turbine, Axial Pump, Mixed Flow Pump), Submersible Pump), Positive Displacement Pumps (Progressing Cavity, Diaphragm, Gear Pump, Others)), By Application (Water, Wastewater), By Country (US, Canada, Mexico, Rest of North America) ... Read more

|

Major Players

|

North America Industrial Water & Wastewater Pump Market Statistics and Insights, 2026

- Market Size Statistics

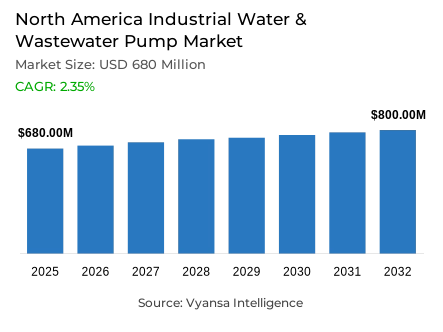

- North America industrial water & wastewater pump market is estimated at USD 680 million in 2025.

- The market size is expected to grow to USD 800 million by 2032.

- Market to register a cagr of around 2.35% during 2026-32.

- Pump Type Shares

- Centrifugal pumps grabbed market share of 85%.

- Competition

- More than 10 companies are actively engaged in producing industrial water & wastewater pump in North America.

- Top 5 companies acquired around 60% of the market share.

- Gorman-Rupp Pumps; Sulzer Ltd.; KSB SE & Co. KGaA; Flowserve Corporation; Xylem Inc. etc., are few of the top companies.

- Application

- Water grabbed 55% of the market.

- Country

- US leads with a 90% share of the North America market.

North America Industrial Water & Wastewater Pump Market Outlook

Valued at approximately USD 680 million in 2025, the regional market is expected to observe a smooth growth trajectory towards reaching close to USD 800 million by 2032, registering a CAGR of approximately 2.35% from 2026-2032. The key growth drivers responsible for this momentum rest in the current age of the existing water and wastewater infrastructure commissioned in the mid-20th century. With approximately 260,000 annual breaks of the US water mains and a rating of C- for drinking water and D+ for wastewater, the need for pump replacements is directly contributing to growth.

There is continued public investment in this vision. Funding under the Bipartisan Infrastructure Law has committed USD 48 billion to address water, wastewater, and stormwater infrastructure through 2026, of which USD 36.9 billion has been appropriated. This level of expenditure focuses on upgrading treatment plant capacity, replacement of lead service lines, and infrastructure upgrades, each of which necessitates replacement or upgrade of pumps. This has led to acquiring pumps being recognized not just as an optional expenditure but also an infrastructural necessity.

There are also increased operational demands brought about by more stringent discharge and drinking water regulations. There are now much tougher limits for biochemical oxygen demand and total suspended solids. Additionally, there are now emerging PFAS regulation limits set at 4 parts-per-trillion levels. These demands are challenging infrastructure capabilities, thus promoting the adoption of efficient pumping technology by end users. The integration of digital technology also enhances demand. There are now significant efficiency gains of 25 to 30 percent by using high-efficiency centrifugal pumps driven by state-of-the-art motors.

Centrifugal Pumps currently occupy the leading market share of 85% within the type segmentation due to their ability to be used continuously. In relation to applications, Water Treatment/Distribution segments the market with the largest share at 55% due to the steady level of application at every phase, starting from abstraction right through to distribution. On the other hand, the United States presently drives the market with a share of around 90% within the geographic segmentation.

North America Industrial Water & Wastewater Pump Market Growth Driver

Infrastructure Renewal Driving Capital Equipment Replacement

Aging infrastructure that dates back to the mid-20th century is contributing to sustained pressure on the industrial water & wastewater pumps market across North America. There are some 260,000 water main breaks that occur each year in this region, indicative of widespread aging infrastructure of a distribution or collecting pipeline. Infrastructure rating analysis further reinforces this challenge, with a rating of C- for water systems and a rating of D+ for wastewater systems, a consequence of many years of deferred maintenance. There is accordingly a sustained need for new pumps that can serve a higher hydraulic head, continuous operation, and increased capacity on systems that have undergone maintenance and modernization.

Federal government funding has driven the replacement process, with a total of USD 48 billion committed to water, wastewater, and stormwater infrastructure through the Bipartisan Infrastructure Law through 2026. Of that, a figure of USD 36.9 billion has been appropriated, addressing lead service line replacements, plant upgrades, and distribution system upgrades. With each of the investment programs, significant replacement or upgrades to pumps must take place, solidifying the demand for pumps as part of the infrastructure process.

North America Industrial Water & Wastewater Pump Market Challenge

Regulatory Stringency Increasing Operational Complexity

Stricter discharge and water treatment standards are reshaping the operating needs of the North America industrial water and wastewater pump installations. New discharge standards call for restrictions on biochemical oxygen demand and total suspended solids to ≤ 30 mg/L with a minimum 85% removal rate, and this is placing old pumping equipment under stress that was not designed to handle this type of precise water control, making it necessary for end users to reevaluate pump reliability and redundancy.

The regulatory driving force is being strengthened further by the newer contaminants regulations, especially for PFAS. The maximum contaminant levels for the contaminants PFOA & PFOS have been set at 4 parts per trillion, among the stringent levels in the world, with the deadline for compliance stretching up to 2031. Already, the uncertainty with the biosolids program and PFAS residuals compounds is adding to the long-term operating cost burden for pump stations.

Unlock Market Intelligence

Explore the market potential with our data-driven report

North America Industrial Water & Wastewater Pump Market Trend

Digital Monitoring and Automation Redefining Efficiency Benchmarks

Digital integration is increasing at a fast pace in the North America market for the operations of water & wastewater pumps within industry. Analysis on the performance aspect shows that high-efficiency centrifugal pumps deliver a saving in power by as much as 25-30% when compared with conventional industry pumps. Such levels of savings have become increasingly more important as a result of rising costs for energy and a constrained budget for utilities.

The adoption of advanced analytics is also moving in lockstep with the installation of sensors, with less than 24% of large municipal utilities in the US currently employing AI, but three-quarters of the respondents indicate plans to employ AI solutions within the next five years. The current use of IoT sensors has made continuous monitoring of flow, pressure, and water quality parameters possible, moving away from the conventional practice of taking manual samples on occasion. Plants using automated control systems indicate better compliance, lower chemical consumption, and extended asset life.

North America Industrial Water & Wastewater Pump Market Opportunity

Water Scarcity Elevating Reliability Investment Priorities

Structural water scarcity is driving strong long-term demand fundamentals in the industrial water & wastewater pumps market in North America. Forty out of fifty US states'water managers predict that there will be shortages even in average hydrological conditions. This trend holds true in current market conditions as well, as 40.52% of the lower 48 states in the US are experiencing drought conditions as of December 2025.

The situation is exacerbated by industrial operations, as industries withdraw over 18.2 billion gallons of water per day through manufacturing plants, especially those dealing with steel, chemicals, and petroleum products located in areas with scarce water resources. Although industries with state-of-the-art pumping systems face reduced interruptions during water shortages, as well as better cost management with rising water sourcing costs, a new normal characterized by water scarcity will increasingly see pumping infrastructure as a risk management strategy.

North America Industrial Water & Wastewater Pump Market Country Analysis

By Country

- US

- Canada

- Mexico

- Rest of North America

Geographic distribution within North America industrial water & wastewater pump market is heavily concentrated in the United States, which accounts for 90% of total regional demand. This dominance reflects the scale of municipal water infrastructure, high industrial water consumption, and stringent regulatory frameworks that shape pump specifications. Federal infrastructure programs directing tens of billions of dollars toward U.S. water systems further reinforce domestic demand momentum.

Canada and Mexico collectively represent the remaining 10% share of regional demand. Canadian growth is stronger in western provinces where water availability constraints and infrastructure renewal drive efficiency investments, while Mexican demand remains concentrated in export-oriented manufacturing hubs and major metropolitan utilities. Differences in capital intensity, regulatory enforcement, and industrial concentration underpin this distribution, with U.S. leadership expected to persist through 2026-2032.

Unlock Market Intelligence

Explore the market potential with our data-driven report

North America Industrial Water & Wastewater Pump Market Segmentation Analysis

By Pump Type

- Centrifugal Pumps

- End Suction

- Split Case

- Vertical

- Turbine

- Axial Pump

- Mixed Flow Pump

- Submersible Pump

- Positive Displacement Pumps

- Progressing Cavity

- Diaphragm

- Gear Pump

- Others

Pump type segmentation within North America industrial water & wastewater pump market is decisively led by centrifugal pumps, which account for 85% of total market share. Their dominance stems from suitability for high-volume continuous operation, compatibility with municipal treatment design standards, and predictable maintenance profiles. Single-stage centrifugal pumps dominate intake, distribution, and recirculation applications, while multistage designs support high-pressure requirements in membrane filtration and advanced treatment processes.

Positive displacement and other specialized pumps collectively represent the remaining 15% market share, serving niche applications requiring precise flow control or viscous material handling. These include sludge transfer, biosolids processing, and specialized industrial applications where centrifugal designs face operational limitations. Despite their importance in specific processes, limited scalability and higher maintenance complexity restrict broader adoption, reinforcing centrifugal technology as the structural backbone of regional pump demand.

By Application

- Water

- Wastewater

Application segmentation shows water treatment and distribution accounting for 55% of total demand across North America industrial water & wastewater pump market deployments. Pumps are essential across raw water abstraction, clarification circulation, filtration feed, and finished water distribution, creating consistent demand across multiple stages within individual facilities. Industrial process water systems further strengthen this segment, particularly in cooling, production, and auxiliary operations located in water-constrained regions.

Wastewater collection and treatment comprise the remaining 45% of market demand, spanning influent pumping, aeration basin circulation, sludge handling, and effluent discharge. These applications impose variable hydraulic and solids-handling requirements, driving selective adoption of specialized designs alongside centrifugal pumps. The balanced split between water and wastewater applications diversifies revenue streams while preserving centrifugal dominance across both end-use categories.

Various Market Players in North America Industrial Water & Wastewater Pump Market

The companies mentioned below are highly active in the North America industrial water & wastewater pump market, occupying a considerable portion of the market and shaping industry progress.

- Gorman-Rupp Pumps

- Sulzer Ltd.

- KSB SE & Co. KGaA

- Flowserve Corporation

- Xylem Inc.

- ITT Inc.

- Pentair plc

- Grundfos Holding A/S

- Wilo SE

- EBARA International Corporation

Market News & Updates

- Flowserve Corporation, 2025:

Flowserve received official U.S. Department of Energy approval under 10 CFR Part 810 to manufacture safety-critical nuclear primary coolant pumps at its Coimbatore, India facility in partnership with Core Energy Systems Limited and India's Nuclear Power Corporation, marking the first-ever U.S. authorization for Indian collaboration of this scope in civilian nuclear reactor equipment manufacturing. Additionally, Flowserve demonstrated strong North America performance in 2025 with power sector bookings surging 23% year-over-year in Q3 2025, including $140 million in nuclear contracts awarded during the quarter, reflecting robust demand for advanced flow control solutions in the nuclear and power sectors.

- Xylem Inc., 2025:

Xylem delivered outstanding 2025 performance across North America with Q3 revenue growth of 7.8% year-over-year to $2.27 billion, driven by robust demand in smart metering, water infrastructure, and industrial applications, while raising full-year 2025 revenue guidance to $9 billion. The company's strategic focus on margin expansion, evidenced by an adjusted EBITDA margin improvement to 23.2% (up 200 basis points year-over-year), reflects operational excellence and successful implementation of its 80/20 resource allocation strategy, positioning Xylem as a leading provider of water infrastructure solutions and industrial pump technologies in the North American market.

Frequently Asked Questions

Related Report

1. Market Segmentation

1.1. Research Scope

1.2. Research Methodology

1.3. Definitions and Assumptions

2. Executive Summary

3. North America Industrial Water & Wastewater Pump Market Policies, Regulations, and Standards

4. North America Industrial Water & Wastewater Pump Market Dynamics

4.1. Growth Factors

4.2. Challenges

4.3. Trends

4.4. Opportunities

5. North America Industrial Water & Wastewater Pump Market Statistics, 2022-2032F

5.1. Market Size & Growth Outlook

5.1.1.By Revenues in USD Million

5.1.2.By Units Sold (Million Units)

5.2. Market Segmentation & Growth Outlook

5.2.1.By Pump Type

5.2.1.1. Centrifugal Pumps- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.1. End Suction- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.2. Split Case- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.3. Vertical- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.3.1. Turbine- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.3.2. Axial Pump- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.3.3. Mixed Flow Pump- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.4. Submersible Pump- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2. Positive Displacement Pumps- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.1. Progressing Cavity- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.2. Diaphragm- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.3. Gear Pump- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.4. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.2.By Application

5.2.2.1. Water- Market Insights and Forecast 2022-2032, USD Million

5.2.2.2. Wastewater- Market Insights and Forecast 2022-2032, USD Million

5.2.3.By Country

5.2.3.1. US

5.2.3.2. Canada

5.2.3.3. Mexico

5.2.3.4. Rest of North America

5.2.4.By Competitors

5.2.4.1. Competition Characteristics

5.2.4.2. Market Share & Analysis

6. US Industrial Water & Wastewater Pump Market Statistics, 2022-2032F

6.1. Market Size & Growth Outlook

6.1.1.By Revenues in USD Million

6.1.2.By Units Sold (Million Units)

6.2. Market Segmentation & Growth Outlook

6.2.1.By Pump Type- Market Insights and Forecast 2022-2032, USD Million

6.2.2.By Application - Market Insights and Forecast 2022-2032, USD Million

7. Canada Industrial Water & Wastewater Pump Market Statistics, 2022-2032F

7.1. Market Size & Growth Outlook

7.1.1.By Revenues in USD Million

7.1.2.By Units Sold (Million Units)

7.2. Market Segmentation & Growth Outlook

7.2.1.By Pump Type- Market Insights and Forecast 2022-2032, USD Million

7.2.2.By Application - Market Insights and Forecast 2022-2032, USD Million

8. Mexico Industrial Water & Wastewater Pump Market Statistics, 2022-2032F

8.1. Market Size & Growth Outlook

8.1.1.By Revenues in USD Million

8.1.2.By Units Sold (Million Units)

8.2. Market Segmentation & Growth Outlook

8.2.1.By Pump Type- Market Insights and Forecast 2022-2032, USD Million

8.2.2.By Application - Market Insights and Forecast 2022-2032, USD Million

9. Competitive Outlook

9.1. Company Profiles

9.1.1.Flowserve Corporation

9.1.1.1. Business Description

9.1.1.2. Product Portfolio

9.1.1.3. Collaborations & Alliances

9.1.1.4. Recent Developments

9.1.1.5. Financial Details

9.1.1.6. Others

9.1.2.Xylem Inc.

9.1.2.1. Business Description

9.1.2.2. Product Portfolio

9.1.2.3. Collaborations & Alliances

9.1.2.4. Recent Developments

9.1.2.5. Financial Details

9.1.2.6. Others

9.1.3.ITT Inc.

9.1.3.1. Business Description

9.1.3.2. Product Portfolio

9.1.3.3. Collaborations & Alliances

9.1.3.4. Recent Developments

9.1.3.5. Financial Details

9.1.3.6. Others

9.1.4.Pentair plc

9.1.4.1. Business Description

9.1.4.2. Product Portfolio

9.1.4.3. Collaborations & Alliances

9.1.4.4. Recent Developments

9.1.4.5. Financial Details

9.1.4.6. Others

9.1.5.Grundfos Holding A/S

9.1.5.1. Business Description

9.1.5.2. Product Portfolio

9.1.5.3. Collaborations & Alliances

9.1.5.4. Recent Developments

9.1.5.5. Financial Details

9.1.5.6. Others

9.1.6.Gorman-Rupp Pumps

9.1.6.1. Business Description

9.1.6.2. Product Portfolio

9.1.6.3. Collaborations & Alliances

9.1.6.4. Recent Developments

9.1.6.5. Financial Details

9.1.6.6. Others

9.1.7.Sulzer Ltd.

9.1.7.1. Business Description

9.1.7.2. Product Portfolio

9.1.7.3. Collaborations & Alliances

9.1.7.4. Recent Developments

9.1.7.5. Financial Details

9.1.7.6. Others

9.1.8.KSB SE & Co. KGaA

9.1.8.1. Business Description

9.1.8.2. Product Portfolio

9.1.8.3. Collaborations & Alliances

9.1.8.4. Recent Developments

9.1.8.5. Financial Details

9.1.8.6. Others

9.1.9.Wilo SE

9.1.9.1. Business Description

9.1.9.2. Product Portfolio

9.1.9.3. Collaborations & Alliances

9.1.9.4. Recent Developments

9.1.9.5. Financial Details

9.1.9.6. Others

9.1.10. EBARA International Corporation

9.1.10.1. Business Description

9.1.10.2. Product Portfolio

9.1.10.3. Collaborations & Alliances

9.1.10.4. Recent Developments

9.1.10.5. Financial Details

9.1.10.6. Others

10. Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Pump Type |

|

| By Application |

|

| By Country |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.